Korean Crypto Accounting Guideline - What Are the Opportunities?

Key points and regulators' intentions

TL;DR

The emergence of virtual assets has made it difficult to value them using existing accounting standards, causing confusion for investors. On December 20, 2023, the Korean regulatory authorities released the 'Guidelines for Supervision of Accounting for Virtual Assets', which states that "virtual assets should be evaluated and disclosed with transparent and strict standards like traditional assets".

The Supervisory Guidance aims to promote transparent accounting for virtual assets by clarifying 1) revenue recognition after completion of performance obligations outlined in the whitepaper, 2) the inability to recognize reserved tokens as assets, 3) enhanced disclosures in the notes, and 4) accounting judgment criteria based on economic control of exchange customer deposits.

The new accounting standards are expected to bring some improvements in market transparency. However, a successful transition will require increased auditing, consulting, and training for companies, and international cooperation to ensure global harmonization.

1. Accounting, the standard for determining the health of a company

"Accounting is the language of business" is a phrase that resonates deeply within the corporate world, owing to the fact that accounting data provides a highly objective view of a company's financial standing and operational performance. However, the rise of virtual assets has introduced complexities in valuing these modern assets through conventional accounting frameworks. For investors, interpreting financial statements that incorporate virtual assets can feel akin to deciphering a document in a foreign language, challenging their ability to assess financial health and performance accurately.

The Korean regulatory body’s decision to establish accounting standards for virtual assets was born out of this concern. The essence of the 'Guidelines for Supervision of Accounting for Virtual Assets,' unveiled last year, centers on the mandate to "evaluate and disclose virtual assets with the same level of transparency and rigor as traditional assets." The approach will be closely scrutinized as it provides a detailed framework for the disclosure of virtual assets, an issue regulators in many countries are grappling with.

2. Background and significance of Korea's adoption of cryptocurrency accounting standards

South Korea has one of the highest per capita cryptocurrency holdings and trading volumes in the world. The institutional framework has lagged in comparison, unable to keep pace with the market's rapid expansion. The lack of uniform standards for the valuation and disclosure of crypto assets across companies has led to growing information asymmetries, complicating the investment landscape and leaving investors vulnerable.

Cryptocurrencies are very different from traditional assets. They exist solely in digital form, are prone to significant price volatility, and have a weak connection with the real economy. These distinctive attributes pose challenges in evaluating and classifying virtual assets through conventional accounting standards. The different accounting methods also make it difficult to compare financial statements across companies

In response, financial authorities have been rushing to establish relevant accounting standards to bring transparency and credibility to the virtual asset market. Following the enactment of regulations that mandated the disclosure of crypto asset holdings in July 2023, financial authorities have drafted a supervisory guideline. This guideline is the culmination of over a year's discussions, incorporating insights from a diverse array of experts, and it proposes a specific methodology for the valuation and reporting of virtual assets.

3. Key Takeaways from the Supervisory Guidance on Accounting for Virtual Assets

3.1. Revenue recognition after the completion of performance obligations in the whitepaper

The supervisory guidance stipulates that revenue from cryptocurrency projects should be recognized upon fulfilling all performance obligations detailed in the project's whitepaper. This principle addresses the distinct challenge in cryptocurrency ventures of clearly defining performance obligations, a task more straightforward in traditional business operations. Consequently, issuers and auditors are tasked with a meticulous approach to recording and identifying these obligations.

Taking Company A as an example, suppose its issued token's whitepaper states: "Complete development of a shooter game that can be used with the token by Phase 1." In this case, revenue recognition would be executed once the shooter game has been fully developed and becomes operational, allowing token holders to utilize their tokens within the game platform.

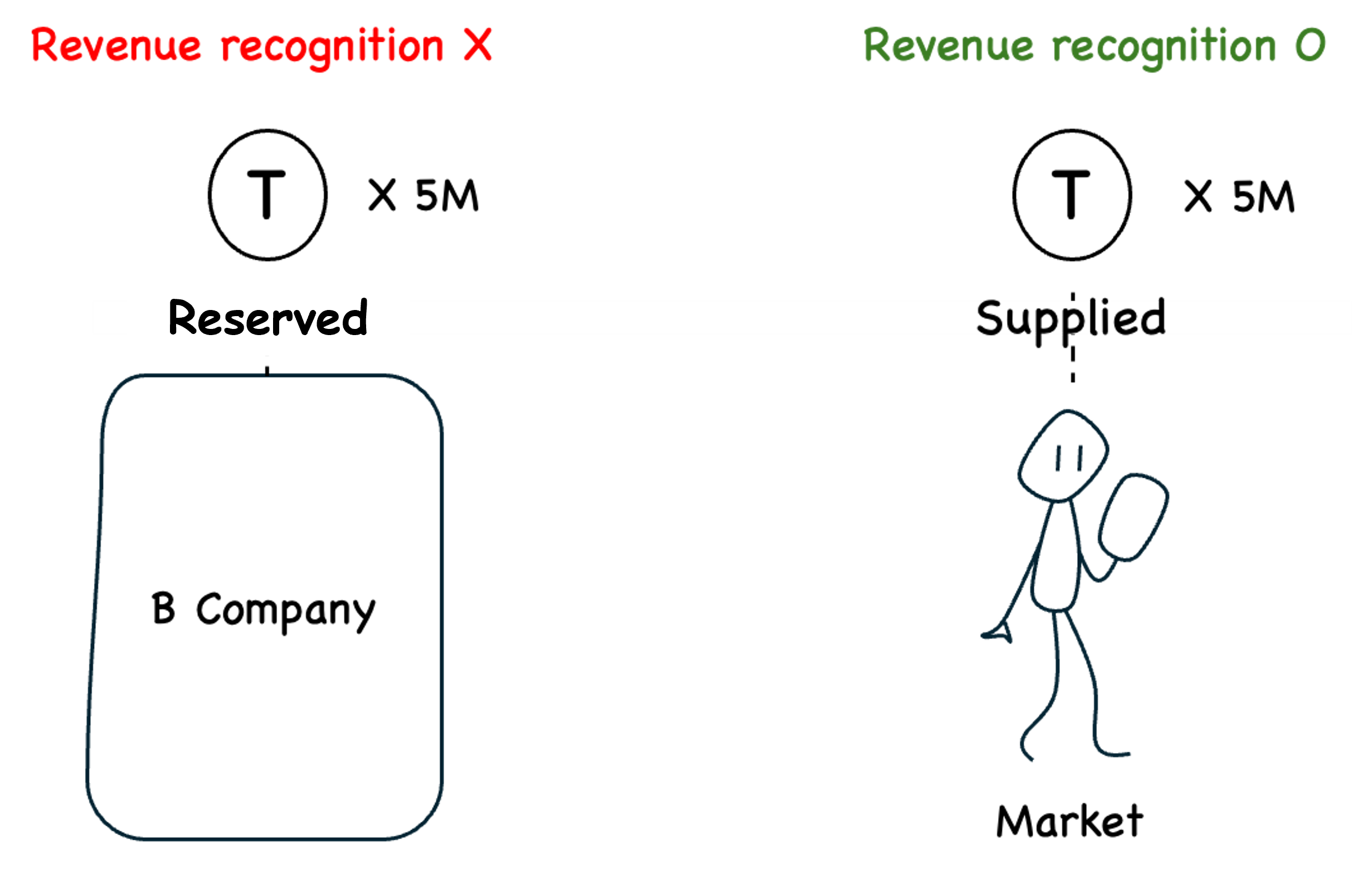

3.2. Token reserves are not recognized as assets

Reserved tokens, which are retained internally by a company, are not initially recognized as assets due to their lack of immediate economic value generation. These tokens may be classified as either assets or liabilities upon their actual distribution, contingent upon the circumstances of their release and utilization. Given this potential shift in classification, it becomes crucial for companies to maintain transparency regarding the volume of tokens held in reserve and their intended distribution plan.

Let's consider Company B, which has issued a total of 10 million tokens. Out of these, 5 million tokens are actively circulating in the market, and the remaining 5 million are held back as reserved tokens. Initially, only the 5 million tokens that are in circulation would be recognized as assets in the company's financial statements, reflecting their active economic contribution. The 5 million reserved tokens, on the other hand, would not be considered assets due to their dormant status.

Should there be plans to release an additional 1 million tokens from the reserve into the market in the future, Company B must disclose this plan transparently. This disclosure ensures that investors and stakeholders are fully informed about the potential increase in circulating tokens and can gauge the impact this may have on the token's value and the company's asset valuation.

3.3 Strengthening annotations

Beyond the establishment of accounting standards, the mandate for disclosing cryptocurrency-related information has been notably reinforced. Critical data, such as 1) the main contents of the whitepaper, 2) distribution and reserve status, 3) customer deposit contract information, and 4) custody risk must now be meticulously detailed in the financial notes and subjected to external auditing.

Take Company C, which has issued a total of 100 million tokens. Of these, 60 million tokens are in circulation, 20 million are held in reserve, and another 20 million are designated for free distribution. The company is obligated to provide a detailed account in the financial disclosures, clarifying the quantity, scheduled timing, and specific plans for distributing each segment of tokens.

Furthermore, should there be 10 million tokens deposited by users on the company's platform, Company C must transparently outline the scope of these deposits, the management practices in place to safeguard these assets, and any potential risks associated with hacking.

3.4. Customer Deposits on an Exchange

Exchanges are tasked with discerning which party maintains "control" over the virtual assets in their custody. Should the exchange be deemed to have control over these assets, it is required to recognize both the asset on its balance sheet and the corresponding liability to the customer. In cases where the exchange does not exercise control, the exchange is obligated to detail this information within the financial notes.

The process for determining control hinges on analyzing various factors, including the stipulations of relevant contracts, applicable laws and regulations, and adherence to international standards, particularly those on safeguarding customer property rights in the event of a security breach.

a customer deposits 10,000 bitcoins with Exchange D, and the terms and conditions clearly stipulate that customer assets are given priority in protection and compensation in the event of a hacking incident, this arrangement implies that Exchange D holds effective control over those deposited assets. Given this control dynamic, it is prudent for Exchange D to detail this arrangement in the financial notes rather than recognizing the deposits directly as an asset and corresponding liability on its balance sheet.

4. Opportunities opened up with accounting standards

The establishment of supervisory guidelines for accounting standards necessitates that foundations, exchanges, and wallets adhere to these guidelines to comply with accounting and disclosure standards for transparency and credibility.

Foundations are required to clearly disclose token issuers and recipients, the time of initial issuance, related parties, and distribution plan at the time of initial listing, and separate the interests of the foundation from the interests of investors.

Exchanges will be required to disclose foundation information and circulation volume, custody, inflow volume at the time of listing, periodic inflow volume and volume attributes, and trading revenue based on trading volume.

Wallet services are not currently subject to disclosure, but it is expected to be expanded in the future to complement the disclosure of foundations and exchanges.

The practical challenges faced by companies holding crypto assets are substantial, particularly concerning 1) the management of their wallets, 2) determining the appropriate timing for the recognition of crypto assets in accounting, and 3) establishing a method for valuing these assets. These complexities have created a niche market demand that several companies have stepped in to fill by offering specialized accounting solutions.

GDAC, Xangle, and Hexlant stand out as leading providers of cryptocurrency wallet accounting services. GDAC, in partnership with Woori Fund Service, initiated a wallet accounting service tailored for cryptocurrency entities in 2022 and is now undergoing a service renewal to enhance its offerings. Xangle, leveraging its extensive experience from running a disclosure portal, is currently beta-testing its 'Xangle ERP' service, aiming to bolster proper disclosure and adherence to accounting standards. Meanwhile, Hexlant, capitalizing on its seasoned experience as a wallet provider, has ventured into offering tax services ‘Octet’ in collaboration with the tech startup Bridgecode.

As corporate investments in cryptocurrency assets become increasingly prevalent, there is a growing demand for specialized accounting solutions tailored to the unique challenges posed by these digital assets. This trend is not limited to companies currently engaged in crypto-related businesses; it is expected to expand to a broader range of industries. Consequently, it is imperative for researchers and industry professionals to closely monitor the business trends of companies that have entered the accounting solution market, as well as stay abreast of any changes in related laws and regulations.

5. Necessary follow-up actions

The new accounting standards will enhance transparency within South Korea's cryptocurrency market. Nonetheless, stabilizing and effectively implementing these standards presents formidable challenges. A critical step is the reinforcement of accounting audits, ensuring rigorous compliance checks with the newly established standards. To guarantee the standards' efficacy, the imposition of stringent sanctions for any violations is essential. Consulting and training for relevant personnel will also be needed to support the smooth implementation of the system.

Global harmonization stands as a pivotal concern, especially given the borderless nature of the virtual asset market. The establishment of international standards is imperative for ensuring consistency and transparency across nations. To this end, Korea needs to actively participate in standard-setting discussions at the IASB (International Accounting Standards Board) and ISSB (International Sustainability Standards Board) and share its experiences and know-how. This leadership could be instrumental in shaping a cohesive and comprehensive international regulatory framework for cryptocurrencies and other digital assets.

Get 20% off your SEABW ticket today!

Join us at the biggest blockchain event of the year in Southeast Asia! This is your chance to connect with industry leaders, explore innovative blockchain solutions, and engage in valuable networking opportunities. The event runs from April 22nd to 28th in Bangkok.

Exclusive Offer for Our Readers: Use code TIGERR20 to receive 20% off your general admission tickets. Tickets are limited — secure yours now to ensure your spot at this event. (Discount automatically applied through the link below).

Get 30% off the biggest SEABW side event: ONCHAIN 2024

Tiger Research is a proud media partner of ONCHAIN 2024.

As Asia’s first Real-World Asset conference, the event will feature speakers including leaders from global financial institutions, leading RWA protocols and regulators.

Get a glimpse into the future of RWA tokenization at ONCHAIN 2024: April 26th, Bangkok!

Enter code “tiger30off” to receive 30% off your tickets to the event.

Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.