How Does the Government Regulate Crypto Exchanges in Korea and Japan ?

Crypto in Contrast: Comparing Cryptocurrency Listing in Korea and Japan

Tl;DR

In the wake of major setbacks such as the Terra/Luna crash in South Korea and the Coincheck hacking in Japan, both countries have launched self-regulatory associations aimed at regulating CEXs.

Furthermore, both governments are focusing on treating the associations as a singular channel for managing and controlling all virtual cryptocurrency exchanges. Consequently, understanding these organizations and their internal processes is very important to enter these markets.

There is an ongoing debate as to whether self-regulation, through direct stakeholders in the virtual asset market, is genuinely effective. Even so, many believe that these self-regulatory mechanisms can indeed pave the way for efficient regulatory measures and foster healthy growth in the virtual asset market.

Introduction

In April 2023, the European Union passed the Markets in Crypto Assets (MiCA) legislation, marking a pivotal step in regulating digital currencies. Around the same time, in June 2022, the United States put forth the Responsible Financial Innovation Act. These developments indicate a shift towards proactive regulation of cryptocurrency exchanges in key jurisdictions.

Similar regulatory proposals are emerging in Asian countries like South Korea and Japan, albeit with distinct nuances. Firstly, both governments have strongly encouraged the formation of associations and alliances amongst Centralized Exchanges (CEXs) for “self-regulation”. Secondly, governments are treating these associations as a singular channel for controlling and managing the entire crypto exchange market, including on/off ramp and trading.

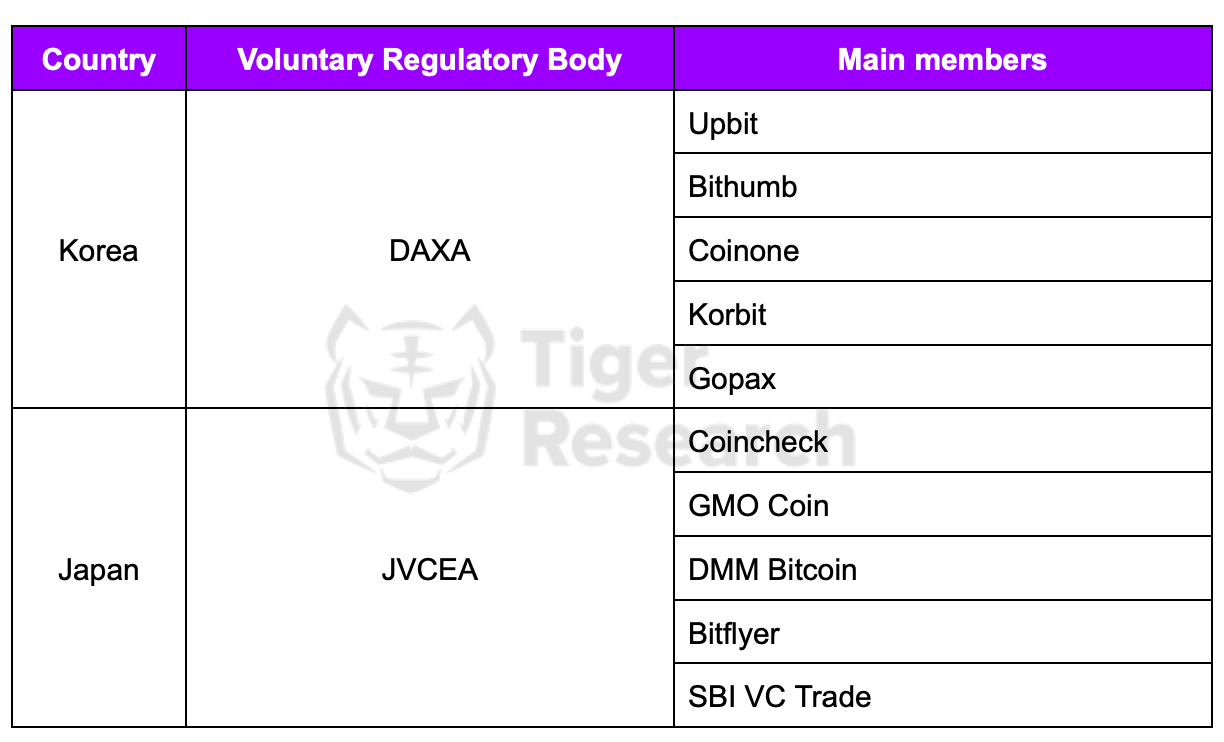

5 South Korean exchanges formed the Digital Asset eXchange Alliance (DAXA). Similarly, Japan launched the Japan Virtual Currency Exchange Association (JVCEA) with sixteen exchanges.

List of members in each self-regulatory association

Understanding these two organizations is essential for anyone wishing to venture into the Korean or Japanese crypto market. The two markets collectively account for roughly 10% of the global cryptocurrency trade volume (estimated at around $280 billion). With trading volumes increasing by 46% and 80% respectively in 2022 compared to 2021, these markets promise attractive opportunities for globally scalable web 3 projects.

Difference between DAXA and JVCEA

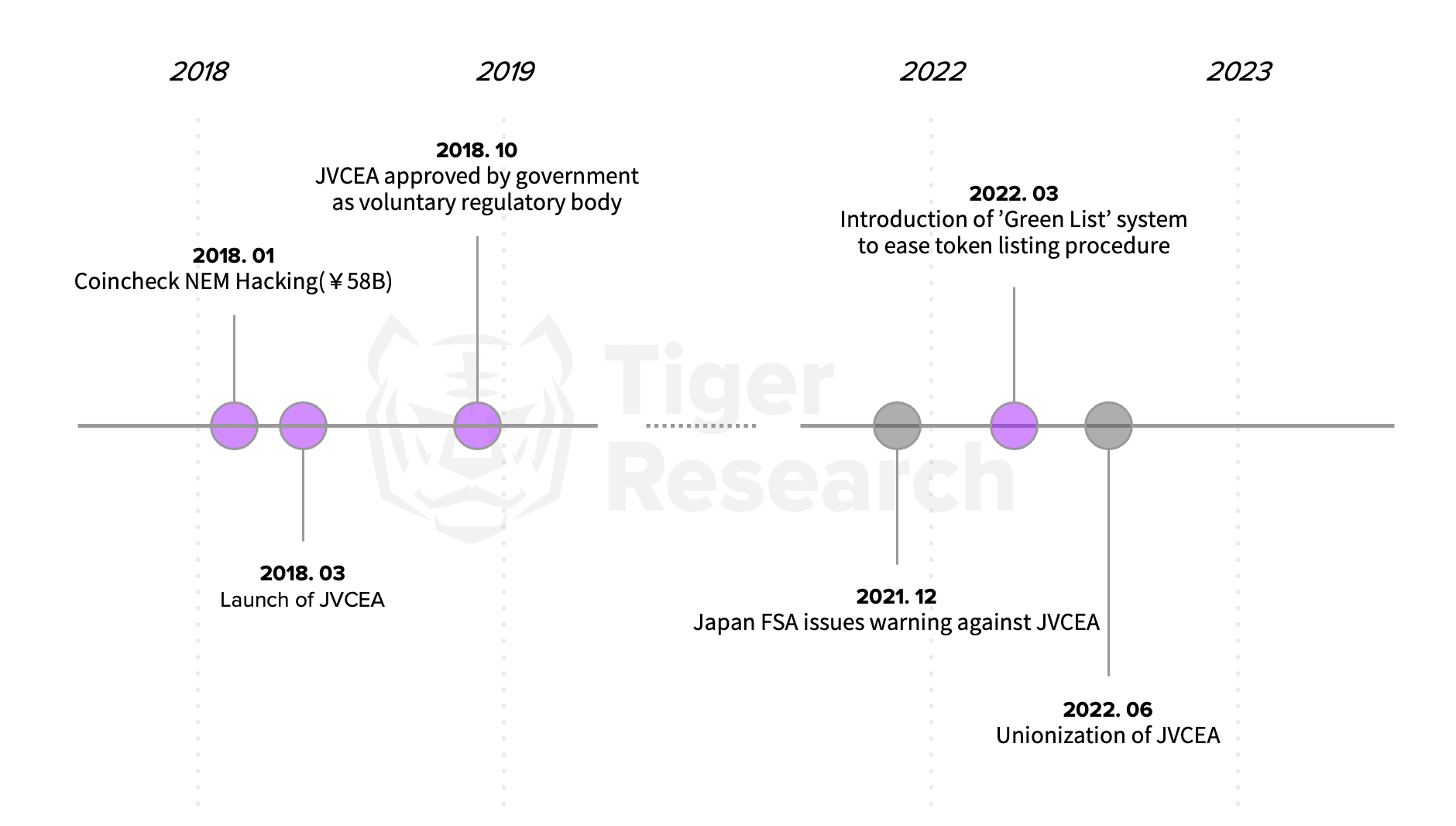

These self-regulating bodies were established as a response to several incidents related to virtual assets. In Japan, the establishment followed a significant hacking incident in January 2018 involving Coincheck, the country's largest cryptocurrency exchange. In South Korea, the discussions became more concrete after the Terra Luna crash in May 2022.

Both organizations share a common goal of 1) investor protection and 2) market stability through regulations. Nonetheless, there are also stark differences between the two organizations, with 'legal authority' being the most substantial.

In Japan, the JVCEA was officially recognized as a self-regulating body under the Payment Services Act by the Financial Services Agency (FSA) in October 2018. This allowed the JVCEA to exert a powerful influence on VASP(Virtual Asset Service Provider) licensing and asset listing as the authorized regulator.

On the other hand, South Korea's DAXA does not hold such legal authority. It is a private organization that primarily serves as a communication channel between the government and the virtual asset market, with a comparatively limited role. The lack of a legal basis to influence exchanges or cryptocurrency projects limits DAXA to only providing self-limiting guidelines. It's plausible to cautiously anticipate the establishment of an official government body similar to JVCEA in South Korea in the mid to long term when regulatory frameworks are established.

Differences in the licensing process

In Japan, running a virtual asset exchange requires meeting two essential conditions: 1) passing a six-month review by the FSA and 2) obtaining the 'Class 1 membership' license issued by the JVCEA. There are three types of membership licenses offered by the JVCEA. 'Class 2 membership' is for businesses preparing or intending to undergo the FSA review, meaning they can join before passing the FSA review. 'Class 1 membership' is granted only after passing the FSA review. The third type of membership, 'Class 3', is for other businesses, although the details have not been fully disclosed yet.

The transition from 'Class 2' to 'Class 1' may seem straightforward, but there have been instances of businesses failing. British crypto payment platform Wirex, for example, passed the FSA review and obtained 'Class 2 membership' but ultimately failed to reach 'Class 1'. This forced the company to withdraw from the Japanese market.

[Types of VASP Licenses for in JVCEA]

Class 1 members have the license to operate exchanges and trade derivative products related to virtual assets.

Class 2 members are those who have applied or are planning to apply for licenses to conduct business as virtual asset operators. They are typically awaiting approval from the financial authorities.

The criteria for Class 3 members are yet to be defined.

The Digital Asset Exchange Association (DAXA), unlike its Japanese counterpart, is a private institution and lacks the power to grant licenses. This falls to governmental agencies like the Financial Intelligence Unit (FIU) and the Financial Supervisory Service. For instance, to start a virtual asset business, a business must submit its application documents to the FIU, which then refers the application to the Financial Supervisory Service for review.

Differences in the listing process

The listing procedure for virtual assets also differs significantly, largely due to the varying legal authorities of their respective self-regulatory organizations.

JVCEA directly involves itself in the procedure, maintaining a "whitelist" of virtual currencies. For a cryptocurrency to be listed on an exchange, it must undergo a mandatory review process, which includes an assessment of the currency's transparency, stability, and marketability. The JVCEA then conducts its own whitelist review process. Ultimately, only after clearing the Financial Services Agency (FSA) review can a cryptocurrency be listed on an exchange. Furthermore, both JVCEA and FSA continuously monitor and manage the listed currencies.

While this cross-validation process creates a safer and more transparent market environment, it also has its critics. The whitelist review process is known to be stringent and time-consuming, taking a minimum of six months, which limits the market's ability to respond proactively. Some argue that this rigorous scrutiny hampers the growth of the virtual asset market and drives Japanese users to foreign exchanges.

In response to these criticisms, JVCEA introduced a "greenlist" system in March 2022 to streamline the listing process. The greenlist system allows for a Fast Track listing, by skipping the preliminary evaluation process, based on the autonomous decision of the exchange. Although this may seem to reduce the influence of JVCEA, it seems highly unlikely. The greenlist criteria are closely related to standards provided by the JVCEA, and the system also strengthens post-listing scrutiny.

Greenlisting criteria include:

The project should be listed on at least three Japanese virtual currency exchanges as per JVCEA guidelines.

The project should have been listed for more than six months on at least one of the three exchanges.

The project should not have any disqualifying reasons identified by the JVCEA at the time of listing.

The project should has not have mandatory listing conditions set by the JVCEA .

In contrast, DAXA, being a private organization without regulatory power, cannot realistically intervene in the listing process of virtual currency projects. It can merely establish and suggest listing standards. However, as DAXA was formed around the five largest exchanges, they may be able to indirectly influence cryptocurrency listings.

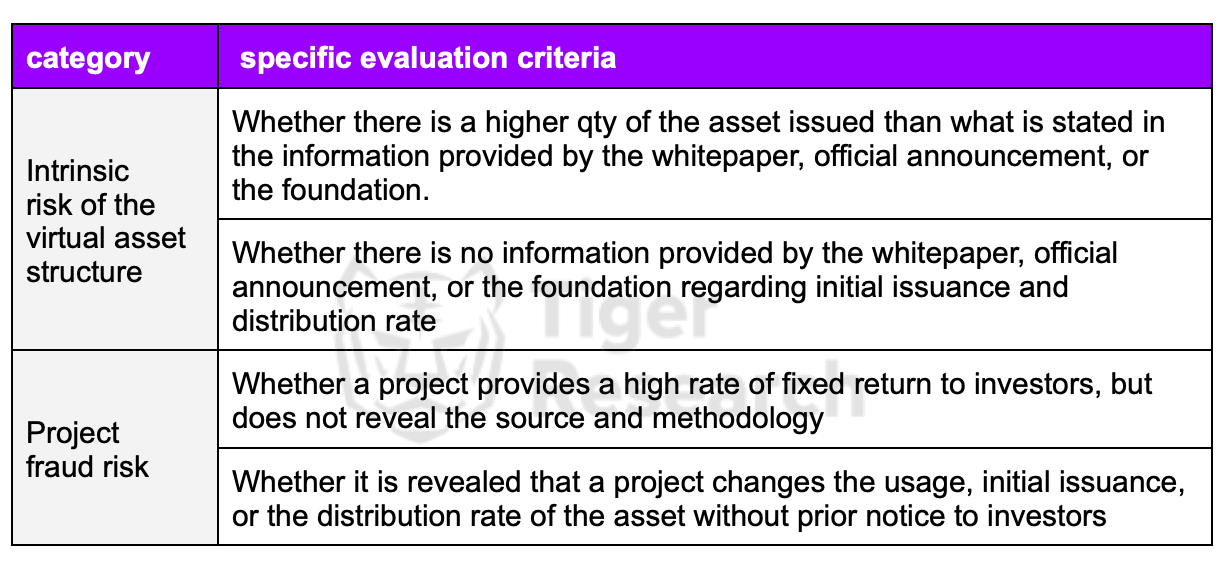

Below are the criteria for risk assessment on crypto listings for DAXA :

Intrinsic Risk

Technical Risk

Conclusion

Both South Korea and Japan are exploring government-led proposals to regulate cryptocurrencies. However, at the moment the focus is still on self-regulation, centered around virtual asset exchanges—something both governments recognize and recommend as part of their regulatory approach. The aim is to manage and control the overall virtual asset market through the exchanges.

However, there are doubts as to whether these self-regulatory organizations can indeed cultivate a transparent and safe market environment. For example, some claim that the Japanese virtual asset exchange Coincheck effectively controls the entire organization's structure of JVCEA. This control has even sparked internal conflicts, resulting in the formation of labor unions.

In South Korea, similar concerns that the exchange Upbit wields significant influence over DAXA also exist. This was especially notable in November 2022, when the decision to delist WeMix led to WeMade's CEO, Hyungook Jang, stating that it was an act of bullying by Upbit.

Furthermore, DAXA members consist of large exchanges, making it challenging to represent and control smaller exchanges. During the joint delisting decision for WeMix by DAXA , the smaller exchange collective GDAC chose to list WeMix, indicating underlying tension within the virtual asset exchange industry.

Despite such concerns, some argue that it's through these self-regulatory bodies that healthy growth in the virtual asset market can be achieved. The high market comprehension of virtual asset exchanges, they suggest, can lay the foundation for efficient regulatory measures. Some of the concerns could also be mitigated if legal authority were given to self-regulatory bodies, ensuring they have safety measures to prevent deviant behavior.

In South Korea, there is currently no official organization with legal grounding like the JVCEA. However, this may change in the long term. This comes as discussions on giving legal authority for self-regulatory bodies like DAXA have surged following a series of negative incidents in the South Korean virtual asset industry. That said, this new way of doing things could cause competition between groups that are already involved, like DAXA, exchanges, FIU, and the Financial Supervisory Service.