Key Takeaways

OUSD turned the reserve-yield structure that Circle once held exclusively into an industry default. The stock fell 17 percent even before launch, not because Circle lost market share but because the announcement unsettled a core premise of its revenue model.

A stablecoin with the same structure already existed in USDG, but it never became a threat because Coinbase stayed out. What sets OUSD apart is that it brought in Coinbase, the partner that actually distributed USDC for Circle.

Three questions matter. The first is whether OUSD becomes real leverage for Coinbase in the August renegotiation. The second is how quickly Circle can reduce its dependence on interest income through CPN and Arc. The third is how long it takes for the logos of 140 traditional companies to translate into actual circulating supply.

On June 30, 2026, Open USD (OUSD) launched as a jointly issued stablecoin backed by more than 140 companies, including Visa, Mastercard, Stripe, and BlackRock.

Unlike the traditional model in which the issuer controls the market, OUSD adopts a structure in which participants can issue and redeem at no cost and receive a share of reserve income. This represents a fundamentally different standard from the USDC model, where the issuer holds revenue rights and negotiates terms with each partner individually.

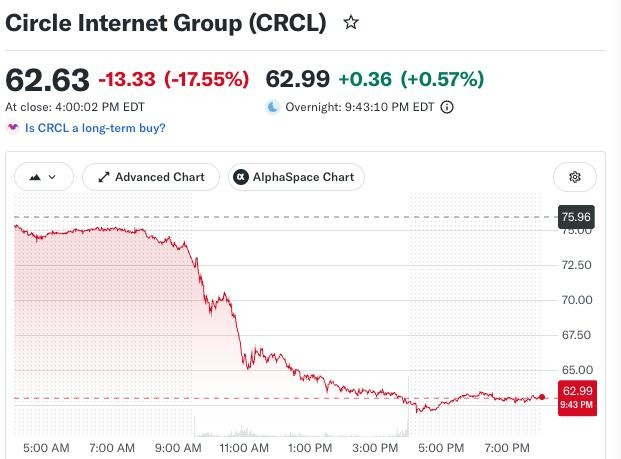

When the announcement broke, Circle’s stock fell 17 percent to its lowest level in four months. OUSD had not yet launched and carried no transaction volume. No share had changed hands in the stablecoin market, yet the market had already concluded that Circle’s existing revenue model was under threat.

Why Now

To understand the reaction, the question is not what OUSD does but how it changes the terms on which revenue is shared across the stablecoin industry.

Circle built its distribution through private negotiations with key partners, most notably Coinbase. Those revenue-sharing arrangements served two purposes simultaneously: they were the cost Circle paid to secure distribution, and the barrier that kept rivals from matching its reach. Revenue sharing was, in this sense, a strategic instrument, one Circle deployed selectively to protect its competitive position.

OUSD converts that instrument into an industry default. Where Circle required negotiation, OUSD distributes reserve income as a matter of course, without conditions. Partners who previously had to bargain with Circle for a share of yield can now access equivalent economics freely.

The market’s concern is not that OUSD has already taken share from Circle; it is that the exclusive value of Circle’s partnership network, built over years of selective deals, can be replicated by any participant from the moment OUSD goes live.

Simple Analogy

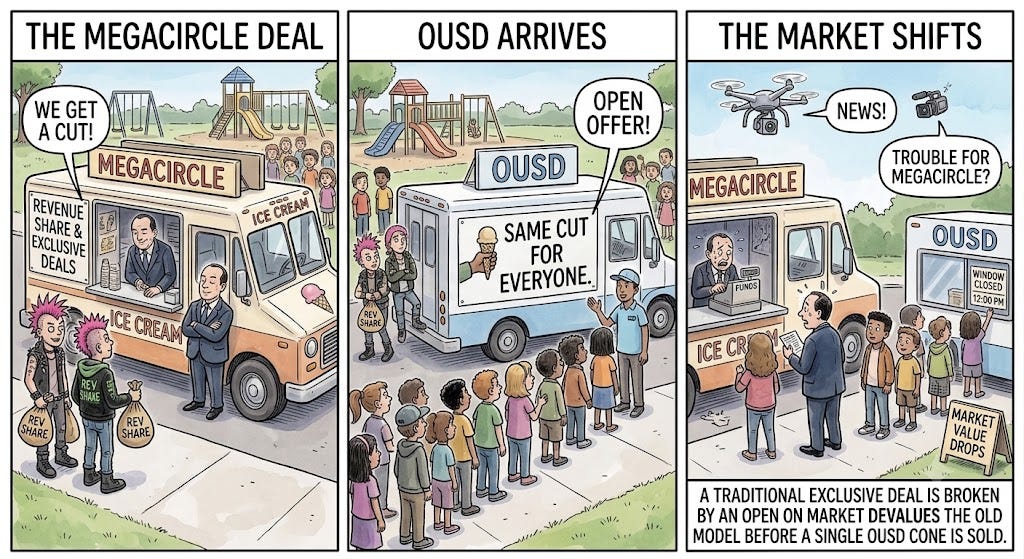

Picture a playground with a single ice cream truck parked beside it. The owner of that truck is Circle.

To build sales, the owner quietly approached the most popular kids and made each one a private offer: bring your friends, sell more ice cream, and you will receive a cut of the proceeds. Those kids stopped looking at any other truck and pushed this one exclusively. Sharing revenue was not a concession for the owner; it was a barrier that kept rival trucks from getting close.

Then a new truck appeared, OUSD. Rather than selecting a few popular kids for private deals, it made the same offer to everyone: sell this ice cream, from any neighborhood, and you receive the same share, regardless of how popular you are or where you come from.

The popular kids reconsidered. The arrangement they had received was no longer exclusive, because the same terms were now available to anyone. The incentive to stay loyal to the older, more expensive truck had weakened considerably.

The new truck had not yet opened its window or sold a single cone. People were already saying the old truck was in trouble, and the owner’s standing fell in a single day. No customers had actually left. The market simply concluded that they were likely to, and priced that in ahead of time.

A Familiar Structure, and Circle’s Exposure

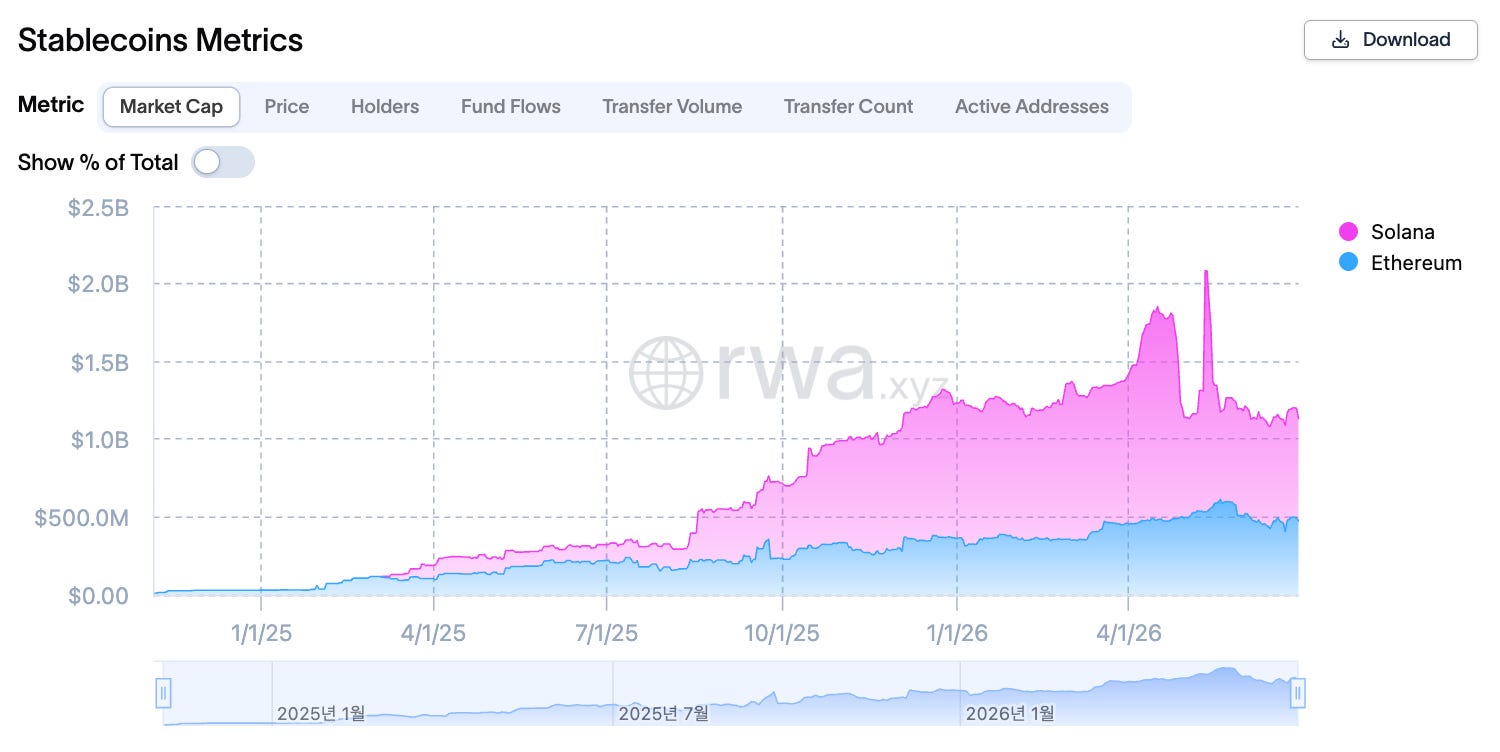

Paxos’s USDG is structurally identical to OUSD: reserve interest distributed to partners in proportion to their contribution. Its circulating supply stands at roughly $1.1 billion, a negligible share compared to USDT’s $185 billion and USDC’s $72.8 billion.

USDG’s partners have been crypto-native platforms such as Kraken and Robinhood. Coinbase, the central node in Circle’s distribution network, was absent, and that absence is precisely why USDG’s growth never translated into meaningful pressure on Circle’s stock or business.

OUSD changes that calculus. Coinbase has joined as a founding member, and the timing matters: Circle’s distribution agreement with Coinbase operates on a three-year cycle, with the first expiration falling in August 2026. Entering a renegotiation as a founding partner of a competing stablecoin gives Coinbase a credible alternative, and with it, considerably more leverage at the table.

The stock decline, then, reflects something more specific than fear of market share loss. It reflects the market’s recognition that the balance of power underpinning Circle’s revenue model has shifted materially toward Coinbase. Circle’s recent progress on self-distribution, raising its proprietary channel share from 6 percent to 17.2 percent over a single year and lifting Q1 RLDC margin to 41.4 percent, underscores the point: the improvement is real, but its scale implies how significant the prior dependence on partners was.

What to Watch

1) The Coinbase Renegotiation

The August renegotiation with Coinbase is the most immediate test. Whether Coinbase uses OUSD as leverage to pull revenue-sharing terms in its favor, or elects to maintain the existing partnership largely intact, will determine how much real-world weight OUSD carries. The outcome will clarify whether this coalition is substantive pressure or an announcement without follow-through. That said, Coinbase is both a major Circle shareholder and a core distribution partner, which makes a full break unlikely. The more probable outcome is that Coinbase uses OUSD as a negotiating instrument to improve specific contract terms, such as the revenue-sharing rate, rather than to exit the relationship.

2) Circle’s Response

Circle’s path is not difficult to read. It will not abandon the reserve interest that accounts for 94 percent of its revenue to match OUSD’s distribution structure. Instead, Circle will concentrate on two things: expanding its Circle Payments Network, which generates revenue without sharing yield with partners, and accelerating the development of Arc, its Layer 1 platform designed to support revenue streams that do not depend on interest income. Arc’s mainnet launch is expected this summer, and how quickly that platform gains traction in the market will be the central test of Circle’s ability to reorient its business.

3) The Speed of Distribution

The majority of OUSD’s 140 partners are traditional companies rather than crypto-native platforms. Regulatory review, operational integration, and the development of meaningful transaction volume take time. The partner count is a signal of intent, but it will not translate into a market position until it is reflected in circulating supply. Until that proof exists, OUSD cannot credibly displace existing stablecoins in day-to-day use.

The balance of the stablecoin market is shifting. How quickly and how far remains the open question. Consortia of this kind are difficult to operate in practice, and incumbent network effects erode slowly.

The severity of Circle’s stock decline looks closer to fear than to a measured assessment of near-term damage.

Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.