Inside Look : How Korean Companies Gear Up for the STO Market Opportunity

#2 STO market strategies for South Korean companies

TL;DR

Korean securities firms are fast moving to establish a strong foothold in the emerging "token securities" asset market. They're partnering with fractional investment and blockchain startups through partnerships and MOUs to explore new business models.

However, the market faces challenges that hinder its potential to promote the spread of Web 3. These include 1) ambiguous regulations and guidelines, 2) entry barriers for individual investors (i.e. invesment cap of $30,000 per asset), and a 3) extremely centralized & controlled system that opposes blockchain's decentralization philosophy.

Korea may follow Japan's path, where the token securities market has been slow to develop. It's likely that Korea will also experience an experimental phase lasting rouhgly 2-3 years.

Introduction

In the previous article, "A Simple Guide to Korean STO Regulations", we summarized the main points of the domestic token securities guidelines. In this follow-up, we'll examine the status of major players preparing to enter the domestic STO market based on these guidelines and explore key trends. Through this, we plan to outline potential and promising businesses in Korea in the final installment, Part 3.

Current State of the Korean STO Ecosystem

Since the announcement of the Financial Services Commission's (FSC) STO guidelines in February, securities firms have taken the lead in the domestic STO ecosystem. They are building partnership alliances by forming a 'Token Securities Council' through MOU agreements or actively pursuing token securities businesses directly through M&A, as seen with DAISHIN Securities Co., Ltd acquiring the real estate fractional investment platform 'Kasa Korea.'

Examining the MOU agreements and councils formed thus far in relation to token securities, partnerships with companies possessing the following capabilities have been emphasized:

Acquire token securities operation know-how through partnerships with fractional investment startups like Kasa Korea and Together Art, who have already operated similar services as part of a government's R&D project.

Source diverse product portfolios through partnerships with companies that have the ability to discover, source, and manage the underlying assets of token securities.

Collaboration with blockchain solution providers for implementing the distributed ledger technology essential for issuing and distributing token securities.

In summary, these companies are preparing a three-pronged approach: 1) product development for token securities brokerage, 2) acquiring operational know-how, and 3) securing blockchain tech capabilities.

Key Players

The domestic token securities ecosystem in Korea is expected to be composed of four main types of players: ① STO underlying asset holders, ② token securities issuers, ③ token securities distributors, and ④ STO technology partners. Each player may not only take on a single role but also perform multiple roles, adopting strategies to secure and develop the market's value chain.

① STO Underlying Asset Holders

'STO underlying asset holders' are players who own physical and financial assets that serve as the basis for token securities issuance. In Korea, existing fractional investment specialists have primarily issued and distributed products focused on physical assets such as real estate and artwork. However, since the incorporation into the regulatory system, the composition and scope of the products have been diversifying. For instance, the range of physical assets now includes precious metals (diamonds, gold, and silver) and intellectual property (IP), and it has expanded to financial assets like loan bonds and unlisted bonds.

② Token Securities Issuers

In the traditional securities issuance system, only financial institutions such as securities firms could issue securities. However, after the announcement of the token securities guidelines, the introduction of the "issuer account management institution" allowed qualified issuers to directly register securities, lowering the barriers to entry.

Nevertheless, it is generally challenging for new businesses to meet the requirements of the financial market, so it is expected that companies with some knowledge and experience in the financial industry will primarily engage in the issuance business.

For example, companies with experience in issuing and distributing fractional investment products through the regulatory sandbox, like existing fractional investment firms, may aim to operate independently by acquiring the newly established "issuer account management institution" license. Securities firms that already have the "account management institution" license and financial infrastructure can easily enter the token securities issuance market as long as they meet the distributed ledger requirements. The market has higher hope from newly emerging startups a strong technological foundation, as seen in the competition between traditional banks and internet banks in the Web 2.0 financial market.

Since the announcement of the STO integration into the regulatory system, active discussions about token securities have been taking place among various players. However, it is still challenging to find concrete details and products. Therefore, it is worth examining the cases of existing fractional investment firms to deduce how future token securities issuers may source and issue token securities in various forms.

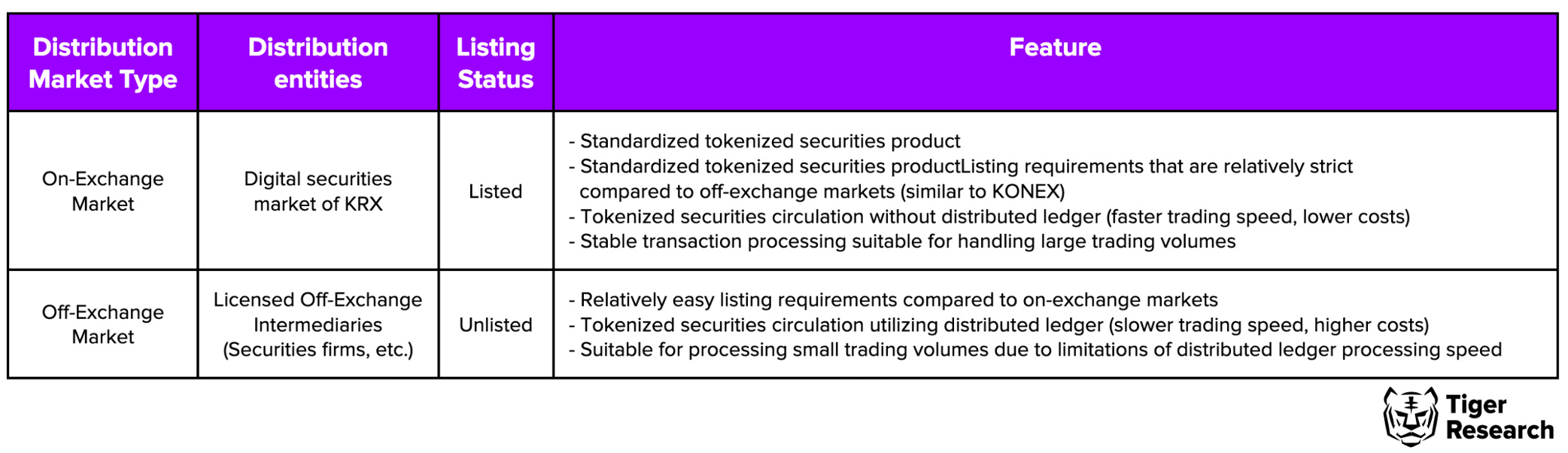

③ Token Securities Distributors

According to the 'Token Securities Distribution Regulatory System' in the token securities guidelines, the distribution of token securities is defined differently depending on whether they are listed or not. For example, listed tokens are expected to be traded through the standardized digital securities market under the Korea Exchange (KRX), which will be launched on a trial basis. Unlisted tokens will be traded over-the-counter through securities firms and new businesses holding the newly established 'OTC trading brokerage' license.

In principle, the distribution of listed token securities is expected to follow the monopolistic system of the Korea Exchange, similar to the existing securities market. However, there is a possibility that token securities could be traded in alternative trading systems (ATS) as the launch of ATS and the authorization of token securities coincide. Although some argue this possibility, it is realistically expected to be low. Nonetheless, the newly established 'OTC trading brokerage' license will likely lead to more diverse entities distributing token securities in OTC markets, resulting in a somewhat open competitive system.

④ STO Technology Partners

Token securities issuers and distributors must fundamentally meet the 'distributed ledger' requirement. Therefore, for most securities firms and fractional investment companies without inherent blockchain technology, a close partnership with blockchain technology companies will be necessary. Blockchain technology companies will mainly provide private blockchains where token securities can be issued or offer solutions for the distribution and management of token securities.

While the underlying technology for issuing token securities is important, cooperation with companies that provide evaluation models for the underlying assets composing token securities will also play a significant role within the STO ecosystem. Theoretically, the range of assets that can be tokenized is vast, and each underlying asset has different characteristics and regulations.

Conclusion

As emphasized earlier, the domestic token securities ecosystem in Korea is expected to be led by ① STO underlying asset holders, ② token securities issuers, ③ token securities distributors, and ④ STO technology partners. Currently, securities firms are mainly forming partnerships, which can be interpreted as an effort to strengthen their competitiveness based on their high market share in the traditional financial system.

However, compared to more developed capital markets, the size of Korea's token securities market is still very small (if any), and the range of underlying assets composing token securities is limited. Furthermore, it is almost impossible for each player to independently meet all the requirements demanded by the FSC. The FSC also doesn't want a monopoly of certain securities firms in this sector. Therefore, it is anticipated that establishing a market ecosystem through mutually complementary partnerships will be crucial. Additionally, considering the adoption timing and maturity level of the blockchain and token securities-related industries, it is expected that the focus will be on expanding the overall market pie rather than on competition between companies for the next 3 to 5 years. This collaborative approach is expected to create a healthier and more sustainable market ecosystem for token securities in Korea, enabling all players to benefit from its growth.