TL;DR

Major token securities markets, such as those in the United States and Japan, remain in their early stages, struggling to generate significant trading volume.

Three key factors contribute to this challenge: 1) a lack of investor trust compared to traditional securities markets, 2) lower volatility compared to the crypto market, making short-term gains less likely, and 3) a shortage of appealing new investment assets for the Millennials and GenZ in tokenized securities form.

Token securities exchanges in major countries face high fragmentation, unlike exclusive traditional securities markets like the NYSE. This prevents exchanges from achieving substantial trading volume.

Given these circumstances, the short-term potential for the Korean STO market to attract retail investors seems limited. The key to success lies in major securities firms and market participants working to tokenize "new innovative assets with high investment return potential" as token securities products.

Introduction

As we examined in the previous two articles, numerous Korean companies currently express interest in and actively pursue entry into the STO market. However, most companies remain in the initial stages of market entry. As the Financial Services Commission announced in the 'Token Securities Guidelines,' the market will likely gain momentum as related legislation comes into effect in the next 6 to 12 months.

The Korean market generally presents a favorable environment for issuing new investment assets as token securities for two main reasons: 1) the expanding concept of fractional investment reduces resistance to new assets classes, and 2) with the retail crypto trading volume ranks third globally, there is less resistance to digital asset investment.

Thanks for reading Tiger Research Reports ! Subscribe for free to receive new posts and support my work.

However, it is crucial to set the right direction from the market entry stage. In the Korean market, there are no precedents to reference other than fractional investment, so it is essential to study international examples and establish a market entry strategy suitable for Korea. In this article, we will examine major international cases and suggest STO market entry strategies for Korean companies.

United States

In contrast to the newly emerging Korean STO market, the United States had its first STO issuance in 2018. For about five years, major platforms like tZero, INX, Aspencoin, and Securitize have been active. While these platforms primarily support issuance, fundraising, and secondary trading, most of them continue to struggle with extremely low trading volumes in secondary trading. This issue likely stems from a lack of attractive factors that would appeal to investors and issuers for entering the STO market.

INX

INX is a service often mentioned in many STO reports, having issued a registered token security with the U.S. Securities and Exchange Commission (SEC) in 2021 and raised $85 million from over 7,200 investors. While existing services had limitations in attracting investors due to using exemption clauses (Reg D, Reg S) for issuance, INX formally registered token securities with the SEC without restrictions on the range of investors.

Regulation D (Reg D): No limit on issuance size but restricted investor range, and the issued securities are non-transferable.

Regulation S (Reg S): No limit on the amount raised and investor type is restricted to offshore investors.

However, the INX token that raised funds is similar to the traditional IPO approach, where the company's dividend rights are tokenized as securities. This likely made it easier for them to officially register with the SEC, which prioritizes investor protection. While subsequently issued tokens exhibited the characteristics of new assets such as marine exploration, the INX token resembles traditional assets, entitling holders to dividends corresponding to 40% of the company's cumulative net cash flow from operating activities.

INX tokens, unlike stocks, do not have voting rights. However, token holders can receive a minimum of 10% commission discount when trading on the INX exchange, with tiered benefits up to a maximum of 40% commission discount. This utility feature sets INX tokens apart from stocks issued through traditional IPOs.

There are currently four investable tokens, all issued through exemption clauses Reg D or Reg S. These clauses impose restrictions during investor recruitment, and it's unclear if the tokens' whitepapers provide enough information for investors.

All tokens currently being raised aim to collect funds via token securities before starting new ventures, making them similar to traditional investment assets. These tokens are at higher risk than those in the securities market because they're unverified. Additionally, they don’t typically offer the expected returns compared to the crypto market, creating an unclear position that may not sufficiently appeal to investors.

INX currently supports secondary trading of token securities, but the trading volume for tokens other than INX is minimal. This is because, unlike a centralized securities exchange, each trading platform operates its own liquidity, similar to the crypto market. For example, most MSTO token trades take place on the XT exchange, while finding trades on INX proves challenging.

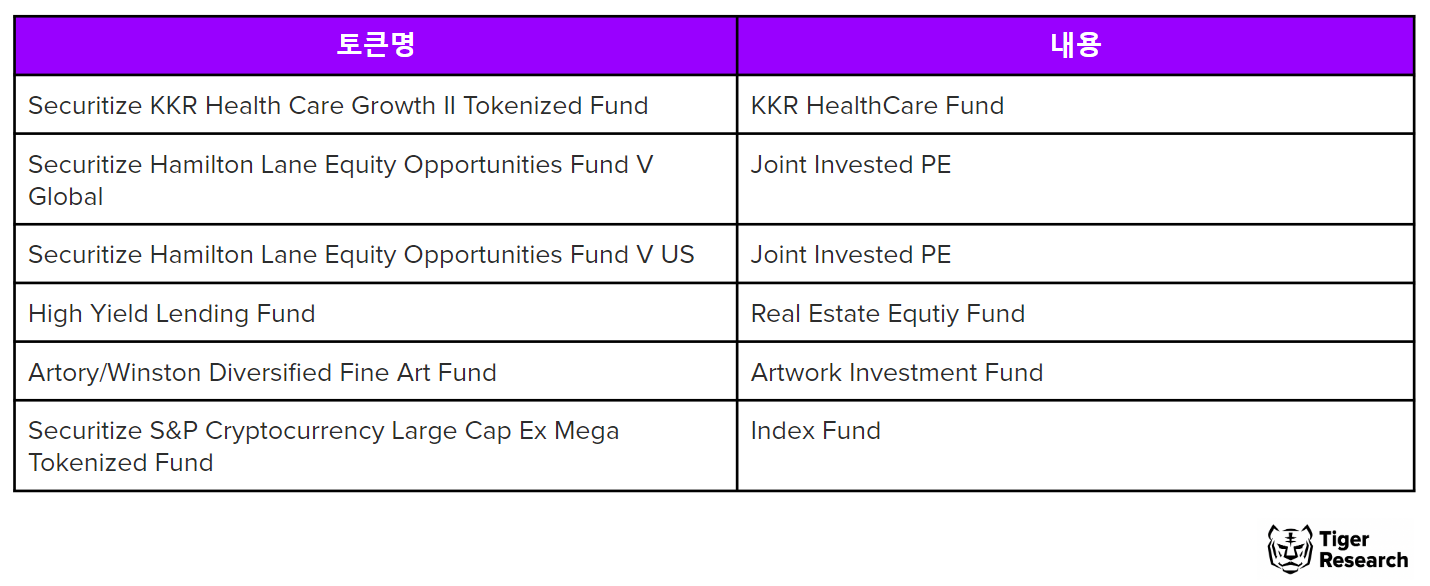

Securitize

Securitize, similar to INX, supports both issuance and distribution and currently allows subscriptions for six tokens. They primarily tokenize funds from large private equity firms like KKR and Hamilton Lane to raise investment capital. However, these tokens also struggle to differentiate themselves from existing investment assets, reducing their appeal to retail investors.

Japan

Japan has revised its STO regulations twice, in May 2019 and May 2020. Since these revisions, Japan's STO efforts, led by financial institutions like SBI Holdings, have taken place without building token issuance and distribution platforms like in the US. Instead, they have conducted test issuances. Notably, in 2021, Mitsubishi UFJ Trust and Banking Corporation tokenized its revenue bonds through the Securitize platform mentioned earlier, an American platform.

In March 2021, SMBC Group and SBI Group announced the establishment of the Osaka Digital Exchange, a joint venture set to handle tokenized securities starting in 2023. However, no concrete progress has been confirmed yet. The Tokyo Stock Exchange also announced plans to launch a securities exchange, but not until early 2025. This means the secondary market has not yet developed, and secondary trading opportunities remain limited.

Ibet for Fin

However, there are noteworthy attempts in Japan. For example, in April 2021, BOOSTRY, along with SMBC Nikko Securities, SBI Securities, and Nomura Securities, launched the Ibet for Fin platform for token issuance and management. SBI Securities issued its bonds as tokenized securities through this platform, and currently, ten financial institutions have joined as members. Ibet also plans to issue and distribute assets like real estate based on its member network. This indicates that Japan, like the US, mainly targets traditional investment assets, and the issuance structure is not significantly different.

Recommendation for Korean STO Market Entry

In February, the Financial Services Commission (FSC) announced that it would support the securitization of various emerging rights (such as fractional investing) and improve the issuance and trading of securities more efficiently and conveniently by utilizing distributed ledger technology through the token securities guidelines. The FSC aims to tokenize new investment assets (revenue securities, investment contract securities) through the STO market opening.

However, as examined earlier, the majority of issuance cases in the US and Japan over the past 3-5 years have involved tokenizing traditional investment assets (private funds, bonds, real estate, etc.). Furthermore, these tokenized securities have been somewhat ambiguously positioned, with higher risk compared to traditional investment assets and without the high returns expected from the more volatile crypto market.

Korean companies entering the STO market should consider differentiating their offerings by focusing on innovative asset classes or providing enhanced utility for token holders. They could also seek strategic partnerships with existing platforms and financial institutions to facilitate the issuance and distribution process.

As illustrated above, to move beyond the gray zone, new investment assets that guarantee both investor protection and profitability potentials are essential for tokenized securities. According to the Tokenized Securities Guideline, new investment assets that were previously hard to access can now be tokenized under securities regulations, ensuring greater stability than before, and with the potential to reap higher returns than existing assets.

Currently, apart from officially registered new investment assets, stability is generally low. Although various new investment assets, such as real estate, artworks, and music copyrights, have emerged, investor protection measures are still lacking. However, tokenizing these assets would subject them to verification processes, which would provide investors with initial guarantees of stability.

New investment assets also offer greater possibilities than existing assets. As of April 13th, the expected rate of return for stock investment is 6.78%. While there is no guarantee for new investment assets, they offer open possibilities, and can provide additional utilities that existing investment assets cannot.

Therefore, companies seeking to enter the domestic STO market should focus on discovering new investment assets that are more attractive to investors than existing financial assets. In particular, they should consider two crucial factors: creating investment products that investors can easily understand, and providing utilities that can be linked to investment products.

In summary, while it is important to apply for sandboxes and dominate the STO market by utilizing existing financial assets, it is ultimately essential to explore new investment assets that are attractive and intuitive to investors. Furthermore, by incorporating lock-in measures that are linked to utilities, as in the case of the INX token, companies can establish a clear grammatical structure that is distinct from existing investments, which is expected to provide a good chance of success.

Thanks for reading Tiger Research Reports ! Subscribe for free to receive new posts and support my work.