Blockchain Cross-Border Payments: Current Trends in Asia

Can Asia revolutionize cross-border payments infrastructure?

TL;DR

With the progress of globalization, the cross-border payment industry is growing rapidly, especially Asian countries are active in this industry with high transaction volume.

Traditional cross-border payment technologies are costly, time-consuming, and in need of improvement. As a result, countries and organizations are turning to blockchain technology to revolutionize the industry.

Cross-border payments is a multi-stakeholder industry, requiring governments, institutions, and the Web3 industry to collaborate in open innovation to deliver technological breakthroughs.

1. Cross-border payment systems in Asia Pacific

'Cross-border Payment System' refers to the infrastructure that enables the transfer of funds from a payer in one country to a payee in another. This infrastructure plays a crucial role in facilitating international trade and supporting smooth global business operations. However, the process is complex due to the need to transfer funds across international borders through a network of banks and financial institutions.

The cross-border payment system is particularly important in the Asia-Pacific (APAC) market, as Asian countries are experiencing rapid economic development and a swift increase in cross-border transaction volumes. According to the World Bank, three of the top five countries for global remittances in 2023 are in the Asia-Pacific region. Consequently, the importance of cross-border payment systems in this region is growing, with a need for stability and efficiency given their scale.

However, current cross-border payment infrastructure faces numerous challenges due to its inherent complexity and inefficiency. Complex procedures and excessive fees significantly diminish the benefits of global transactions. Therefore, many Asian countries are pursuing innovations using blockchain technology to facilitate seamless domestic and international transactions. This approach aims to reduce costs and increase accessibility, enhancing financial inclusivity.

2. Issues with Traditional Cross-Border Payment Systems

The traditional cross-border payment system primarily relies on the SWIFT messaging network, connecting over 11,500 financial institutions worldwide. However, this system is inefficient for international transactions. The process of transferring funds from the payer to the payee through multiple intermediary banks can take up to two weeks. Additionally, real-time processing is impossible due to capital controls, regulatory compliance procedures, and batch-processing systems, resulting in high fees. An analysis by the Bank of Japan revealed that from 2013 to 2019, the average cost of sending $200 overseas through traditional banks was nearly 20%, or about $40.

Conversely, using distributed ledger technologies like blockchain for cross-border transactions offers significant advantages:

Enhanced Transparency: Blockchain transparently records all transactions, making it easy to track the flow of funds and related information. Central banks can leverage CBDCs integrated with blockchain to facilitate cross-border payments, ensuring all transactions are traceable and verifiable to combat financial crimes like money laundering.

Removing Middlemen: Traditional cross-border payment systems involve multiple intermediaries, resulting in high costs and delayed processing. Blockchain enables direct transactions between banks, reducing costs and supporting real-time processing.

Enhanced Global Accessibility: Blockchain processes payments through a decentralized network accessible from anywhere, enabling cross-border payments even in developing countries and regions with limited financial services, thus promoting international trade.

3. Asia’s Race to Applying Blockchain for Cross-Border Payments

3.1. Government CBDC Initiatives: Hong Kong's Digital Yuan Pilot

In May, the Hong Kong Monetary Authority (HKMA) announced a pilot program for the digital yuan (e-CNY) to support cross-border payments between Hong Kong and mainland China, including Guangdong and Macau. This CBDC provides Hong Kong residents with a digital alternative to cash payments and integrates China's central bank digital currency into Hong Kong's financial system. From its pilot launch in 2019 until June 2023, the digital yuan facilitated transactions totaling 1.8 trillion yuan ($250 million), with over 10 million merchants in 17 regions of mainland China accepting it.

This pilot project allows Hong Kong residents to create digital yuan wallets linked to their mobile numbers and top up their wallets through the Fast Payment service, which operates 24/7. This marks the first integration of a central bank digital currency with a fast payment service. As usage increases, the digital yuan wallet may fully transition to topping up without the need for a mainland bank account.

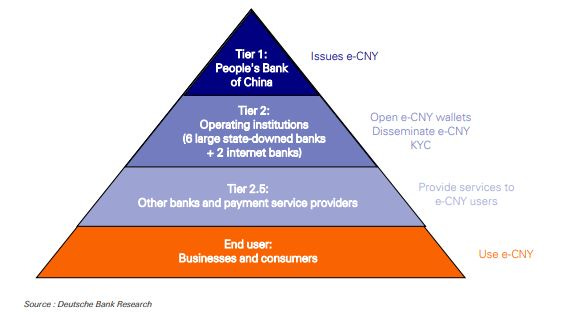

The digital yuan operates through a well-structured dual-layer framework. Issuance and distribution occur in two stages: the central bank and commercial banks, followed by commercial banks and retail. Essentially, the People's Bank of China distributes the digital yuan to commercial banks and other financial institutions, which then use the existing financial infrastructure to manage and distribute the digital currency to retail users. This structure allows the central bank to control the money supply while efficiently managing it through the established financial system.

However, the use of the digital yuan in Hong Kong is still in the pilot phase and is somewhat limited. For example, transaction limits are strict: individual payment amounts cannot exceed 2,000 yuan, the total daily transaction limit is 5,000 yuan, and the maximum wallet balance is capped at 10,000 yuan. Additionally, peer-to-peer (P2P) transfers are not possible. This cautious approach aims to expand the use of digital currency while maintaining financial stability. It is anticipated that this pilot project will reduce dependence on traditional banks and simplify regional transactions, benefiting both retail and corporate users.

3.2. Financial Industry Innovations: Standard Chartered's Blockchain-Based Euro Payments

In May, Standard Chartered Bank successfully conducted euro-based cross-border transactions between Hong Kong and Singapore using the blockchain-based payment system 'Partior.' This marked the first euro-based payment using blockchain technology. Partior operates a 24/7 real-time cross-border payment system, enhancing transaction speed by automating clearing and settlement processes through a blockchain ledger. During this process, Standard Chartered collaborated with Siemens, a Germany-based technology company, and iFAST, a Singapore-based fintech firm, to integrate blockchain technology into actual workflows, demonstrating its practical application.

3.3. Web3 Native Projects: Oobit's Crypto Payment System Using Tether and TON

Singapore-based Oobit aims to revolutionize the cross-border payment market with its 'Tap and Pay' feature, allowing users to make cryptocurrency payments as easily as Visa and Mastercard contactless payments. Oobit plans to support integration with external wallets and traditional payment systems, significantly reducing the gap between them. Currently, Oobit supports over 35 cryptocurrencies, including Bitcoin and Ethereum, and has secured investments from Tether and TON, with plans to collaborate further.

Oobit is expected to innovate cross-border payments, especially in retail, allowing users to make easy and fast payments while traveling abroad without incurring the typical 1-3% transaction fees. However, regulatory challenges may arise as many countries do not recognize cryptocurrencies as a payment method. Therefore, supporting CBDCs alongside cryptocurrencies may be necessary.

4. Conclusion

Recent developments, such as the introduction of China's digital currency e-CNY in Hong Kong and Standard Chartered's blockchain-based cross-border payments, highlight the dynamic changes in Asia's cross-border payment industry. Additionally, Ripple is expanding its influence in the Asian market, and several countries are actively developing their own CBDCs, further driving innovation in this sector.

Despite the dynamic market conditions, industry innovation led by Web3 companies is expected to be challenging. There are three main reasons for this. First, regulatory issues are the biggest obstacle. Cross-border payments involve technology spanning multiple countries, making it complex to persuade various stakeholders and apply it across diverse industry environments. Second, cooperation with governments is a significant challenge. Payments can impact national monetary policies, necessitating close collaboration with governments, which is not easy to achieve. Lastly, there is a lack of expertise. Cross-border payments are already dominated by participants with strong expertise, making innovation difficult.

Therefore, Web3 companies need to collaborate in an open innovation model with institutions possessing various expertise and with governments. In this model, Web3 companies would focus on specialized technological areas, while other entities handle operations and regulations. Such collaboration is expected to drive technological innovation in the cross-border payment industry.

Take a quick, 1-minute survey to enhance the weekly insights we provide. In return, get immediate access to the updated "2024 Country Crypto Matrix" by Tiger Research, featuring the latest global virtual asset market trends. Your participation helps us provide valuable content while you gain cutting-edge analysis.

Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn't harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research's reports, it is mandatory to 1) clearly state 'Tiger Research' as the source, 2) include the Tiger Research logo, and 3) incorporate the original link to the report. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.