Key Takeaways

Upbit delayed $PRL trading immediately after its listing announcement, following allegations of insider selling. Perle Labs stated the flagged tokens were ecosystem allocations; Upbit accepted the explanation and proceeded with the listing.

The explanation is difficult to verify, but no clear evidence of wrongdoing exists. Tokenomics discloses allocation amounts, not recipient identities. Ecosystem wallet ownership is known only to the project internally, and exchanges have no means to confirm it.

Had Upbit canceled the listing, it would have been compelled to apply the same standard retroactively to virtually every project listed domestically. Cancellation would also have amounted to a public admission of prior screening failure.

This structural gap is not new. As long as blockchain preserves anonymity by design, exchange-level due diligence alone cannot close it. The problem belongs to the industry as a whole.

Upbit announced the listing of Perle Labs’ $PRL token across its KRW, BTC, and USDT markets. Almost immediately, allegations emerged that team insiders had sold tokens ahead of the announcement, prompting a delay. Upbit’s official notice cited “clarification of circulating supply issues” as the reason for postponing trading. Shortly after, Upbit confirmed that the clarification process had been completed, and $PRL was officially listed.

Why Now?

Insider trading allegations are not uncommon in the crypto industry. What was uncommon this time was that an allegation alone was enough to delay a listing. The on-chain activity in question was as follows:

Approximately 90 million PRL was transferred from the original foundation wallet and distributed across five separate addresses.

Two of the five wallets sold before the KRW listing announcement; the remaining three sold after.

The timing led many to suspect the tokens were team holdings offloaded around the announcement. Perle Labs pushed back, stating the tokens were ecosystem allocations distributed within the published vesting schedule from external wallets.

But how could anyone confirm that?

Simple Analogy

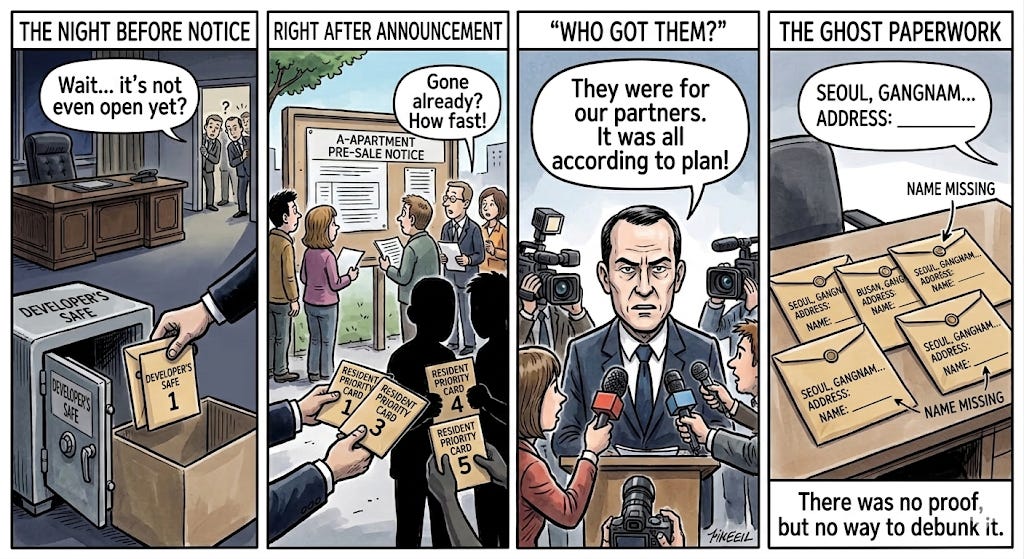

Imagine a condo development in a hot market. Before the public sales launch, five units quietly leave the developer’s inventory. Two are flipped the day before the announcement. Three more move right after.

People start asking: “Who got those units?”

The developer says: “Those went to a partner. It was always part of the plan.”

But the paperwork only has a mailing address, no name. There is no record of who actually received them. And there is nothing proving the developer is wrong.

Not a Cap Table

A cap table records who holds what and tracks every change over time. Tokenomics does not work that way.

Tokenomics is an allocation plan: total token supply divided into categories such as team, investors, ecosystem, and community, each with a stated percentage and unlock schedule. That much is public. That much is transparent.

But “Ecosystem: 20%” says nothing about who actually receives that 20%. It could go to partners, developers, or community contributors. There is no disclosure obligation, and most projects do not name recipients.

A cap table records who. Tokenomics records how much. It looks transparent, but the most consequential piece of information is absent. Who received the ecosystem allocation is known only inside the project. It could be a partner. It could be a founder’s family member. There is no way to know from the outside. Upbit is in the same position.

What exchanges can verify at the screening stage is total circulating supply and whether team and investor tokens are properly vested and locked. If those are in order, listing requirements are met. In Perle Labs’ case, team and investor wallets showed no irregularities. The ecosystem tokens that moved were distributed within structurally permitted parameters.

From Upbit’s position, canceling a listing on the basis of an unverifiable allegation, after a public announcement has already been made, is not a viable option. Applying that standard consistently would mean subjecting virtually every listed project to the same scrutiny retroactively. And the cancellation itself would amount to a public admission that the original screening had failed.

This is not a problem that surfaced for the first time today. The incident is a moment of visibility, not a new vulnerability. Remediation is clearly needed, but no realistic solution exists. Blockchain makes transaction history transparent while keeping recipient identities anonymous. That is not an oversight; it is the architecture. As long as that structure holds, exchange screening alone cannot fill the gap. This is an industry-wide problem.

Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.