The crypto market has grown, but retail investors are declining. We analyzed the entry barriers across 9 Asian markets with the largest potential user base, and how exchanges are responding. Read the full report now.

1. The Market Grew, but Retail Shrank

Since the U.S. spot ETF approval in 2024, institutional capital has flooded in. Companies are adding Bitcoin to their balance sheets. Exchanges are tokenizing U.S. large-cap stocks. The wall between traditional finance and crypto is breaking down on both sides. The market has clearly expanded.

But retail is moving in the opposite direction. Across countries, retail trading volume and user counts are declining.

In previous cycles, high altcoin returns pulled in new users. That engine is no longer running. Altcoins are not showing the same volatility as before. BTC dominance has reached roughly 60%. There is no mechanism left to attract new users; only existing participants remain.

Yet exchanges are deploying a range of strategies to bring in new users.

Exchanges call these potential entrants “crypto-curious”: people who are aware of crypto, interested in it, but have not yet invested. Given the population and internet penetration of major Asian countries, this latent pool numbers in the tens of millions. With existing users hitting a growth ceiling, the crypto-curious are the variable that determines the industry’s next phase.

Volatility is the most cited barrier. But volatility is a surface symptom, not the root cause. Equities are also volatile, yet people buy stocks, because government oversight exists, funds are protected, and society treats it as a legitimate investment. Crypto lacks all three.

Five core barriers keep the crypto-curious out:

Regulatory uncertainty: No clarity on legal protection. Some countries have clear rules; others have none.

Security risk: Fear of exchange hacks, disappearances, or asset freezes.

Tax burden: Unpredictable tax rates and potential policy changes.

Accessibility: Difficult to know where and how to start. Staking, DEX trading, and other complexities add friction.

Social perception: Crypto trading is viewed as “gambling.”

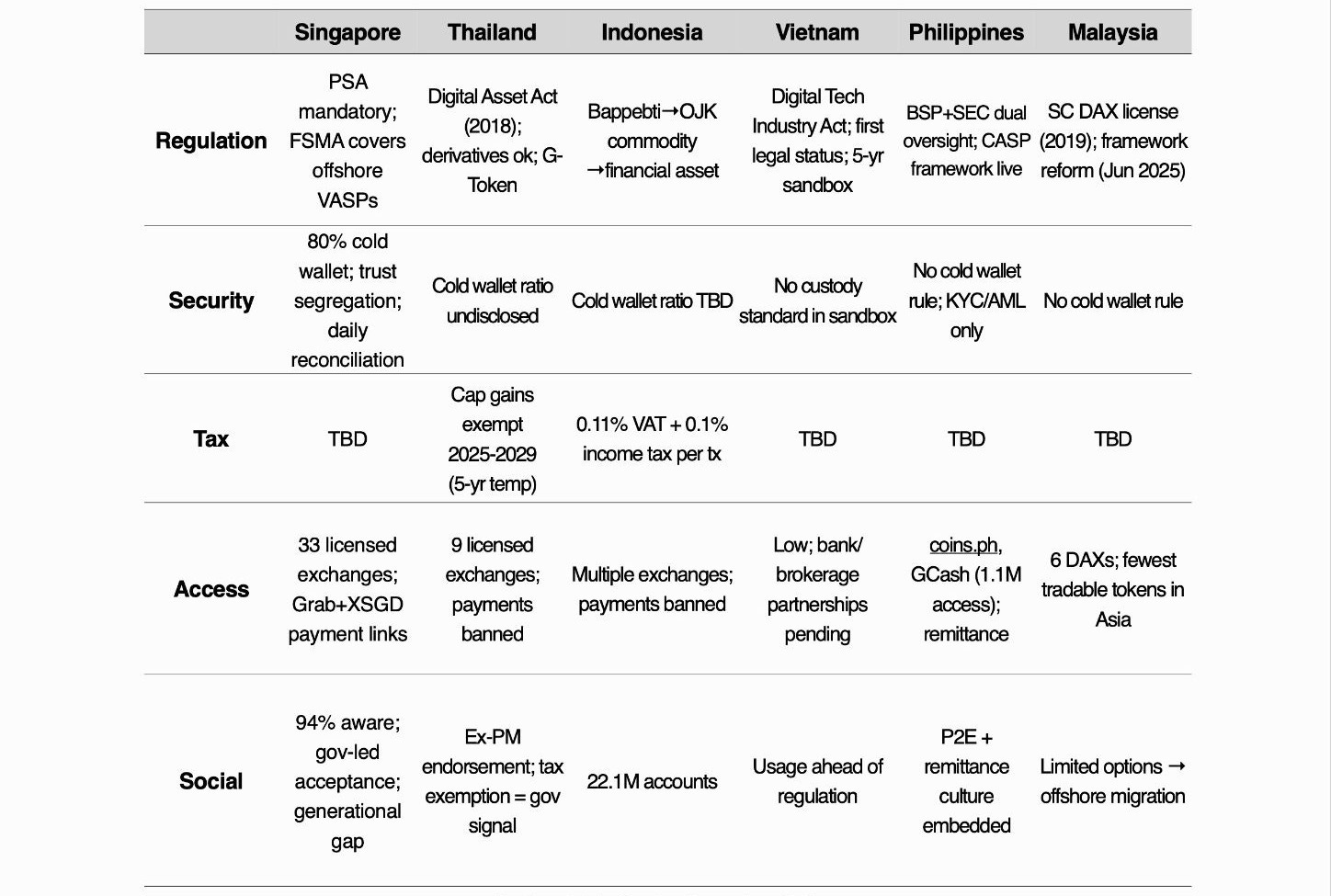

The eight Asian markets examined in this report each stall at a different barrier.

2. Crypto-Curious Analysis Across Major Asian Markets: Different Barriers in Every Country

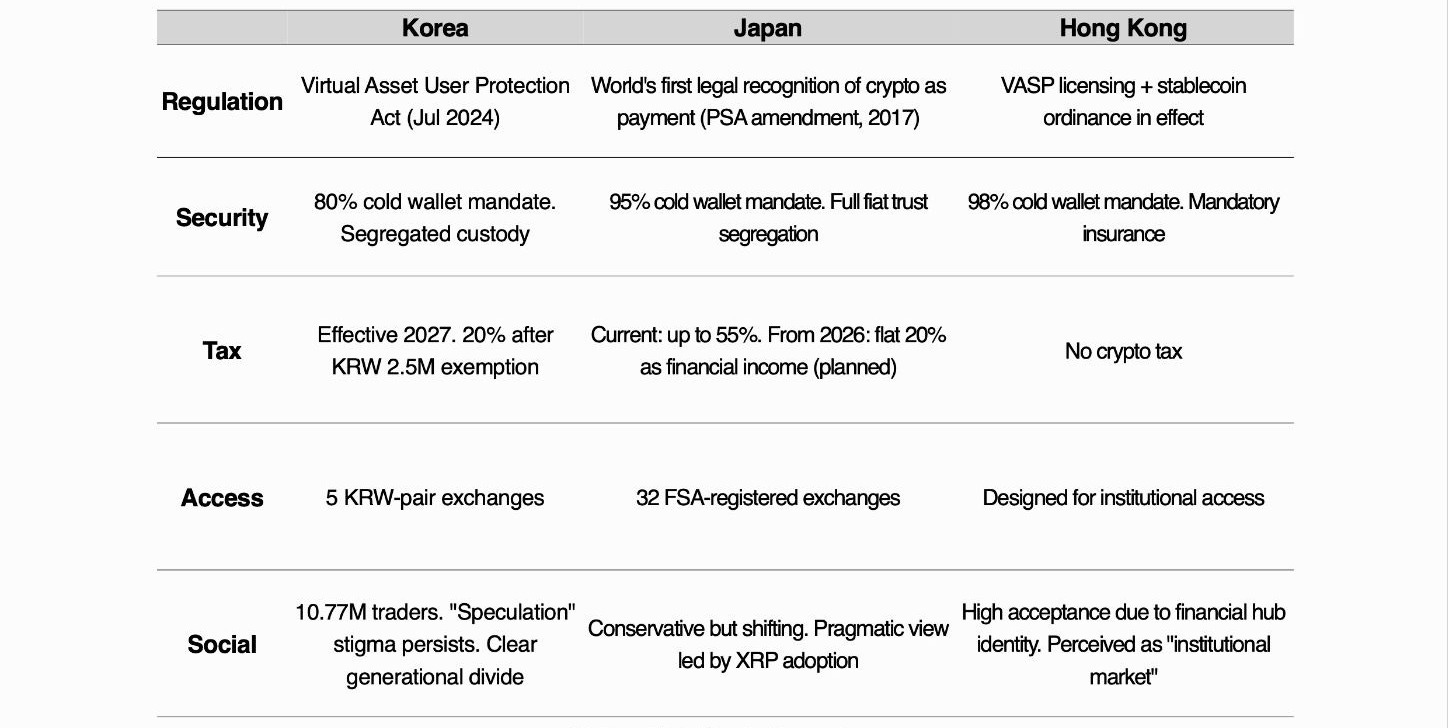

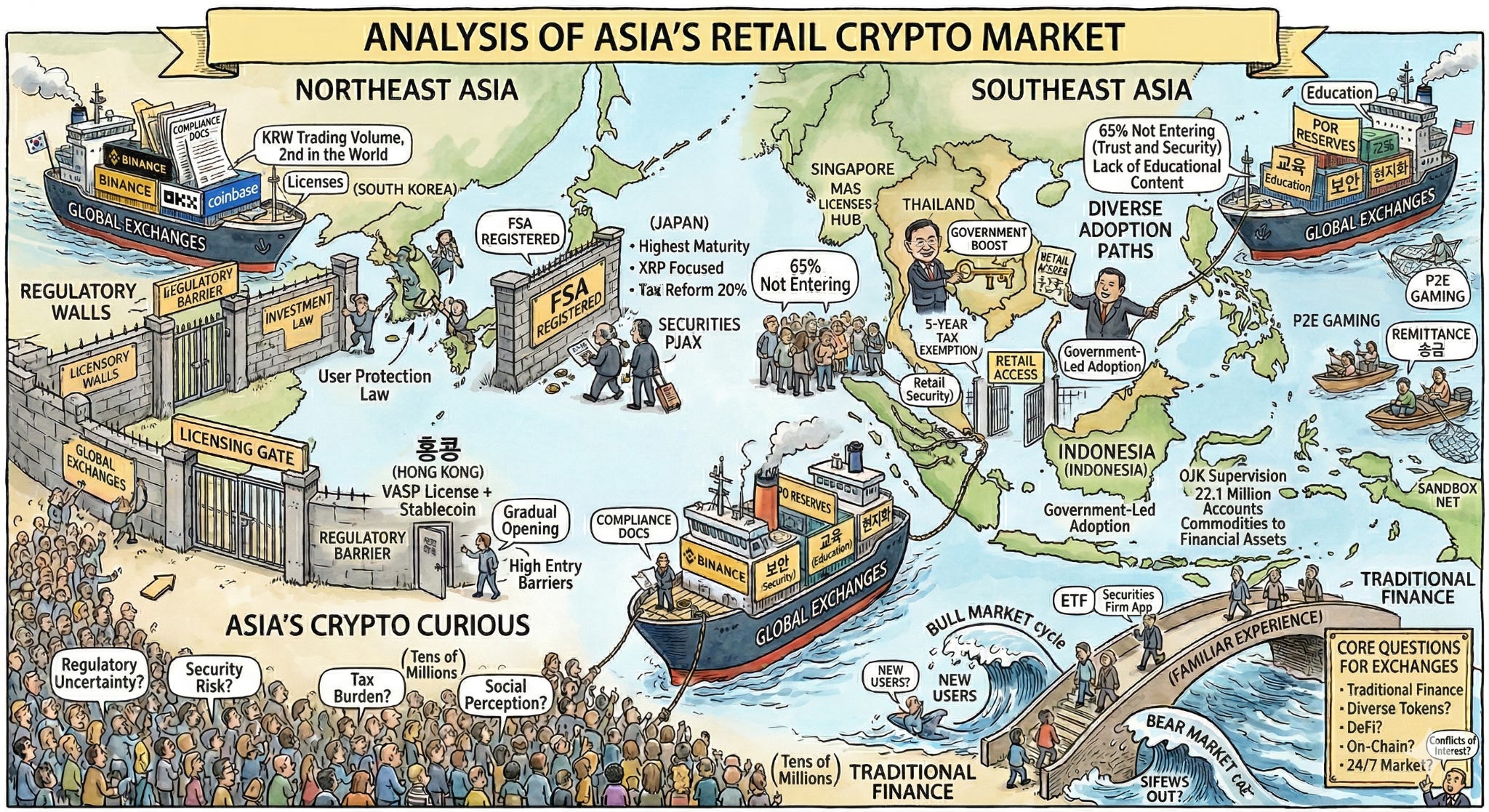

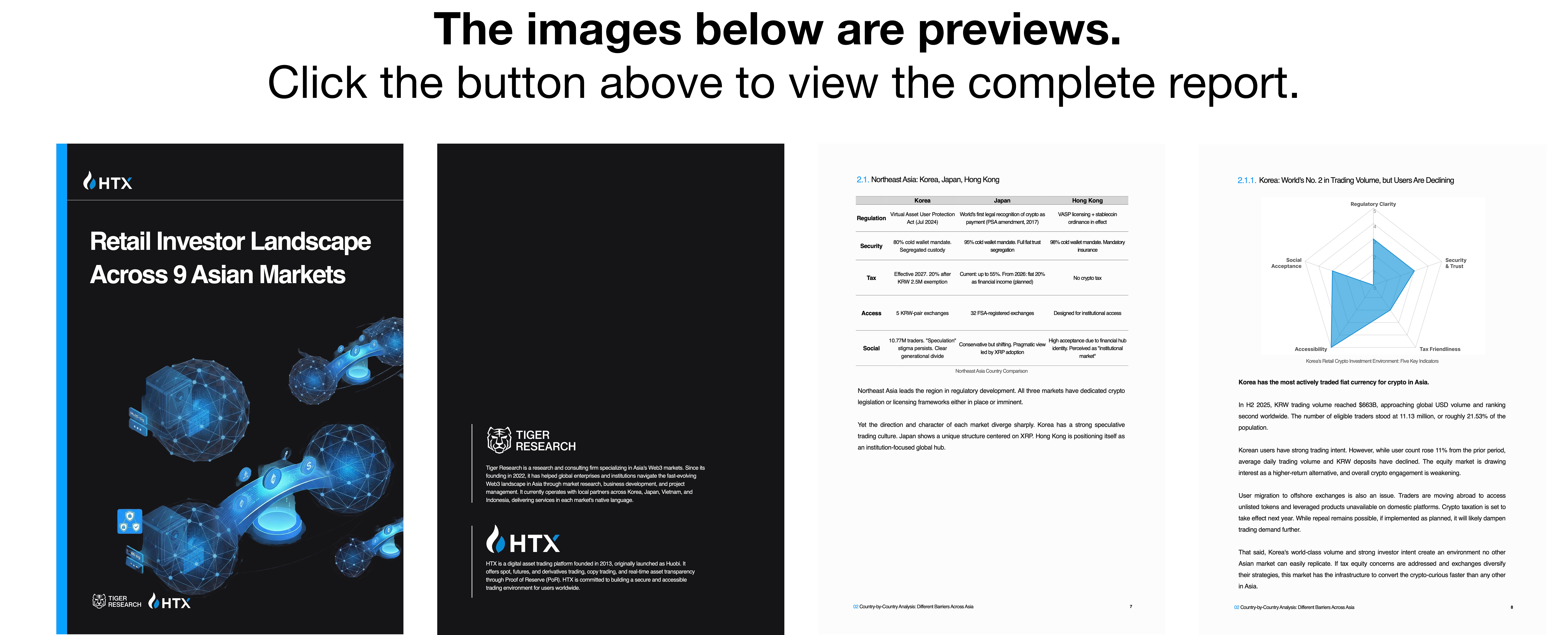

2.1 Northeast Asia: Korea, Japan, Hong Kong

Northeast Asia is where crypto regulation is advancing fastest in the region. All three markets either have dedicated legal frameworks or licensing regimes in place, or are about to introduce them.

But the direction of regulation and the character of each market differ entirely. Korea has a strong speculative trading culture. Japan shows a unique trading structure centered on XRP. Hong Kong is positioning itself as an institution-focused global hub.

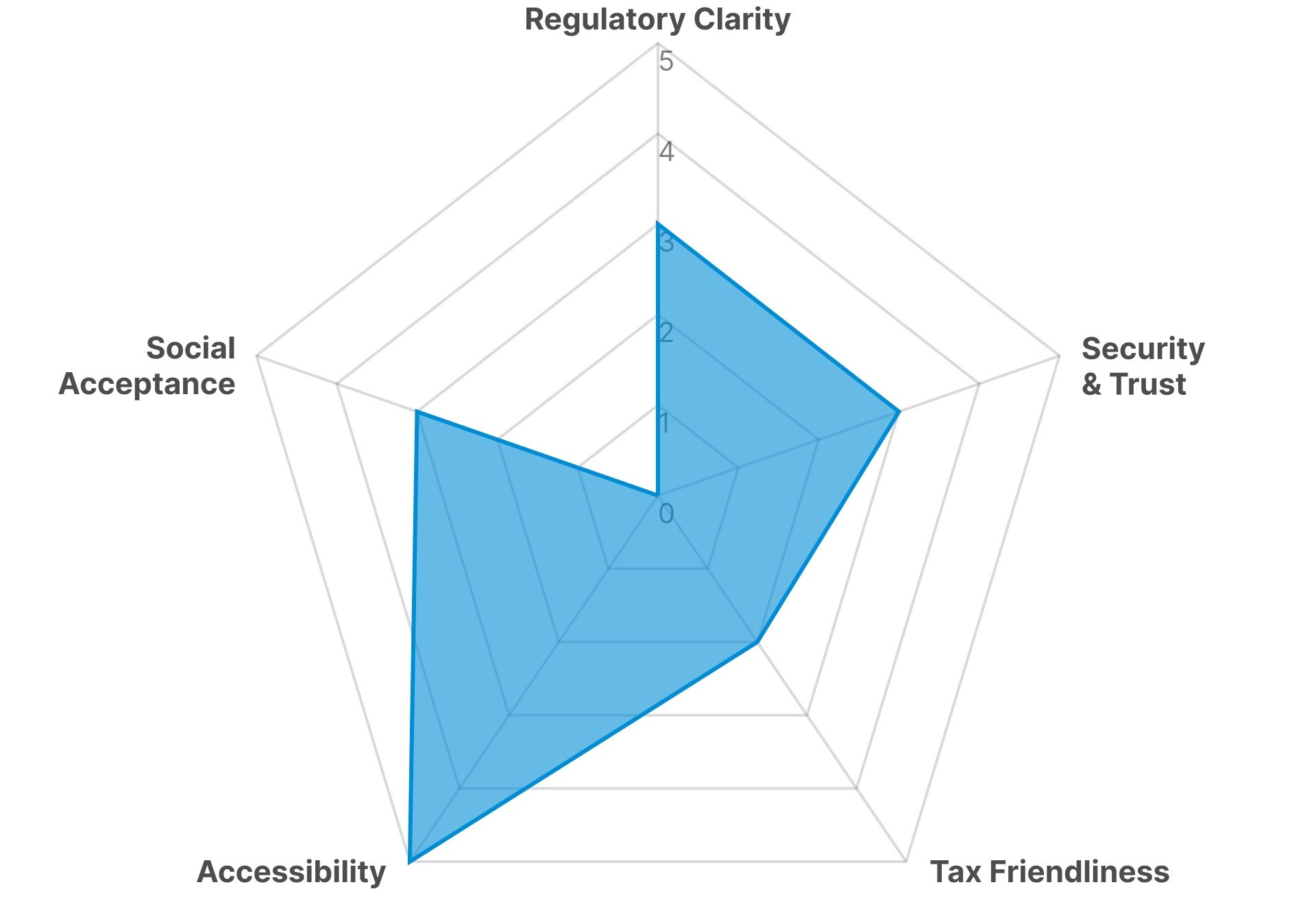

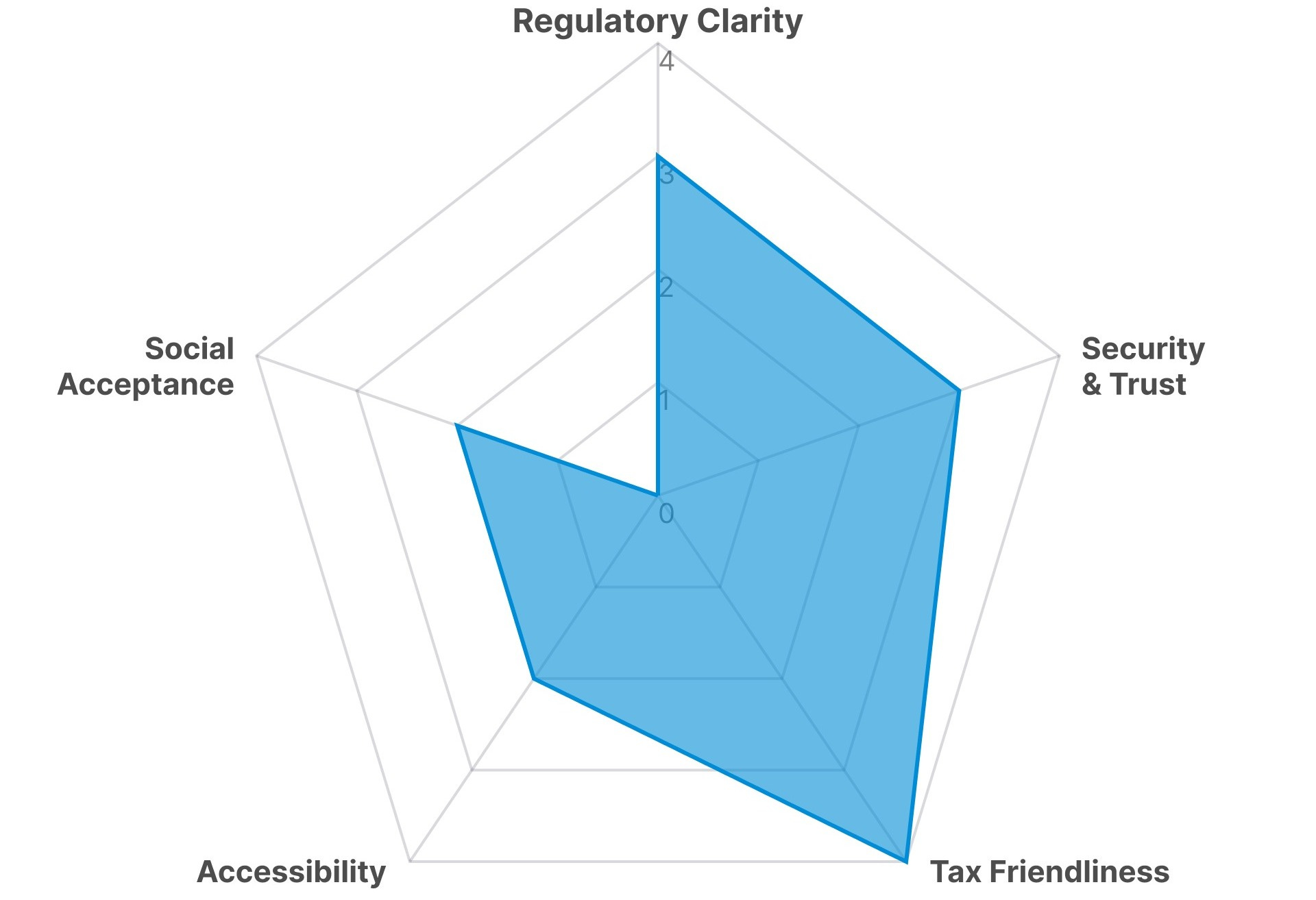

2.1.1. Korea: No. 2 in Volume, Declining Users

Korea has the most actively traded fiat currency for crypto in Asia.

In H2 2025, KRW trading volume reached $663B, nearly matching global USD volume and ranking second worldwide. The number of eligible traders stood at 11.13M, roughly 21.5% of the population.

Korean users have shown a strong willingness to trade crypto. However, while user counts rose 11% from the prior period, average daily trading volume and fiat deposits have declined. The equity market is emerging as a more attractive alternative, and interest in crypto is fading.

Users are also migrating to offshore exchanges to access unlisted tokens and leveraged products. Crypto taxation is scheduled for implementation next year. Because the proposed rules differ from existing equity tax treatment, there remains a possibility of repeal, but if enacted as planned, trading demand is expected to decline further.

Still, Korea’s position as the world’s second-largest trading market, combined with the aggressive investment appetite of Korean traders, creates an environment difficult for other Asian markets to match. If tax parity with equities is achieved and exchanges deploy diversified strategies, Korea’s established infrastructure makes it the market where crypto-curious conversion could happen fastest.

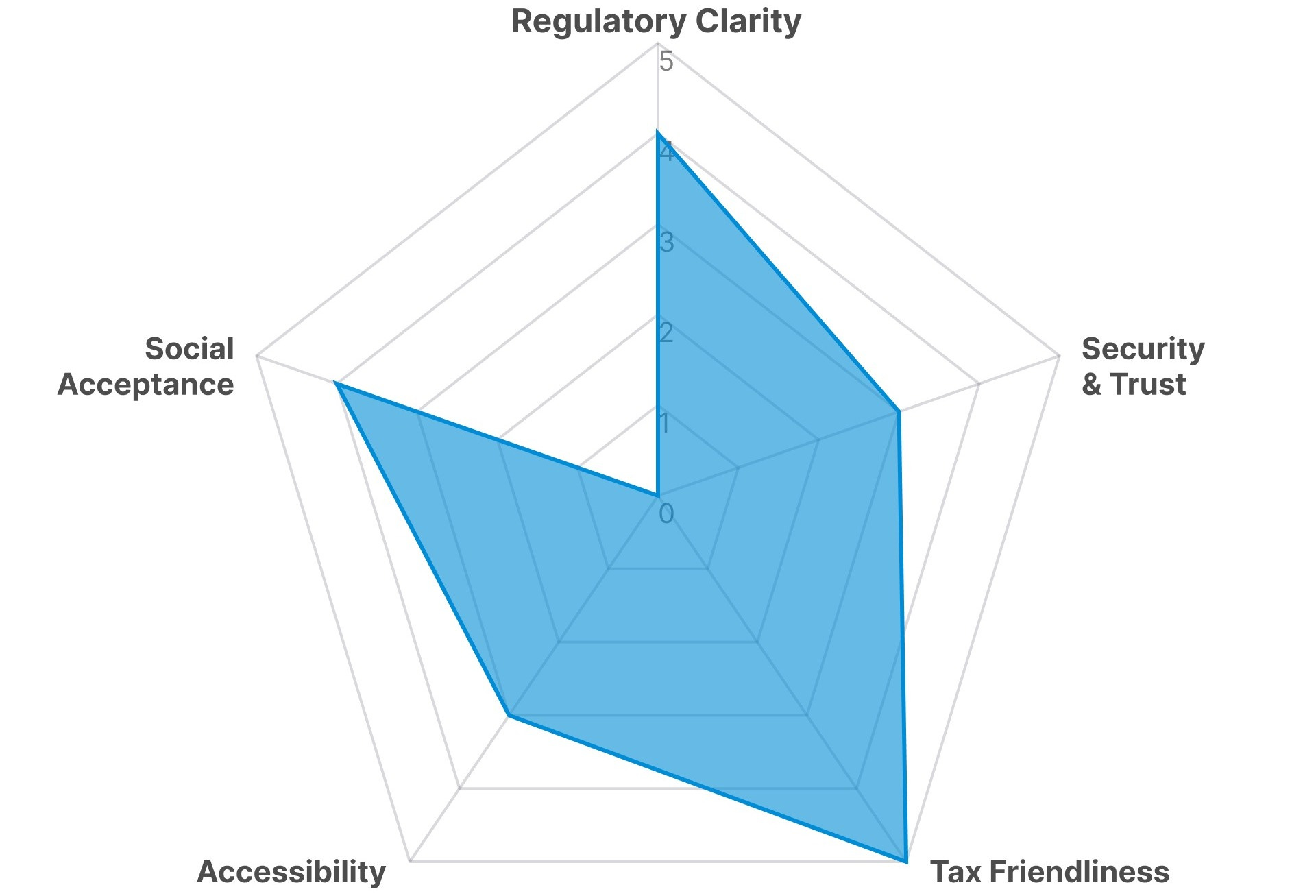

2.1.2. Japan: Safest and Most Expensive

Japan is the safest crypto market in Asia, and simultaneously the most expensive.

After losing roughly 850,000 BTC in the 2014 Mt. Gox hack, Japan became the first country to create an exchange licensing system. That lesson shaped the current structure. Exchanges must store 95%+ of client assets in cold wallets and hold all client fiat in fully segregated trust accounts.

There are 32 FSA-registered exchanges, 12M cumulative accounts, and JPY 5T in client deposits . The signal that “it is safe to enter” is stronger in Japan than anywhere else in Asia.

But once inside, taxes are waiting. Crypto gains are currently classified as miscellaneous income, subject to a maximum rate of 55%. Earning JPY 100M means JPY 55M in tax. The same gain from equities would be taxed at roughly 20%, or JPY 20M. A 2.7x gap. Asia’s safest market imposes Asia’s highest tax.

This contradiction is the core barrier for Japan’s crypto-curious. Confidence in safety is sufficient. But safety comes at a cost. You can enter, and you are protected, but you may have nothing left.

The market structure is also distinctive. From July 2024 to June 2025, XRP purchases on exchanges in JPY totaled roughly $21.7B, 4.6x that of BTC ($4.7B). Japan is the only market globally where a single altcoin overwhelms Bitcoin.

This is a product of the strategic partnership between SBI Holdings and Ripple. In Japan, XRP is accepted not as a speculative asset but as a crypto asset with real utility. In a savings-oriented, speculation-averse society, crypto gained a foothold in a fundamentally different way than in Korea.

Yet social adoption remains slow. Among individual investors with investment experience, only 7.3% hold crypto assets. By contrast, corporations are embracing crypto actively. Metaplanet, dubbed “Asia’s Strategy,” is accumulating Bitcoin as a strategic asset, and SBI Holdings plans to list a BTC+XRP dual-asset crypto ETF on the Tokyo Stock Exchange.

A decisive variable exists: two reforms scheduled for April 2026. One reclassifies crypto assets under the Financial Instruments and Exchange Act (FIEA). The other changes the tax rate to a flat 20% on financial income, identical to equities. If both take effect simultaneously, the largest barrier for Japan’s crypto-curious disappears.

With these changes pre-announced, there is no reason for the crypto-curious to enter now under a potential 55% tax rate.

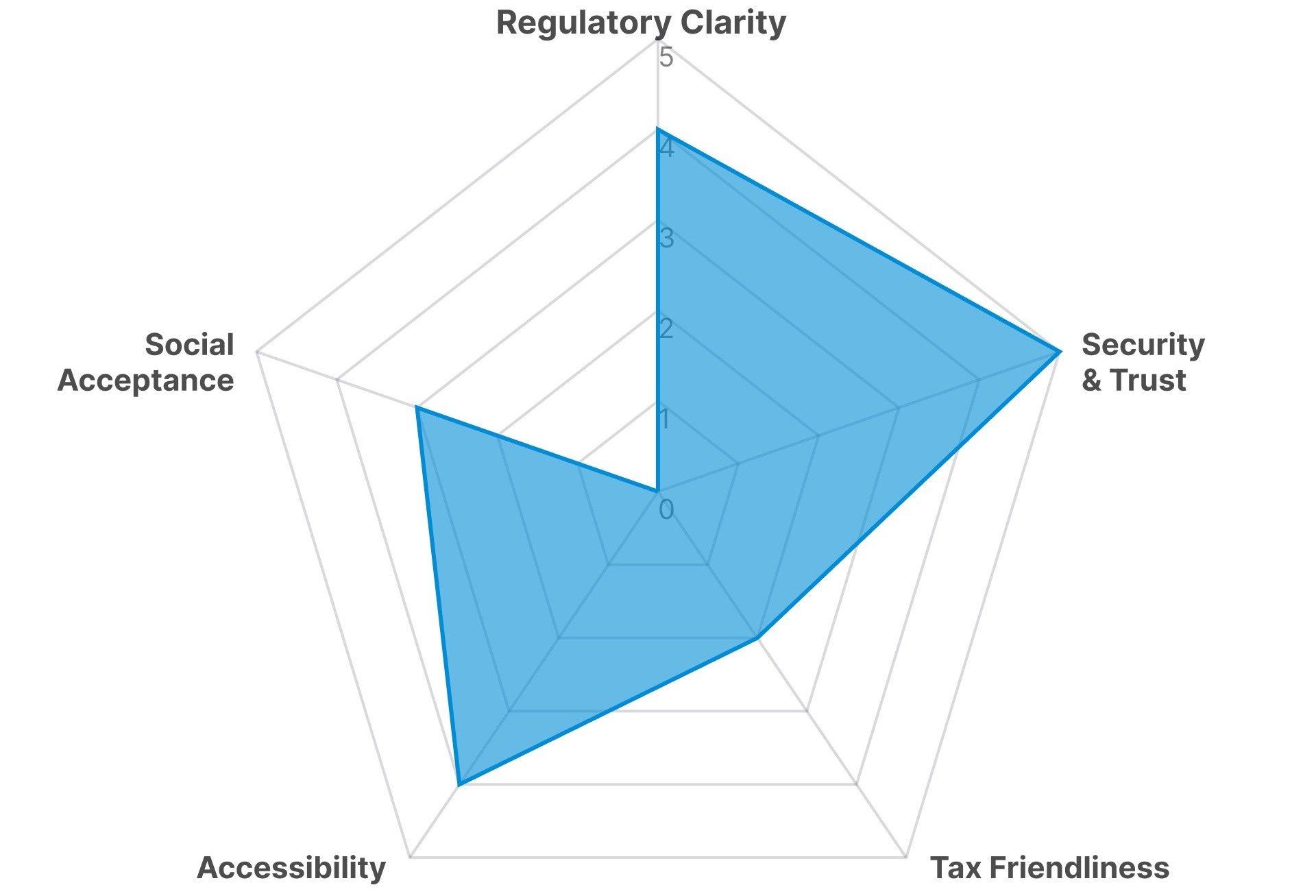

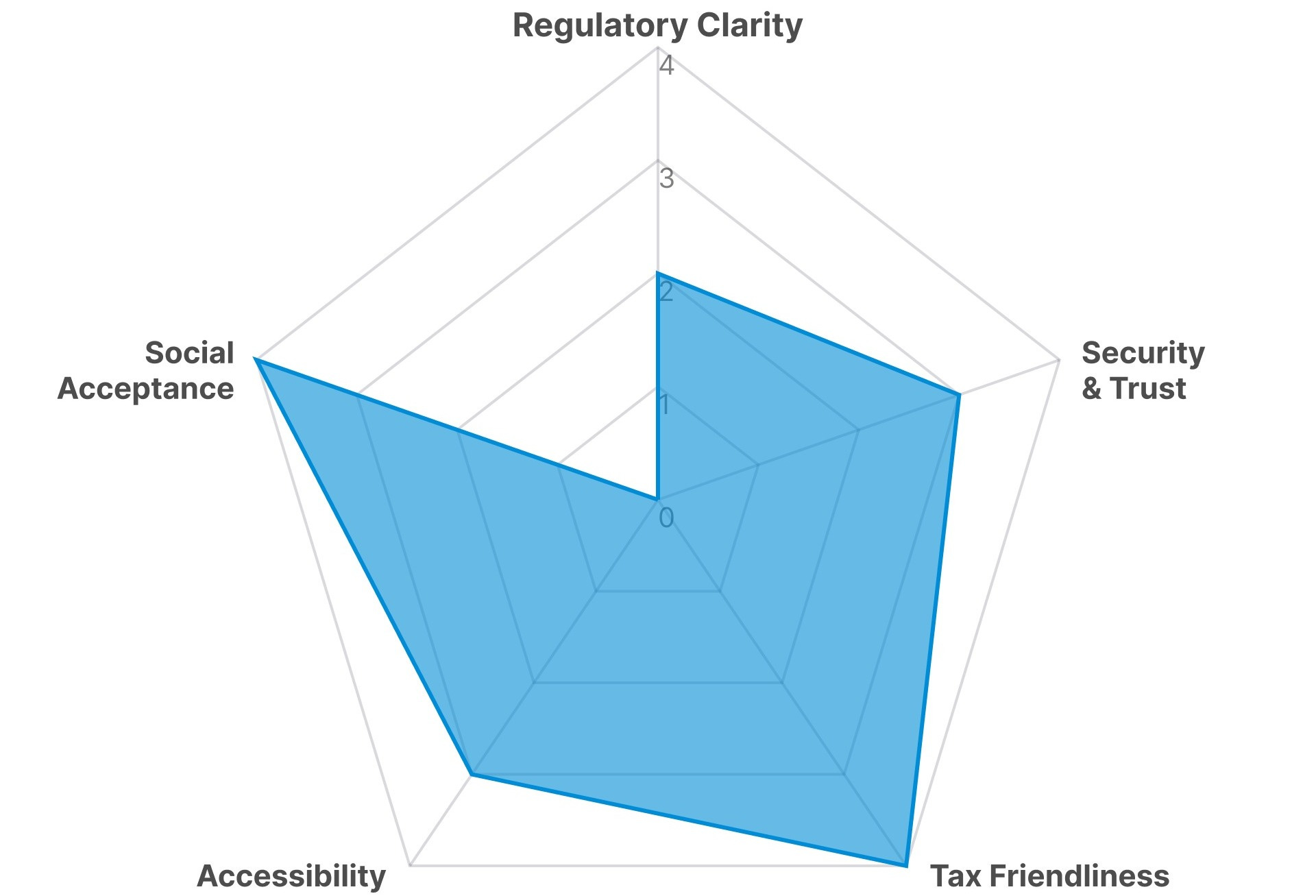

2.1.3. Hong Kong: Three Barriers Cleared, Access Still Blocked

Hong Kong has resolved more of the crypto-curious’s key barriers than any other market in Asia. Regulation is clear, security standards are high, and there is no tax burden. No other Asian market meets all three at the highest level simultaneously.

The SFC has operated the VATP licensing framework since 2023. In February 2025, it published the ASPIRe roadmap outlining the future regulatory direction. In August of the same year, a stablecoin regime was announced, with the first license expected in early 2026.

Exchanges must store 98%+ of client assets in cold wallets. Mandatory insurance and annual cybersecurity audits are required. There is no crypto tax. In 2024, Hong Kong approved Asia’s first Bitcoin/Ethereum spot ETFs.

Regulation, security, and tax are largely resolved. The remaining problem is accessibility.

As of February 2026, 12 platforms hold SFC licenses, but their services primarily target professional investors with assets of HKD 8M (roughly KRW 1.3B) or more. Unlike Korea, where users can download an app and buy immediately, Hong Kong’s structure does not allow this. Regulatory quality is among Asia’s best, but the door into that regulatory framework is narrow.

Social perception occupies a unique position. Thanks to the city’s identity as a global financial hub, the “gambling” stigma is weaker than in Korea or Japan. But there is a strong perception that crypto is “a domain for professionals.” No social stigma, but no social familiarity either. The psychological distance is too large for the crypto-curious to feel “maybe I should try it.”

Pathways for change are opening. The SFC introduced a shared-liquidity framework allowing licensed platforms to access offshore order books. Staking services are conditionally permitted. Dealer and custody licensing regimes are scheduled for legislative consultation in 2026. Available products and channels are widening.

In one sentence: Hong Kong has resolved three of the five barriers, but the fourth, accessibility, is neutralizing the other three. No matter how safe and tax-free, if you cannot enter, it is meaningless. Hong Kong’s task is to widen the door so that more people can experience the trust it has already built.

2.2. Southeast Asia: Singapore, Thailand, Indonesia, Vietnam, Philippines, Malaysia

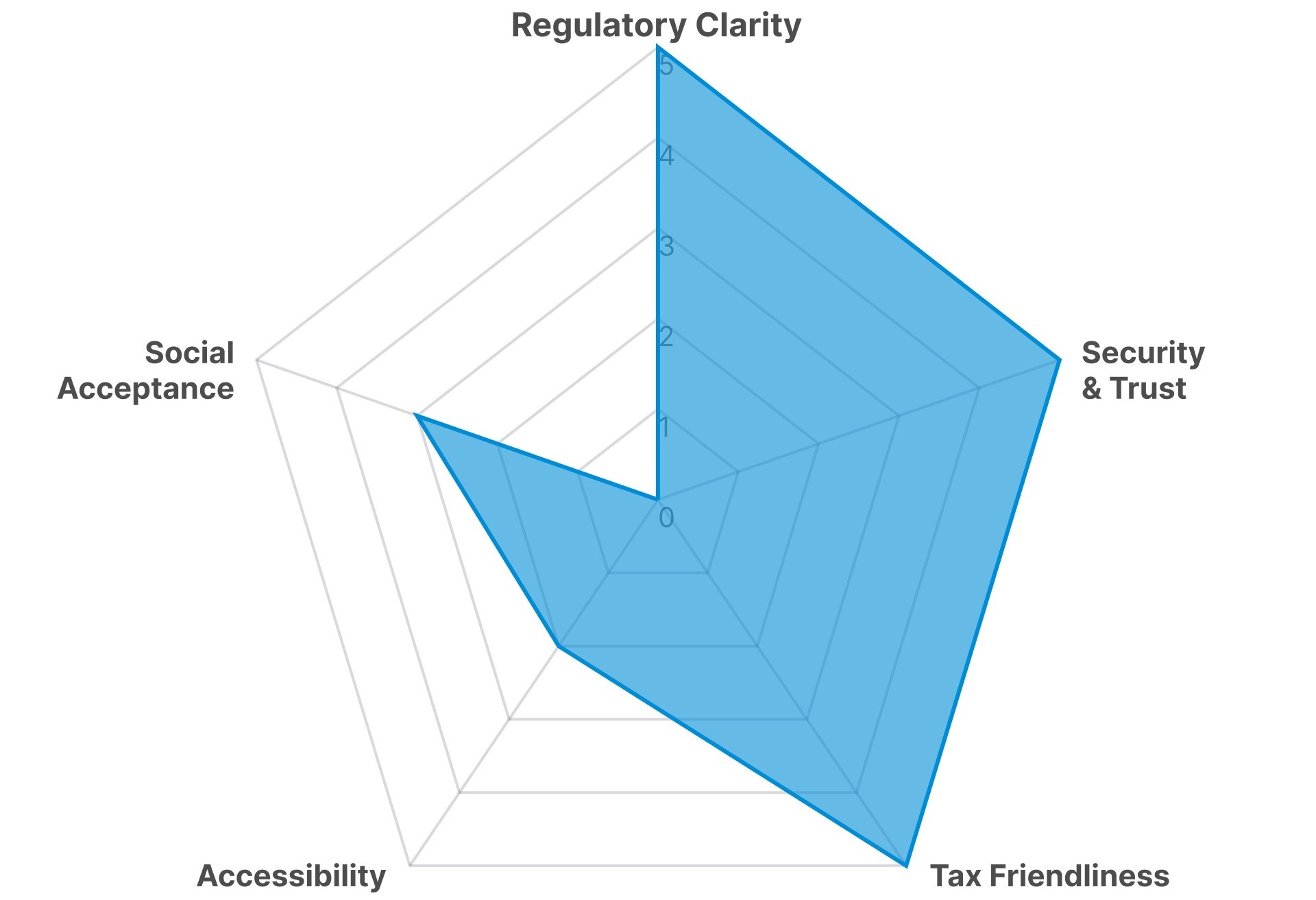

2.2.1. Singapore: All Conditions Met, Yet 65% Stay Out

Singapore is the most balanced market among the eight countries in this report across all five barrier dimensions: regulation, security, tax, accessibility, and social perception. None is notably weak.

MAS operates Asia’s most consistent licensing regime. In June 2025, it extended licensing requirements even to operators serving only overseas clients. Exchanges must segregate client assets in trust, and Singapore has completed its FATF mutual evaluation. There is no crypto tax.

Real-world usage is expanding. Grab has integrated stablecoin XSGD payments. MAS has piloted tokenized government bonds, and the three major banks have tested CBDC-based interbank lending. Crypto is extending into everyday finance within the regulated framework.

By these measures, there should be no reason for the crypto-curious to stay out. Yet the numbers tell a different story. Crypto awareness stands at a record 94%, but actual ownership is just 29%. The remaining 65% are Singapore’s crypto-curious.

These 65% are not uninformed. They are aware, have access, face no social stigma, and still choose not to participate. Their top cited barrier is market volatility (68%), and their No. 1 criterion for choosing an exchange is “trust and security” (65%), above fees.

Singapore is an instructive counterexample. Even with nearly all institutional barriers removed, 65% remain outside the market. The fact that crypto-curious conversion cannot be achieved by barrier removal alone is a point other Asian markets should note.

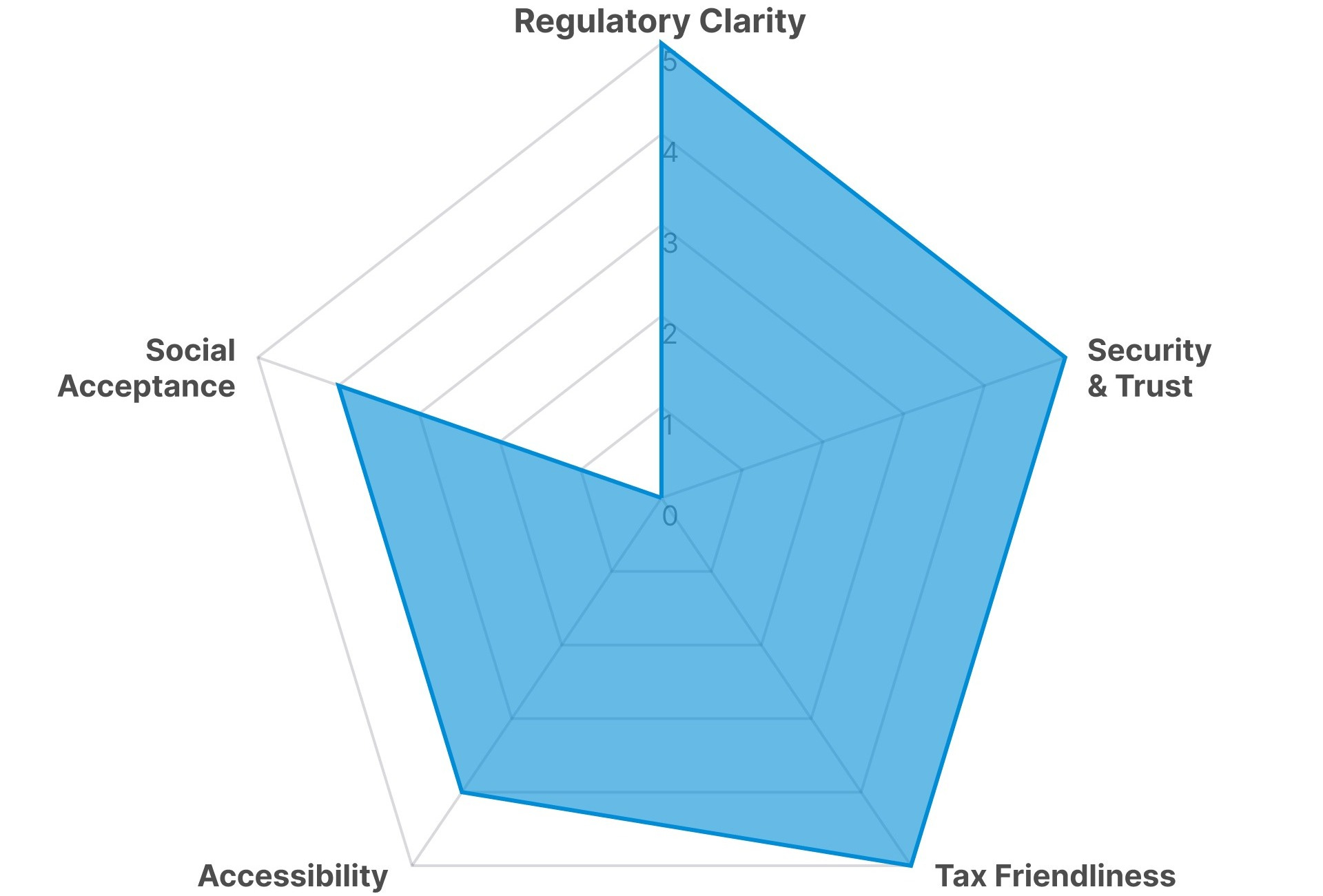

2.2.2. Thailand: Government-Led Market Opening

Thailand is the market in Asia where the government is most directly signaling “it is okay to enter.”

In January 2025, the government exempted personal income tax on crypto trading gains through licensed exchanges for five years. In the same month, it permitted mutual funds and private funds to invest in crypto. Since then, it has cut taxes, opened institutional capital channels, and the government itself has issued digital assets.

Thailand’s crypto user base is approximately 13M, about 18% of the population. The 2018 Digital Asset Business Emergency Decree established a legal framework early by Asian standards, and the SEC has licensed 9 exchanges. THB-based stablecoin trading volume reached $9.4B, second only to KRW in APAC. This is no longer mere permissiveness; it is active promotion.

Regulatory enforcement operates on two fronts. In April 2025, offshore regulation blocked 5 unauthorized foreign platforms including Bybit and OKX. In July, it allowed securities firms to offer investment token services and launched a public consultation on crypto derivatives. The approach: block the illegal, widen the legal.

The government’s role in shaping social perception is also significant. Former PM Thaksin Shinawatra publicly emphasized the need for crypto regulation and praised the Phuket crypto payment pilot positively. The perception forming is: “If the government exempts taxes on it, it must be acceptable.” Opening brokerage channels so existing equity investors can access crypto through familiar pathways is also aiding conversion.

One element is missing: payments. Since 2022, using crypto as a payment method has been prohibited. The TouristDigiPay sandbox allows foreign tourists to convert crypto to baht, and the Bank of Thailand is running a separate baht-stablecoin sandbox. But Thai consumers still have no daily crypto payment experience.

Thailand’s defining feature is that the government is removing crypto-curious barriers from the top down: tax exemption, G-Token issuance, institutional channel opening, derivatives introduction. Government signals this proactive are rare in Asia. The remaining task is the transition from “an asset you trade” to “an asset you can spend.” The lifting of the payment ban could be the next inflection point for Thailand’s crypto-curious.

2.2.3. Indonesia: From Commodity to Financial Asset

In January 2025, Indonesia changed crypto’s identity. Oversight was transferred from the Commodity Futures Trading Supervisory Agency (Bappebti) to the Financial Services Authority (OJK), reclassifying crypto from a “commodity” to a “digital financial asset.” This is not a simple jurisdictional change. OJK oversees banks, insurance, securities, and pension funds. Crypto has been elevated to the same level as equities and bonds.

The structure has shifted from exchanges making their own listing decisions to a centralized Bourse determining the list of eligible crypto assets. Mandatory security staffing, prohibition on using loans as a capital source, and strengthened consumer and data protection obligations were also introduced. Regulation has tightened, but it simultaneously signals that crypto is now a “government-recognized financial product.”

Transition-period uncertainty is unavoidable. The transition window runs through January 2027, and regulatory interpretation gaps may emerge in the interim. As in Thailand, use as a payment method is prohibited due to currency law designating the rupiah as the sole legal tender.

Indonesia’s potential lies in its population. Of its 280M population in 2025, the crypto account penetration rate remains in single digits. The remainder represents the market’s latent crypto-curious. The OJK transfer is the strongest institutional signal to this group that crypto has been “recognized as a financial product.” For this signal to translate into actual conversion, the transition period must conclude smoothly.

The next chapter for this 280M-person market depends on whether the OJK regime stabilizes.

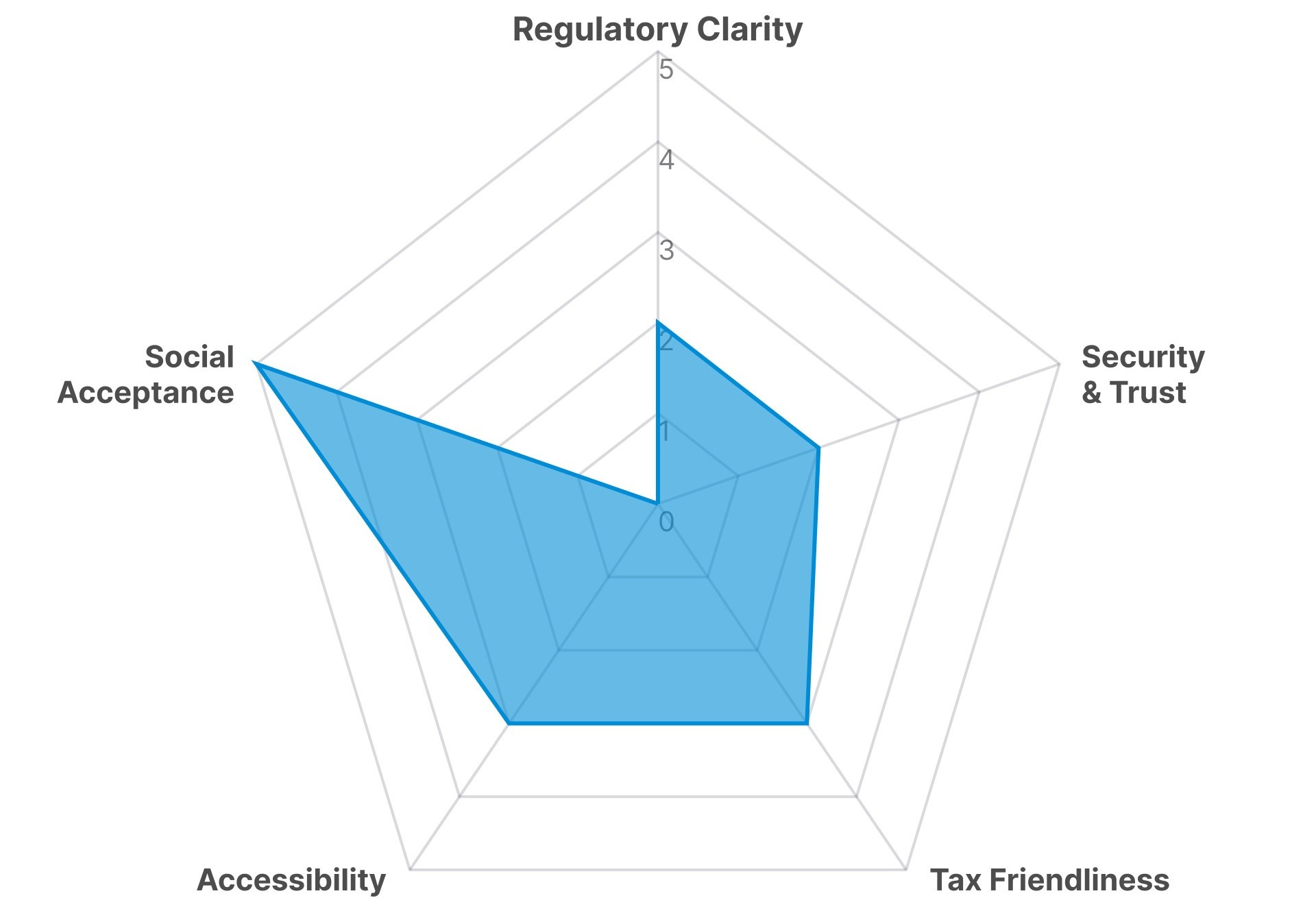

2.2.4. Vietnam: People Entered First, Regulation Is Catching Up

Vietnam’s sequence is the reverse of most markets. Typically, regulation comes first and users follow. In Vietnam, people entered the crypto market first, and regulation is now catching up.

For Vietnamese users, crypto is already close to everyday finance. It has penetrated daily life through remittances, gaming, savings, and other channels.

In response, the government passed the Digital Technology Industry Act through the National Assembly in June, officially recognizing digital assets as property under civil law, enabling ownership, transfer, inheritance, and legal protection. Additionally, in September 2025, a five-year (2025-2030) pilot program for the crypto asset market was introduced. The shift is from a prolonged regulatory vacuum directly to a comprehensive framework.

However, the institutional foundation is still in its earliest stage. Investor protections apply only within the sandbox on a limited basis, and detailed rules on exchange security standards and asset segregation obligations are still being developed. Exiting the FATF grey list remains a challenge; while on the list, international partnerships face constraints.

Accessibility is changing rapidly. As of early 2026, the Ministry of Finance is leading pilot licensing procedures for approximately five exchanges. Bank-affiliated entities such as Techcombank (TCEX), VP Bank, and LP Bank, as well as securities-firm affiliates like VIX Securities (VIXEX), are leading the process. The minimum capital requirement has been set at $400M, creating a high entry bar and ensuring the financial stability of approved operators.

Previously, offshore platforms like Binance dominated the market, but a shift toward locally licensed exchanges is likely. For the first time, a regulated entry path is opening in a market where large-scale adoption already occurred outside any regulatory framework.

Vietnam’s five-barrier profile shows overwhelmingly high social acceptance with the rest trailing, an extreme imbalance. But the direction of that imbalance matters. This is not a market where regulation needs to be built to drive adoption; it is one where adoption is already high and regulation must catch up. If the sandbox operates smoothly and detailed rules are established, the fastest institutional transition could occur atop an already-formed base.

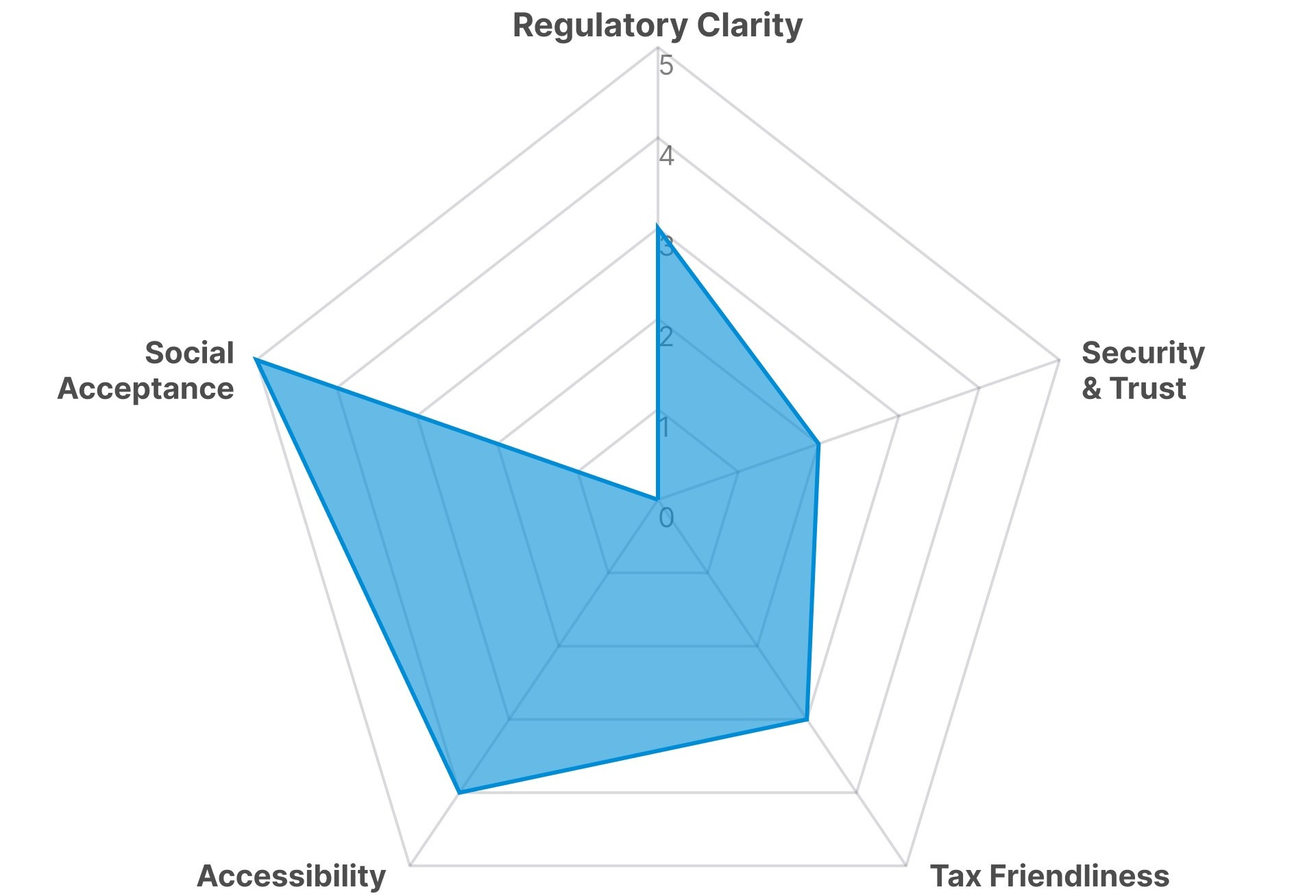

2.2.5. Philippines: A Crypto Market Built by Daily Life, Not Investment

The Philippines is the market among the eight where the concept of “crypto-curious” applies most differently. In other markets, the crypto-curious are people who are interested but have not entered. In the Philippines, there are more people already using crypto without realizing it.

Adoption was driven by daily life, not investment. During the pandemic, P2E gaming became young people’s first contact with crypto, and the world’s largest overseas remittance demand fueled the growth of stablecoin-based remittance channels. Crypto functions as living infrastructure, not an investment asset.

Social acceptance is already sufficient. The issue is the institutional protection built on top of it. BSP has frozen new VASP license issuance since September 2022. Despite an additional extension in September 2025, only 9 VASPs exist. The SEC implemented the CASP framework in July 2025, introducing minimum capital, asset segregation, and marketing regulations, but it remains in early stages.

Security risk is this market’s most pronounced weakness. The SEC has gone as far as requesting app store removal of unregistered platforms, but social media phishing scams persist. In a structure where real-world usage substitutes for trust, if institutional protection fails to follow, that trust can collapse with a single incident.

Positive developments are underway. The Philippines has exited the FATF grey list. UnionBank and GoTyme Bank obtained licenses as moratorium exceptions and offer crypto trading within banking apps. A strategic Bitcoin reserve bill has been introduced in the House. President Marcos Jr.’s public support for digital innovation is also building political legitimacy.

The Philippines’ profile resembles Vietnam in showing high social acceptance with low regulation and security, but the nature differs. Vietnam is building new institutions where none existed; the Philippines has locked the door on institutions that already exist. If the VASP moratorium is lifted and the CASP framework takes hold, institutional trust can be layered onto the real-world usage base already in place.

2.2.6. Malaysia: Regulation Exists, but Options Do Not

Malaysia is a rare case where a regulatory framework exists but the market has failed to grow.

The Securities Commission (SC) has issued Digital Asset Exchange (DAX) licenses since 2019, with basic protections including KYC/AML, asset segregation, and periodic audits in place. There is no crypto tax. On paper, the institutional framework is reasonable.

The problem is that too little can be done within it. Only 6 DAX operators are registered with the SC, and the number of tradable tokens is among the most limited in Asia. DeFi and derivatives have not been incorporated into the regulated framework. Total DAX trading value in 2024 was RM 13.9B (approximately $3.1B), up 2.6x YoY but small in absolute terms compared to Thailand or Indonesia.

When choices are limited, users go elsewhere. According to the SC, 996 complaints related to unregistered DAX platforms have been filed since 2019. Investors seeking a wider range of tokens and products are moving to unregistered offshore platforms. Regulation provides protection but simultaneously narrows the market’s options, driving leakage to unregulated spaces.

The SC has acknowledged this problem and in June 2025 announced a revised DAX framework. It is simultaneously pursuing a liberalized listing framework to shorten new token listing procedures and strengthened capital adequacy and asset segregation requirements. The Prime Minister’s Office has also approved the establishment of a Digital Asset and AI Advisory Committee, signaling movement at the industrial strategy level, not just regulation.

For Malaysia’s crypto-curious, this market is “possible but not compelling enough.” Regulation protects the market, but it is also capping its growth. Whether the revised DAX framework can raise that ceiling is Malaysia’s next question.

3. How Exchanges Are Targeting the Crypto-Curious

The next question is how global crypto exchanges are trying to enter these different markets. As shown above, Asia is not a single market. Regulation, investor protection levels, and social perception vary entirely by country. A single strategy cannot address all of Asia.

The challenge for global exchanges does not end at “how to grow users.” What matters is what to offer the crypto-curious in each market and how to deliver it.

3.1. Securing Licenses: The Right to Exist in the Market

The priority is securing the right to operate in a market. As regulation takes shape across Asia, operating without a license is becoming impossible.

This shift is already in motion by country. Thailand blocked 5 unauthorized offshore platforms in 2025. Singapore mandated local licensing even for operators serving only overseas clients. “Comply or be removed” has moved from rhetoric to reality.

Exchange strategies fall broadly into two approaches.

The first is volume-based expansion: acquiring licenses across as many jurisdictions as possible to maximize global coverage. Binance’s 20+ licenses and OKX’s MiCA-based coverage across 30 EU countries exemplify this model. License count itself becomes market access.

The second is strategic concentration: establishing regulatory compliance as a trust anchor in select markets. Coinbase’s FINRA-registered U.S. subsidiary building a compliance-first brand is the primary example. HTX is also systematically securing footholds in strategic locations including Australia, Lithuania, and Dubai.

However, in markets like Korea and Japan that require registration under domestic law, global licenses do not apply. Korea requires VASP registration under the Special Financial Transactions Act; Japan requires FSA registration. Apart from Binance’s acquisition of Gopax, few precedents exist.

At the same time, exchanges that fill the regulatory gaps across Asia can position themselves first for the region’s growth.

Regardless, exchanges must continue pursuing market entry. The fact that “I am trading on a licensed exchange” itself lowers the psychological barrier for the crypto-curious. Thailand’s 5-year tax exemption applying only to trades on SEC-licensed exchanges follows the same logic. Being inside the regulatory framework is now a competitive advantage.

3.2. Transparency and Security: Can I Trust Them with My Money?

Licenses alone are not enough. FTX collapsed under regulation. If securing the right to exist is step one, the next step is answering the question: “Can I trust this exchange with my money?”

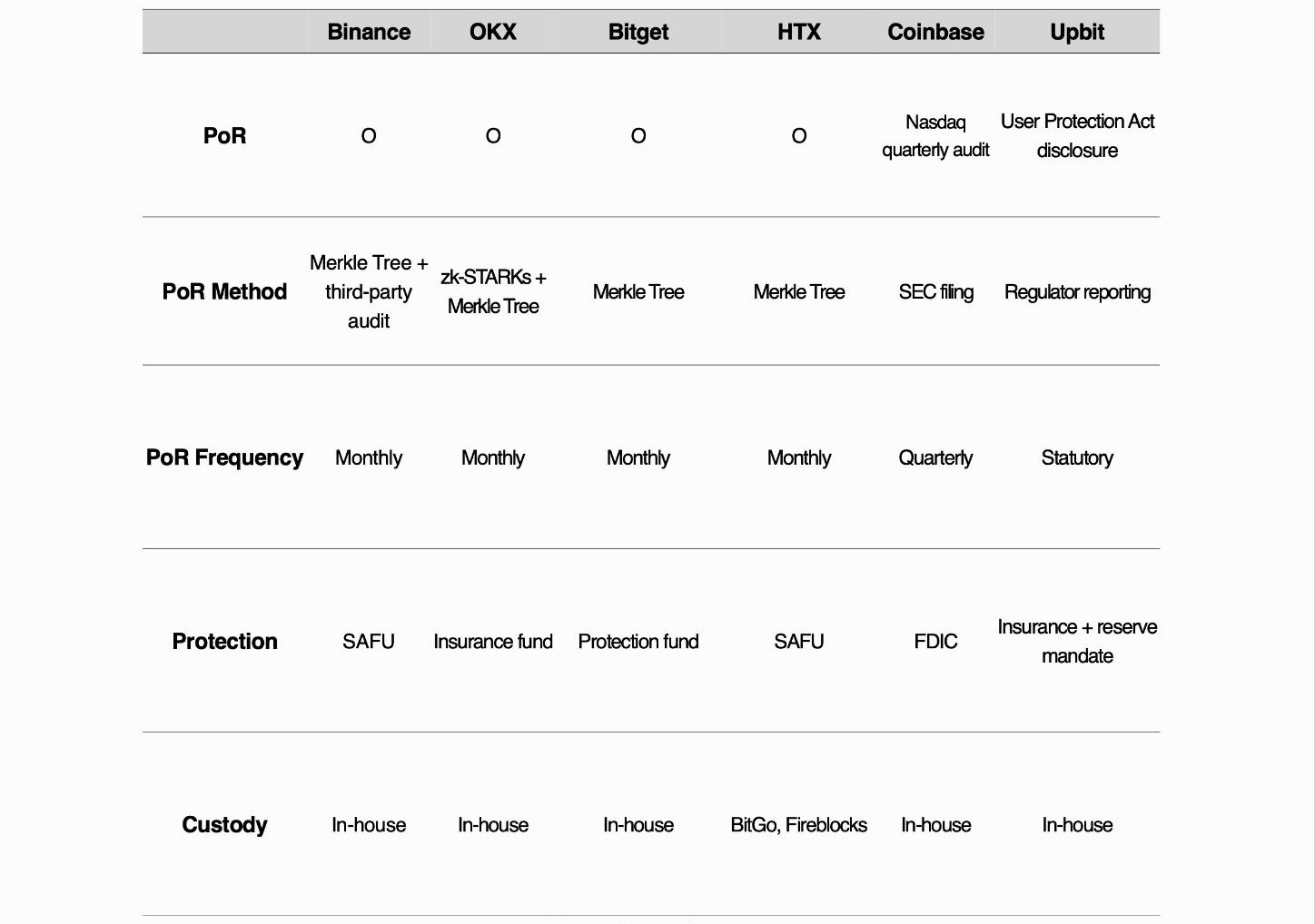

When the crypto-curious ask this question, the most direct answer an exchange can offer is transparency. After the FTX collapse, the entire industry began competitively publishing Proof of Reserves (PoR). Most major exchanges now disclose reserve status monthly. PoR disclosure itself has become an industry standard.

The difference lies in method. Simply showing numbers is not the same as providing them in a verifiable form. Some apply zero-knowledge proofs like zk-STARKs so users can verify independently. Others combine third-party audits or use SEC quarterly filings to establish financial transparency.

Security follows the same logic. Cold-wallet storage ratios, MPC technology adoption, and use of third-party custody solutions are emerging as differentiators. What the crypto-curious should focus on is not “has there been an incident” but “if an incident occurs, will my assets be protected.”

In practice, few major exchanges have never experienced a hack. Some fully compensated users through internal protection funds; others decommissioned compromised networks and restarted. In several cases, incidents became catalysts for strengthening security systems.

National security regulations are reinforcing this trend. Japan’s FSA is pursuing mandatory liability reserves. Hong Kong’s SFC has introduced 98%+ cold-wallet storage and mandatory VASP insurance. What exchanges once disclosed voluntarily is becoming the regulatory minimum.

One caveat applies. The PoR, protection funds, and security frameworks summarized in the table reflect a point-in-time snapshot. It matters whether monthly PoR disclosures continue and protection funds remain intact even when trading volumes decline sharply.

3.3. Education and Localization: Reaching Users in Local Languages and Currencies

Even with regulation and security in place, the crypto-curious will not open an app and trade without media exposure and education. Exchanges are addressing this through locally tailored education.

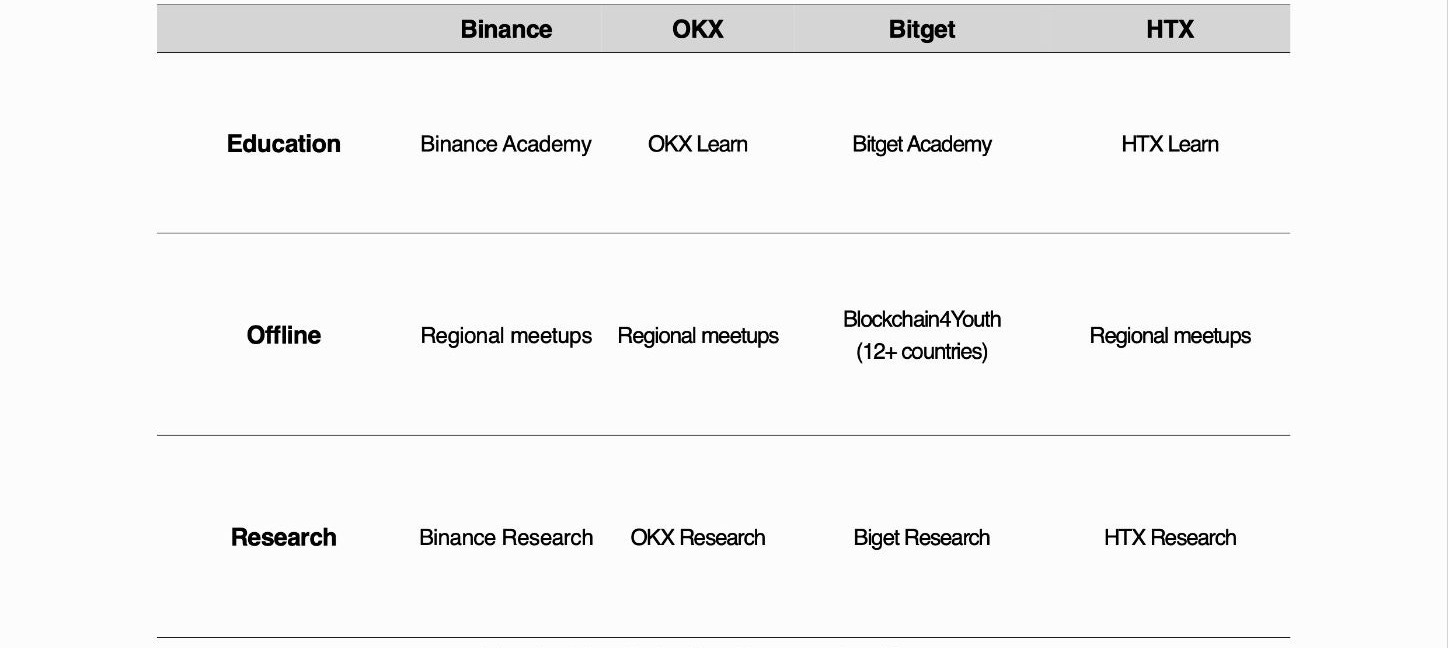

Education content, however, is no longer a differentiator. Every major exchange runs Learn & Earn, an academy, and a research arm. The differentiator lies in where and how content is delivered.

Global exchanges pursue two directions. The first is deepening online content: hundreds of tiered educational modules, university-affiliated certification programs, and Learn & Earn models that reward learners with small amounts of crypto to create a first-ownership experience.

The second is going offline. Bitget’s Blockchain4Youth is a leading example, operating hands-on onboarding across 12+ countries as of 2025, including NFT minting, stablecoin payment trials, and wallet creation.

Local exchanges go deeper into domestic context. Upbit invested KRW 10B to establish an Investor Protection Center, offers free standardized digital asset textbooks and Korean-translated whitepapers. In 2025, it launched “Up Class,” a generational education program in which 1,200+ older adults participated, later expanding to a youth program across five universities nationwide.

But even the best education is meaningless if users cannot access it in their own currency and language. Asia’s languages, currencies, and regulations differ by country. A single English-language interface cannot reach these markets.

This is why global exchange strategies are converging on localization: local languages, local fiat on-ramps, and product configurations aligned to local regulation, pursued simultaneously. Maintaining entities or partnerships in 12+ countries and collaborating with market-specific research institutions to deliver local insights is also expanding.

4. Now, Before the Next Bull Run

Mass conversion of the crypto-curious happens in bull markets. Tens of millions across Asia opened accounts in 2021 because prices rose, not because education improved. No infrastructure replaces a bull market’s pull. Deny this, and strategy becomes wishful thinking.

But most who entered in 2021 left when prices fell. Education stopped, communities went silent, media moved on. Without change, bull markets will keep pulling users in and pushing them out. That is not onboarding. It is a revolving door.

Equity markets crash too. But brokerages stay open, rebalance portfolios, and guide clients through downturns. New accounts still open in bear markets. Crypto has no equivalent.

Meanwhile, the competitive landscape is shifting. U.S. spot BTC ETFs, Japan’s SBI crypto ETF in preparation, Hong Kong spot ETFs live, Thai brokerages authorized for investment tokens. TradFi is entering directly. The crypto-curious can now buy Bitcoin on a brokerage app they already use. TradFi’s edge is not better information but a familiar experience.

This forces a fundamental question: as TradFi expands into crypto, what can only exchanges offer? Broader tokens, DeFi access, on-chain experience, 24/7 global markets. These could be answers, but only if translated into the crypto-curious’s language.

Asia can be crypto’s next growth engine. The next bull run will be the ignition. But if exchanges are not ready when it comes, the opportunity ends as just another cycle.

Disclaimer

This report was partially funded by HTX. It was independently produced by our researchers using credible sources. The findings, recommendations, and opinions are based on information available at publication time and may change without notice. We disclaim liability for any losses from using this report or its contents and do not warrant its accuracy or completeness. The information may differ from others’ views. This report is for informational purposes only and is not legal, business, investment, or tax advice. References to securities or digital assets are for illustration only, not investment advice or offers. This material is not intended for investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo following brand guideline. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.