Korea holds one of the world’s largest retail crypto investor bases. In 2026, the market is at a turning point: retail is stepping back as institutions step in.

Key Takeaways

Korea’s crypto market stands at a structural inflection point. With 11 million registered investors, the base is large, but retail engagement is declining as institutional capital begins to fill the gap.

More is happening beneath the surface than the headlines suggest. The GTM playbook is already public. Korean builders, long operating out of sight, are shifting toward AI in declining numbers. Won based stablecoin positioning is underway among institutions, even before legislation is finalized.

2026 does not reward last year’s playbook. Retail is exhausted. Institutions are still finding their footing. The teams that map the structure first will capture the next phase.

1. Why Korean Investors Are Different

The key to understanding Korea’s crypto market is understanding its investors.

Korean consumers rank among the world’s highest in willingness to adopt new digital services and spend on them. OpenAI identified Korea as the largest ChatGPT market in Asia-Pacific in September 2025, and Anthropic’s Economic Index report published in January 2026 ranked Korea among the top countries globally for Claude usage per capita.

When new technology emerges, Korea adopts it fast and uses it directly.

This pattern appeared in crypto before it appeared in AI. Korean investors have a high share of altcoin trading and actively participate in new project ecosystems. Crypto was at the center before AI ever was.

But market sentiment has shifted.

Years of recycled narratives and projects that faded without delivery have built up investor fatigue. At the same time, the structural environment is changing in ways that have no precedent: equity market policy tightening, institutional inflows beginning in earnest, and regulatory frameworks taking shape.

A maturing market and an exhausted investor base are converging at the same moment. That intersection is why this market deserves a second look now.

2. Crypto Investor Landscape

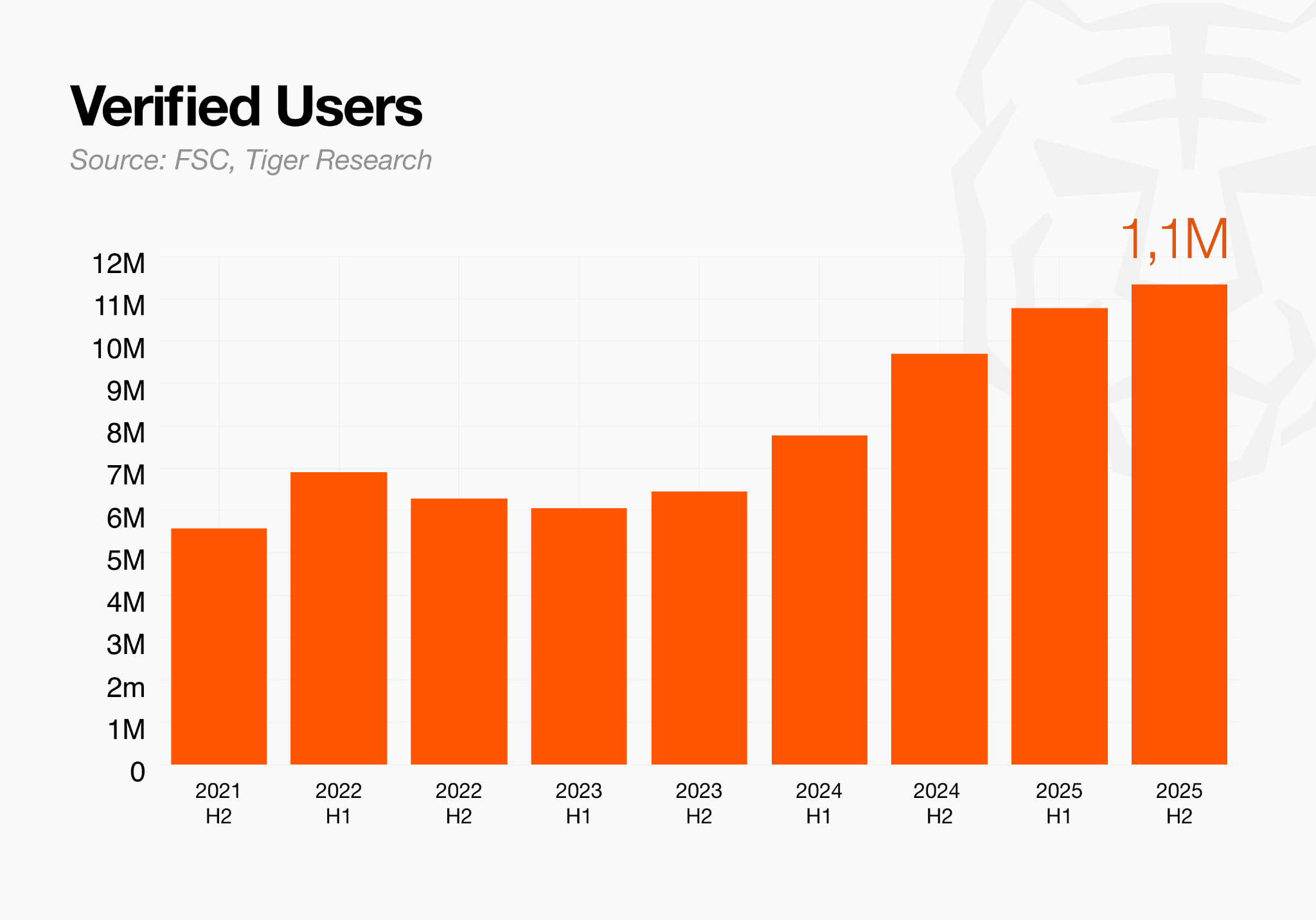

Domestic crypto trading is centered on KRW-denominated exchanges. As of end-2025, the number of verified users reached 11.13 million, an all-time high. Growth, however, is slowing. After peaking at 24.7% in H2 2024, the growth rate fell to 11% in H1 2025 and 5.2% in H2 2025. The pool of new entrants is shrinking.

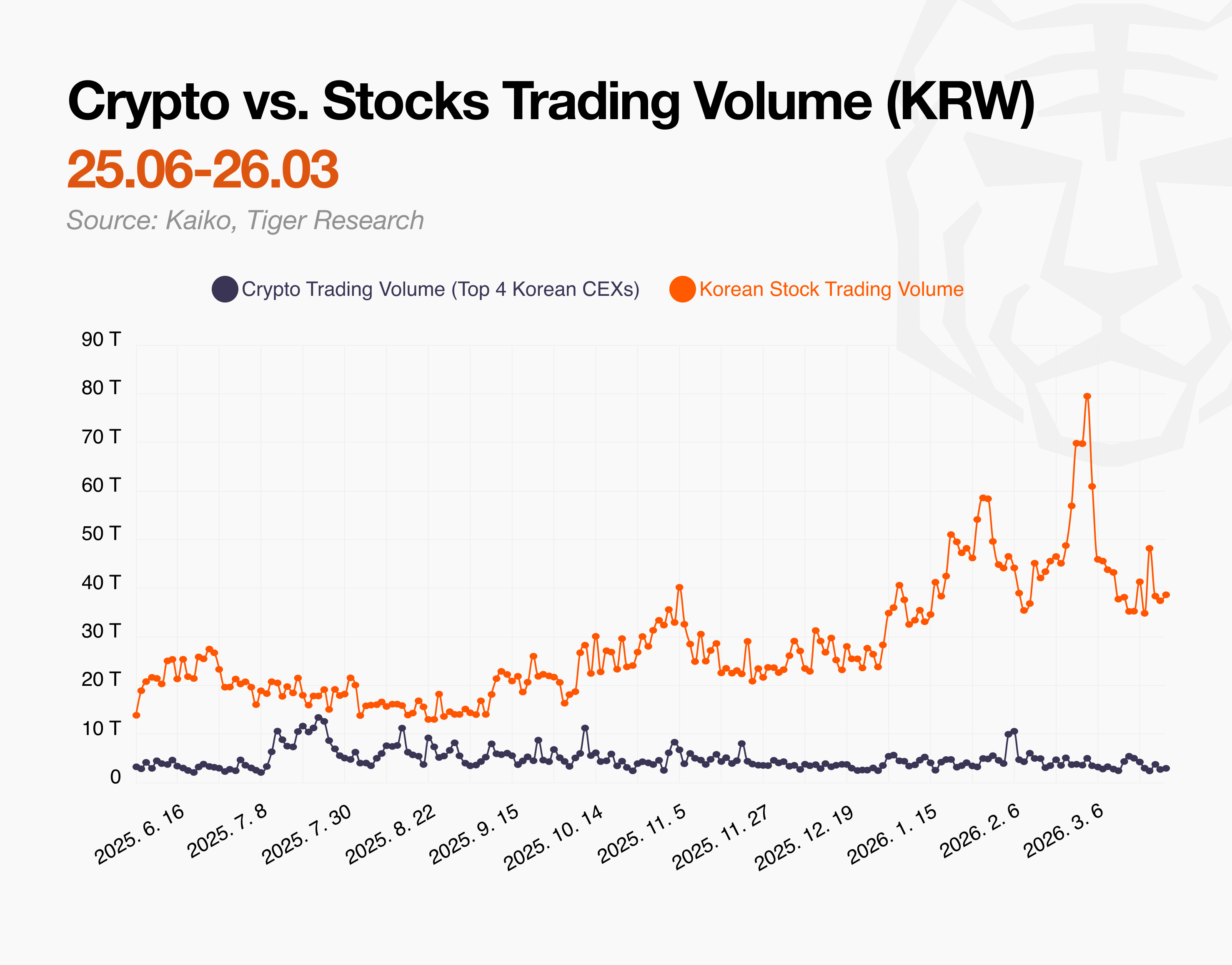

Daily average trading volume declined to approximately USD 3.7 billion, down 15% from the prior half-year, while exchange operating profit fell 38% over the same period. More participants are registered, but actual trading activity is contracting.

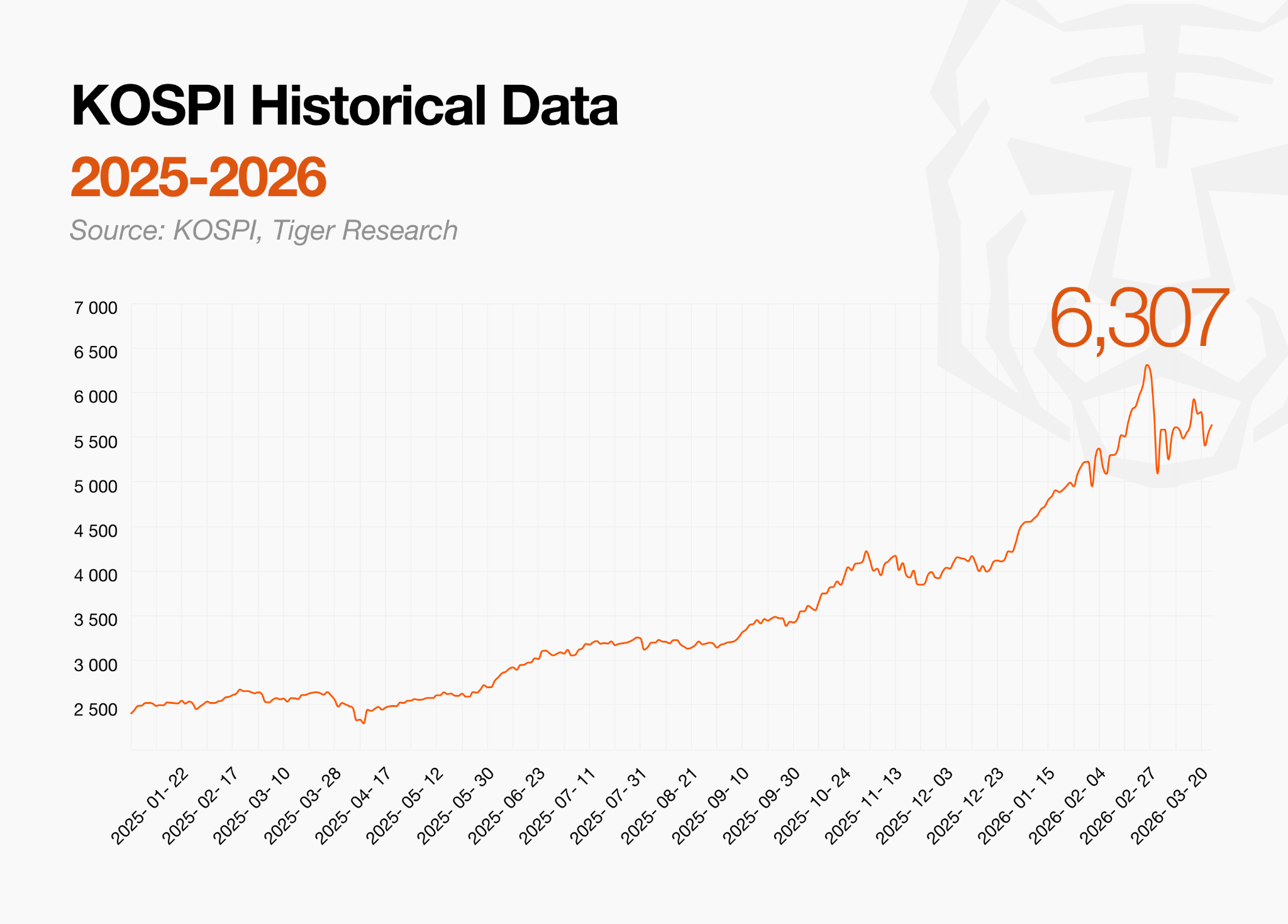

The backdrop is a bull run in equities. The KOSPI started January 2025 at roughly 2,400 and broke through 6,300 in February 2026, more than doubling in just over a year.

Over the same period, a widening gap emerged between crypto trading volume and equity market turnover. The divergence has become particularly acute since early January this year. This is not a loss of interest in crypto. It is the result of investors having more options.

3. Five Sectors You Need to Know in Korea

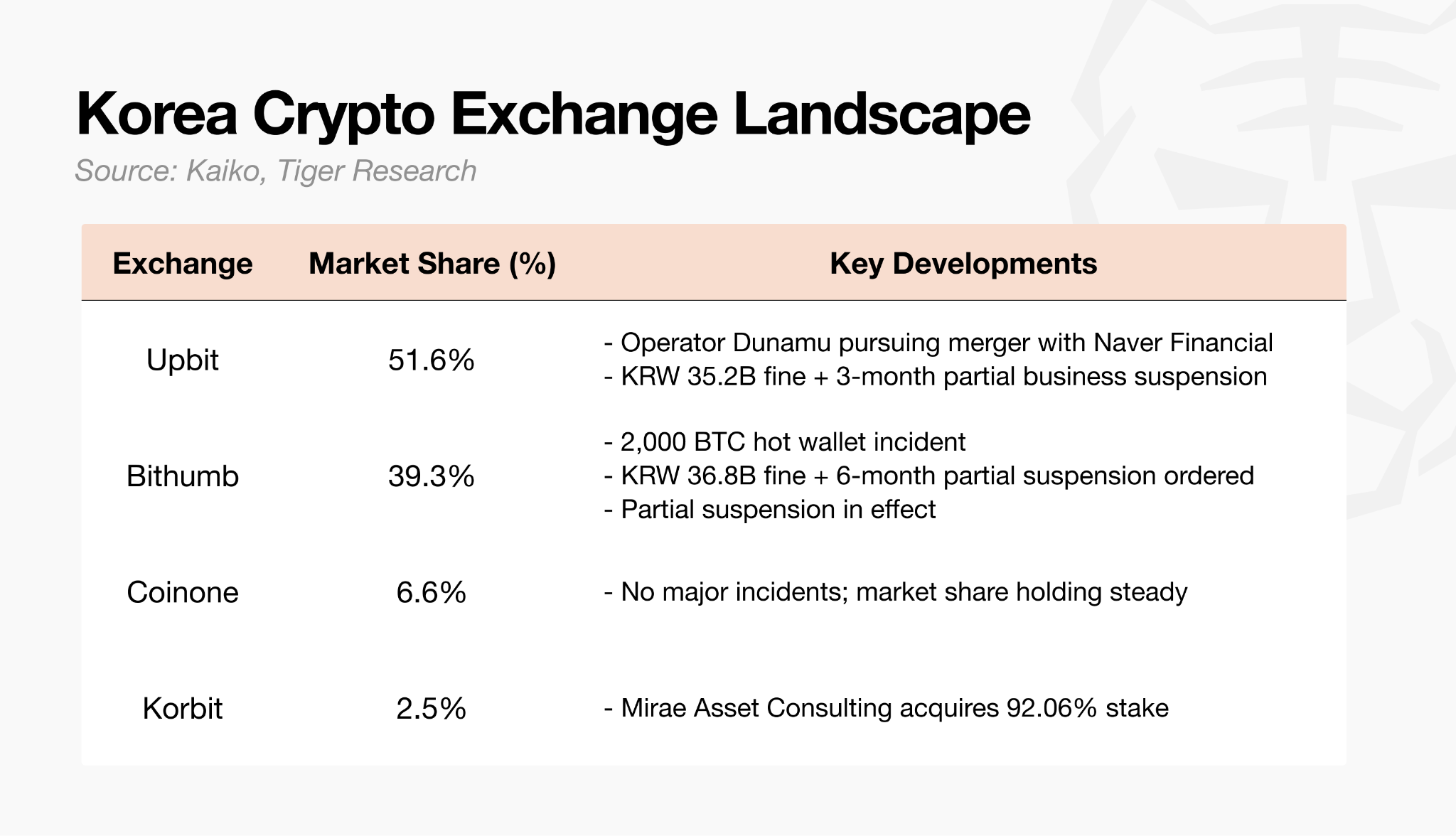

3.1. Crypto Exchanges: Will the Duopoly Hold?

Korea’s domestic crypto exchange market remains firmly structured around two players: Upbit and Bithumb. Together they hold approximately 87% market share, with Coinone trailing at around 10%. Recently, simultaneous regulatory pressure and M&A activity have begun to shake the structure itself.

Three developments are worth watching this year.

Will the Naver Financial x Dunamu merger close? The May 2026 shareholder meeting is the deciding moment. If more than 8% of Dunamu shareholders vote against, the deal falls through. Price volatility in Dunamu’s approximately USD 2.1 billion in digital asset holdings is an additional variable.

What is the real impact of Bithumb’s partial business suspension? This is not an exchange closure. Only external withdrawals by new users are restricted for six months. Existing customers can continue operating normally.

What does Mirae Asset’s Korbit acquisition mean going forward? The target model is vertical integration: Mirae Asset tokenizes real assets such as real estate and bonds, while Korbit handles distribution.

3.2. GTM: Surviving the Crypto Winter

Most players operating in Korea’s crypto market are GTM agencies. The service offering is largely uniform: KOL marketing, blog management, Naver SEO, community viral campaigns, PR, and YouTube. Low barriers to entry mean new players continue to emerge.

Foundations use GTM agencies for two reasons. Unfamiliarity with local market dynamics is one factor, but the core reason is the difficulty of maintaining in-house operational headcount. Services may look similar on paper, but execution requires significant effort, and subtle differences in linguistic nuance often determine outcomes.

The problem is that as the industry matures, this formula is no longer a secret. The “Korea playbook” has circulated widely, and foundations now know it well. Even when GTM agencies set the strategy, actual operations are often outsourced externally. As a result, some foundations are bypassing agencies entirely and contracting KOLs directly.

Since last year in particular, KOLs have increasingly been forming collective agency structures. Operating in DAO-like groups, they pitch end-to-end marketing packages as a unified entity.

Established GTM players are responding by changing their approach. Management depth and strategic capability remain clear advantages, but not every client prioritizes quality. To differentiate, incumbents are exploring product development, expanded research content, and other avenues. Without a clear edge, convincing foundations that already know the playbook is increasingly difficult.

Three things to watch this year:

KOL collectives: will they replace agencies? KOLs are moving beyond channel management to pitch strategy directly as organized groups. For foundations, this means execution without agency margin. The coordinator role that agencies once owned is being displaced quickly.

How does prolonged TGE delay affect agency revenue? When listings are pushed back, foundation marketing budgets shrink. GTM agencies built around short-term contracts lose stable income. Without restructuring contract models, sustainability becomes difficult.

Where does the undifferentiated agency go from here? When services are identical, competition collapses to price. Only agencies with capabilities that are hard to replicate, such as proprietary products or research content, can hold their rates.

3.3. KRW Stablecoin: Who Will Lead?

The KRW stablecoin market is taking shape. While legislation stalls in the National Assembly, banks have already moved.

The central question is who gets to issue. The FSC and Bank of Korea maintain that only bank-majority consortiums (50%+1 share) should be permitted. The Democratic Party TF is pushing back, arguing that fintech and platform companies must also have access to issuance rights. No legislation has been finalized.

Even so, banks have moved to secure partners first, operating on the assumption that they will hold the lead regardless of how the legislative outcome lands.

Shinhan and Hana Financial are in discussions to form a consortium with Samsung. Hana Financial has been the fastest-moving of the four major financial groups, signing MOUs in succession with BNK Financial, iM Financial, and SC First Bank. If Samsung Wallet and its global distribution network are brought into the structure, the resulting setup could capture both online and offline payment infrastructure in one move.

KB Financial is in talks with Toss domestically and Circle internationally, pursuing a strategy to secure both issuance technology and distribution platforms simultaneously. K-bank has declared its intent to join an issuance consortium, leveraging its BC Card payment network as a differentiator. Toss Bank is placing its weight on distribution and ecosystem development, backed by a 30 million user base.

No final consortium structure has been confirmed, but every major financial institution is now in the race.

Two variables will determine the outcome.

The first is the legislative result. If a bank-centric structure is codified, today’s consortium competition solidifies as-is. If fintechs are granted access, the competitive landscape changes entirely.

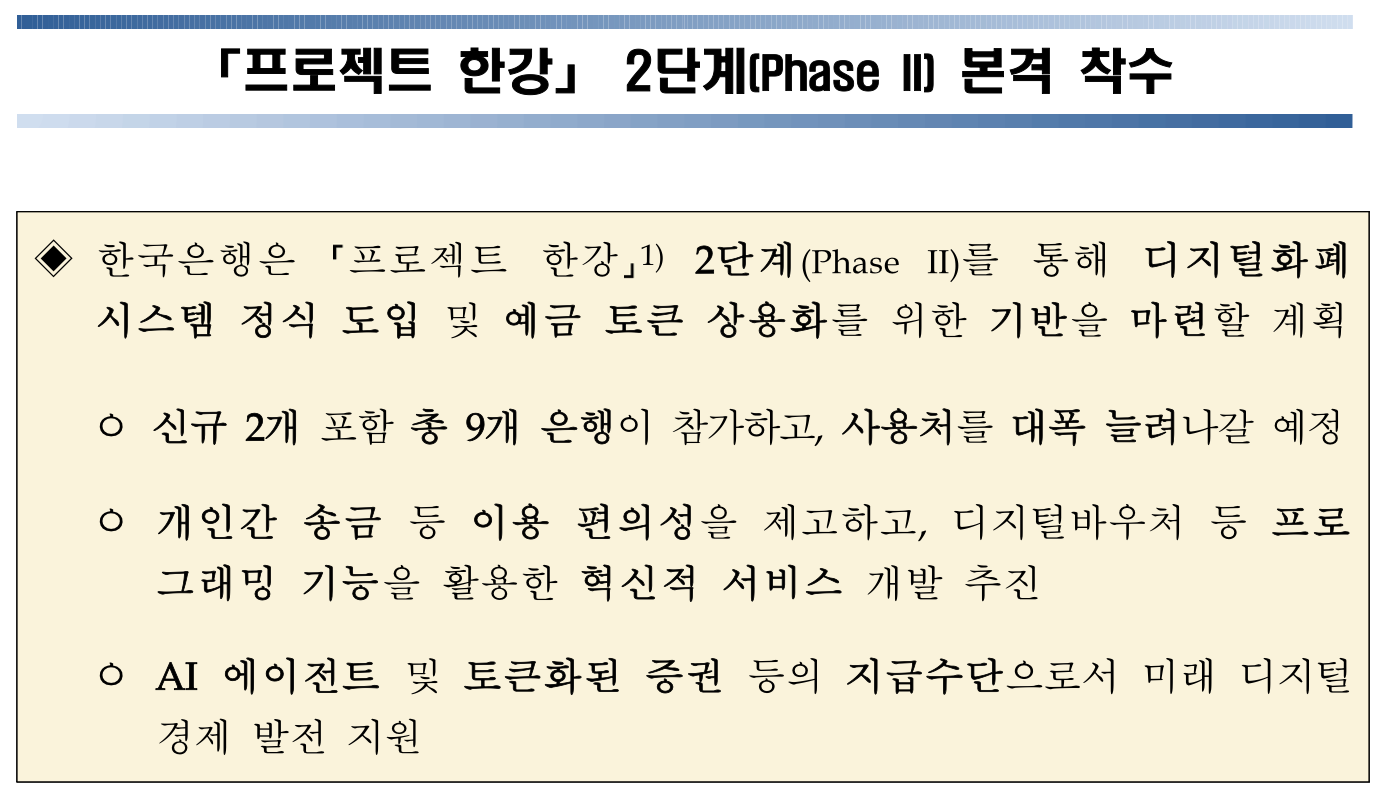

The second is the Bank of Korea. Incoming Governor Shin Hyun-song has signaled a CBDC-first orientation and is emphasizing the BOK’s role in the stablecoin licensing process. The faster Project Hangang Phase 2 advances, the narrower the space for private stablecoins becomes.

Two things to watch in the KRW stablecoin market this year:

Will banks lock in the issuance role? The FSC and BOK are holding firm on the bank 50%+1 consortium structure; the Democratic Party TF is pushing for fintech inclusion. The legislative outcome will either cement the current consortium dynamic or reset the playing field entirely.

Is the Bank of Korea a friend or adversary to private stablecoins? Incoming Governor Shin Hyun-song has signaled a CBDC-first approach. The faster Project Hangang Phase 2 advances, the more constrained the private stablecoin market becomes.

3.4. Builders: Many but Invisible, and Now Fewer

Korea has a substantial base of hidden builders. But since the Terra-Luna collapse, Korean founders making a visible mark on the global stage have become harder to find. Not because they are absent, but because they are out of sight.

The core reason is deliberate concealment.

Teams targeting global markets tend to obscure their Korean identity. The trust damage from Terra-Luna is a factor, but the more direct reason is closer to home: skepticism toward Korean projects has taken root among Korean investors themselves.

One of the largest potential markets is, paradoxically, one of the hardest for Korean projects to penetrate. Appearing less Korean is a survival strategy. Founders incorporate in Singapore or Dubai, assemble multinational teams, and structure projects in ways that make the Korean origin difficult to identify.

The deeper problem is that this already-hidden builder pool is now shrinking. Developers with Web3 experience are migrating toward AI agents and on-chain AI infrastructure. The shift is a natural one, but the byproduct is a thinner pipeline of pure crypto builders. Those who were many but invisible are now genuinely fewer.

3.5. Academic Societies: Talent Pipeline and Industry Network

SNU Decipher and KAIST Orakle are the most prominent examples. These are not casual study groups. Both run regular research presentations, product pitches, and hackathons, with major industry players participating directly as sponsors.

What makes them distinctive is their composition. Societies made up exclusively of students are the exception, not the rule. Developers, product managers, and finance professionals with an interest in crypto participate alongside university students.

These organizations function simultaneously as talent development pipelines and industry networking hubs. This is precisely why global chains actively support Korean academic societies: they offer a single channel through which to recruit core developers and cultivate on-chain builders at the same time.

Blockchain academics exist in many countries, but the model where working professionals and students actively participate together is particularly pronounced in Korea. It appears to have emerged organically, in the absence of formal channels capable of absorbing the high level of public interest in crypto.

4. Korea’s Crypto Market: Time to Look Again

Retail interest in the Korean market is cooling, and the data is clear. Trading volumes are down, and new user growth has slowed. Yet over the same period, institutional activity, including in KRW stablecoins, is moving faster than ever, and regulatory discussions are becoming increasingly concrete. For a detailed overview of the regulatory landscape, refer to our previous report.

Retail is stepping back. Institutions are stepping in.

This transition looks like a healthy one. Retail has always exited during crypto winters. The real concern would be an empty room, but right now institutions are filling those seats quickly. The new developments emerging from this inflection point will shape the next phase of Korea’s crypto market.

For foundations, the clearest opportunities right now lie in targeting institutions. That said, retail cannot be written off entirely. Users who have stayed in the market through the cycles no longer respond to familiar narratives. The same approach will not work.

Capturing opportunity in this market requires understanding the full structure first.

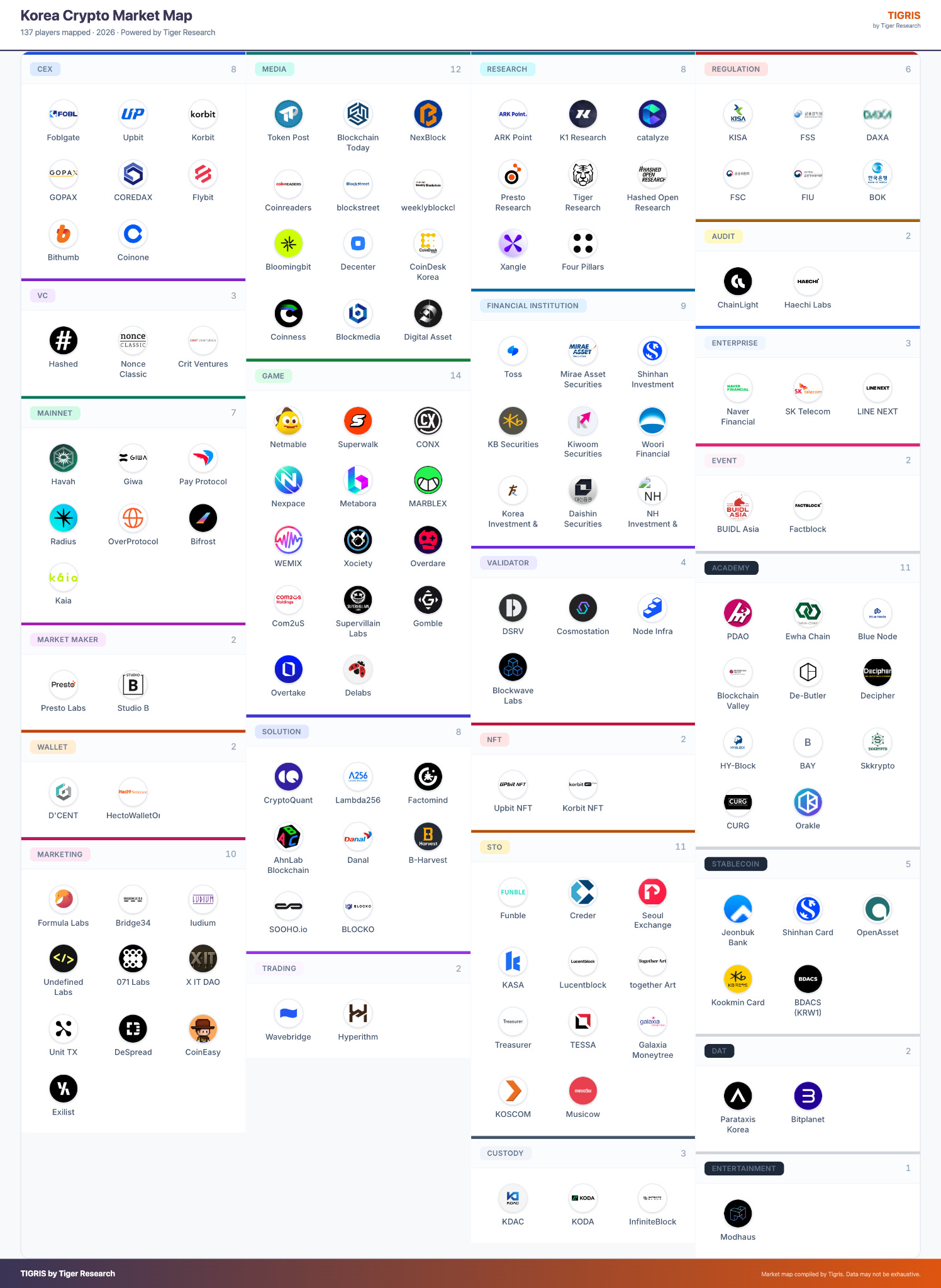

Tiger Research has built a Korea crypto market map for exactly this purpose, with continuously updated coverage available through Tigris. Alongside the market map, an AI-powered GTM strategy tool provides early-stage guidance for teams planning their Korea market entry.

Korea’s market is still large, and still fast-moving. But it no longer responds to the old playbook. Retail is fatigued. Institutions are still finding their footing. Somewhere in between, the opportunity exists. The teams that see it first will define the next phase.

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.