Key Takeaways

Drift’s Tether loan is effectively unrepayable. Drift’s cumulative revenue stands at just $31M, while it borrowed up to $127.5M from Tether. Terms and schedule remain undisclosed, but at current revenue levels, full repayment would take considerable time. Tether knew the numbers.

Tether’s real goal is securing USDT as Solana’s base currency. USDC leads USDT by more than 2x in Solana’s stablecoin market. With Drift switching settlement from USDC to USDT post-relaunch, Tether flipped the base currency of Solana’s #2 perp DEX with a single loan.

The loan is both a financial deal and a branding play. Tether has long carried trust risk from opaque operations. It is now building a track record as crisis savior while capturing spillover as Circle faces a class action over alleged hack complicity. The form is a loan; the substance is market capture.

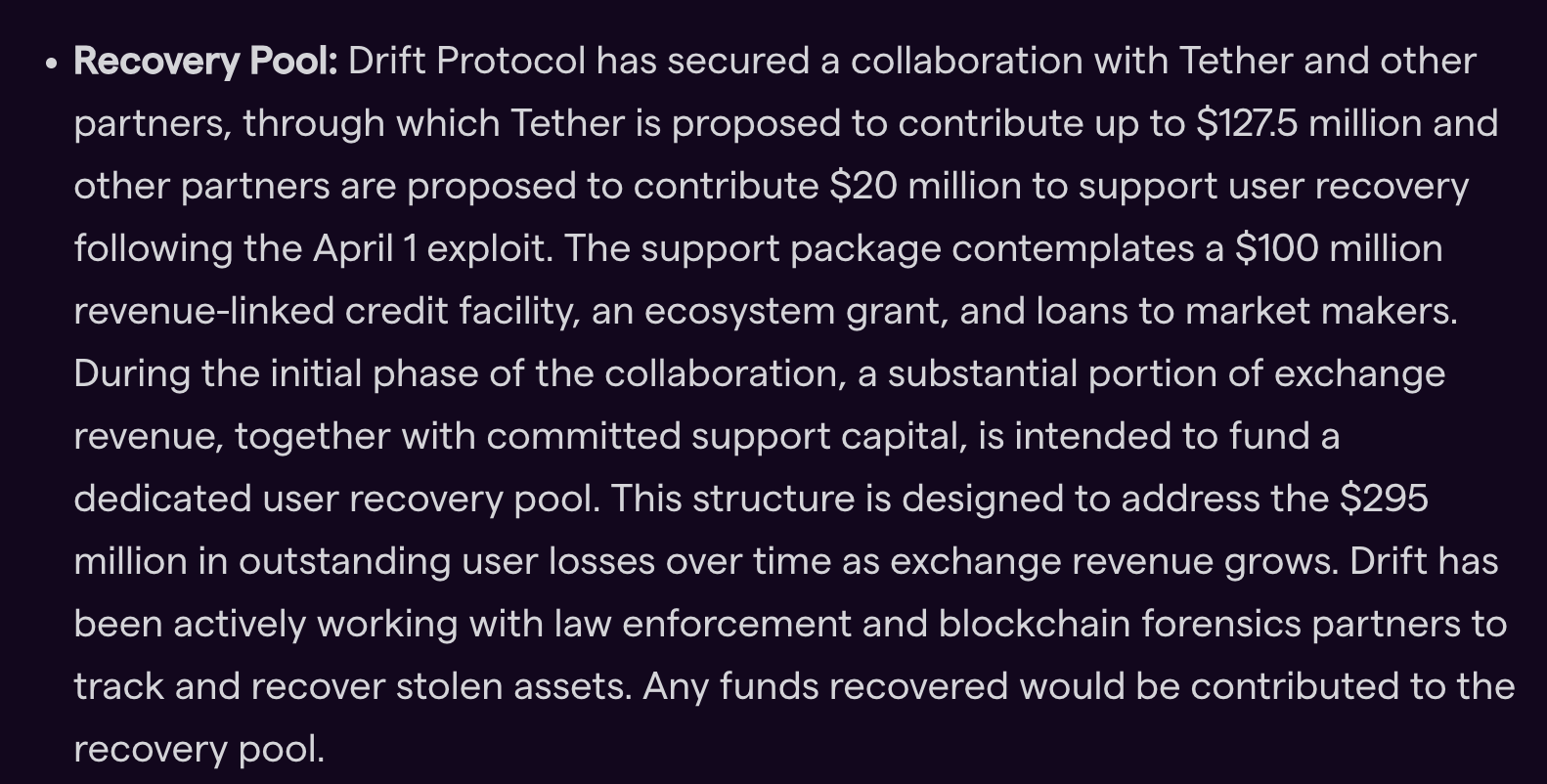

On April 1, 2026, Solana-based perpetual futures exchange Drift suffered a hack causing approximately $295.7M in losses. Two weeks later, on April 16, Drift announced it had secured loans from Tether and several partners.

ether committed up to $127.5M and other partners $20M. Drift plans to combine this capital with post-relaunch exchange revenue to fund a victim recovery pool. Victims receive separate recovery tokens representing claims on the pool.

Why Now

This is a loan, not a grant. Drift must repay it out of exchange revenue, which to date totals only $31M. Terms and schedule remain undisclosed, but at current revenue levels, full repayment would take considerable time.

Tether knew the numbers.

A Simple Analogy

A neighborhood convenience store burns down. A beverage supplier lends rebuild capital, but only if the store stocks its drinks exclusively going forward. Repayment comes from store sales, with no clear timeline.

The supplier cared more about exclusive distribution than getting the principal back. And by helping a burned-down store, it earned a reputation as a good neighbor. This is precisely what Tether did to Drift.

Tether’s Long Game

Tether earns interest on the loan, but likely targeted two bigger gains.

Sub 1: USDT as Base Currency

Securing USDT as the base currency. Solana’s stablecoin market currently holds roughly $7.8B in USDC versus $3.4B in USDT, more than a 2x gap. Closing this gap requires a platform that uses USDT as its default, and Drift fit that need.

In Q3 2025, at the peak of Solana’s perp DEX market, Drift ranked #2 with $465M in average daily volume and 28% market share. With a single loan, Tether flipped the base currency of the most symbolic exchange in a USDC-dominated ecosystem.

Sub 2: Lender of Last Resort

positioning as DeFi’s lender of last resort. Tether is actively building a track record of stepping in as savior during crises. Hacks of this scale typically trigger investor support or equity sales. Tether chose a third path, taking on creditor and savior status simultaneously without demanding the money back. The loan is both a financial deal and a branding exercise.

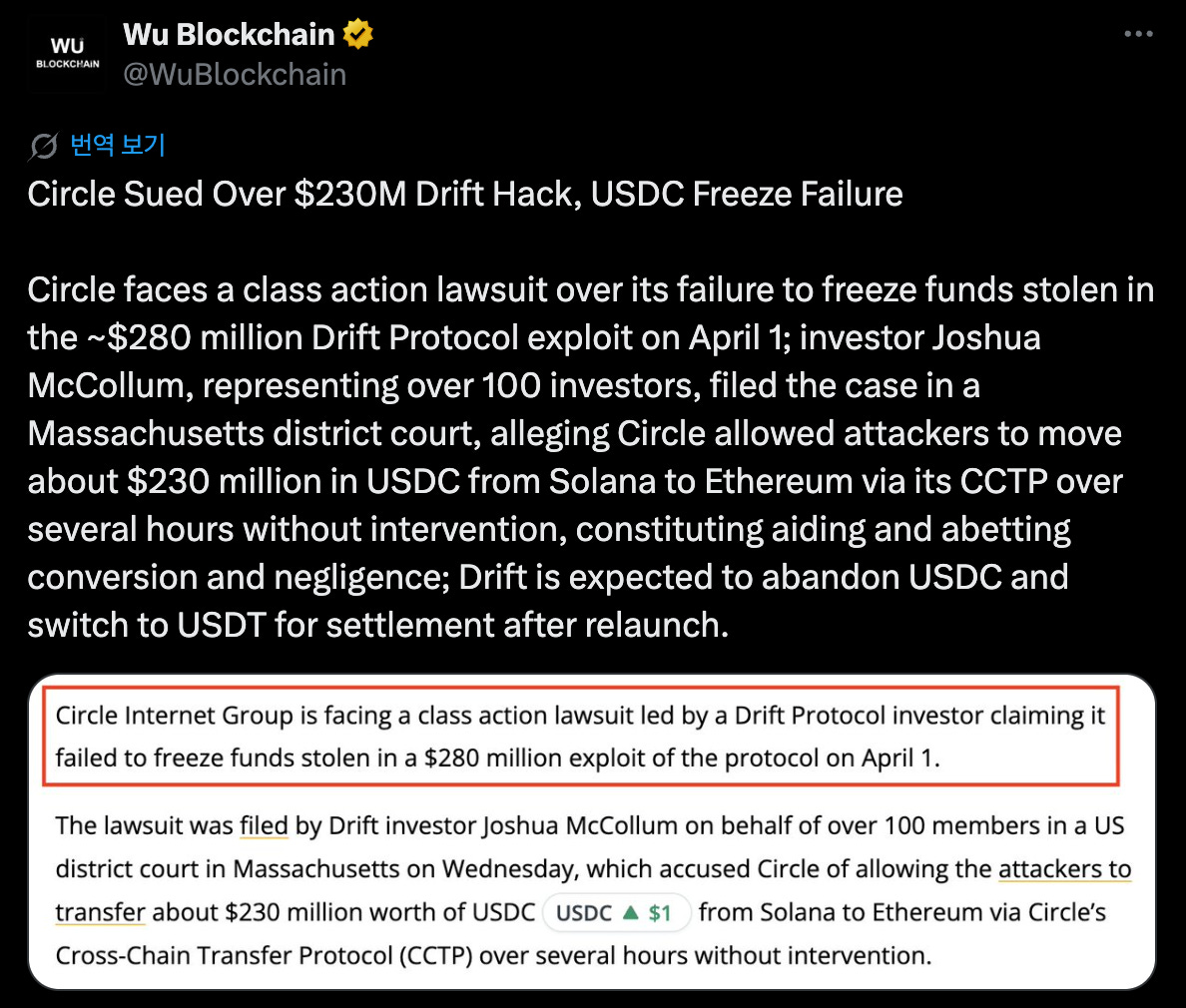

One event accelerates this dynamic. According to Wu Blockchain, Drift investor Joshua McCollum filed a class action in Massachusetts federal court against Circle on behalf of over 100 investors. The suit alleges Circle allowed roughly $230M in USDC to exit via its Cross-Chain Transfer Protocol (CCTP) over several hours without intervention during the hack.

Whether the allegation holds is beside the point. Circle will defend itself in court regardless, and in the meantime, Tether quietly builds its savior brand.

Tether’s goal here was never interest.

It was flipping the base currency of Solana’s largest perp DEX, imprinting itself as crisis savior, and capturing spillover while Circle is tied up in court. The form is a loan. The substance is market capture.

Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.