Key Takeaways

The U.S. SEC is preparing to announce an “innovation exemption” framework that would allow third parties to tokenize listed stocks without issuer approval.

Tokenized stocks risk triggering two structural disruptions: liquidity fragmentation, as capital disperses from centralized exchanges across multiple blockchain platforms, and revenue fragmentation, as fee and intermediation income leaks offshore or to competing venues, threatening national financial competitiveness.

Capital fragmentation is already a reality. With RWA open interest on decentralized platforms like Hyperliquid hitting all-time highs, financial institutions and jurisdictions that fail to absorb innovation quickly will lose long-assumed dominance over their domestic capital markets.

On May 18, 2026, Bloomberg reported that the SEC could announce its “innovation exemption” framework within the week, permitting third parties to offer tokenized stocks such as Apple or Tesla without issuer approval.

This follows a February proposal by pro-crypto commissioners Paul Atkins and Hester Peirce, who outlined a deregulatory vision for public blockchains. It also reflects sustained industry pressure: Coinbase and the Blockchain Association formally submitted support letters calling for third-party tokenization rights without issuer veto.

Despite market expectations for broad deregulation, Commissioner Peirce’s guidelines released as of May 22 are narrower in scope than anticipated. The exemption explicitly excludes synthetic stock tokens carrying no voting or dividend rights, applying only to on-chain stock instruments that fully preserve shareholder rights.

Why Now

Tokenized stocks are fundamentally tied to fragmentation, specifically two forms: 1) liquidity fragmentation and 2) revenue fragmentation.

1) Liquidity Fragmentation

While the crypto ecosystem tends to discuss liquidity aggregation, traditional finance views the breakup of its previously consolidated, centralized liquidity as a serious structural threat.

When third parties tokenize the same listed stock across different blockchain networks and decentralized platforms, trading volume and order flow that should concentrate on a single venue such as the NYSE or Nasdaq instead disperses across multiple venues.

This creates price discrepancies across platforms, increases slippage on large orders, and ultimately degrades overall market efficiency.

2) Revenue Fragmentation

Revenue fragmentation follows directly from market fragmentation. As tokenized stocks trade across multiple platforms in disaggregated form, financial revenues that should accrue to domestic exchanges instead flow offshore, with direct implications for national financial competitiveness.

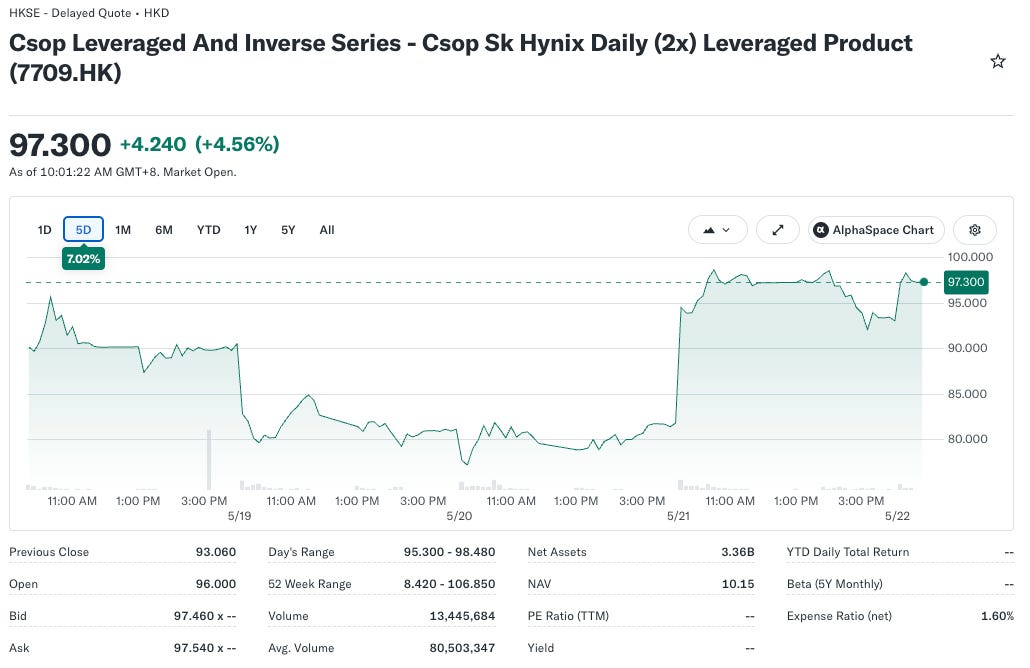

Consider CSOP’s SK Hynix 2x leveraged ETF, launched by the Hong Kong-based asset manager, which has grown into the world’s largest single-stock leveraged ETF with net assets exceeding KRW 11 trillion (approx. USD 8 billion). Had Korea moved first through a regulatory sandbox or similar mechanism, the resulting management fees and financial revenues would have accrued to domestic institutions.

Fragmented liquidity thus produces fragmented revenue, and at its extreme, a shift in financial leadership over national capital markets. The SEC’s urgency in codifying its “innovation exemption” reflects precisely this logic: contain fragmentation and pull global financial revenues back within the domestic regulatory perimeter.

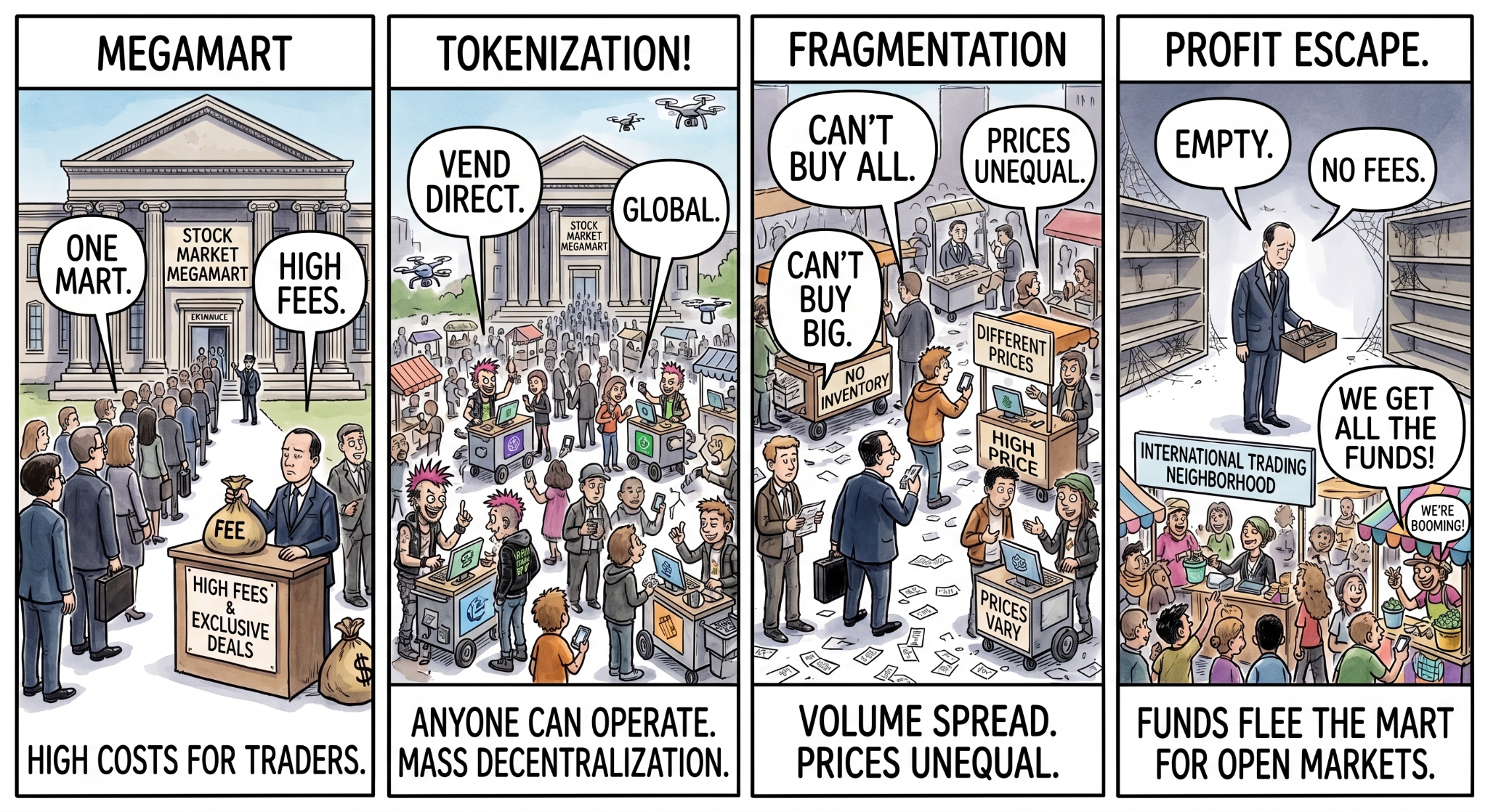

Simple Analogy

The traditional stock market functions like a single dominant superstore. All buyers and sellers converge in one place, the exchange monopolizes transactions, captures the fee revenues, and offers no alternative route to trade.

Tokenized stocks allow anyone to set up thousands of street stalls without the store’s permission, enabling direct transactions outside the established venue. This is what produces structural fragmentation across capital markets.

Liquidity Fragmentation (Dispersed buyers): Order flow that should concentrate in one venue scatters across thousands of stalls. Thin inventory at each stall makes large trades difficult, and prices diverge across venues.

Revenue Fragmentation (Dispersed earnings): As buyers disperse, so do the fee revenues the exchange once monopolized. If a local exchange hesitates due to regulatory constraints, a competing venue in another jurisdiction launches first and captures both the global capital flows and intermediation revenues entirely.

What Financial Institutions Risk by Standing Still

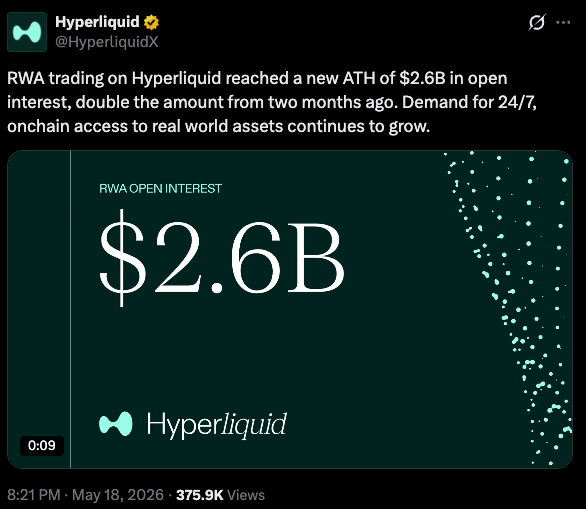

Capital fragmentation is already underway. On May 18, the same day the SEC signaled its forthcoming framework, Hyperliquid’s RWA open interest surpassed USD 2.6 billion, an all-time high. Driven by demand for 24/7 on-chain access to traditional assets, RWA trading volumes on Perp DEXs are expected to grow sharply going forward.

This shift poses the deepest strategic dilemma for incumbent financial institutions and regulators alike.

Incumbent exchanges face two paths: actively designing tokenized stock infrastructure through partnerships, as the NYSE has begun to pursue, or lobbying regulators to block it in order to protect existing revenue positions.

Regulators face the same tension. With domestic exchange revenues eroding in real time, the instinct is to apply institutional brakes rather than permit full adoption, allowing innovation while controlling the pace at which trading migrates outside established infrastructure.

Even once the framework is formally announced, the underlying conflicts are only beginning. Two issues will define the market going forward.

A second “CLARITY battle” over shareholder rights. Just as the stablecoin yield debate pitted traditional finance against crypto, tokenized stocks are likely to trigger an equally sharp legal dispute over form and implementation pace.

The unlicensed exchange risk from platforms that grew in regulatory gray zones. Whether high-growth platforms like Hyperliquid, which absorbed significant RWA volume outside the regulatory perimeter, can be smoothly brought within it remains an open question. The moment regulators classify them as unlicensed exchanges, market liquidity and uncertainty will face another sharp disruption.

In the digital asset era, financial institutions and jurisdictions that fail to move quickly will permanently forfeit the fee monopolies and financial leadership they have long taken for granted, as capital continues to fragment and disperse in all directions.

Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.