Key Takeaways

The Bank of Korea’s 2025 Payment and Settlement Report officially flagged exchanges’ lack of internal controls and called for a review of circuit breaker adoption

Crypto markets have fragmented liquidity across exchanges, unlike stock markets. A domestic-only circuit breaker could create price dislocations against offshore venues, amplifying rather than reducing risk

The priority is not transplanting traditional financial regulation but designing rules that reflect the structural realities of crypto markets

On April 13, the Bank of Korea included a review of systemic safeguards such as circuit breakers in its 2025 Payment and Settlement Report.

The BOK argued that these measures should be codified in the Digital Asset Basic Act (working title) currently under discussion in the government and National Assembly, strengthening exchange safety and transparency.

This traces back to an incident in February 2026, when Bithumb mistakenly overpaid Bitcoin during an event prize distribution. A staff error led to roughly KRW 6 billion (approximately USD 4.3 million) in Bitcoin being sent in excess.

According to Bithumb’s own disclosure, the resulting investor losses amounted to approximately KRW 1 billion (approximately USD 720,000).

Why Now

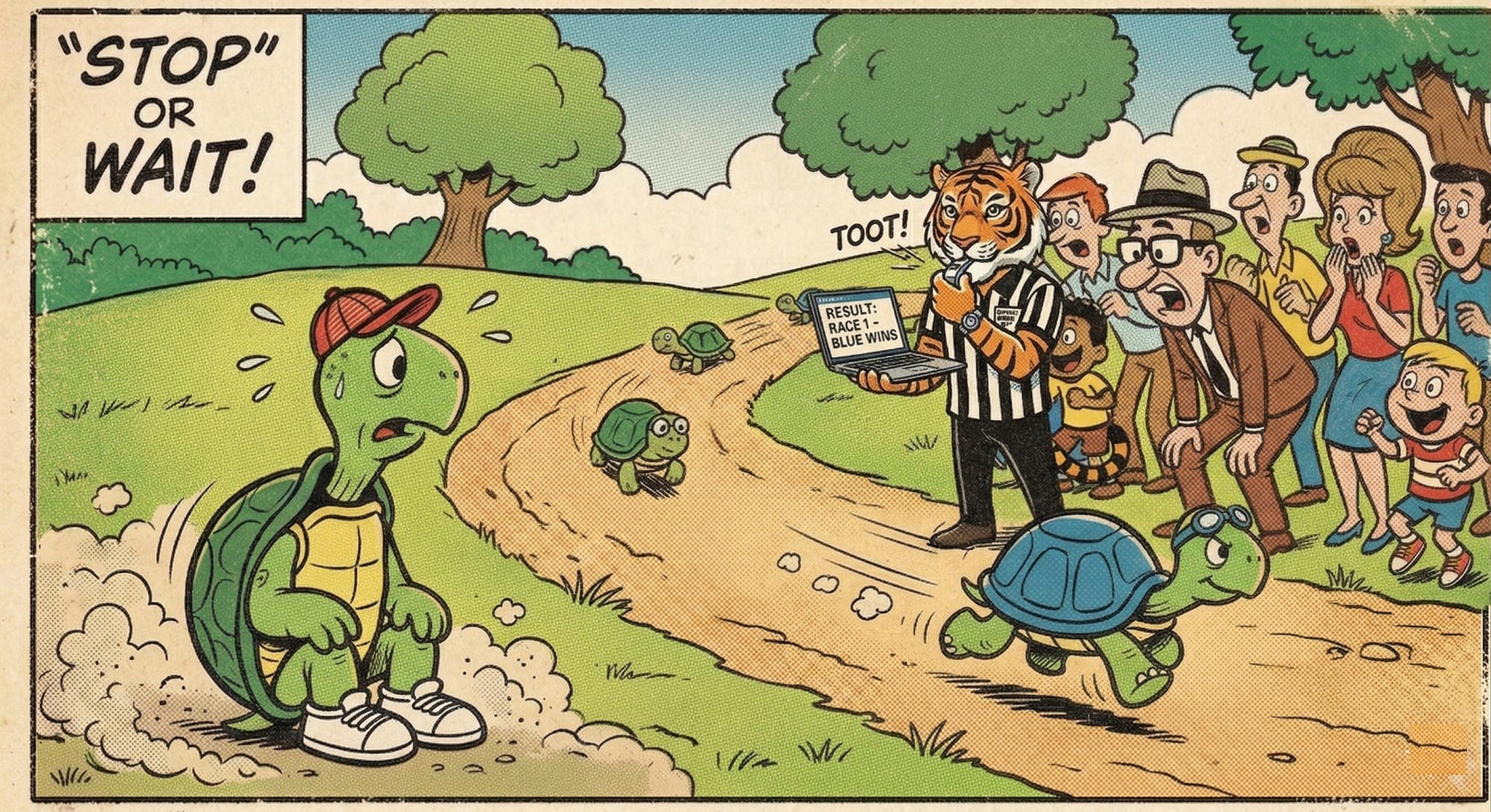

A circuit breaker in the stock market is a mechanism that temporarily halts trading when a specific index or stock drops sharply. What happens when the same mechanism is applied directly to crypto exchanges?

Even if Bithumb halts trading, Binance and Coinbase do not. When a circuit breaker triggers only on domestic exchanges, the same assets continue trading offshore. Price gaps accumulate in the interim, and the moment trading resumes, arbitrage volume targeting that gap floods in all at once.

The problem is amplified in a broader downturn. An investor holding coin A exclusively on a domestic exchange cannot act while trading is paused. During that same window, offshore users freely sell coin A to cut their losses. When trading resumes, pent-up sell orders from stranded domestic investors hit the market simultaneously, making the drop even steeper.

In the end, a circuit breaker may not diffuse the shock. It may intensify it.

Plain Explanation

A simple analogy helps. Imagine a building on fire where one emergency exit is locked. It may stop people from rushing toward that door in the short term. But the fire does not go out.

People gather in front of the locked door. Meanwhile, those at other exits have already escaped to safety. The moment the locked door reopens, everyone trapped inside pours out at once, and the damage is compounded.

The congestion was never dispersed. It was only compressed into a single moment.

A circuit breaker applied solely to domestic exchanges works the same way. Halting trading does not eliminate market panic. Because domestic exchanges are not integrated with global markets, transplanting traditional financial market regulations as-is simply does not work.

Crypto Requires a Different Regulatory Framework

There is no guarantee the Bithumb incident will be the last of its kind. If a similar crisis recurs, financial regulators cannot escape accountability.

For financial authorities, the crypto market was never a pressing priority. There was little incentive to study its characteristics deeply, and jurisdiction was split across multiple agencies, blurring the direction of reform. Relevant overseas precedents were scarce. The result: regulators fell back on familiar traditional finance rules.

The Bank of Korea’s circuit breaker recommendation likely emerged from this very backdrop.

The diagnosis that Bithumb’s internal controls were inadequate is fair. The problem is the prescribed remedy does not fit the crypto market’s reality. When a circuit breaker triggers on a domestic exchange, local trading halts, but offshore exchanges keep moving. Price gaps accumulate, and the moment trading resumes, pent-up arbitrage pressure is released all at once.

The very crash regulators tried to prevent may reappear in a more compressed form at the point of reopening. A measure designed to reduce harm becomes the trigger for the next round of damage.

This is not about nitpicking a single circuit breaker recommendation. Regulators themselves lack clear answers, and that is understandable. Crypto operates in a trading environment without historical precedent. No jurisdiction has yet designed a regulatory framework suited to a 24/7 global decentralized market.

Reaching for familiar tools when there is no reference point is a natural response. But an understandable choice is not necessarily the right one.

The more rational approach is to prioritize preventive controls over reactive measures. Post-incident responses only work when applied uniformly across all exchanges, making them inherently difficult to enforce.

Preventive controls can at least reduce the likelihood of incidents like the Bithumb crisis. Exchange-level internal control standards, segregation of customer assets, and mandatory real-time risk monitoring should all be discussed before circuit breakers.

It is better to design systems that prevent fires than to lock the door after one has already started.

Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.