Summary

What the market calls asset tokenization is only the visible tip of the iceberg. Beneath the surface lies a market worth hundreds of trillions of dollars that stands to restructure the foundational rails of conventional finance.

Many observers treat the placement of U.S. Treasuries onchain as the whole of the RWA market, but that view captures only the surface of a far larger capital market. The real transformation is taking place not in the visible digitization of assets, but in the wholesale reconstruction of the financial infrastructure that has long remained submerged: the clearing systems, settlement layers, and liquidity networks that underpin every transaction.

The scale of activity already underway makes this concrete. According to Broadridge, the firm processes roughly $7.7 trillion in onchain repo transactions each month, and the DTCC has moved into Treasury tokenization, with both operating not as pilot experiments but as live components of financial market structure. The Hong Kong government’s issuance of HKD 6 billion in digital green bonds through HSBC Orion, combined with the immediate deployment of repo collateral, demonstrates a future in which issuance and distribution form a single, uninterrupted process.

These developments share a common foundation: the Canton Network. Canton was designed from the outset for institutional use. It protects commercially sensitive information through Daml, its smart contract language, while eliminating counterparty risk through atomic settlement, the simultaneous exchange of assets and payment in real time. Its public permissioned structure satisfies Basel Committee on Banking Supervision (BCBS) requirements, giving global financial institutions a compliant path into the onchain ecosystem without material balance sheet burden.

Having built a substantial record of institutional deployments in Western markets, Canton is now extending its reach into Asia. Korea is emerging as a focal point: following the passage of security token offering (STO) legislation in 2026, which establishes the legal standing of distributed ledgers, major institutions including Hanwha Investment Securities, Shinhan Securities, Shinhan Asset Management, and KB Securities have moved quickly to join the Canton ecosystem in order to establish positions in global issuance and distribution networks.

The infrastructure layer of a new financial standard is being assembled now, and the institutions that engage at this stage will have shaped its architecture before later entrants arrive.

1. The Internet of 1996 and the RWA Market

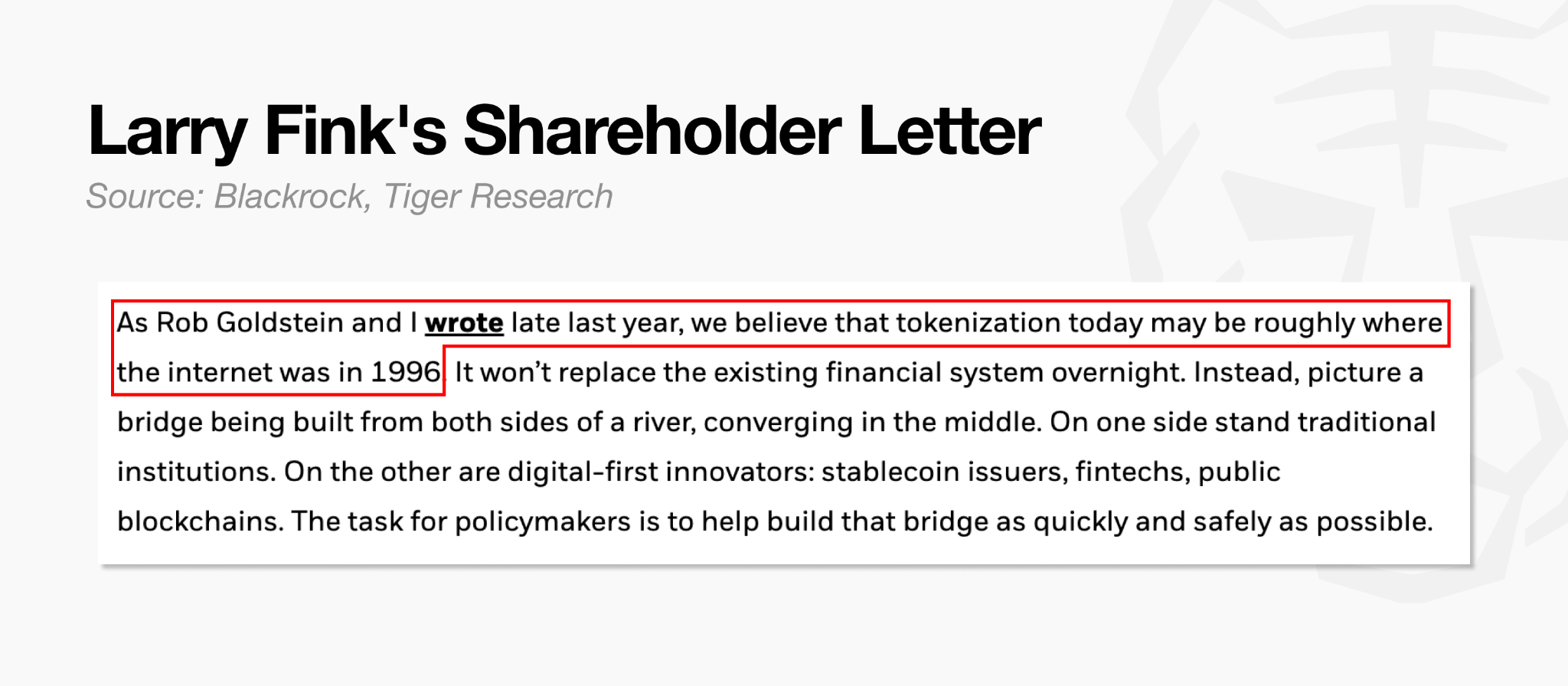

Larry Fink, CEO of BlackRock, wrote in his 2026 shareholder letter: “We believe tokenization today may be at a similar point as the internet in 1996.”

1996 was an inflection point. The internet existed, but most enterprises held back. Only 26% of Fortune 500 companies had integrated online commerce at the time. When early adopters demonstrated success, the rest rushed in, but by then, the early movers had already entrenched their positions.

The RWA tokenization market is at a similar juncture. Many institutions remain on the sidelines, yet leading cases are already emerging. The most prominent is BlackRock’s BUIDL (BlackRock USD Institutional Digital Liquidity Fund), a tokenized fund holding U.S. Treasuries onchain. Launched in March 2024, it expanded to seven blockchains within 18 months and, according to rwa.xyz, the fund grew to approximately $2.5 billion in market cap.

Scale alone does not capture the shift. The market has moved past simply putting real-world Treasuries onchain. New financial services are now being layered on top of issued assets. Multiple DeFi protocols have adopted BUIDL as a base asset, and Binance officially accepted BUIDL as trading collateral.

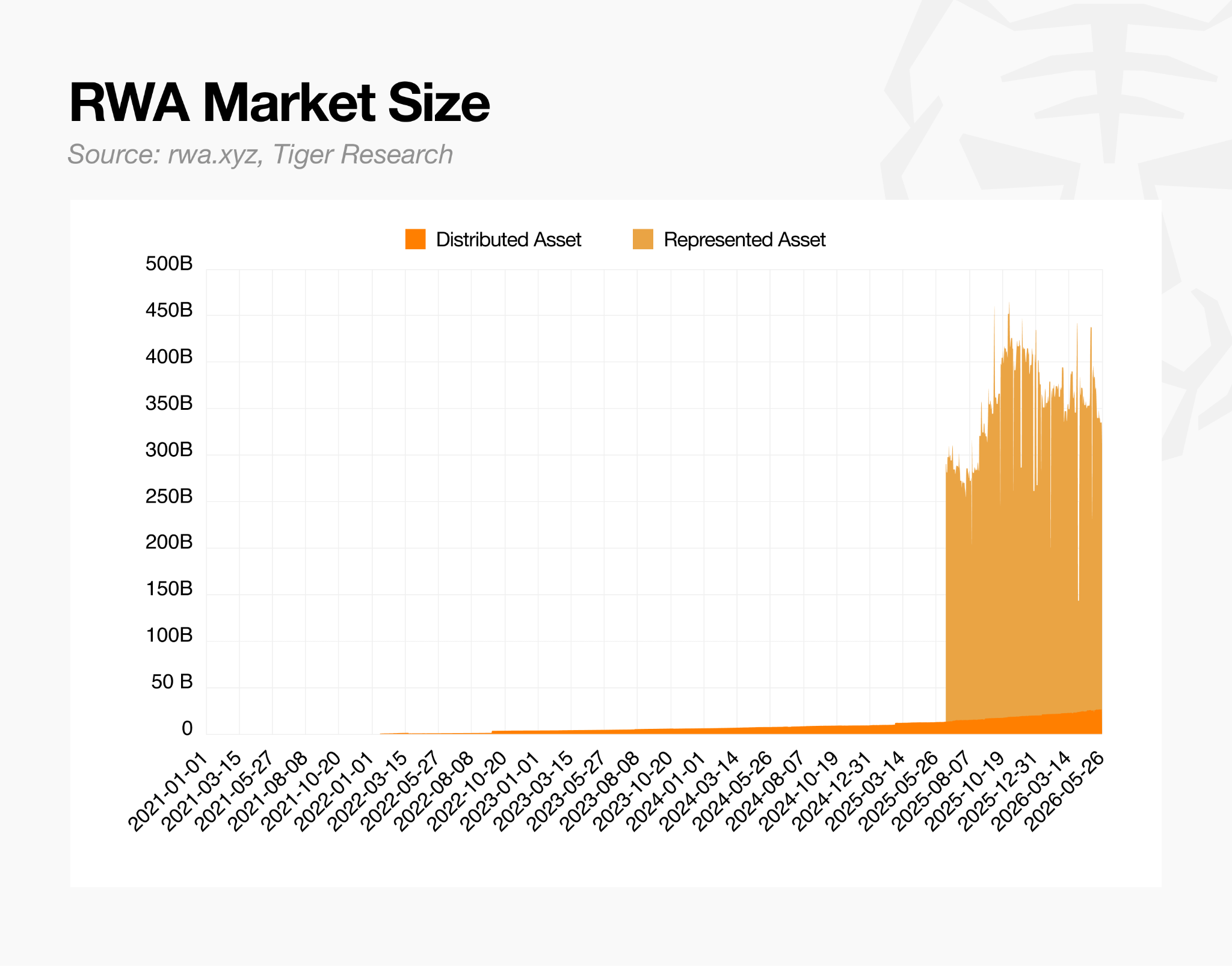

According to rwa.xyz, onchain-issued assets (Distributed Assets) stood at approximately $34 billion as of May 2026, more than 20 times the $1.5 billion recorded in early 2020. Adding Represented Assets, where physical assets remain with custodians, but ownership is recorded onchain, brings the total to approximately $360 billion.

2. The RWA Market Has Already Started

Tokenizing an asset is not just a matter of converting existing financial products into a digital format. It changes how those products work, including settlement speed, post-trade infrastructure, and the full processing stack. The approach is not to replace legacy systems but to build faster and more precise rails on top of them.

Most discussions of RWA tokenization stop at BlackRock’s BUIDL, a tokenized fund that issues U.S. Treasuries as tokens on a blockchain. BUIDL is a landmark case in the RWA market, but a single example is not enough to answer why tokenization matters.

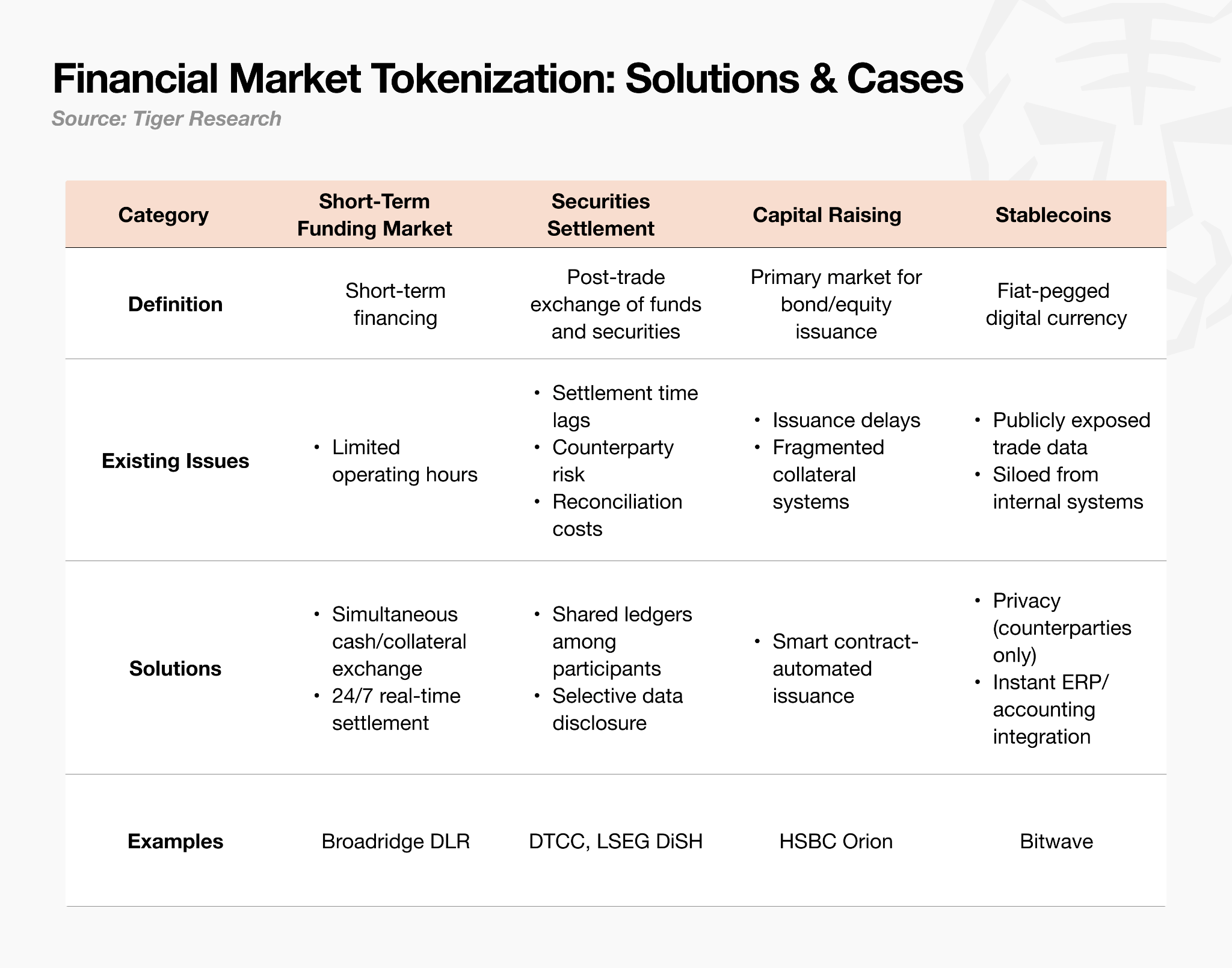

Finance spans far more than bond issuance. The repo market, securities settlement, and capital raising each carry distinct structural inefficiencies, and the value tokenization can unlock in each differs considerably. To understand why tokenization matters, each sub-market needs to be examined on its own terms.

Short-Term Funding (Repo)

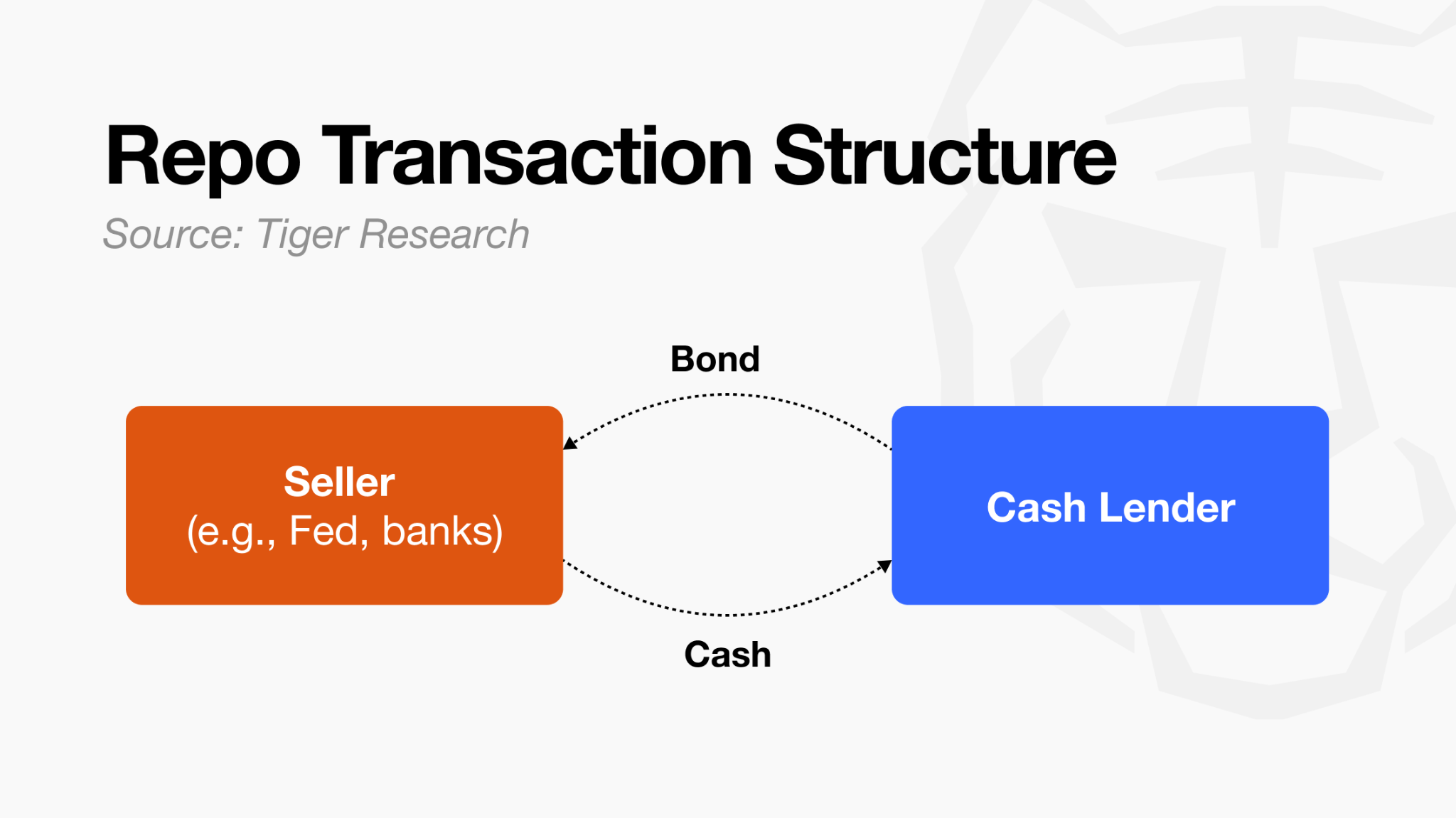

A repo (repurchase agreement) is the defining transaction of short-term funding markets. An institution pledges bonds as collateral to borrow cash, then returns the cash plus interest at maturity in exchange for the bonds. Most contracts are overnight. The collateral is safe, the rates are low, and the transaction is routine.

Problem

Limited operating hours

Repo markets operate only within system hours. On weekdays, settlement runs once a day. On weekends and holidays, it stops entirely. But risk does not stop with it.

If adverse news hits over the weekend, mark-to-market losses accumulate without settlement. When markets open Monday, the entire weekend’s accumulated exposure hits as a single margin call. Meeting that call immediately is not realistic. Selling bonds or monetizing them via repo takes time. The only solution is pre-positioned cash held in reserve, capital that sits idle precisely because the settlement infrastructure cannot move continuously.

Solution

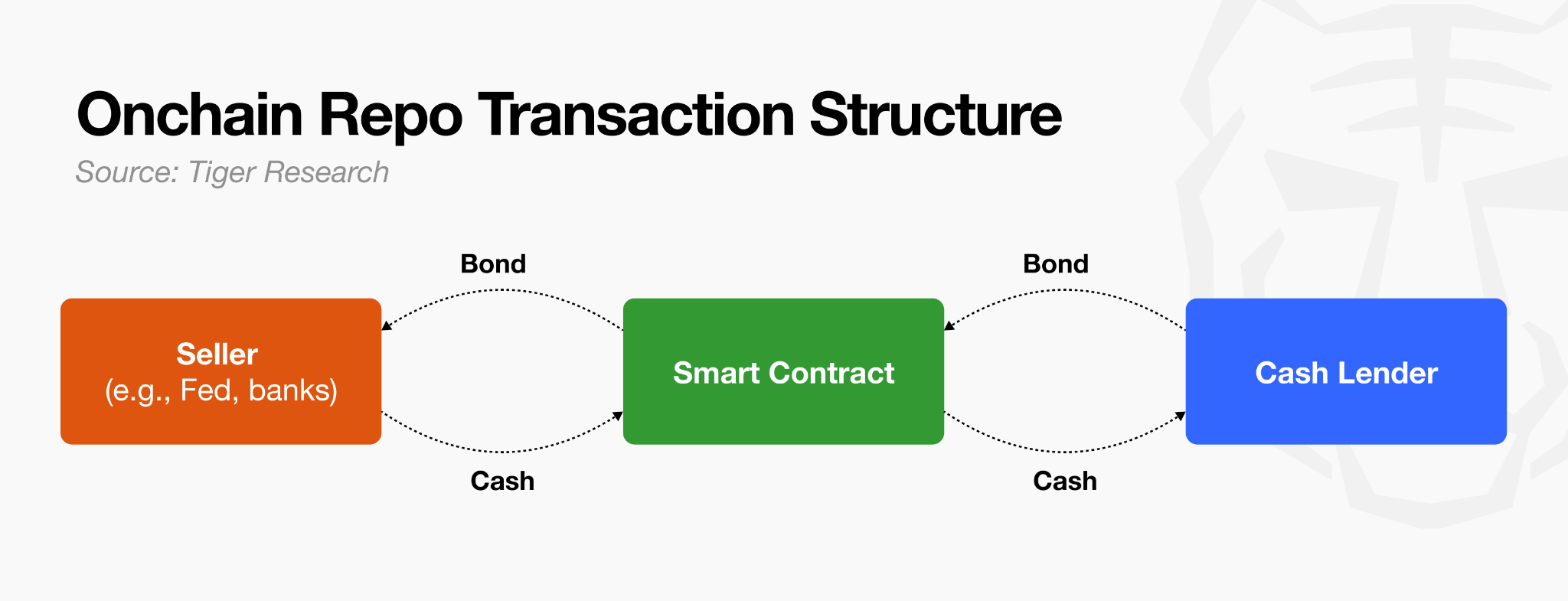

Onchain repo solves this problem at the structural level. The core is the DvP (Delivery versus Payment) mechanism. It works on the same principle as paying for an item at the cash register: collateral and cash are exchanged simultaneously, and it is structurally impossible for one side to transfer first.

In practice, the transaction works as follows. The party seeking funds posts the amount, rate, and maturity terms, and the counterparty accepts. Both sides deposit their respective assets into a smart contract, a digital agreement that executes automatically when conditions are met. The cash borrower deposits tokenized bonds; the cash lender deposits tokenized cash. The moment both confirmations are received, the exchange completes automatically.

Tokenized bonds and stablecoins move onchain 24 hours a day. Because they do not depend on legacy settlement infrastructure, collateral can be moved on a Friday afternoon or a Sunday morning. The constraint of system operating hours disappears.

Settlement frequency changes as well. Under the legacy system, manual confirmation limited settlement to once a day. Smart contracts automatically trigger margin calls and settlement the moment a position incurs a loss. With no gaps, there is less reason to pre-position excess cash reserves.

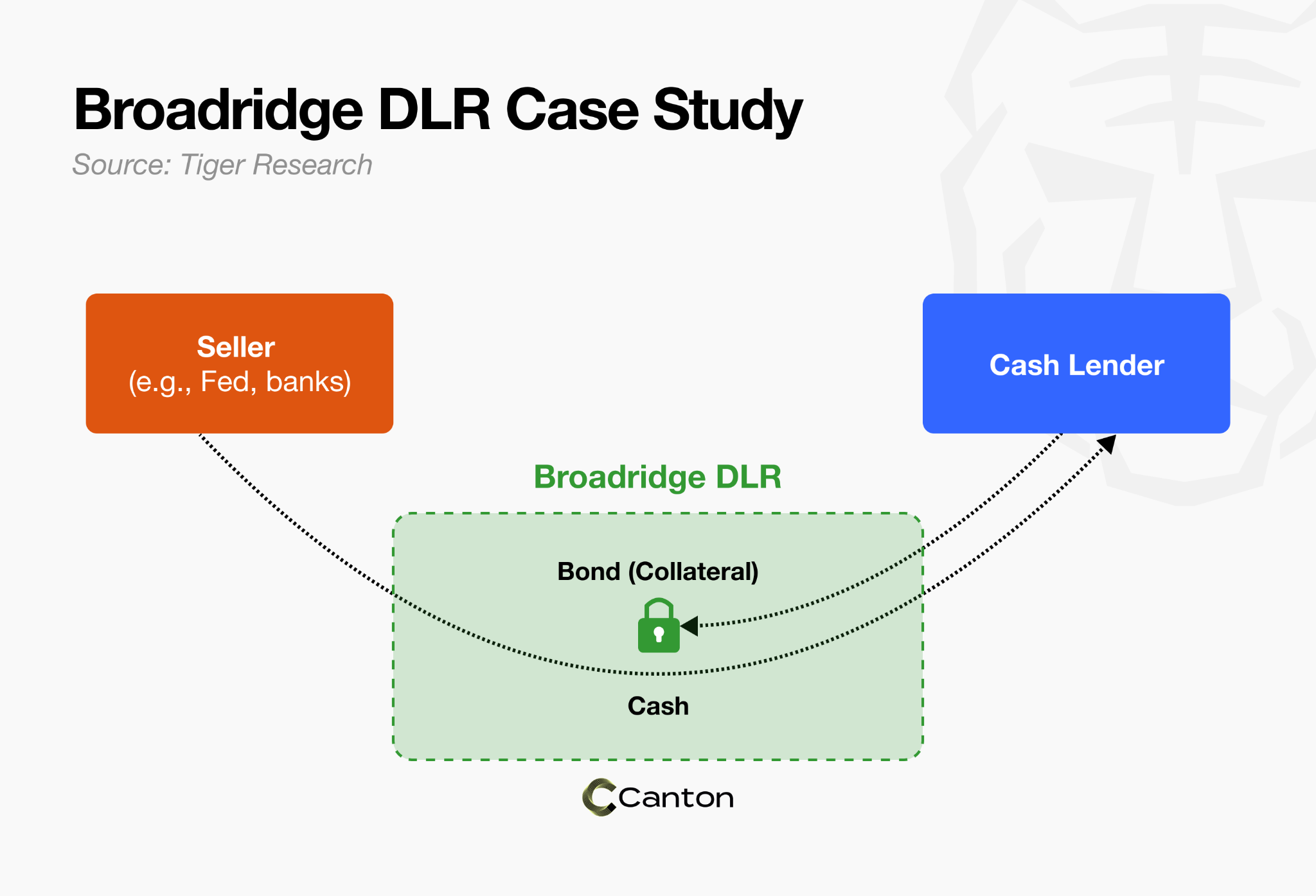

Case Study: Broadridge DLR

Broadridge is a global capital markets infrastructure firm that handles settlement and clearing processes for banks and broker-dealers through technology. The company launched DLR (Distributed Ledger Repo), a distributed ledger-based repo trading platform built on the Canton Network as its underlying blockchain.

Because DLR is blockchain-based, it is not bound by the operating hours of legacy settlement infrastructure. Collateral movement and settlement are available on weekends and public holidays, and repo transactions can be initiated and closed at any point in the day. The risks that arose from limited system operating hours are structurally reduced. Smart contracts also automate the full repo lifecycle, reducing settlement failures and disputes while improving collateral reusability.

As of April 2026, DLR processes $7.7 trillion in monthly settlement volume and $368 billion in average daily volume. HSBC, UBS, and Société Générale are among the global banks already participating on the platform.

Securities Settlement Infrastructure

Securities settlement is the stage after a trade is executed, where the buyer delivers payment and the seller delivers the securities. T refers to the trade date. Under standard practice, settlement occurs on T+1 or T+2, meaning funds do not move until at least one to two days after the trade.

Problems

Problem 1: Settlement Lag and Counterparty Risk

A real estate transaction is a useful analogy. Signing a purchase contract does not transfer the title or the final payment. Those happen days later. The trade and the asset transfer occur at different points in time.

As noted above, the current securities settlement infrastructure creates a time gap between trade execution and asset transfer. If a counterparty defaults during that window, significant losses follow.

Central Counterparty Clearinghouses (CCPs) exist to prevent this. A CCP interposes itself between buyer and seller so that if one side defaults, the other does not absorb the loss directly. In the United States, the NSCC fills this role. In Korea, it is the clearing and settlement division of the Korea Exchange (KRX).

Historically, no CCP has reached outright default. The systemic consequences of a CCP failure are severe enough that member institutions and governments have intervened before that point. CCPs have, however, been pushed to their limits under extreme market conditions.

During Black Monday in 1987, the Hong Kong Futures Exchange clearinghouse was brought to the brink of insolvency by mass margin call failures. The Hong Kong government injected public funds and halted trading for four days before the situation was resolved. In the 2008 Lehman Brothers collapse and the 2018 Nasdaq Clearing crisis, portions of loss-absorption funds were actually depleted.

Problem 2: Fragmented Ledgers and Reconciliation Costs

When a single equity trade is executed, the issuer, custodian, clearinghouse, and settlement institution each record it separately in their own ledgers. The same transaction is entered four times across four institutions. As these ledgers do not synchronize in real time, they are matched up retroactively using standardized message formats. This process is called reconciliation.

The ledgers do not always match. Each institution processes the same trade at different times, and differences in internal system formats mean data can be lost or altered during message conversion. When records differ, staff must manually identify and correct the discrepancy. Some steps are automated, but errors persist.

This is why ongoing operational headcount and systems costs for reconciliation and position breaks remain a permanent fixture. Corporate actions, events that affect company structure or shareholder rights such as dividends, stock splits, and mergers, add further complexity. Each institution must update its ledger independently and run reconciliation again, multiplying the workload.

Solution

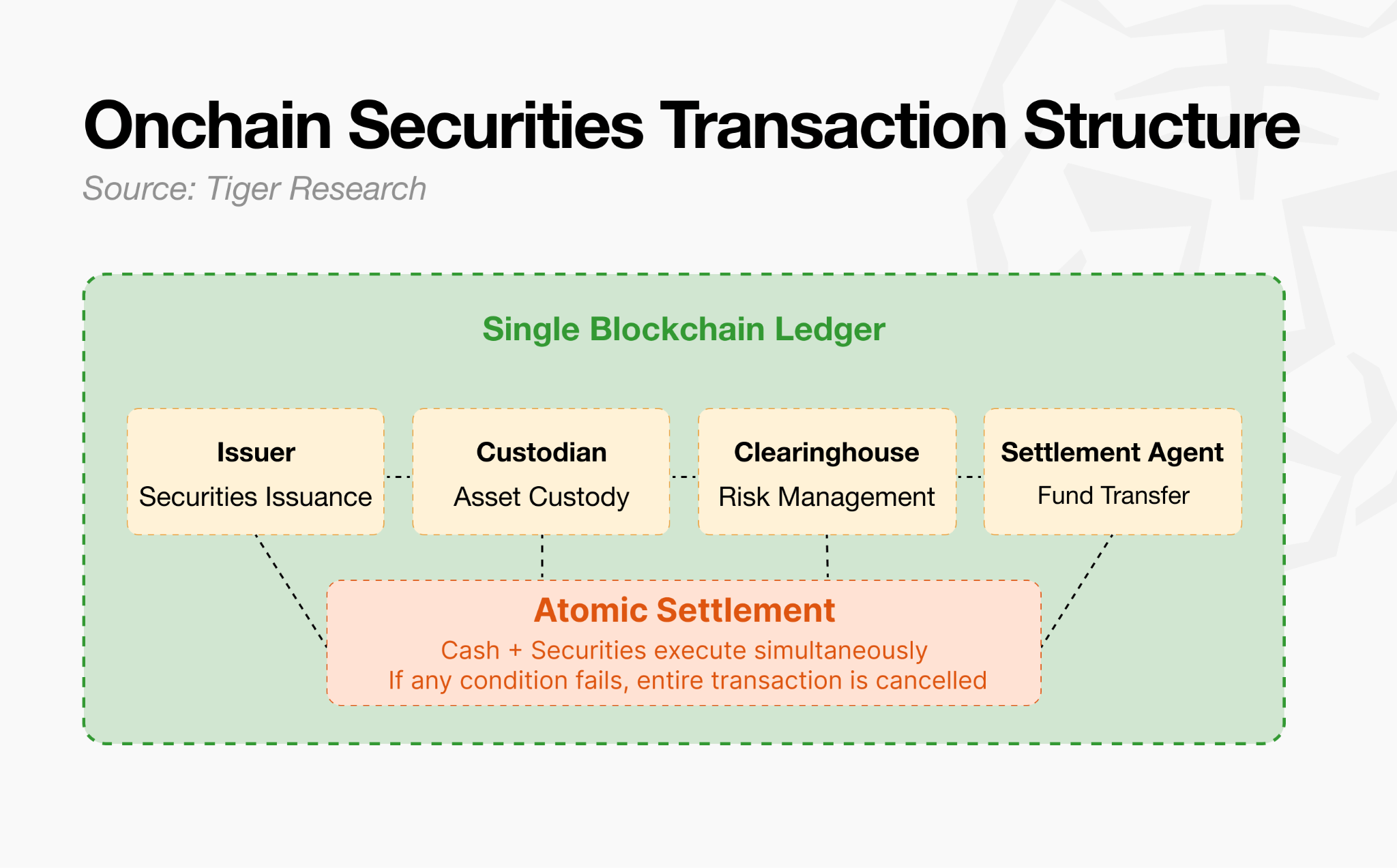

Moving securities settlement infrastructure onchain changes two things. All participants see the same ledger, and trade execution and asset transfer happen simultaneously.

Moving securities settlement infrastructure onchain addresses both problems through a single structural change: all participants share one authoritative ledger, and trade execution and asset transfer occur within the same transaction. The shared ledger means every participant’s data updates simultaneously when a trade is recorded, eliminating retroactive reconciliation. The unified environment for cash and securities removes the settlement lag that creates counterparty exposure.

When cash and securities are both onchain, trade execution and asset transfer can be bundled into a single transaction. Today, cash moves through the banking system and securities move through the central securities depository separately. Onchain, both exist in the same environment and execute simultaneously.

This is Atomic Settlement. If all conditions are met, the entire transaction succeeds. If any single condition fails, the entire transaction is cancelled.

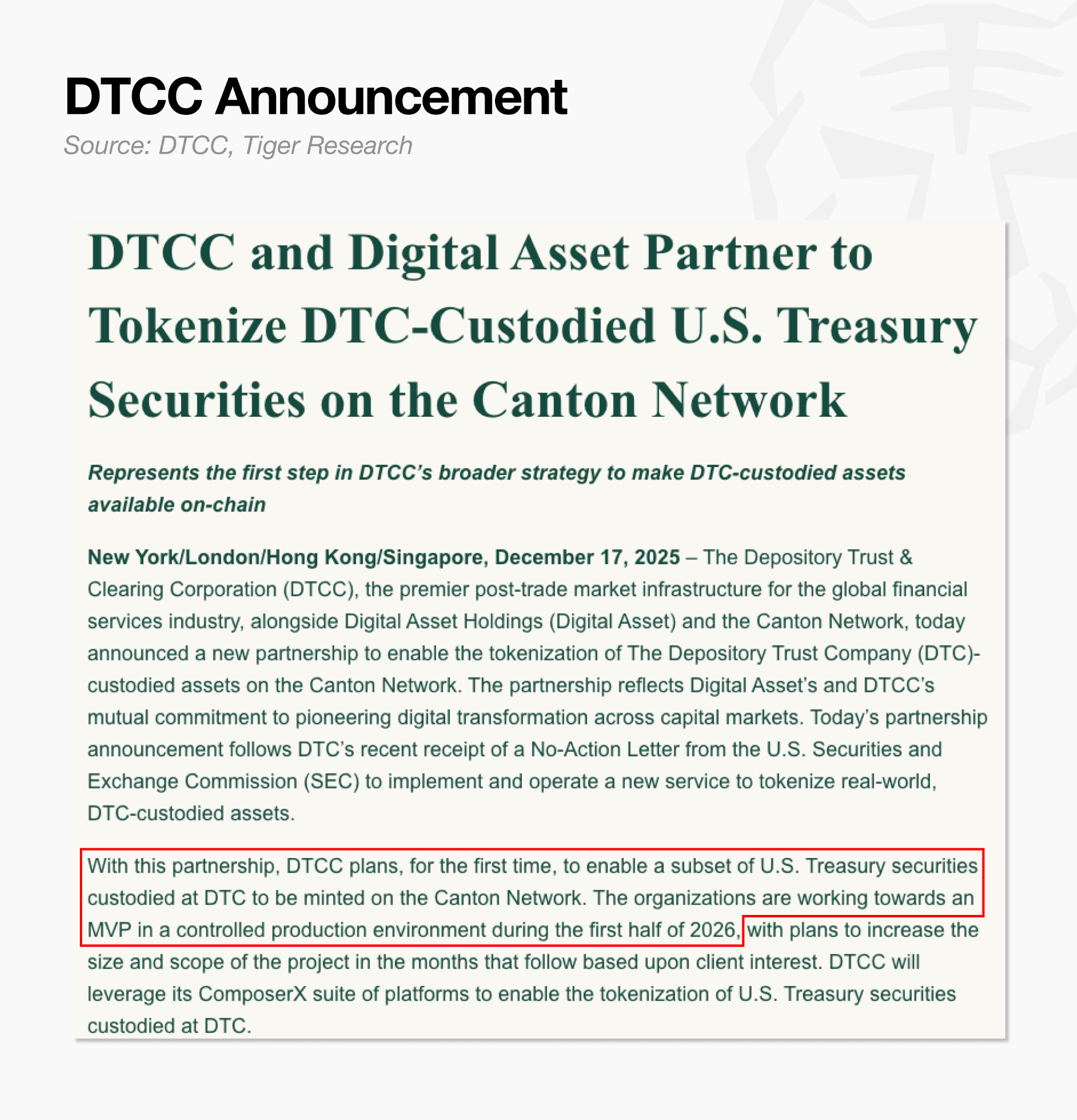

Case Study: DTCC

Onchain securities settlement is already operating in live transactions. The London Stock Exchange Group (LSEG) deployed its digital settlement platform DiSH on Canton and applied it to securities settlement. Lloyds Bank completed a transaction purchasing tokenized UK gilts with tokenized deposits. From issuance to settlement, the entire process was handled onchain.

The most significant case is DTCC. The Depository Trust & Clearing Corporation is the core infrastructure of U.S. securities settlement, processing the clearing and settlement of most securities traded in the United States.

Partnering with Digital Asset, the company behind the Canton Network, DTCC received a no-action letter from the SEC in December 2025, a regulatory pre-commitment not to take action against a specified activity. The target is an MVP (minimum viable product) launch in the first half of 2026.

For an institution where a single settlement failure could trigger license revocation, the decision to adopt onchain infrastructure is not a casual experiment. It reflects a considered judgment that the risks embedded in the current settlement architecture outweigh the operational risk of moving to new rails.

Capital Raising

The capital raising market is where governments and corporations issue bonds and equities to raise funds. It divides into a primary market, where new securities are issued, and a secondary market, where issued securities are traded and utilized among investors. A bond represents a promise to repay borrowed principal plus interest at maturity; an equity grants the holder an ownership stake in the issuing company.

Problems

Problem 1: Issuance Process Delays

The longer the preparation period, the more variables outside the issuer’s control accumulate. Hedging costs accrue, investor demand can shift, and in the worst case the deal falls apart entirely. Each week added to the timeline is a week of exposure to conditions the issuer cannot control.

Problem 2: Fragmented Collateral Systems

Institutional investors buy assets for the yield. The issue is what comes next. If purchased assets can be deployed in repo, posted as collateral, or linked to other transactions, capital keeps working. The smoother those connections, the more transactions the same asset can support, and the more valuable the asset becomes from the issuer’s perspective.

But even when counterparties have agreed on collateral utilization, execution is difficult. A collateral transaction requires eligibility verification, haircut calculation, and title transfer to proceed in sequence, with a different institution involved at each step.

These institutions’ systems are not connected to one another. At each stage, staff must send messages and wait for confirmation. In this structure, the volume of issued assets has little bearing on what can actually be put to work, which is a considerably smaller figure.

Solution

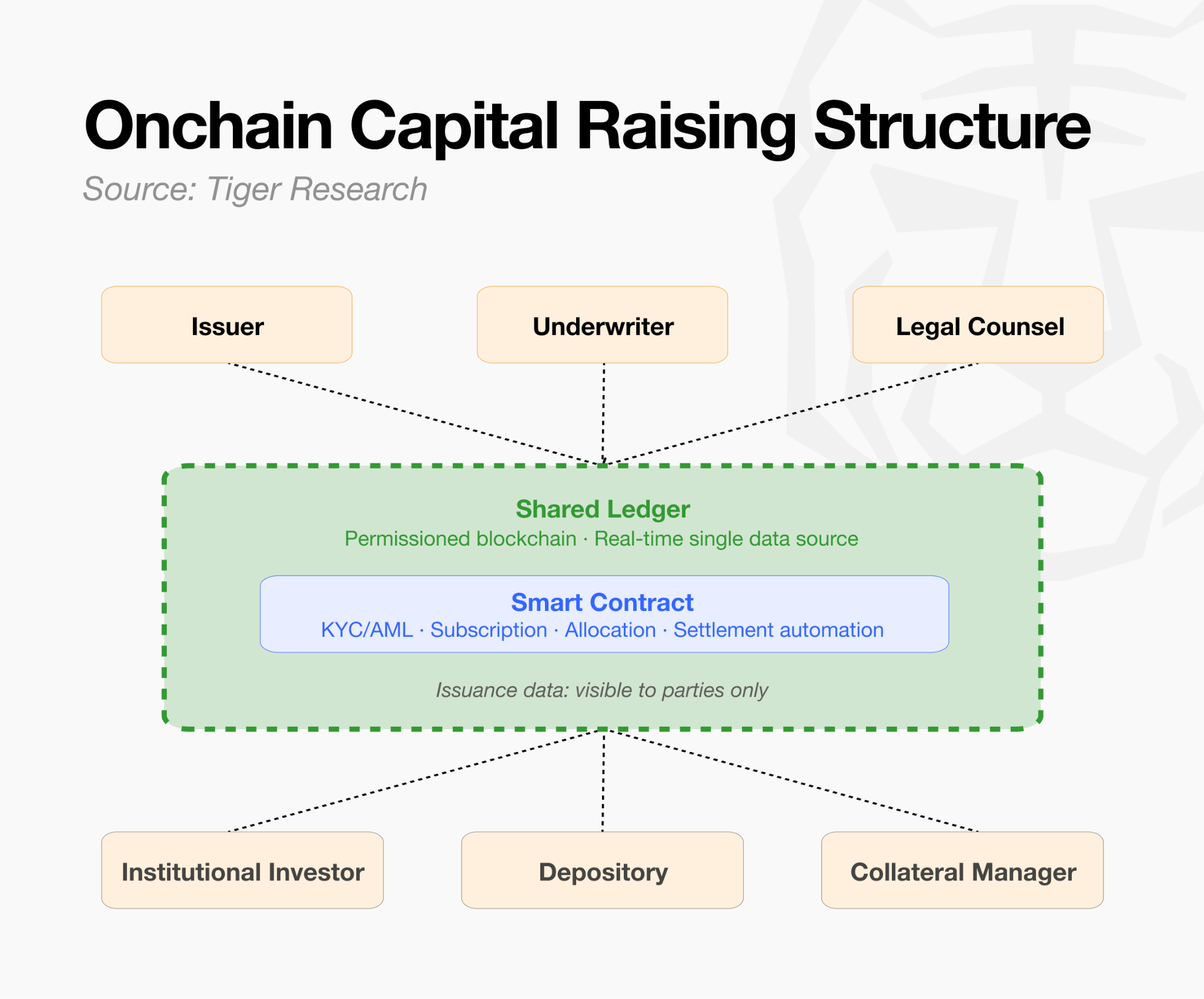

Onchain issuance approaches both problems differently.

The entire issuance process runs on smart contracts. Within regulatory parameters, agreed issuance terms are defined in code. After KYC and AML verification, subscriber registration, allocation, and payment settlement are processed automatically. The steps where staff manually confirmed and converted messages are eliminated, compressing the issuance cycle significantly.

The post-issuance utilization structure changes as well. Tokenized assets exist in an environment where all participating institutions share the same data in real time on the same network. Eligibility verification, haircut calculation, and title transfer for collateral transactions are handled within a single flow, without passing between separate systems. The ledgers that issuers, underwriters, depositories, and collateral managers once maintained separately consolidate into one. Once an asset is issued and adopted, it can immediately serve as collateral or an underlying asset for other transactions.

One prerequisite must be addressed for this model to take hold. Issuance privacy. Issuance terms, underwriter allocations, subscription prices, and investor lists are data that cannot be exposed to the market. If that information leaks, market prices move in advance and issuers absorb more expensive terms. Existing public permissionless blockchains conceal only wallet addresses while exposing all transaction data to everyone. For onchain issuance to scale, it must operate on permissioned infrastructure where transaction data is visible only to the parties involved.

Case Study: HSBC Orion

HSBC is a UK-based global bank with $3 trillion in assets. One of the leading institutions in bond underwriting and issuance, it launched its own digital asset platform, HSBC Orion, in 2023 to serve as digital bond issuance infrastructure. HSBC Orion operates on the Canton Network.

In February 2024, the Hong Kong government issued HKD 6 billion (approximately USD 770 million) in digital green bonds through HSBC Orion. It was the first government-issued digital bond denominated in multiple currencies simultaneously, covering HKD, CNH, EUR, and USD. More than 50 global investors across eight nationalities participated, an unusually large participation base for an early-stage digital bond issuance. The settlement cycle was compressed from T+5 to T+1.

The significance of this issuance lies not in the issuance itself but in what followed. Within days of completion, HSBC and the Bank of East Asia (BEA) entered into a repo transaction using the digital green bond as collateral. The moment the bond was live in the market, it was immediately put to use as collateral on the same network. It was the first confirmed instance of issuance and utilization connecting without interruption.

The structure works as follows. When HSBC Orion issues a digital green bond, the bond is recorded as a token in a Bond Registry on Canton. When HSBC and BEA execute a repo transaction, a separate application on the same Canton network takes the token as collateral and settles payment simultaneously.

The Hong Kong government did not treat this issuance as a one-off. Following the transaction, the HKMA launched the Digital Bond Grant Scheme, committing to subsidize half the issuance costs for issuers who issue digital bonds. The intent is to convert a single experiment into a standard for market infrastructure.

Digital Payment Currency (Stablecoins & Payments)

Stablecoins are digital currencies pegged 1:1 to the US dollar. Unlike conventional cryptocurrencies, their value is largely stable, making them function as currency moving on a blockchain. USDC and USDT are the leading examples.

Problems

Problem 1: Public Transaction Data

On public blockchains, all transactions are visible to anyone. Who sent what amount to whom, when, and with what balance can be retrieved instantly by searching a single wallet address on a block explorer, a tool for querying blockchain transaction records.

Analyzing a company’s stablecoin payment history reveals unit prices negotiated with counterparties, seasonal revenue patterns, new market entry timing, M&A fund flows, and executive compensation.

There are clear efficiency gains in payment. Full public exposure of transaction data, however, is a structural limitation.

Problem 2: Disconnection from Internal Systems

When a company receives a stablecoin payment, the funds arrive in a blockchain wallet that sits entirely outside its accounting system, ERP, and treasury platform. Before that money can be used, the treasury team must manually withdraw it to a bank account, book the accounting entries, and route it to wherever it needs to go. Each of those steps requires manual intervention and time. A payment that arrived in seconds can take hours or days to become operationally available, erasing the speed advantage entirely.

Solution

Changing the blockchain infrastructure design addresses both problems structurally.

Transaction data is visible only to the parties involved. Payment amounts, counterparties, and balances are not exposed externally. Only authorized regulators and compliance partners can access the records. Privacy and oversight operate together.

When a payment arrives, it connects directly to the ERP and accounting system, putting the funds to work immediately without intermediate steps.

Case Study: Bitwave

Bitwave is a US-based digital asset accounting and treasury platform. It integrates with major ERPs including NetSuite, QuickBooks, and Sage Intacct. Bitwave built a private stablecoin-based B2B payment infrastructure on the Canton Network.

When an invoice is issued, Bitwave generates a payment via smart contract on the network. The moment the payment executes, revenue is automatically recorded in the sender’s ERP and a payable is recorded in the recipient’s ERP. SOC compliance audits run on the same data. Payment, accounting, and compliance are completed within a single workflow.

Transaction data does not leave the network. Only the two parties and authorized auditors can view the records. Other participants in the network cannot see the transaction at all. Commercial information such as counterparty pricing, revenue patterns, and transaction frequency is fully protected. This is the result of Daml, Canton’s smart contract language, being designed to block transaction visibility to non-parties by default.

3. Where All These Cases Converge: Canton Network

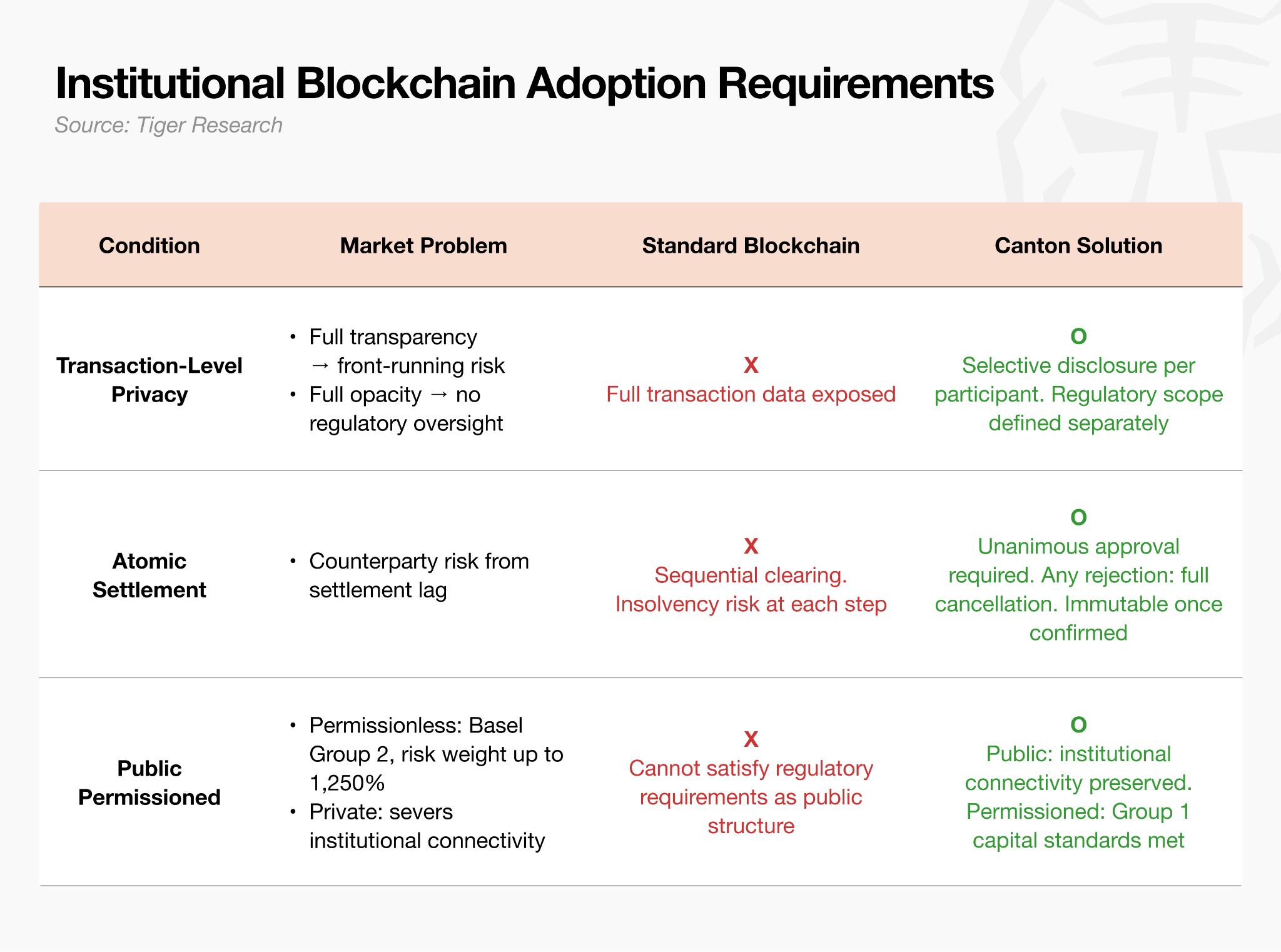

The cases covered above span different sectors and involve different institutions. All of them run on the Canton Network because the infrastructure satisfies the three conditions that institutions require.

Condition 1: Transaction-Level Privacy

In government bond repo transactions, participating institutions saw only the transactions they were party to. Stablecoin payments concluded without balances or counterparty information being exposed to the market.

If transaction data is open to everyone, positions are visible to the market and participants are exposed to front-running risk. Blocking all information prevents regulators from oversight. What is needed is a structure where the parties to a transaction see everything, regulators see what they need for supervision, and all other participants are blocked from information irrelevant to them.

The Canton Network implements sub-transaction privacy at the protocol level, with smart contracts delivering to each participant only the portion of a transaction relevant to them. In an exchange involving securities and cash, the bank sees only the cash movement and the securities registry sees only the securities movement, while the seller, buyer, and transaction application see both sides. This selective visibility aligns directly with regulatory audit requirements.

Elliptic and TRM Labs are connected as Super Validators and integration partners, conducting AML oversight and maintaining compatibility with major jurisdictions’ reporting requirements.

Condition 2: Atomic Settlement and Cross-Application Interoperability

In government bond repo transactions, tokenized government bonds and cash were exchanged in a single transaction. The digital green bond issued by HSBC was immediately used as repo collateral by BEA within days of issuance.

For these transactions to work, atomic settlement is required. Every step must complete simultaneously or cancel simultaneously. Selling a government bond and receiving cash typically takes two days, passing sequentially through a clearinghouse, custodian bank, and settlement system. If one party has already transferred its asset and the counterparty becomes insolvent, the party that performed first absorbs the loss. The Lehman Brothers collapse illustrated the consequence: unsettled trades locked up markets for weeks precisely because one side had already transferred assets when the other became insolvent.

Atomic settlement eliminates the problem. When a transaction is initiated, all parties verify the validity of their respective positions and send approval signals. Execution requires unanimous approval. If any single party rejects, the entire transaction is cancelled. Once confirmed, a transaction cannot be reversed.

Condition 3: Public Permissioned Structure

There is a reason conservative global financial institutions such as HSBC, UBS, Société Générale, and LSEG appear repeatedly across Canton use cases.

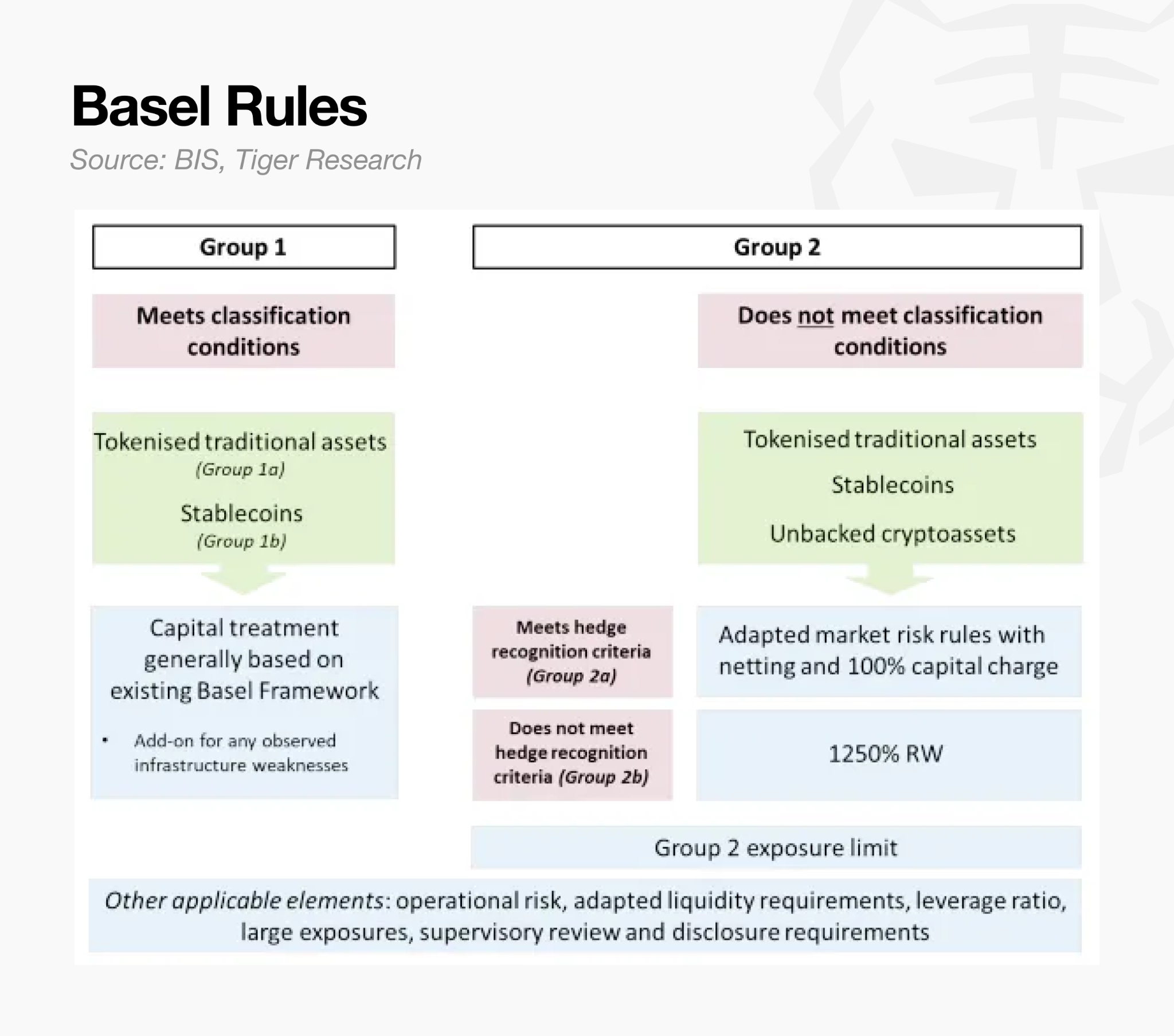

In December 2022, the Basel Committee on Banking Supervision (BCBS) divided tokenized assets into two classifications. Group 1 covers tokenized traditional assets and stablecoins, subject to the same capital requirements as their underlying assets. Group 2 covers assets issued on permissionless blockchains, carrying a risk weight of up to 1,250%. That is the equivalent of holding capital equal to the full value of the asset.

The same bond carries an entirely different capital burden depending on which blockchain it sits on. A fund like BlackRock’s BUIDL, which grew on Ethereum, was viable because its primary holders were exchanges, DeFi protocols, and crypto funds, entities outside the Basel regulatory perimeter.

For regulated global banks to hold the same asset on their balance sheets, two options exist. Permissionless chains are classified as Group 2, creating significant capital pressure. Closed private chains avoid regulatory friction but sever institutional connectivity.

The Canton Network aims to address this through a public permissioned structure. Application providers define participant verification standards and access permissions directly. Each transaction is validated only by the nodes that are parties to that transaction.

By seeking to mitigate the core risk factors that Basel identified in permissionless chains, the network is designed to align with characteristics generally associated with BCBS Group 1 treatment.

4. Canton Network’s Institutional Design Architecture

The Canton Network was designed for institutional finance from the ground up. Digital Asset, the company that developed the Canton protocol and the Daml smart contract language, received investment from global institutions including JPMorgan, Citi, Goldman Sachs, and DTCC.

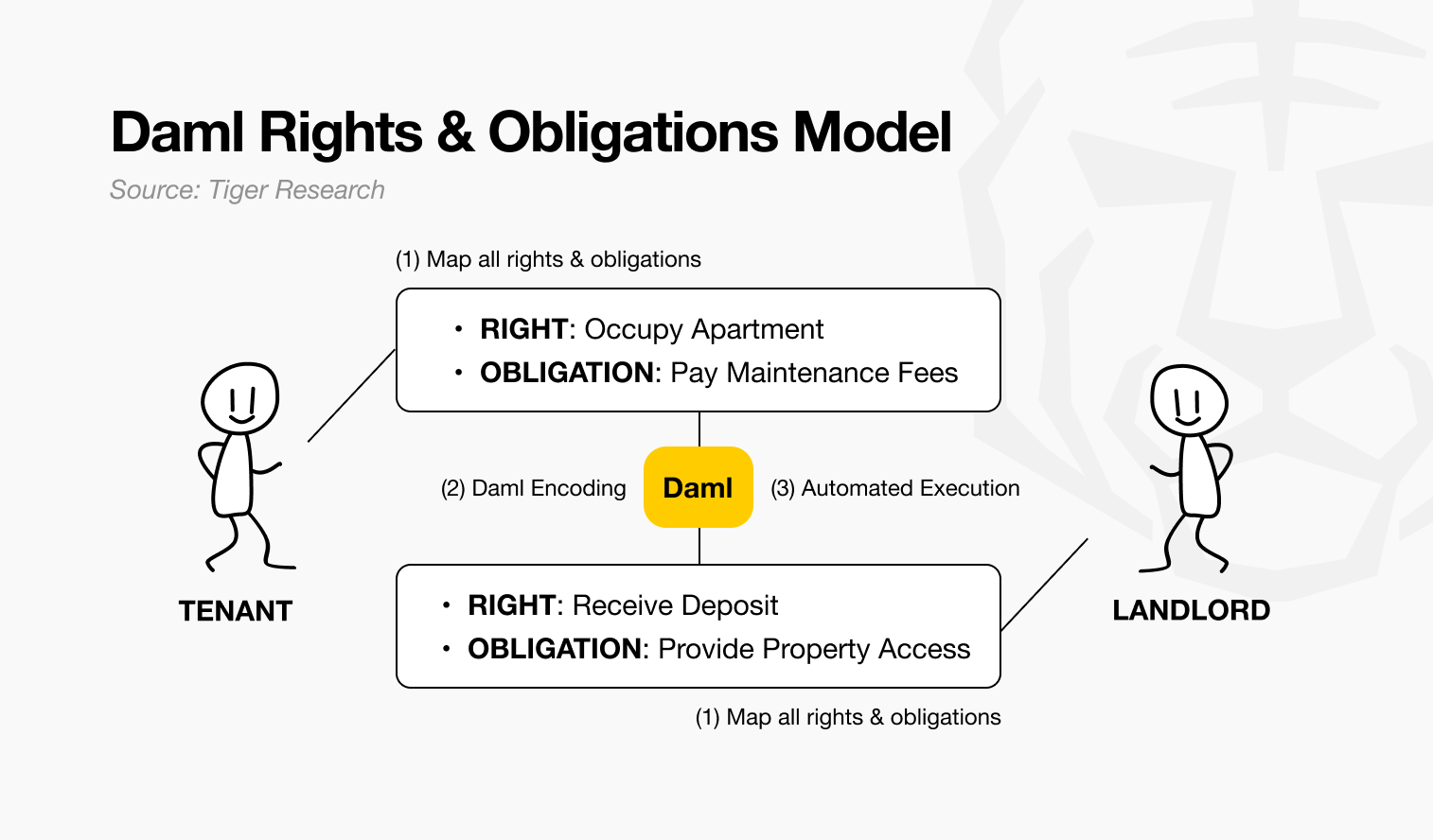

Daml: Authorization and Privacy Built Into the Language

In institutional finance, access control is not a peripheral requirement. It is the substance of the transaction itself. In bond issuance, if underwriter allocation data leaks, market prices move in advance. In repo, if collateral size is exposed, the counterparty loses negotiating leverage. Authorization is not an add-on to a transaction. It is part of the transaction.

The Canton Network uses Daml to define data permissions at the code level. When writing a contract, the same code specifies who is a signatory, who is an observer, and who is a controller authorized to execute specific actions. Business logic and privacy policy are not managed separately. The contract itself defines who can do what.

Canton Protocol: Consensus Validated Only by the Parties to a Transaction

If Daml defines authorization, the next question is how that authorization is enforced in actual transactions. Standard blockchains record every transaction identically across tens of thousands of nodes worldwide. If transaction data can be read through any node, the privacy defined earlier becomes meaningless.

Canton resolves this by limiting visibility and validation to the parties with a stake in the transaction.

Sub-transaction Privacy: Within a single transaction, each party receives only the portion relevant to them. Transaction data is end-to-end encrypted, and decryption keys are delivered only to those with the appropriate permissions as defined by Daml.

Proof-of-Stakeholder: The parties to a transaction are its validators. Third parties cannot see the data. False validation does not hold. If the transaction records of both sides do not match, the discrepancy is immediately surfaced. If either party rejects, the transaction does not proceed.

Those who should not see, neither see nor validate. Those who should see, validate only what they can see.

Network of Networks: An Internet-Like Architecture of Connected Subnets

Each institution has different authorization policies, governance structures, and fee models. There is no reason for one institution to adopt another’s rules wholesale. The Canton Network allows each participant to build subnets in the structure they require.

Participants are controlled via whitelist. Governance policy determines whether transaction approval rests with a single operator or a consortium majority. Fee structures, processing speed, and compliance check timing are all configured differently per subnet.

With multiple subnets, the question is how transactions between them are handled. A standard bridge locks assets on one side and mints new ones on the other. If a single set of custodial keys is compromised, the entire asset pool collapses. The combined losses from the Ronin, Wormhole, and Nomad hacks alone exceeded $1 billion. Canton does not move assets. It leaves assets in place on each subnet and updates ownership on both ledgers simultaneously.

Take the HSBC and BEA collateral transaction as an example. The bond issued by HSBC remains on the HSBC subnet. BEA’s repo application executes the transaction using that bond as collateral directly. HSBC validates the bond leg under its subnet rules; BEA validates the cash leg under its own. When both subnets send their approval signals, ownership on both ledgers updates simultaneously.

Global Synchronizer: Infrastructure That Synchronizes Transactions Without Seeing the Data

With multiple subnets, there needs to be infrastructure that determines the order of transactions between them. But if that infrastructure can read the transaction data, the entire privacy architecture collapses. A structure where data is hidden from the parties but visible to the operator exposes the most sensitive information to the widest possible audience.

The Global Synchronizer resolves this contradiction. It orders transactions without the authority to decrypt their contents. Like a postal service delivering sealed envelopes, it receives messages, assigns order, and delivers to the destination without knowing what is being transacted.

The validation structure operates in two layers.

Validators: Verify application-level transactions and see only the transactions in which they are a party.

Super Validators: Operate the Global Synchronizer and reach consensus on transaction ordering, but cannot see transaction data.

According to Canton Network data, Super Validators are restricted to identity-verified institutions and have expanded to more than 45 as of April 2026, keeping infrastructure operation and data access structurally separate.

CIP-56: The Standard That Assets Follow

If the preceding four components are infrastructure, CIP-56 is the ruleset that assets on top of that infrastructure must follow. Assets that do not conform to a standard are incompatible with wallets, exchanges, and payment applications. If compliance procedures such as KYC cannot be embedded within the standard, institutions must operate separate systems alongside.

CIP-56 is the interface standard defining the issuance and transfer of tokens on Canton. It is the Canton equivalent of Ethereum’s ERC-20, with three additions built for the institutional environment.

Privacy-preserving balance management: Balances and transaction history are visible only to authorized parties. Unlike ERC-20, wallet balances are not publicly exposed.

Multi-party transfer approval: A transfer is completed only after both the token issuer and the recipient provide approval. KYC and whitelisting are embedded within the token standard itself.

Native atomic DvP support: Assets and cash are exchanged simultaneously within a single transaction. In ERC-20, this requires a separate smart contract or DEX infrastructure.

Assets conforming to CIP-56 operate as-is across all compatible wallets, exchanges, and applications. Bitwave’s USDCx payments and the real-time onchain repo of U.S. Treasuries against USDC executed by Tradeweb in December 2025 were both built on CIP-56.

5. The Canton Network Expands Into Asia

Canton Network has spent the past several years building its institutional infrastructure base and establishing its presence in the United States and Europe through a growing body of real-world cases. That expansion is now extending into Asia.

Korea stands out for the pace of activity. Amendments to the Capital Markets Act and the Electronic Securities Act, establishing a legal framework for security token offerings (STOs), passed the National Assembly on January 15, 2026, as announced by the Financial Services Commission of Korea. Distributed ledgers are now formally recognized as electronic registration account books with legal effect, giving rights recorded on blockchain the same legal standing as those under existing electronic securities law. The amendments take effect in January 2027.

The government has also designated “digital asset ecosystem development” as one of the 123 national policy priorities under the Financial Services Commission’s mandate, and has signaled that it will move quickly to establish a legal framework for won-denominated stablecoins.

Institutions did not wait for the legislation to be finalized. Major brokerages including Mirae Asset, Korea Investment Securities, and NH Investment Securities have already completed system builds through STO consortia. Banks are forming custody alliances and positioning for leadership in the space.

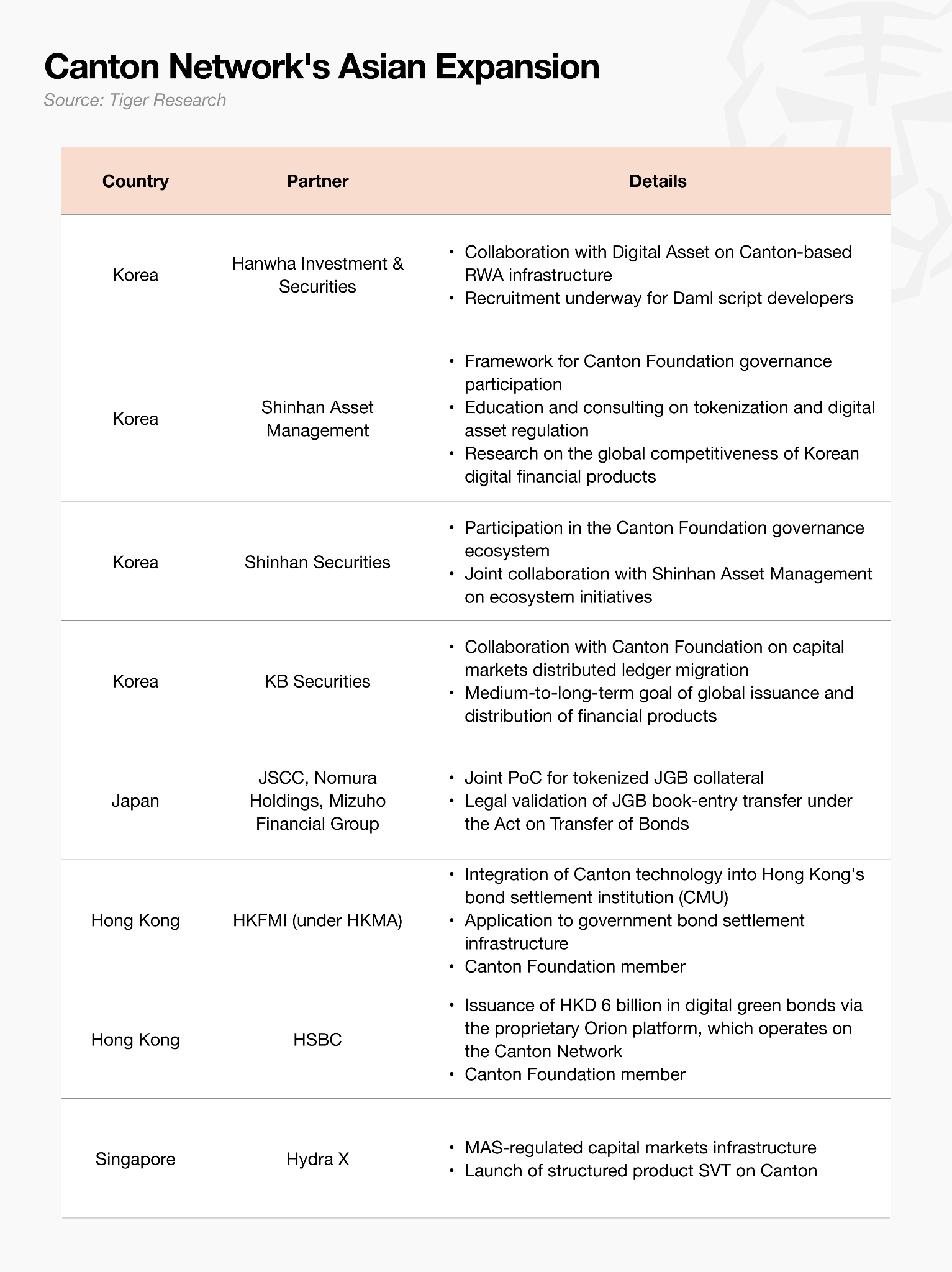

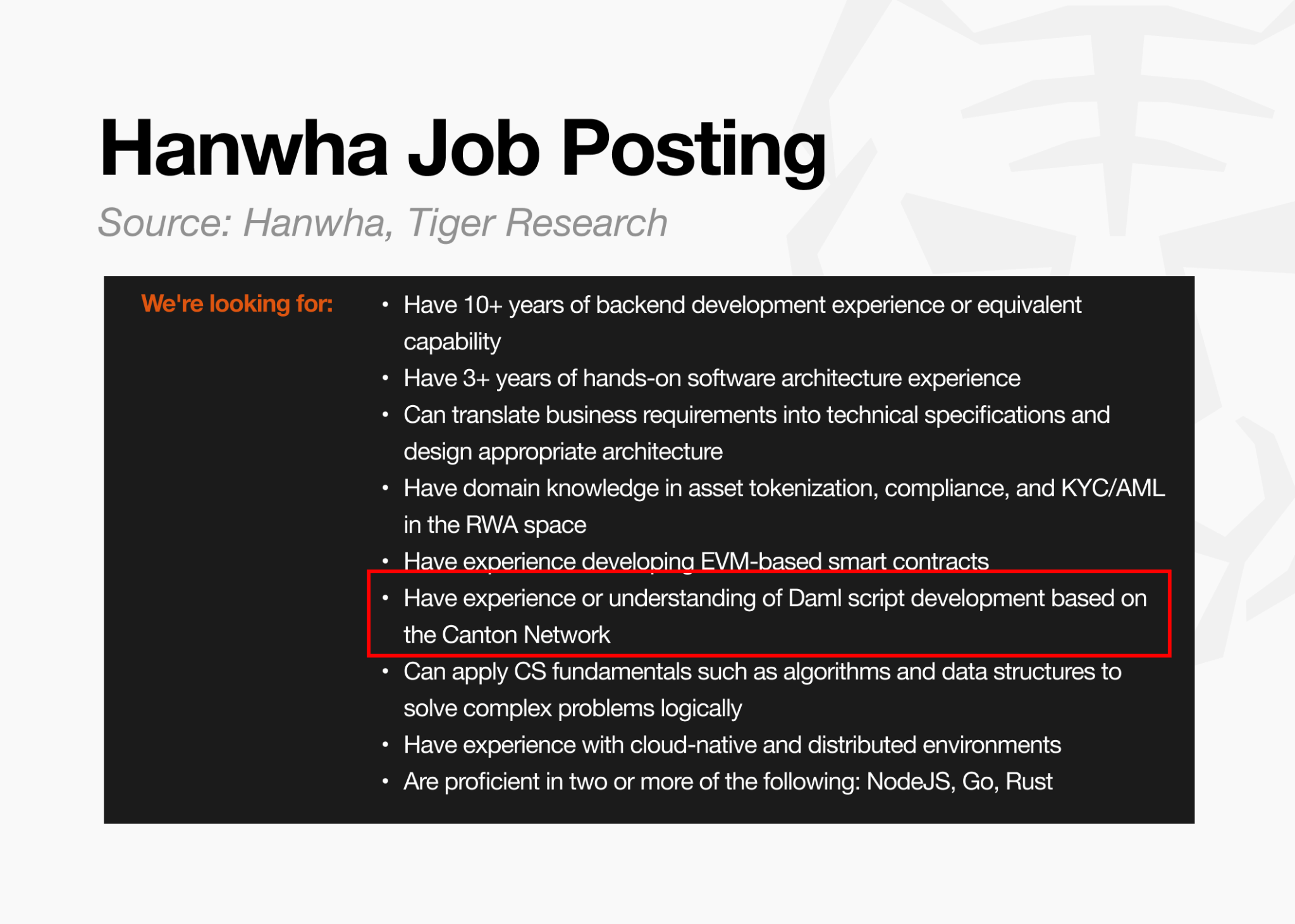

Hanwha Investment & Securities has been among the most active on Canton. In its February 2026 recruitment drive for its RWA division, the firm’s job postings listed “experience with or understanding of Daml script development on Canton Network” as a preferred qualification for Web3 back-end roles, a signal that suggests growing internal capability development around Canton-related infrastructure.

Momentum accelerated further in June 2026. Shinhan Asset Management and Shinhan Securities had each signed separate memoranda of understanding with the Canton Foundation. Both entities will participate directly in Canton Network governance and work jointly to connect Korean financial products with overseas investors.

KB Securities joined shortly after, agreeing to a joint review with the Canton Foundation and blockchain infrastructure firm Wavebridge on how to apply distributed ledger infrastructure to domestic capital markets transactions. The stated objective is to issue and distribute products backed by domestic financial assets in global markets.

Parallel developments are visible across the rest of Asia. In Japan, JSCC, Nomura Holdings, and Mizuho Financial Group launched a joint tokenization proof-of-concept in April 2026 focused on using Japanese government bonds (JGBs) as collateral on Canton. In Hong Kong, HKFMI has integrated Canton technology into the Central Moneymarkets Unit (CMU) for government bond settlement. HKFMI operates as the settlement institution under the Hong Kong Monetary Authority, making this one of the first cases of Canton adoption at the level of a monetary authority. In Singapore, Hydra X has completed live validation by launching a structured product SVT on Canton within the MAS regulatory framework.

The regulatory scaffolding is taking shape, and institutions are already building on it.

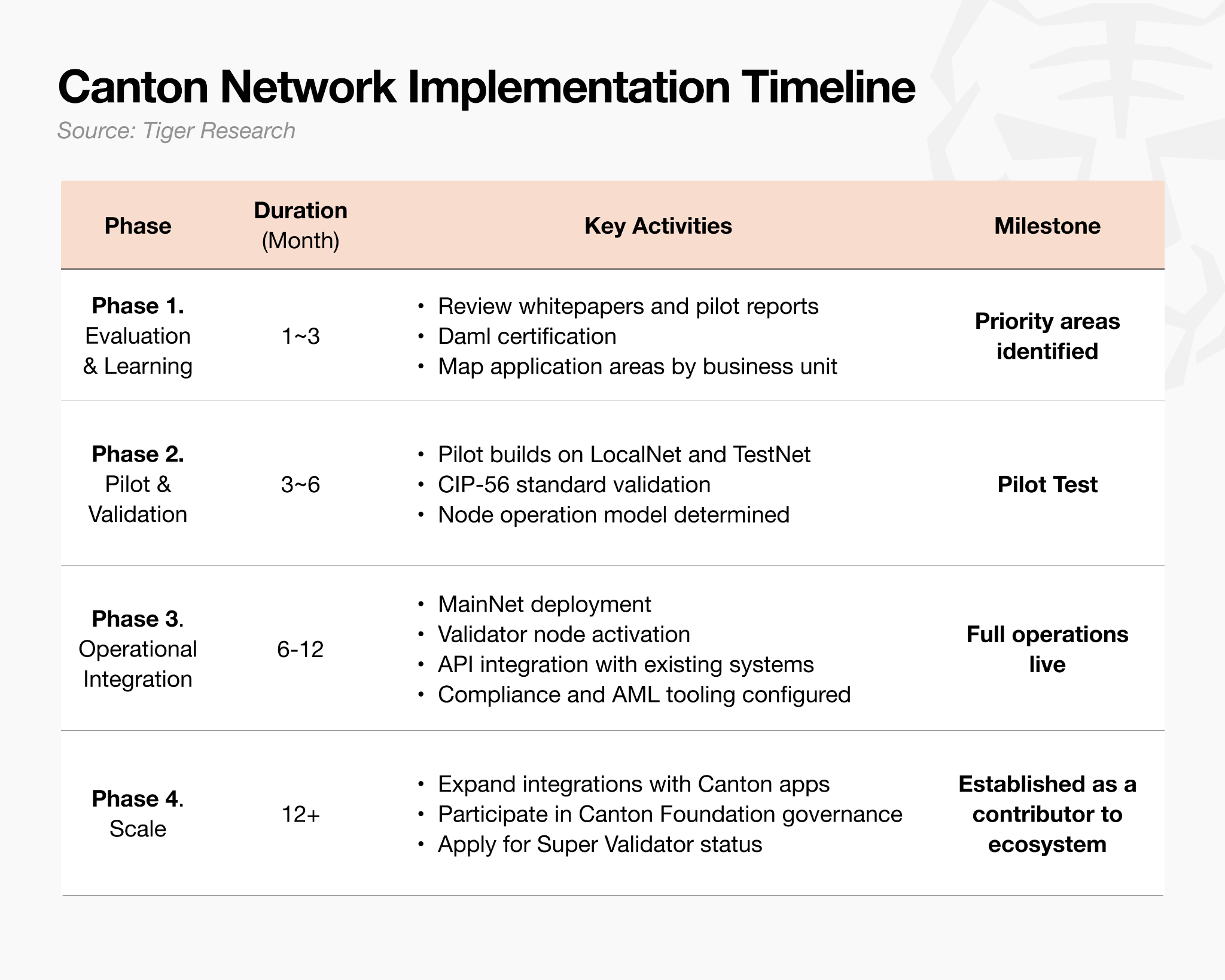

6. How to Get Started

The market is already moving. Institutions considering entry need to answer two questions: what form participation will take, and how long each stage will require. Without a defined entry mode, resources scatter across competing priorities. Without a realistic timeline, decisions get deferred.

What Form of Participation?

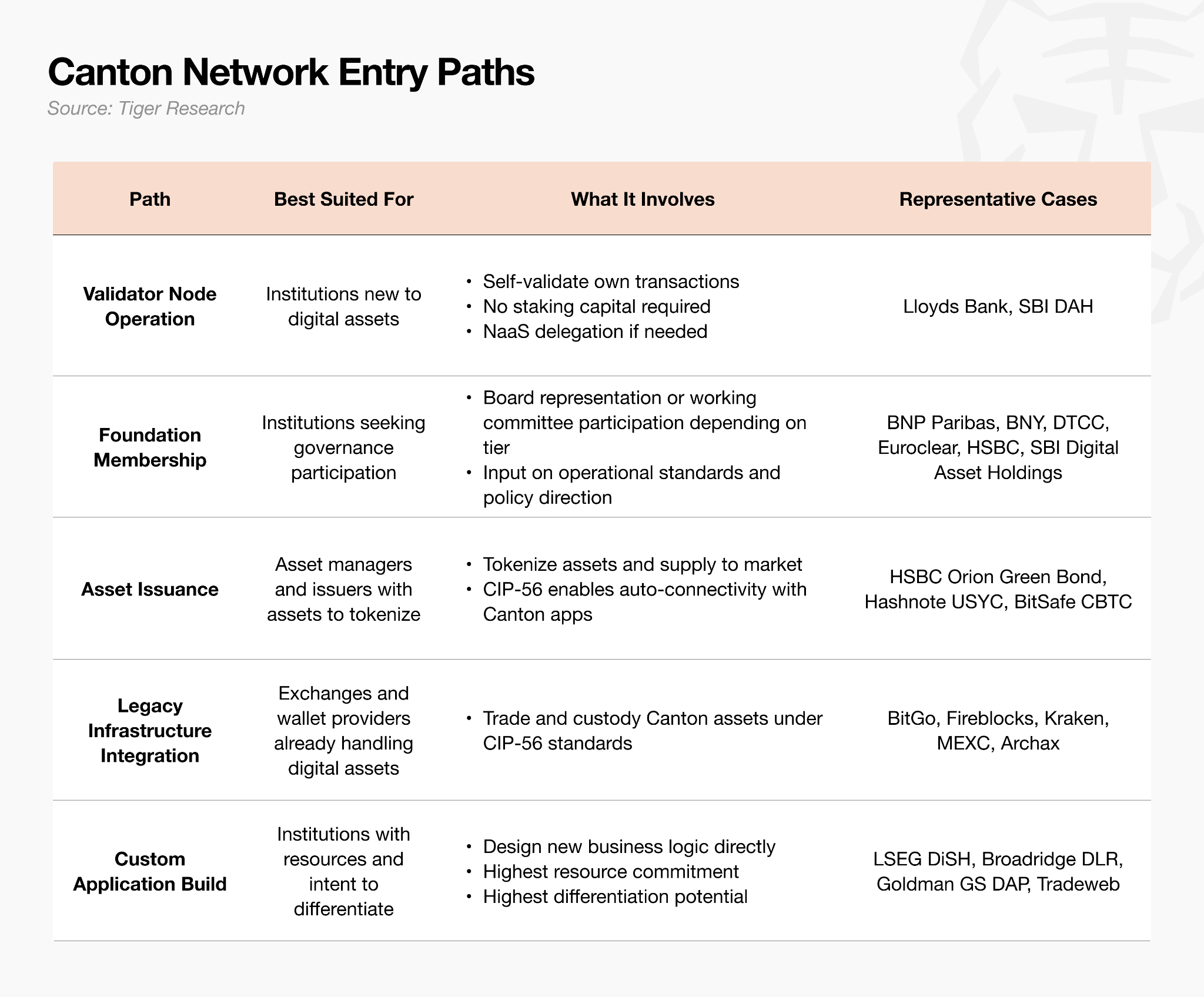

The right starting point depends on where an institution stands today. There are five broad entry paths into Canton, arranged here in ascending order of complexity.

The choice of entry path follows from an institution’s current position. Starting directly with asset issuance is not a realistic first step. The natural entry point is node operation or foundation membership, which allows an institution to gain direct experience with Canton’s ecosystem and direction before layering on asset issuance, infrastructure integration, and eventually proprietary application development. These five options are not mutually exclusive alternatives. They are better understood as a cumulative architecture, where an institution begins where it can and builds toward a more complete presence over time.

How Long Does Each Stage Take?

The trajectory observed among overseas institutions, from initial review to operational stability, follows a broadly consistent pattern. Each phase takes no more than a year in most cases, and institutions that move quickly can advance to the next phase in as little as three months.

LSEG’s DiSH platform, for example, completed a POC on Canton with a consortium of Digital Asset and financial institutions before launching formally in January 2026. SBI Digital Asset Holdings, meanwhile, assumed a Super Validator role in July 2024 and secured Canton Foundation Premier membership at the same time, establishing itself as a core participant in the network.

Each phase must be completed in order, and no phase can be bypassed. The full progression typically takes about a year. Of all the phases, the first, assessment and learning, is the most important. While the stated goal of this phase is to evaluate Canton’s technical architecture and infrastructure design, the more fundamental work is internal.

An institution needs to determine which assets it intends to tokenize, which business units they sit in, and whether the internal decision-making structures are in place to act on that. Entering Phase 2 without answers to those questions tends to produce a return to Phase 1. Institutions considering a Canton entry should address these internal questions before anything else.

7. The Window Is Open

Thirty years ago, the internet reshaped capital markets infrastructure, and once that infrastructure was built, it did not change easily. The governance structures, token standards, and Super Validator rosters being established on the Canton Network today will form the backbone of the next generation of capital markets. Institutions that join while those standards are still being set will hold structural advantages that are difficult to replicate once the architecture has hardened.

The first step does not need to be large. Delegating a validator node, sending a developer through Daml certification, or committing to a one-to-three-month evaluation are all viable entry points. The world’s leading financial institutions have already established positions on the same infrastructure, and the network’s expansion into Asia is adding to the momentum.

In 1996, the institutions that moved early on internet infrastructure were not making a speculative bet. They were responding to evidence that the technology worked and that the cost of delay was rising. That same evidence exists today.

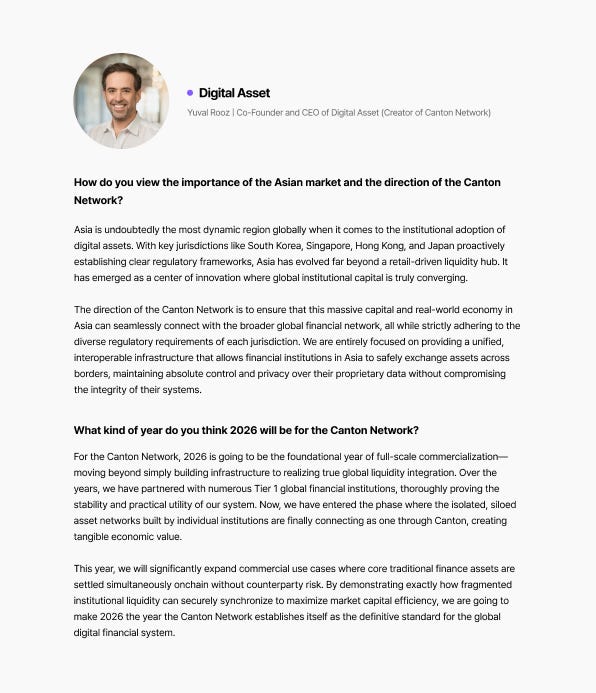

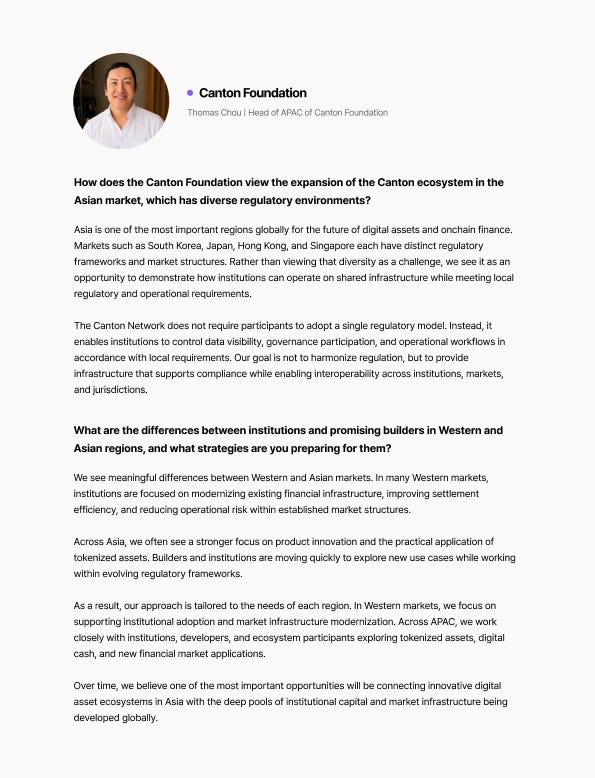

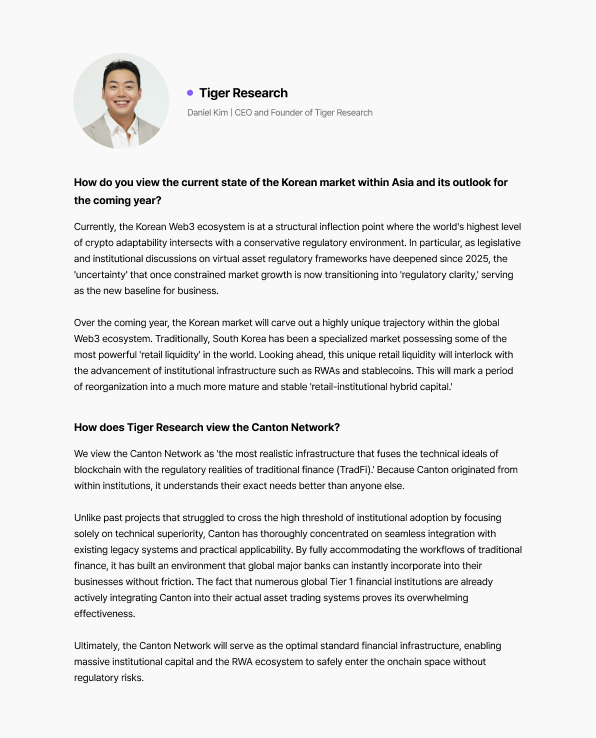

Leadership Insights

Disclaimer

This report was partially funded by Canton Network. It was independently produced by our researchers using credible sources. The findings, recommendations, and opinions are based on information available at publication time and may change without notice. We disclaim liability for any losses from using this report or its contents and do not warrant its accuracy or completeness. The information may differ from others’ views. This report is for informational purposes only and is not legal, business, investment, or tax advice. References to securities or digital assets are for illustration only, not investment advice or offers. This material is not intended for investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo following brand guideline. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action