The DeFi ecosystem already contains every core financial primitive, from swap and lending to yield and derivatives. What remains absent is the execution layer that makes these products accessible to a mainstream audience. We examine why prior attempts to eliminate wallet complexity and chain friction have fallen short, and what structural differentiation defi.app brings to that gap.

Key Takeaways

DeFi infrastructure has matured, but consumer-facing apps capable of retaining users remain absent. Traditional fintech firms like Robinhood face regulatory barriers that block entry into self-custody and high-leverage products.

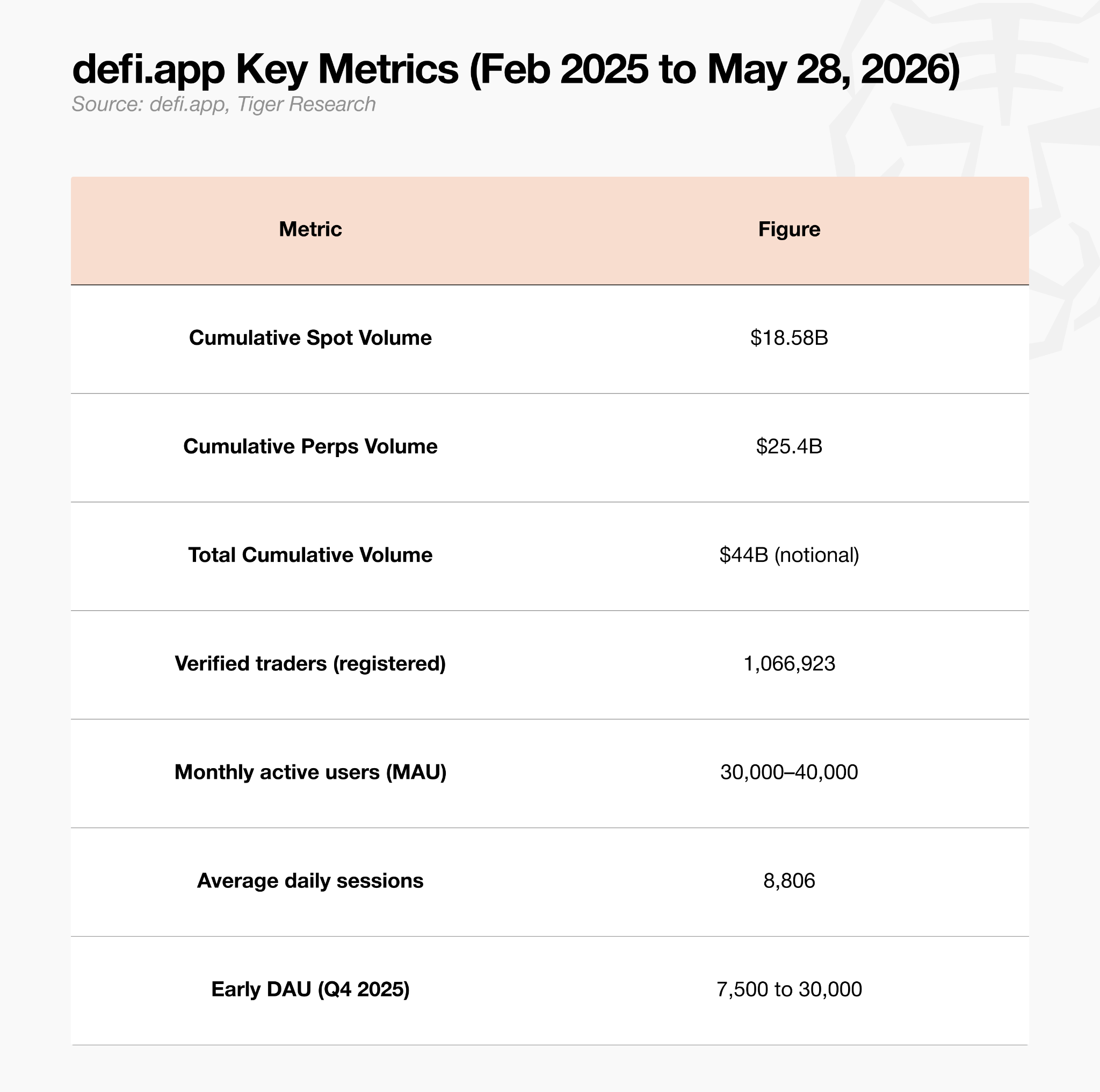

Since its February 2025 launch, defi.app has accumulated $44B in cumulative trading volume and 1.06M registered users, validating its gas-abstracted, chain-agnostic interface.

Rocket Perps charges fees significantly above standard DEX rates, but directs 80% of total platform revenue to a governance-approved $HOME buyback program under DIP-004.

For defi.app to achieve long-term growth, it must go beyond short-term user acquisition and create conditions for daily habitual engagement built on a foundation of trust.

1. Why No One Has Captured the DeFi Execution Layer

Despite a decade of DeFi development since Ethereum’s 2015 launch, mainstream adoption has stagnated. The core barrier is not product quality but user experience friction.

A 2023 Consensys/YouGov survey found 93% of global respondents had heard of crypto, yet only 8% described themselves as familiar with Web3 or DeFi. Conditions have not materially improved since.

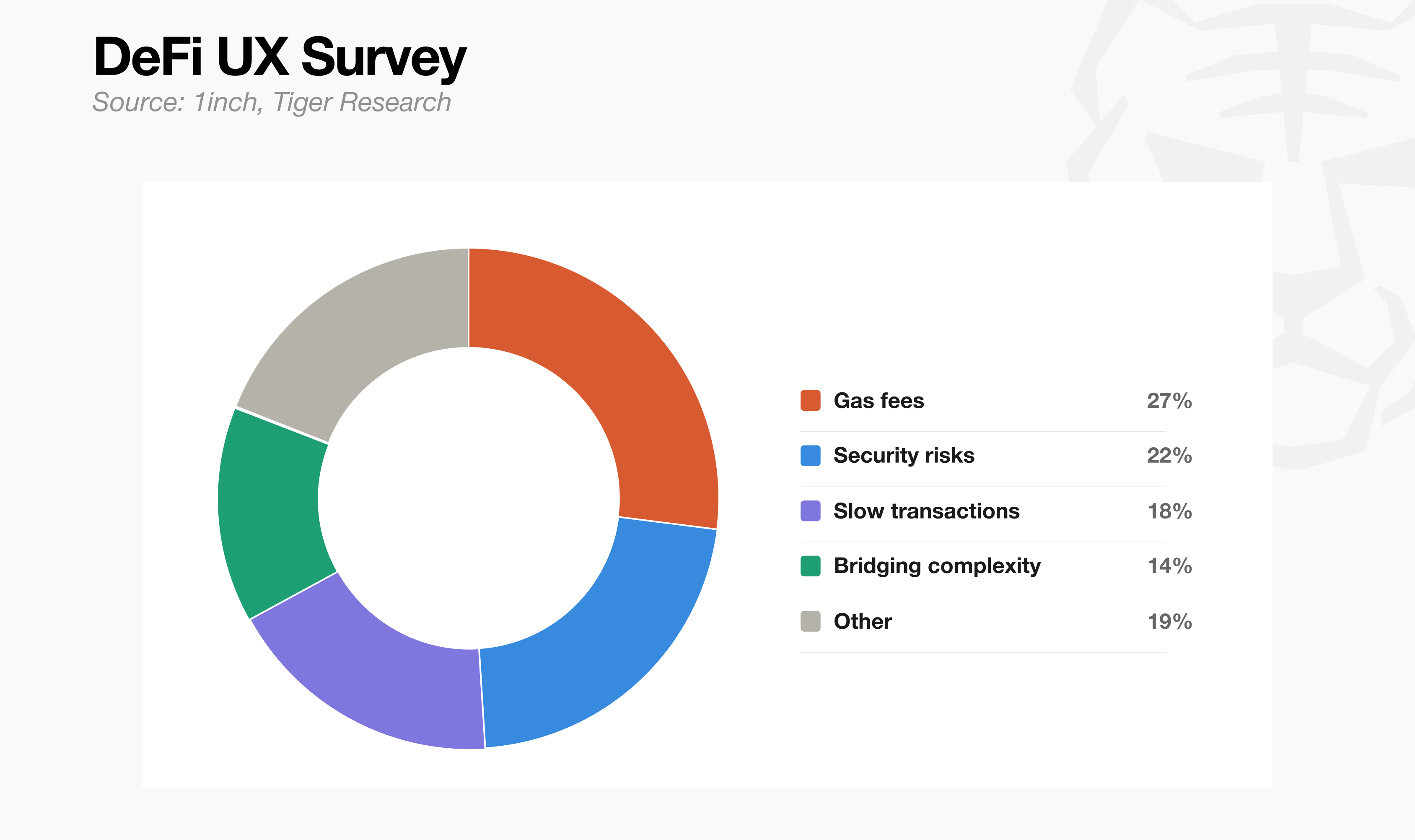

A 2025 1inch survey identified the top DeFi pain points as gas fees (27%), security risks (22%), slow transactions (18%), and bridging complexity (14%). These are UX frictions, not product failures.

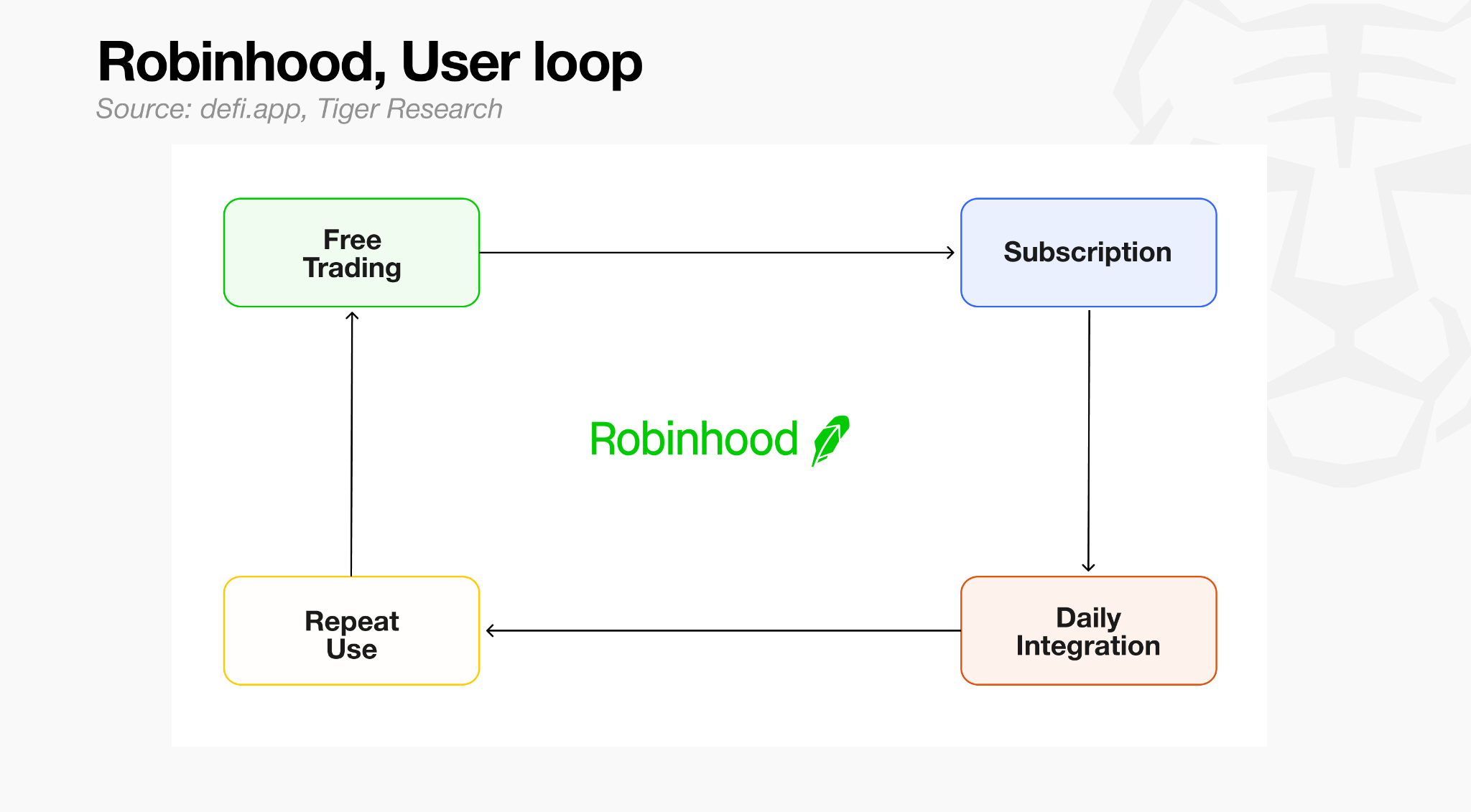

Robinhood succeeded in traditional finance by making stock trading free and accessible from a single smartphone, at a time when brokerage fees and complex account-opening procedures were the norm. Its success came from simplifying a low-barrier investment experience that anyone could try.

DeFi’s native demand is structurally different, covering high-leverage derivatives, onchain yields, and self-custody. These are areas regulated fintech cannot legally offer. Robinhood has begun handling some crypto spot assets, but self-custody and permissionless high-leverage products remain firmly outside its regulatory perimeter.

The DeFi execution layer’s goal is not to replicate Robinhood’s business, but to deliver Robinhood-level UX on the territory Robinhood cannot enter.

2. Why Prior Attempts Failed

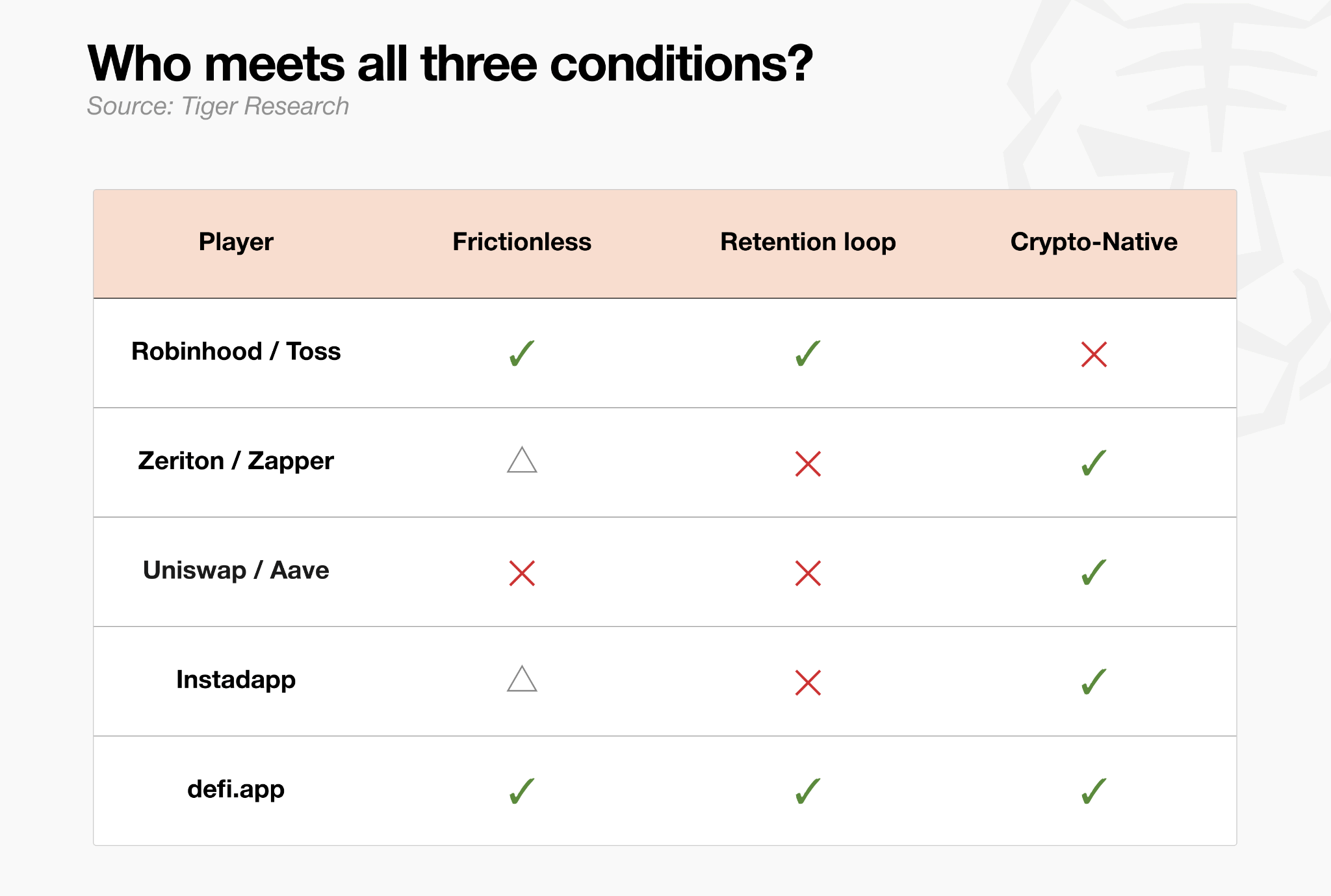

Zerion, Zapper, and Instadapp (Avocado) all attempted to reduce DeFi entry friction through aggregated dashboards and smart account (Account Abstraction) technology. Direction was correct; retention was not.

The structural failure was the absence of a durable retention loop. When token or point incentives ended, users migrated to the next reward cycle. These platforms cleared the technical hurdle but could not retain users without incentives, falling short of the fintech D30 retention benchmark of 9.2%.

Reducing friction and building daily return habits are separate design problems. Robinhood retained users not simply because trading was free, but because notifications, spending analytics, and daily rewards created autonomous re-engagement loops. Existing DeFi apps lacked the product design capability to build those loops without incentives.

Reviewing prior failure patterns, three conditions must be satisfied simultaneously for a platform to capture this market.

Frictionless access, meaning users experience no chain separation, gas fees, or bridge complexity.

Retention loop: a mechanism that keeps users returning after token incentives expire.

Crypto-native coverage: full coverage of self-custody and high-leverage products that regulated fintech cannot offer.

The platform that integrates all three becomes the market standard.

3. defi.app’s Approach: What the Numbers Show

defi.app consolidates Swap, Earn, and Perps into a single interface. EIP-4337 smart account-based gas abstraction eliminates the need for users to manage gas separately. Trades across EVM and Solana ecosystems are automatically routed via optimal paths through aggregators including 1inch and Jupiter. The design prioritizes financial product accessibility while concealing Web3 infrastructure complexity.

The following figures were recorded across the period since launch.

With 1.06M registered users, defi.app has demonstrated strong onboarding capacity. An MAU of 30,000–40,000 and DAU growth of approximately 3,000% from inception indicate that a meaningful retention base was already in place ahead of the Rocket Perps public launch. The key question now is how far the June 4 launch can extend that base.

4. Rocket Perps: Linking Engagement to Revenue and Token Value

Until now, defi.app had focused on eliminating friction and building retention loops, but remained in direct comparison with traditional fintech. It consolidated many services into one place, yet stopped short of the third condition: crypto-native coverage.

Source: defi.app

Rocket Perps is defi.app’s answer to that gap.

Rocket Perps is a 1000x leverage perpetuals product integrated with a pixel-art arcade game interface. Built on Aark Digital’s oracle infrastructure, it enables instant position execution without counterparty matching. Tapping incoming asteroids accumulates XP, claimable as $HOME token rewards, creating a gamified loop designed to drive repeat engagement.

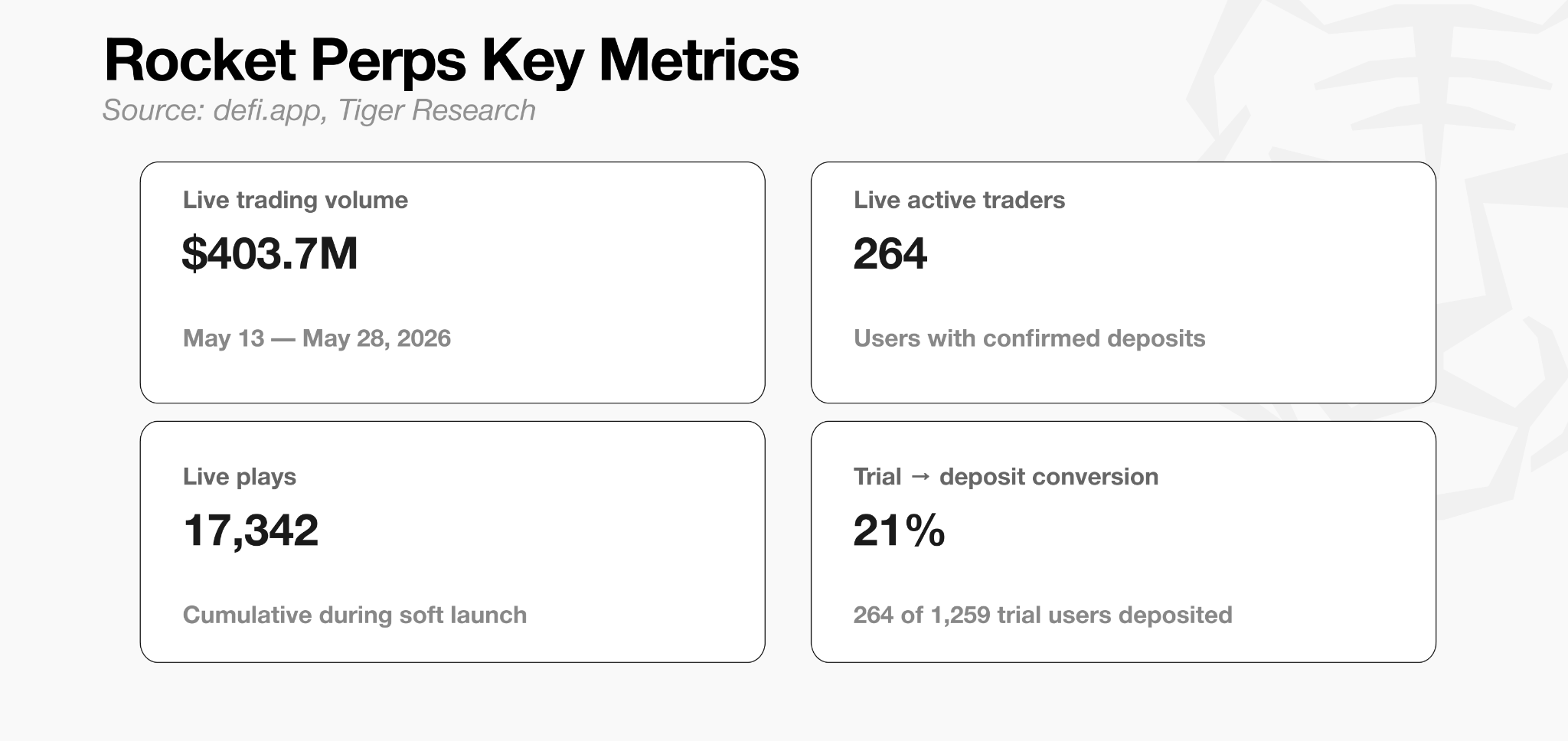

The following figures were recorded during the soft launch period (May 13 to May 28, 2026).

264 users generating over $400M in volume over two weeks reflects the capital efficiency and intensity characteristic of high-leverage products. These are early-adopter, high-risk-tolerance traders. Public scalability requires separate validation.

1000x leverage may appear excessive at first glance, but it maps directly onto the psychology of crypto market participants. Many crypto traders willingly accept high risk in pursuit of outsized returns. Rocket Perps translates that appetite into a product occupying the territory regulated fintech cannot enter.

The fee structure warrants attention. Entry carries a 4% margin fee, and profitable exits are subject to a tiered fee of up to 50% of gains. This is significantly higher than standard perpetuals DEXs, which typically charge between 0.02% and 0.07%. Total platform revenue across spot, perpetuals, and the Rocket Perps arcade is directed 80% to the $HOME buyback program under DIP-004, making the fee structure a deliberate design choice aligned with the platform’s ecosystem goals. As a high-conviction trading product rather than a hedging instrument, the premium fee model is likely to be received as reasonable by its target users.

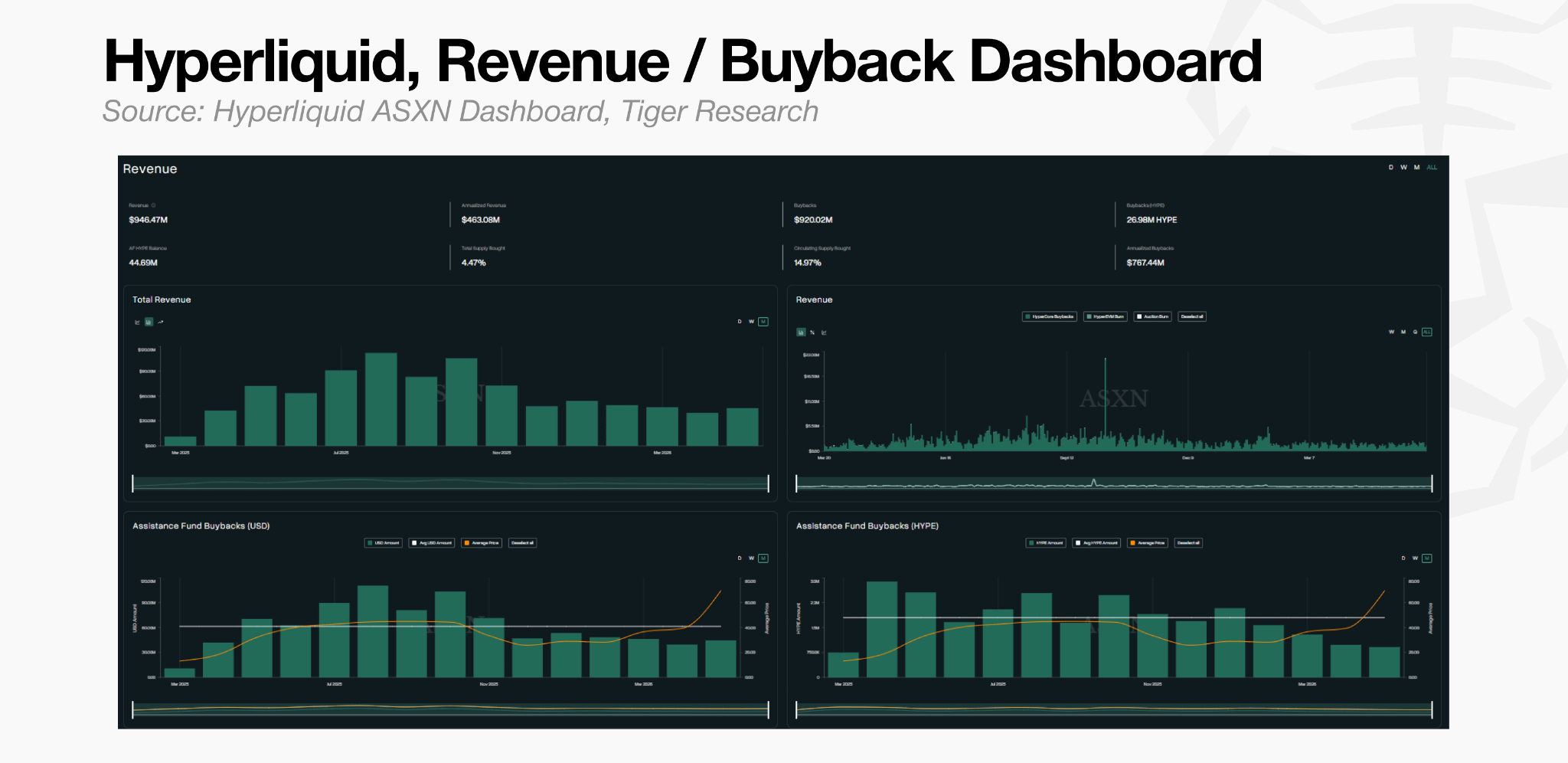

Hyperliquid offers the clearest precedent for this kind of fee-to-buyback flywheel. The protocol directs 97% of all fees toward HYPE token buybacks, with every transaction immediately and publicly verifiable onchain. If defi.app can demonstrate the same virtuous cycle onchain, the cost premium for users becomes offset by a powerful incentive to stay.

5. Milestones defi.app Must Clear

5.1. Retention Validation and Trust Framing

The 264 soft launch traders were self-selected high-risk participants. The June 4 public launch of Rocket Perps marks the first real test of general user retention, and the question is whether the existing MAU base of 30,000–40,000 can be meaningfully scaled from that point.

Robinhood faced this challenge first. When the meme stock cycle ended in 2021, MAU dropped sharply from its peak. The response was to add credit cards, banking, and social features, giving users reasons to open the app independent of trading activity. It demonstrated that a separate daily loop is required to retain users regardless of portfolio performance.

defi.app faces the same design challenge. Continuously launching features that align with the instincts of crypto-native traders will attract users, but sustaining them requires building the perception that the platform is a reliable place to put assets to work. Both must happen in parallel. Only when retained users find reasons to engage with defi.app as part of their daily routine does the platform become a true everything app.

5.2. Onchain Transparency for Buyback Execution

For investors evaluating $HOME today, the most compelling thesis is the commitment to direct 80% of total platform revenue to a governance-approved buyback program. But crypto investors have been burned by this type of promise before, and scrutiny is high. Even a small gap between stated commitments and onchain evidence can erode market trust faster than expected.

Hyperliquid resolved this most cleanly. Buybacks execute automatically the moment fees are generated, and every transaction is publicly queryable onchain. No announcement is needed because the data speaks for itself.

defi.app’s 80% commitment is compelling on its face. If the platform publishes the buyback execution wallet address and launches a real-time revenue dashboard simultaneously with the Rocket Perps public launch, it has the foundation to build the same trust-driven flywheel Hyperliquid demonstrated.

6. Conclusion

Robinhood transformed the financial experience but operates within regulatory boundaries. Self-custody, high leverage, and permissionless yield remain inaccessible. DeFi built finance beyond those boundaries but could not retain users. The infrastructure exists; the daily return loop does not.

defi.app’s objective sits precisely in that gap: building the experience DeFi has not yet created, on territory Robinhood cannot enter.

The approach operates across three axes. 1) Eliminate friction through gas and bridge abstraction. 2) Add features like Rocket Perps that give users reasons to return repeatedly. 3) Route fees into a governance-approved $HOME buyback program tied to real platform usage.

defi.app is a team that understands what draws users into the crypto market. For users who embrace the volatility native to crypto, Rocket Perps offers a compelling entry point and a reason to come back. Beyond short-term acquisition, the deeper question is whether the platform can build the conditions for daily habitual use: users generating yield through Earn, accumulating XP through gameplay, and returning not because of incentives but because the app has become part of how they manage their assets.

When that condition is met, defi.app becomes not merely another DeFi app, but the first market standard in a space Robinhood cannot enter.

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report was partially funded by defi.app. It was independently produced by our researchers using credible sources. The findings, recommendations, and opinions are based on information available at publication time and may change without notice. We disclaim liability for any losses from using this report or its contents and do not warrant its accuracy or completeness. The information may differ from others’ views. This report is for informational purposes only and is not legal, business, investment, or tax advice. References to securities or digital assets are for illustration only, not investment advice or offers. This material is not intended for investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo following brand guideline. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action