Circle has released its Q1 2026 earnings report. Reserve interest income from USDC still accounts for over 90% of revenue. To move beyond this concentration, Circle is developing initiatives including the Ark Network. What does the next phase look like?

Summary

With Q1 2026 results as the inflection point, Circle is accelerating its paradigm shift from a simple stablecoin issuer to an integrated infrastructure operator for the digital asset industry. Its forward business strategy rests on three core pillars.

Maximize USDC margin and circulation: Reserve interest income accrues on both external and proprietary platforms. Higher USDC use on Circle’s own channel (CPN) drove RLDC margin to a record 41.4% this quarter. To expand issuance, Circle has partnered with the DEX Hyperliquid.

Launch the proprietary L1 ‘Arc’ to diversify gas and fee revenue: 94% of Circle’s revenue currently comes from USDC reserve interest. Once Arc expands Circle’s platform and generates platform fee revenue, the over-reliance on reserve interest can be structurally resolved.

Capture AI payments via Agent Stack: Circle is staking out the standard for autonomous micro-payments between AI agents. Full commercialization is targeted for 2028, aligned with infrastructure rollout and GENIUS Act effectiveness.

In sum, Circle is putting aggressive USDC issuance expansion through anchor platforms like Hyperliquid at the front, while vertically integrating its financial stack across its own L1 (Arc), payments network (CPN), and AI nano-payments (Agent Stack). The key point is that USDC circulation growth and diversified infrastructure now pull each other forward.

Through this, Circle is expanding from a simple interest-revenue business into a platform business driven by traffic and transaction fees.

Q1 2026 Recap. Margins on the Mend

1. Top-line growth and margin gains. On-platform mix strengthens earnings quality

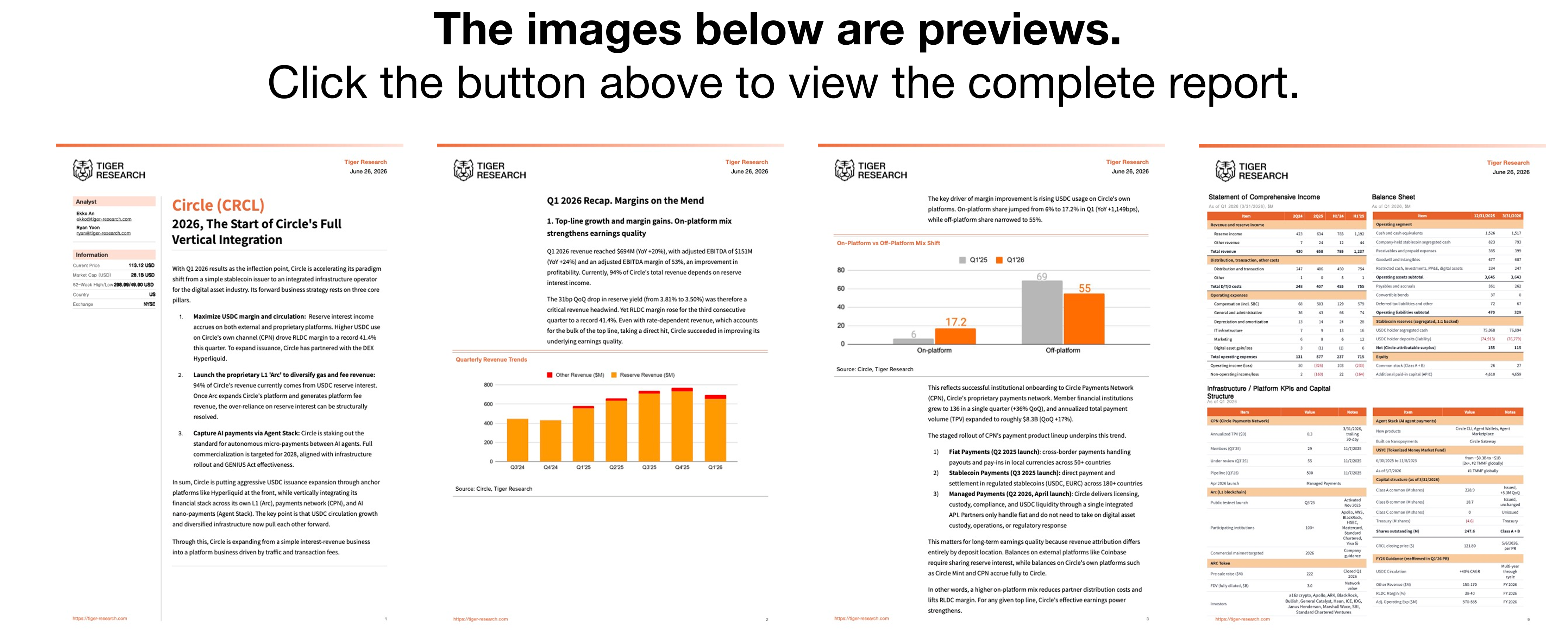

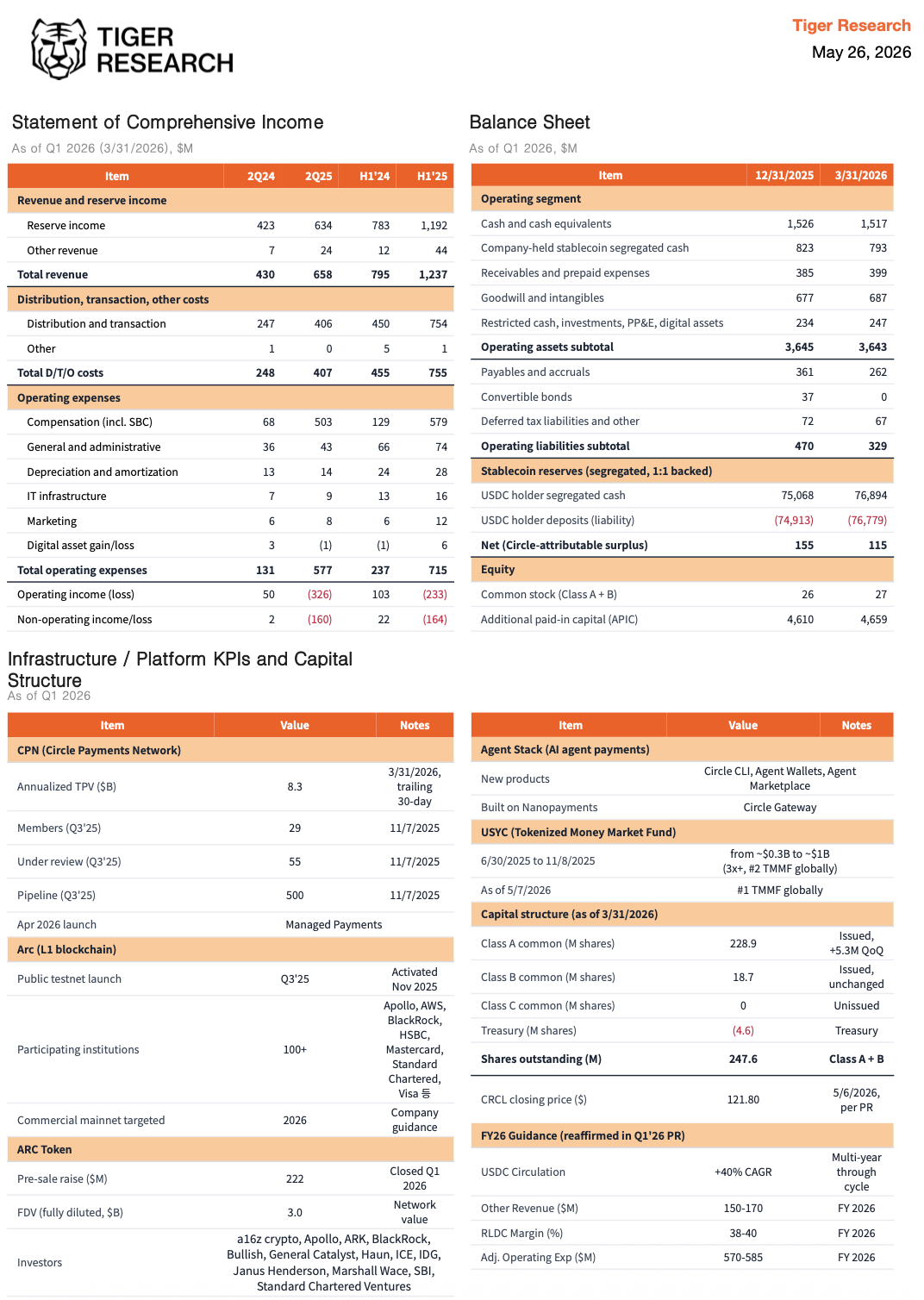

Q1 2026 revenue reached $694M (YoY +20%), with adjusted EBITDA of $151M (YoY +24%) and an adjusted EBITDA margin of 53%, an improvement in profitability. Currently, 94% of Circle’s total revenue depends on reserve interest income.

The 31bp QoQ drop in reserve yield (from 3.81% to 3.50%) was therefore a critical revenue headwind. Yet RLDC margin rose for the third consecutive quarter to a record 41.4%. Even with rate-dependent revenue, which accounts for the bulk of the top line, taking a direct hit, Circle succeeded in improving its underlying earnings quality.

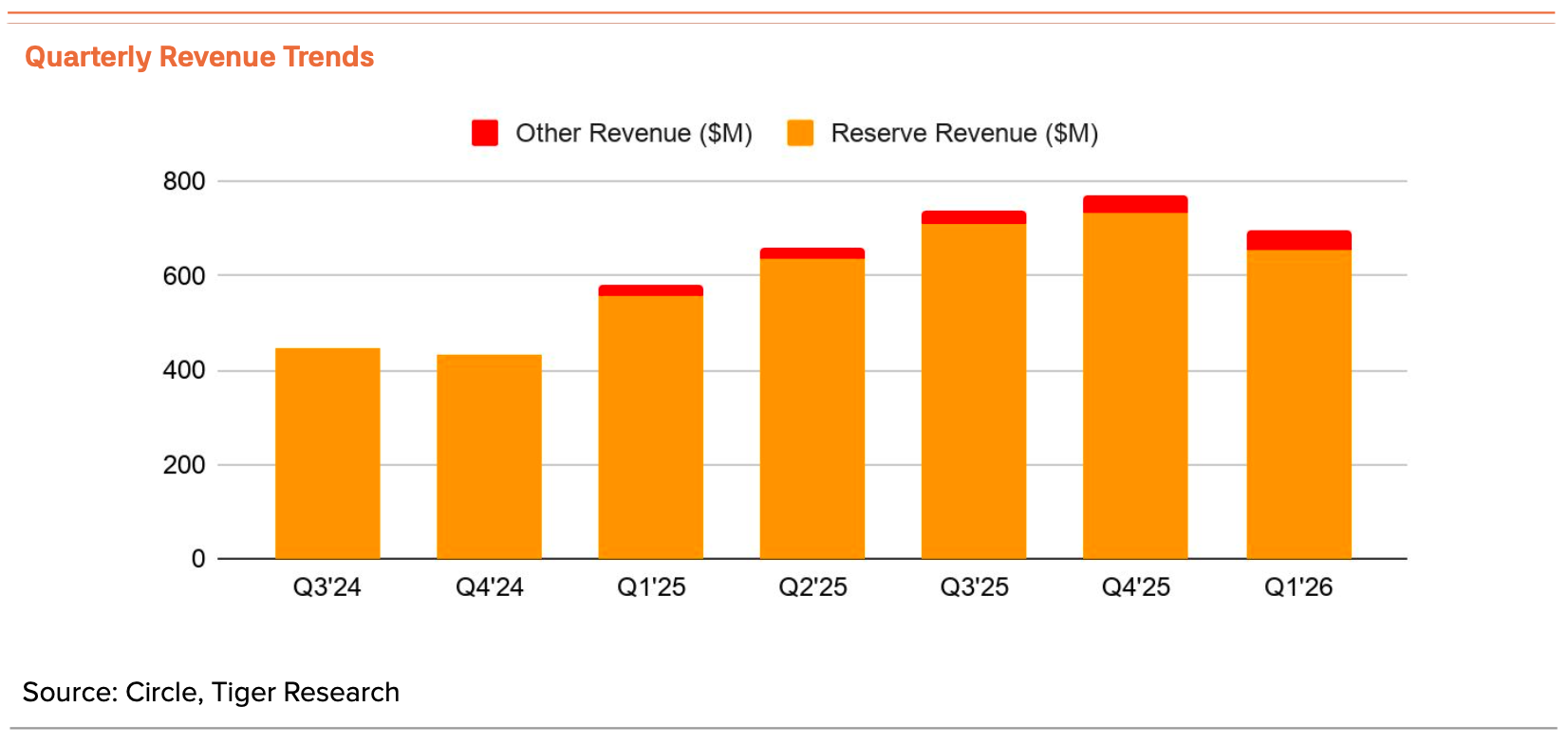

The key driver of margin improvement is rising USDC usage on Circle’s own platforms. On-platform share jumped from 6% to 17.2% in Q1 (YoY +1,149bps), while off-platform share narrowed to 55%.

This reflects successful institutional onboarding to Circle Payments Network (CPN), Circle’s proprietary payments network. Member financial institutions grew to 136 in a single quarter (+36% QoQ), and annualized total payment volume (TPV) expanded to roughly $8.3B (QoQ +17%).

The staged rollout of CPN’s payment product lineup underpins this trend.

Fiat Payments (Q2 2025 launch): cross-border payments handling payouts and pay-ins in local currencies across 50+ countries

Stablecoin Payments (Q3 2025 launch): direct payment and settlement in regulated stablecoins (USDC, EURC) across 180+ countries

Managed Payments (Q2 2026, April launch): Circle delivers licensing, custody, compliance, and USDC liquidity through a single integrated API. Partners only handle fiat and do not need to take on digital asset custody, operations, or regulatory response

This matters for long-term earnings quality because revenue attribution differs entirely by deposit location. Balances on external platforms like Coinbase require sharing reserve interest, while balances on Circle’s own platforms such as Circle Mint and CPN accrue fully to Circle.

In other words, a higher on-platform mix reduces partner distribution costs and lifts RLDC margin. For any given top line, Circle’s effective earnings power strengthens.

That said, CPN’s own usage-fee revenue has not yet ramped. As CFO Jeremy Fox-Geen noted on the prior earnings call, the current phase prioritizes network growth over monetization. CPN today functions less as a direct fee channel and more as a conduit pulling funds into Circle’s own platform. As a stepping-stone defending against external distribution costs, the Q1 results show that this strategy is working.

2. Net income decline hidden behind the growth

However, unlike the top-line growth and margin gains, the bottom line shows a clear divergence that warrants attention. Q1 net income came in at approximately $55M, down 15% YoY.

Drivers are post-IPO stock-based compensation flowing through and a sharp rise in pre-launch Arc infrastructure and R&D spend. Adjusted figures, stripped of one-time and non-cash items, remain strong. Net income trajectory still warrants attention.

Circle Moves Into Full Vertical Integration

1. USDC. Strengthen the core, expand issuance

Reserve income in Q1 2026 was $653M, accounting for 94% of total revenue. With Circle’s core business so concentrated in reserve income, top-line growth requires USDC issuance expansion.

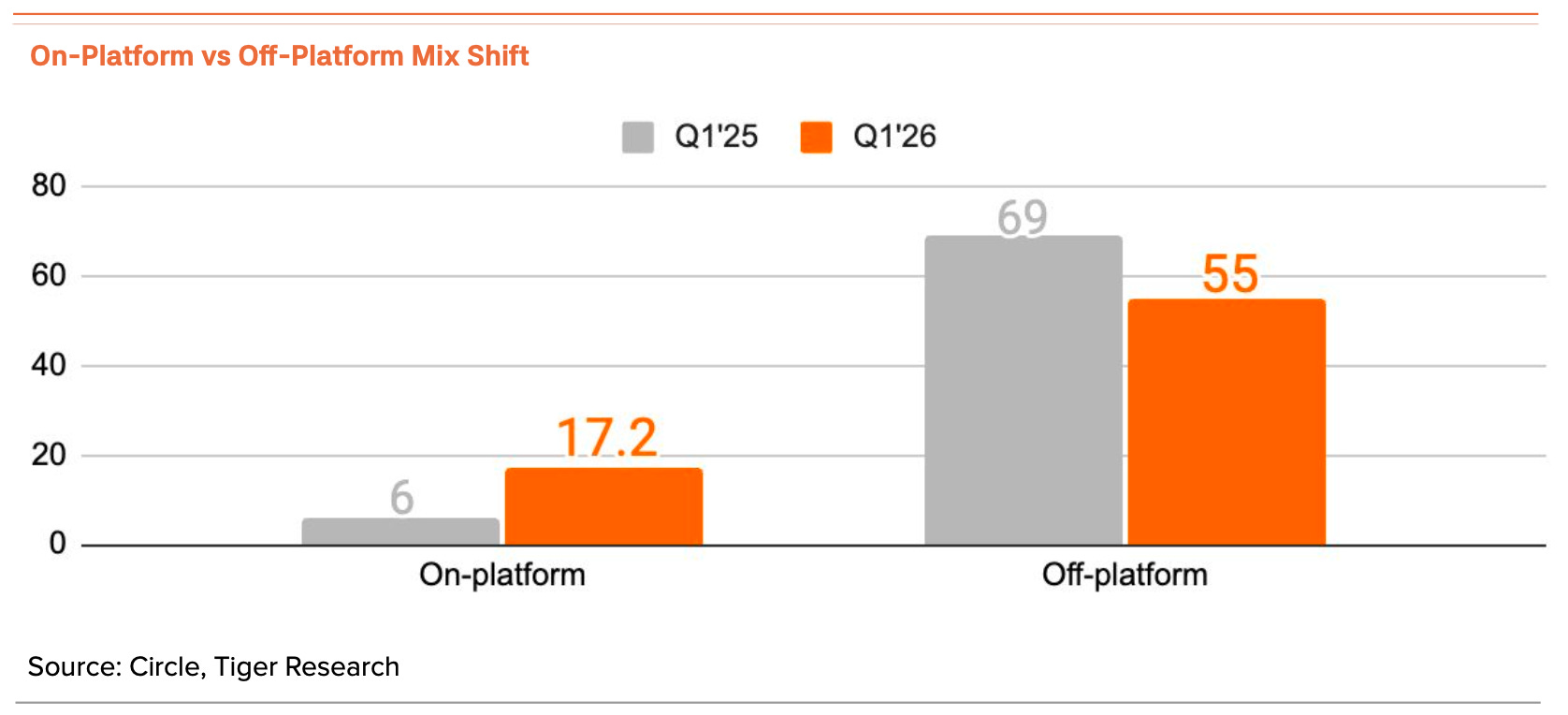

USDC circulation currently sits around $77B. The core question for Circle’s structural growth is how far this circulation ceiling can be pushed. USDT’s earlier surge was anchored in Binance trading-pair preemption.

Circle plans to extend this preemption playbook to the DEX Hyperliquid. Coinbase’s recent acquisition of Hyperliquid’s native stablecoin USDH is a representative case. Rather than deploying USDH as the platform’s native pair, Hyperliquid sold it and registered USDC as the official pair.

Hyperliquid’s deposit growth flows directly into USDC issuance. Hyperliquid TVL doubled from $2B in Q1 2025 to $4B in Q1 2026, and peaked at $6B. Because Hyperliquid uses USDC as its base deposit asset, platform growth translates directly into new USDC issuance. The forward circulation scenario built on this is as follows.

Under this scenario, growth from Hyperliquid alone could lift total USDC circulation from $77B today to $84B in three years. A single platform would account for more than 10% of total circulation, becoming a massive issuance channel.

Conceding 90% of reserve interest income to the platform does leave Circle with reduced near-term profitability. But as the cost of securing irreplaceable volume of roughly KRW 15T (~$11B) in daily turnover and a 17% share of the DEX derivatives market, this is close to an acceptable trade-off.

If Hyperliquid-based derivatives products follow, the virtuous-cycle structure strengthens further. For a Circle that prioritizes circulation expansion over near-term margin, Hyperliquid is a strategic stronghold worth preempting even by splitting margin.

2. Arc. How Circle Exits Rate Dependency

As noted above, Circle’s revenue is heavily concentrated in reserve interest income, leaving the business structurally exposed to a rate-cutting environment. Arc is still in the testnet phase and generates no visible revenue yet. With its recent ~$222M institutional funding round, Arc has emerged as the core infrastructure designed to sever this rate dependency at the root.

Arc’s primary target is the global cross-border payments market. According to the World Bank report (RPW Issue 54), the global average remittance cost is 6.36% and the bank remittance cost reaches 14.99%. The drivers of this high-cost structure include SWIFT’s multi-tier intermediation, opaque FX spreads, and weekend settlement delays.

In addressing the inefficiencies of legacy financial rails, Circle aims to generate platform business revenue on top of Arc. The infrastructure fee revenue that lowers rate dependency is built on two core pillars.

Circle Payments Network (CPN): onboards global institutions and corporates to Arc for cross-border payments and settlement, capturing processing fees on traffic. Q1 institutional inflow seeds full Arc mainnet transaction revenue.

On-chain FX engine (StableFX): supports on-chain stablecoin conversion, replacing the high intermediation spreads of traditional FX. On execution, smart contracts collect predefined fees from each trading currency.

StableFX runs on an RFQ model, not SWIFT’s fixed-cost structure. Market makers competitively bid in real time and quote the tightest wholesale spread. Large transfers settle 24/7 with no SWIFT fixed fees and no slippage.

More CPN traffic and StableFX volume on Arc means more direct infrastructure and fee revenue. The non-rate revenue structure completes.

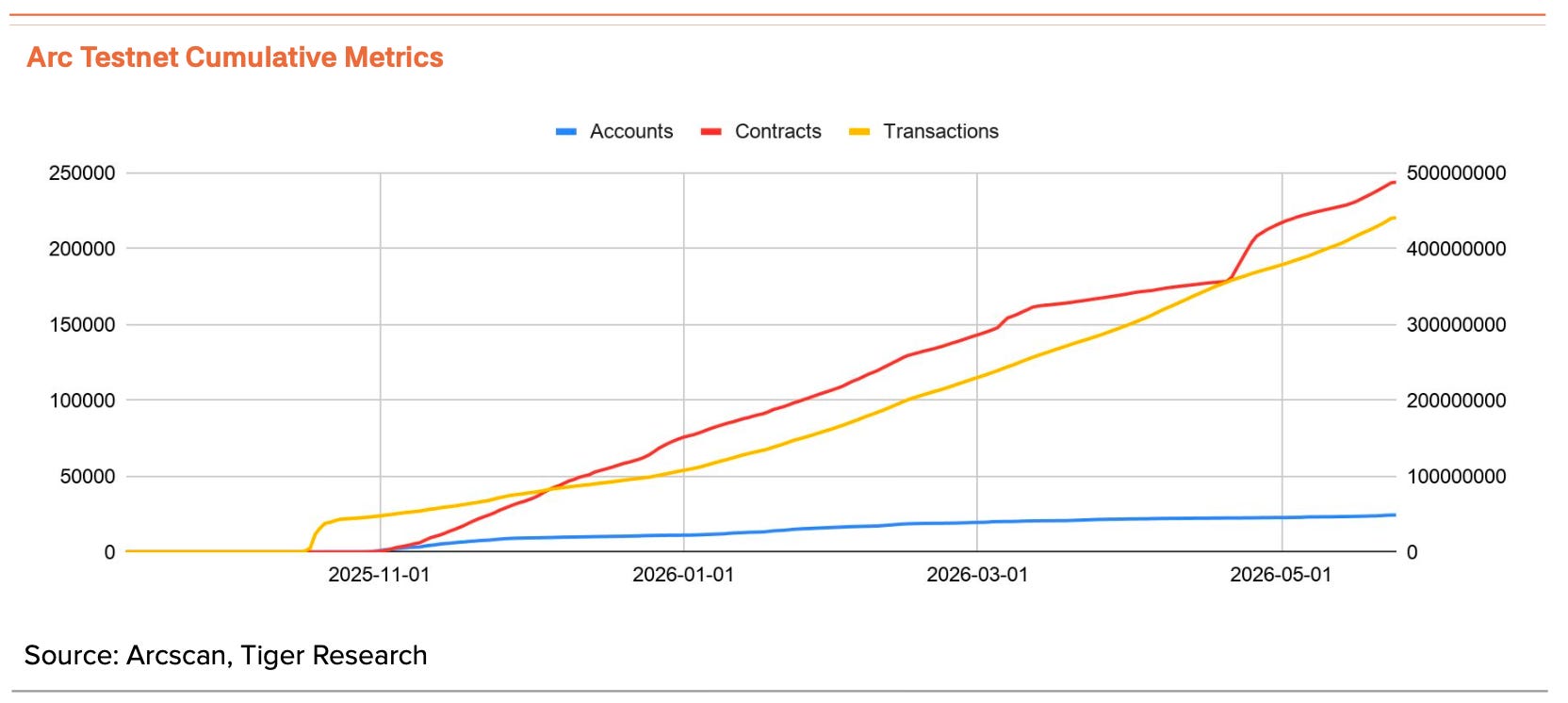

This shift is already being validated through the testnet and participating enterprises. Per Arcscan, the public testnet has logged roughly 430M cumulative transactions and 3.26M transactions in the last 24 hours since opening. Over 100 global institutions are participating, including BlackRock, HSBC, Visa, and AWS.

Beyond traditional finance, Polymarket, a blockchain-based prediction market, has also joined the ecosystem.

This goes beyond piloting features and platforms. Arc is pulling in real enterprises and driving real transaction traffic. If Arc operates as intended, Circle can expand from a USDC reserve-interest revenue structure to infrastructure operating revenue. Arc is the first step in unwinding a revenue structure tied to interest rates.

According to the roadmap, Arc mainnet launch is set for this summer. Meaningful Arc revenue is expected to come after mainnet launch.

3. Agent Stack: Blueprint for autonomous AI payments

An ‘agentic economy’, in which AI agents make decisions and transact on behalf of users rather than humans, is approaching. Global big tech firms including Google and OpenAI have already begun actively rolling out such autonomous systems.

The bottleneck is payment infrastructure. The fees generated when AI agents call APIs are priced at micro levels (sub-cent units) that legacy payment systems cannot process. Routing such micro-payments through credit card networks produces a fee structure where the cost outweighs the principal, so every transaction generates a net loss. Agent payments cannot structurally fit existing card rails.

Circle targeted this gap and launched the ‘Circle Agent Stack’, which uses USDC as the settlement asset and provides the tooling to build the surrounding environment.

Agent Wallets: AI autonomously holds and sends USDC within human-set rules (e.g., spend limits)

Agent Marketplace: storefront where AIs source API services and settle per call

Agent Nanopayments: instant USDC settlement down to ~$0.000001 with no gas

Circle CLI: command-line tool for wallet creation and agent connections

Circle Skills: modules letting AI agents operate Circle’s financial product suite directly

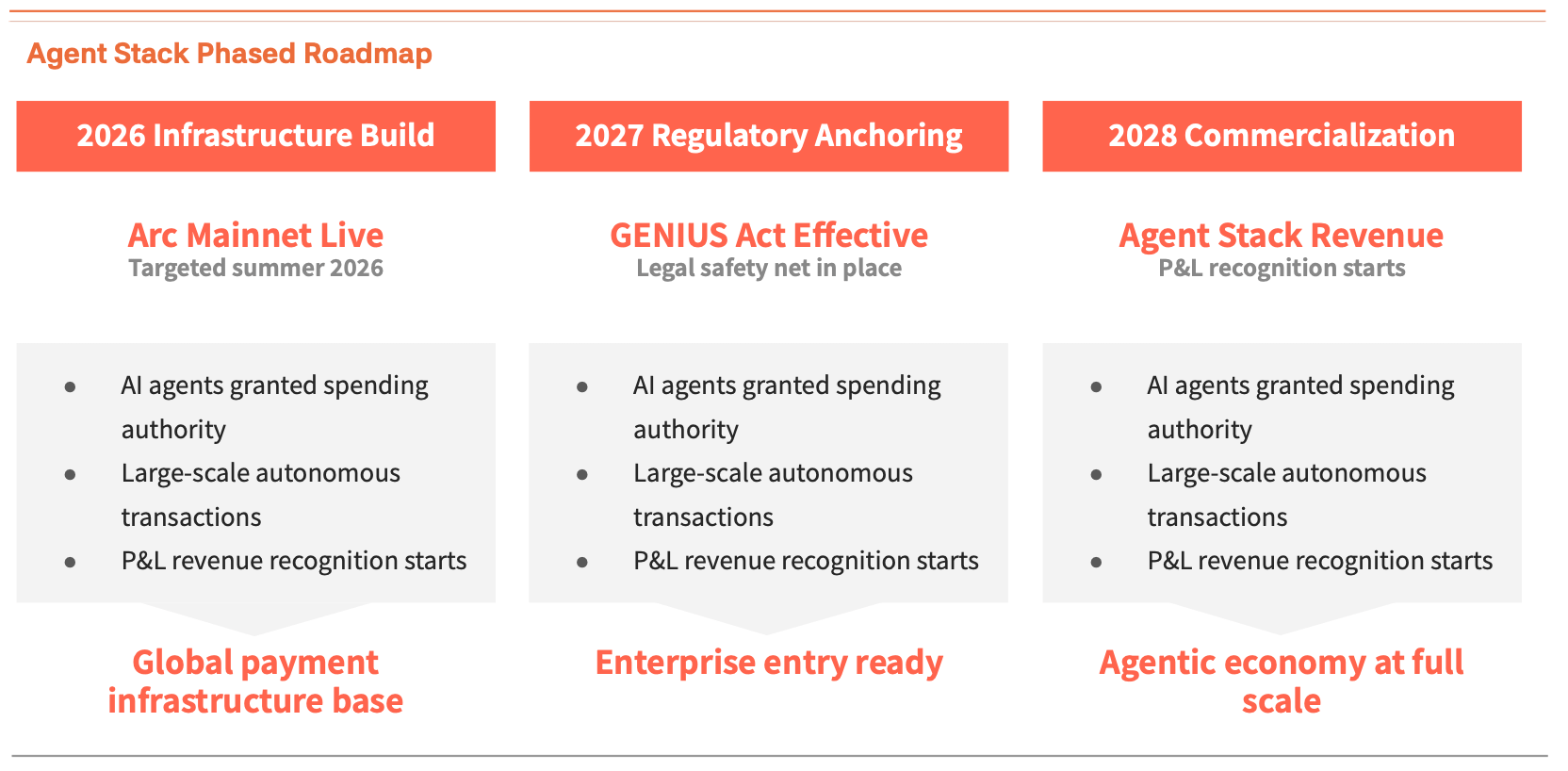

Revenue here is not yet at the visible stage either. The path to market adoption and revenue recognition is expected to progress through the phased roadmap below.

2026 (Infrastructure phase): technical foundation for stable, large-scale nano-payment processing. Arc mainnet activation this summer anchors partner integration of Circle CLI and financial modules.

2027 (Regulatory anchoring phase): GENIUS Act takes effect, completing the institutional safety net for enterprise entry. With stablecoin securities exemption and 100% safe-asset backing legally binding, even conservative corporate legal teams can adopt and test USDC payment systems internally without risk.

2028 (Commercialization and monetization): technical foundation and regulatory legitimacy fully align. The agentic economy reaches full commercialization. Enterprises grant AI agents real spending authority, large-scale transactions emerge, and Agent Stack results land in reported revenue.

As a result, until full traffic-driven revenue arrives in 2028, Agent Stack is likely to operate as an ‘expectation premium’ priced into the share price as future market preemption value, ahead of actual revenue.

Disclaimer

This report reflects the authors’ independent views, free from external pressure or undue influence. As of the publication date, it has not been shared with institutional investors or third parties in advance. Tiger Research and its authors hold no position in the covered security (CRCL) and have no material financial interest to disclose.

This report is prepared based on objective facts and information from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. Opinions are subject to change without notice.

This report is a reference document prepared solely for industry and company analysis. It does not constitute investment advice or a recommendation to buy or sell any security. All investment decisions are the sole responsibility of the investor. Tiger Research accepts no legal liability for any outcomes arising from use of this report.

This report may not be used as evidence in legal proceedings. The copyright of this report belongs to Tiger Research. Unauthorized quotation, reproduction, display, distribution, transmission, editing, translation, or publication without prior consent may result in civil or criminal liability under applicable law.