Capital in the crypto market is undergoing a paradigm shift, concentrating into specific sectors and companies. Tiger Research and RootData examined this shift in capital markets using data on 9,416 investment deals recorded from 2018 through the first half of 2026.

Key Takeaways

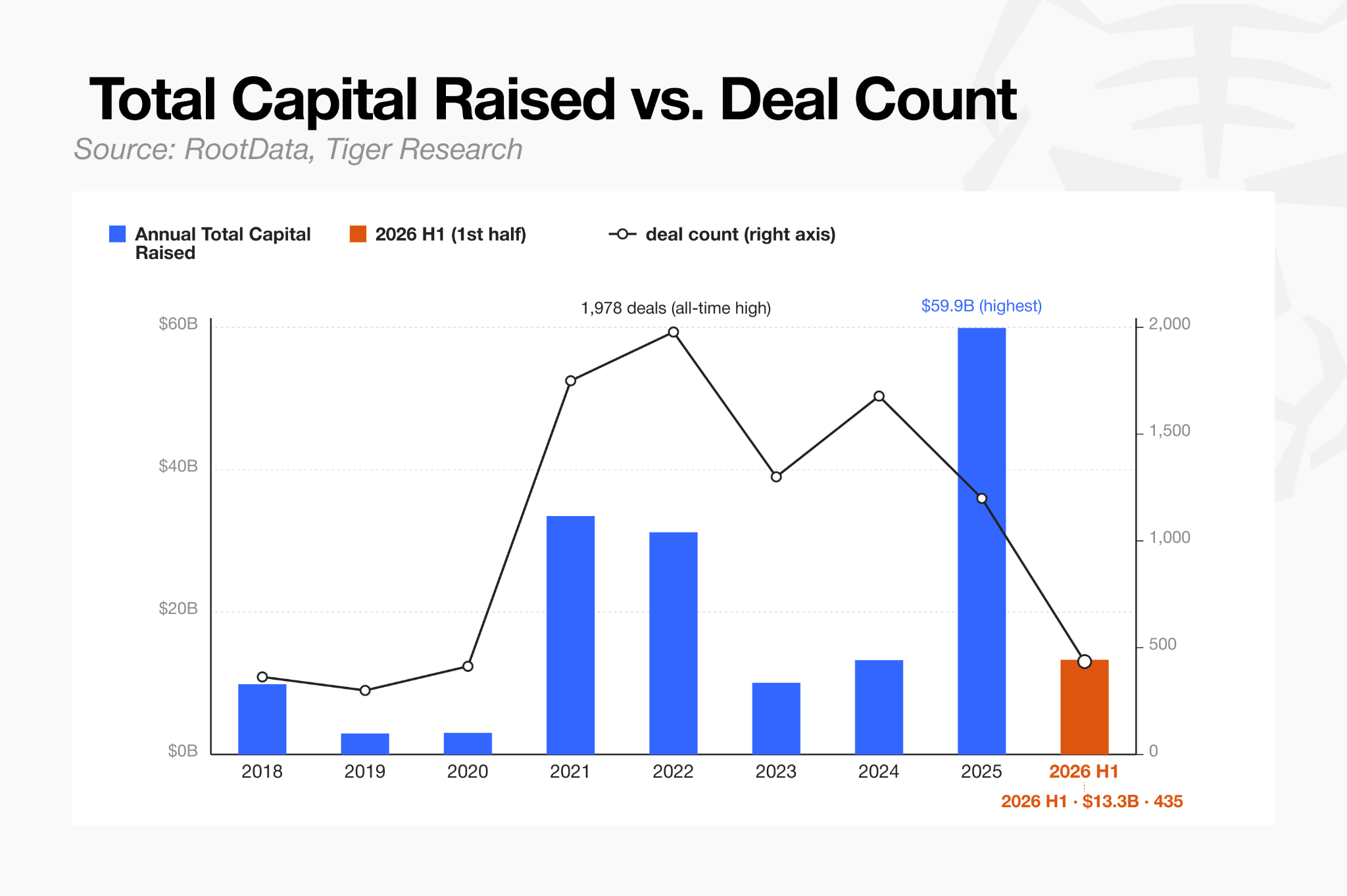

Capital inflows in the first half of 2026 reached $13.3 billion, already comparable to the $13.2 billion recorded for all of 2024, even as the number of funding rounds fell to just 435, a 78% decline from the 2022 peak of 1,978.

The market is now split between a small number of large, crypto-native venture capital firms that concentrate on lead investments and exchange-affiliated venture arms that compete on liquidity, while mid-sized firms without a clear competitive edge are being pushed out of the market at a rapid pace.

The number of funding rounds in the gaming sector fell 96%, from 141 in 2024 to just 5 in the first half of 2026.

Capital inflows into the payments and stablecoin sector and the centralized exchange (CEX) sector were driven entirely by mergers and acquisitions.

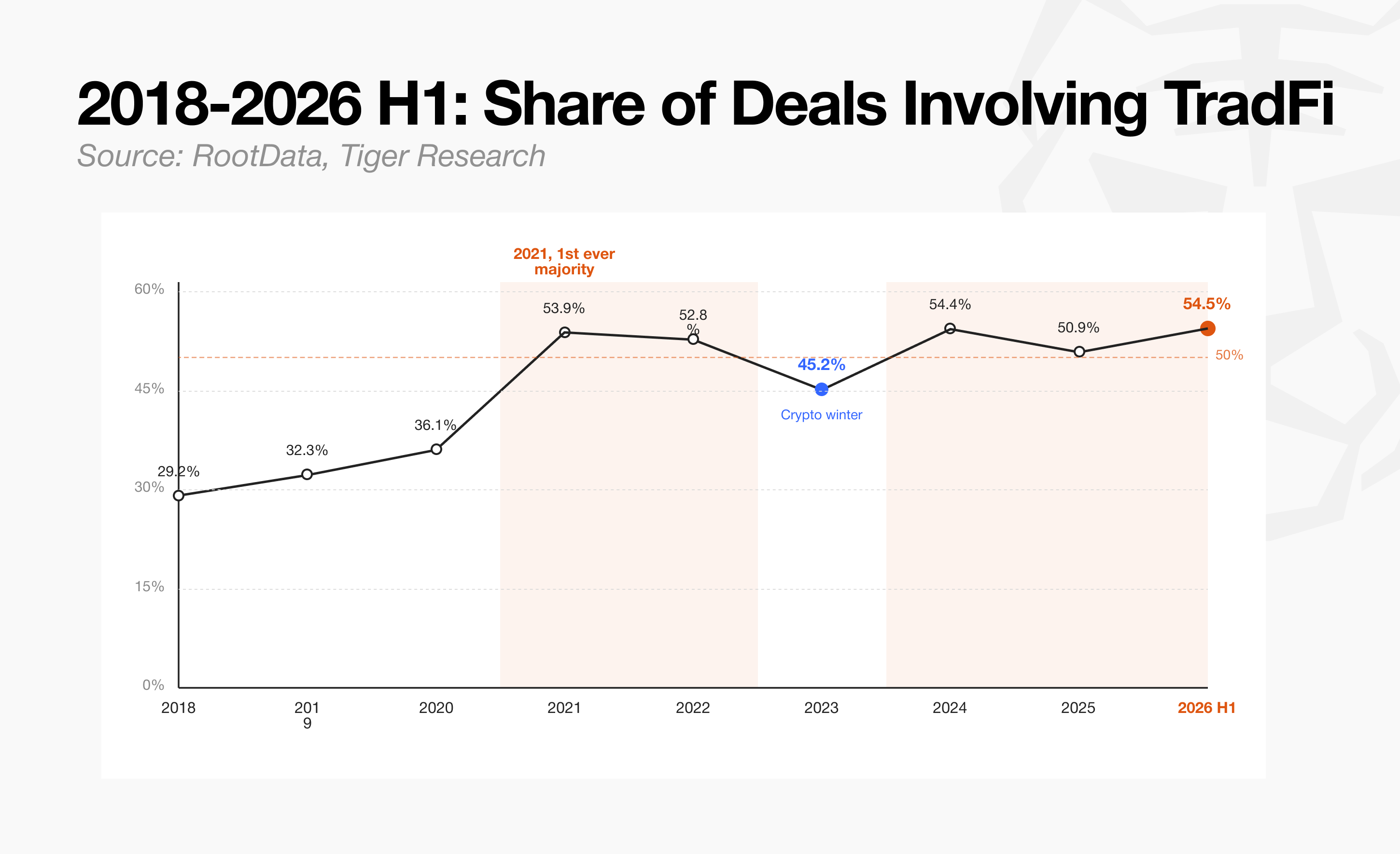

Traditional financial institutions took part in 54.5% of all investment deals recorded in the first half of 2026.

1. The 2021 Market: Speed and Diversification as Strategy

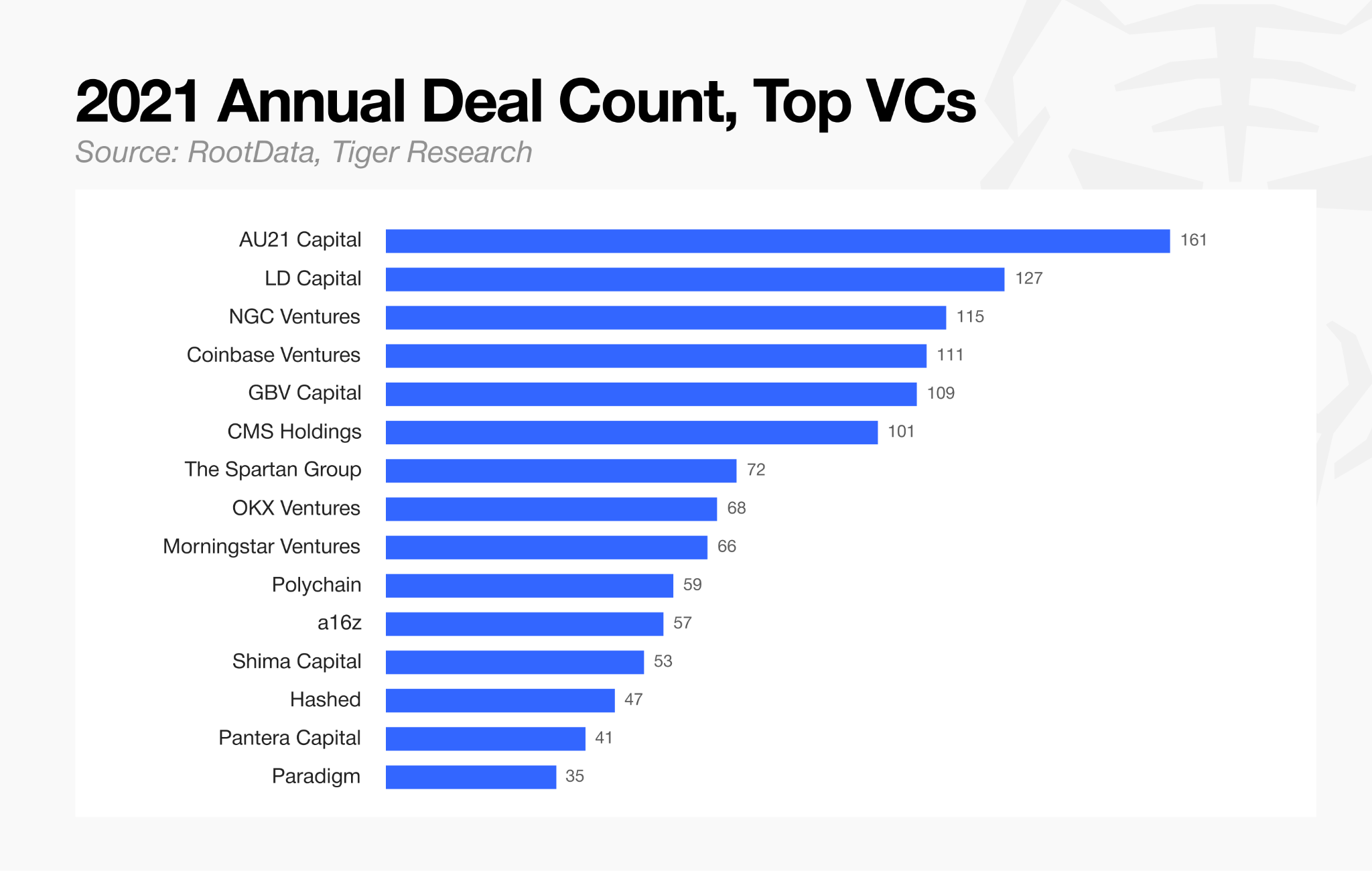

The core strategy in the 2021 crypto investment market was speed and portfolio diversification. Investors executed 1,750 deals that year, including seed rounds, and competition over speed was intense enough that AU21 Capital alone closed more than 13 deals a month on average.

Investment decisions at the time were reduced to simple criteria such as the token generation event (TGE) schedule and tokenomics, the structure governing how a project’s tokens are issued and distributed. Because token issuance alone could generate returns without any real product development, venture investors largely pursued a “spray and pray” strategy, spreading capital across dozens or even hundreds of projects regardless of valuation.

Speed of execution took priority over thorough due diligence. New rounds closed almost instantly, and VCs that missed a round often chased the next one at a higher valuation, a pattern of FOMO that repeated across the industry.

Many VCs that ran this strategy did not survive the bear market that followed, while the ones that did survive fundamentally changed their approach.

2. Which VCs Survived: A Changed Landscape

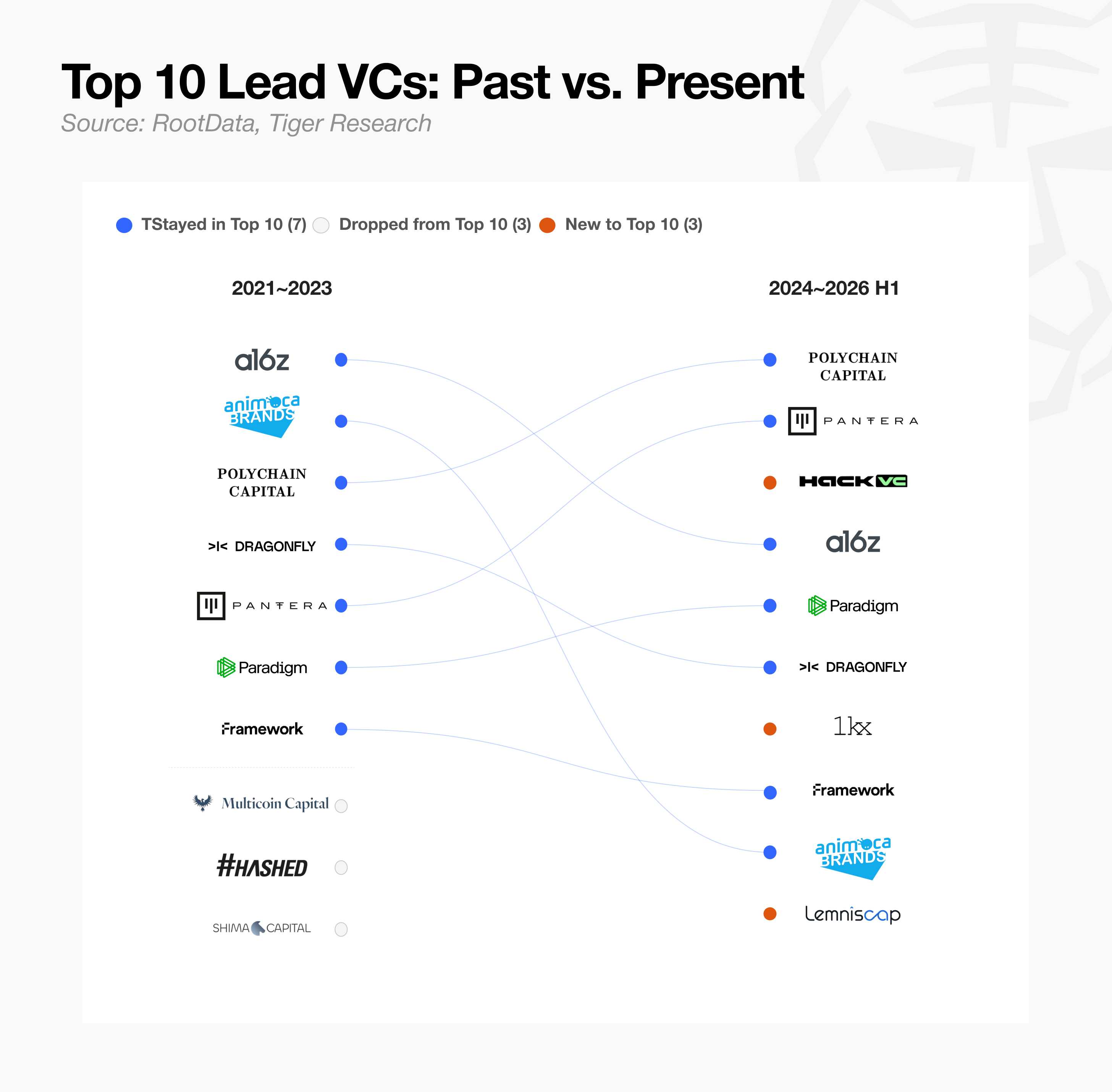

2.1. Lead Investment, Then and Now

The first metric to examine is lead investment, the rounds that major VCs have historically directed.

Some VCs remain active in leading deals today, while others have disappeared entirely or emerged only recently. Because leading a round has always required the reputation and scale of capital that only large VCs possess, the firms that led major rounds in the past have proven resilient, and most still rank among the top ten today.

2.2. How Surviving VCs Diverged

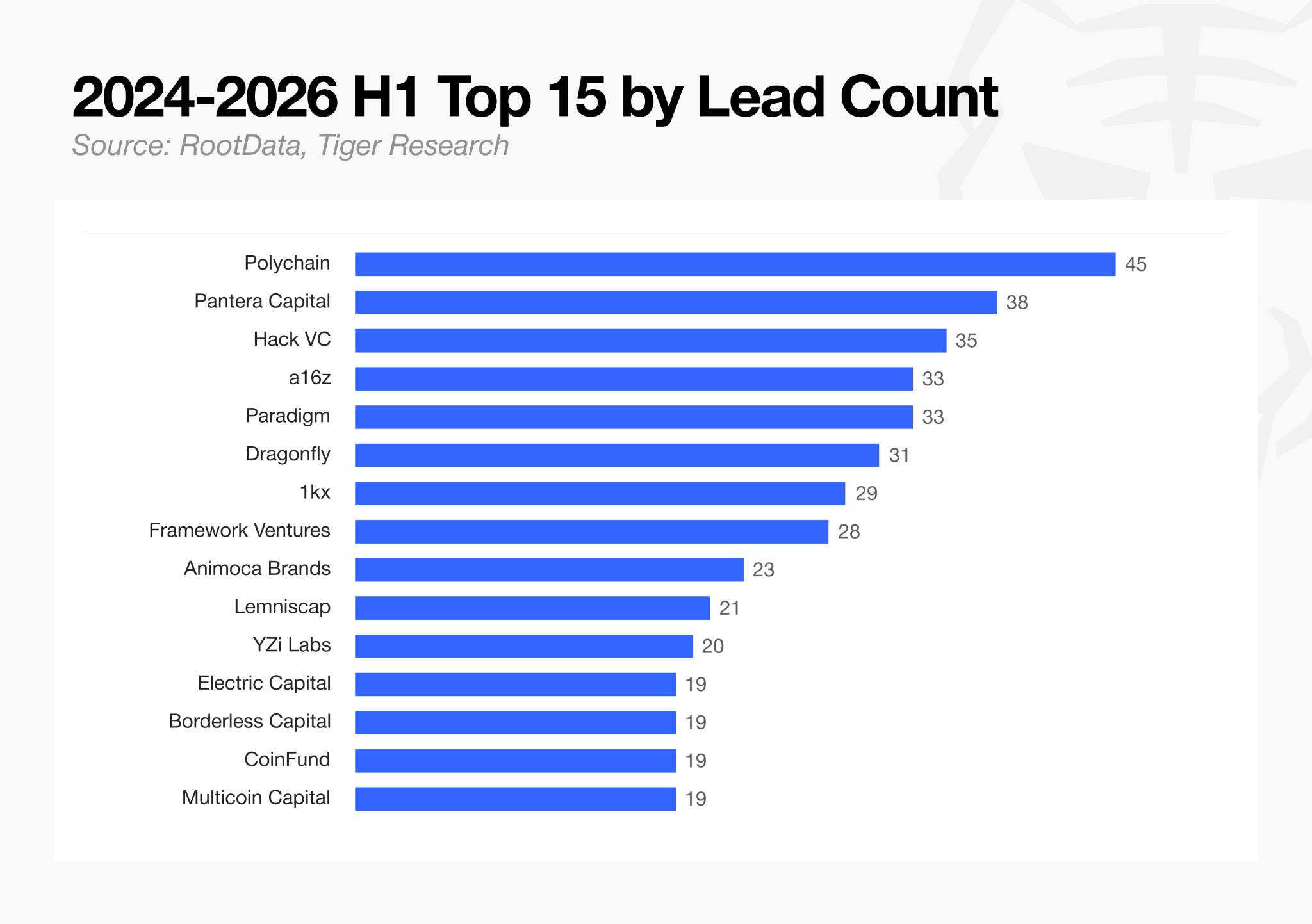

Looking at data from 2024 through 2026 as the most recent period, crypto-native VCs and established large firms are concentrating their resources on lead investments, engaging more deeply in individual deals. They have shifted their business model toward doing fewer deals overall while raising the bar on due diligence and securing board seats and greater influence over governance.

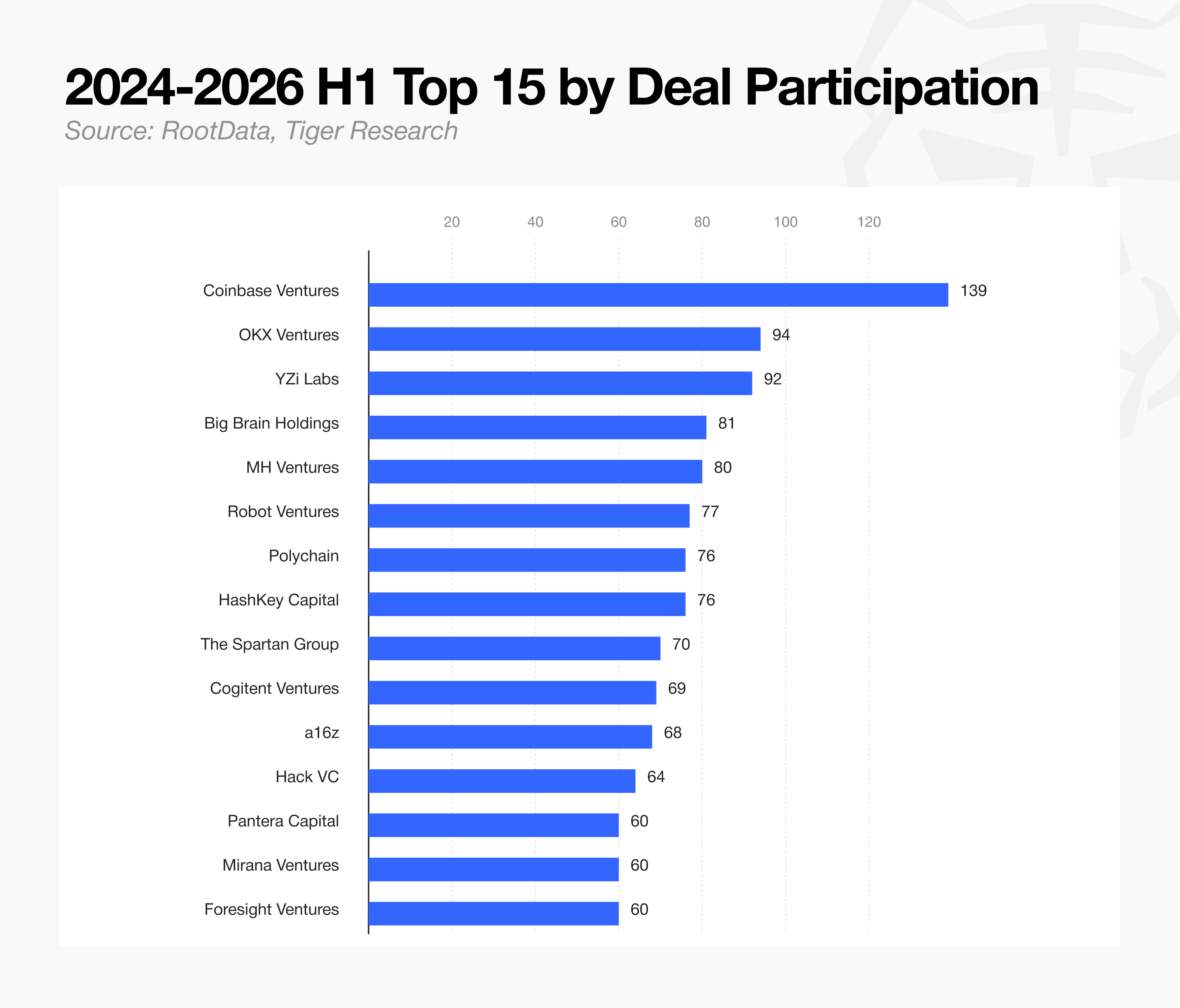

A different pattern emerges, however, in the cumulative count of round participation outside of lead investments.

Among the top 15 VCs by round participation from 2024 through the first half of 2026, exchange-affiliated firms account for a large share. Exchanges have been more active in joining rounds than in leading them. Coinbase Ventures ranked first with 140 deals, OKX Ventures second with 94, and YZi Labs third with 92. YZi Labs is the organization that resulted when Binance Labs rebranded in January 2025.

HashKey Capital, ranked seventh, is the venture arm of the Hong Kong exchange HashKey Exchange, and Mirana Ventures, ranked fourteenth, is the venture arm of Bybit. Five major exchanges appear in the top 15 through their respective venture arms alone. Large VCs that focus on leading rounds, such as Polychain and Pantera Capital, rank lower by this measure of overall round participation.

CEX-affiliated VCs have established themselves as core participants in major rounds by leading with the liquidity and marketing support their platforms can provide. Mid-sized VCs that lack a clear, defensible advantage, whether economies of scale, brand recognition, or exchange-level liquidity support, are being squeezed out of the market quickly as capital pressure and failed exits reinforce each other.

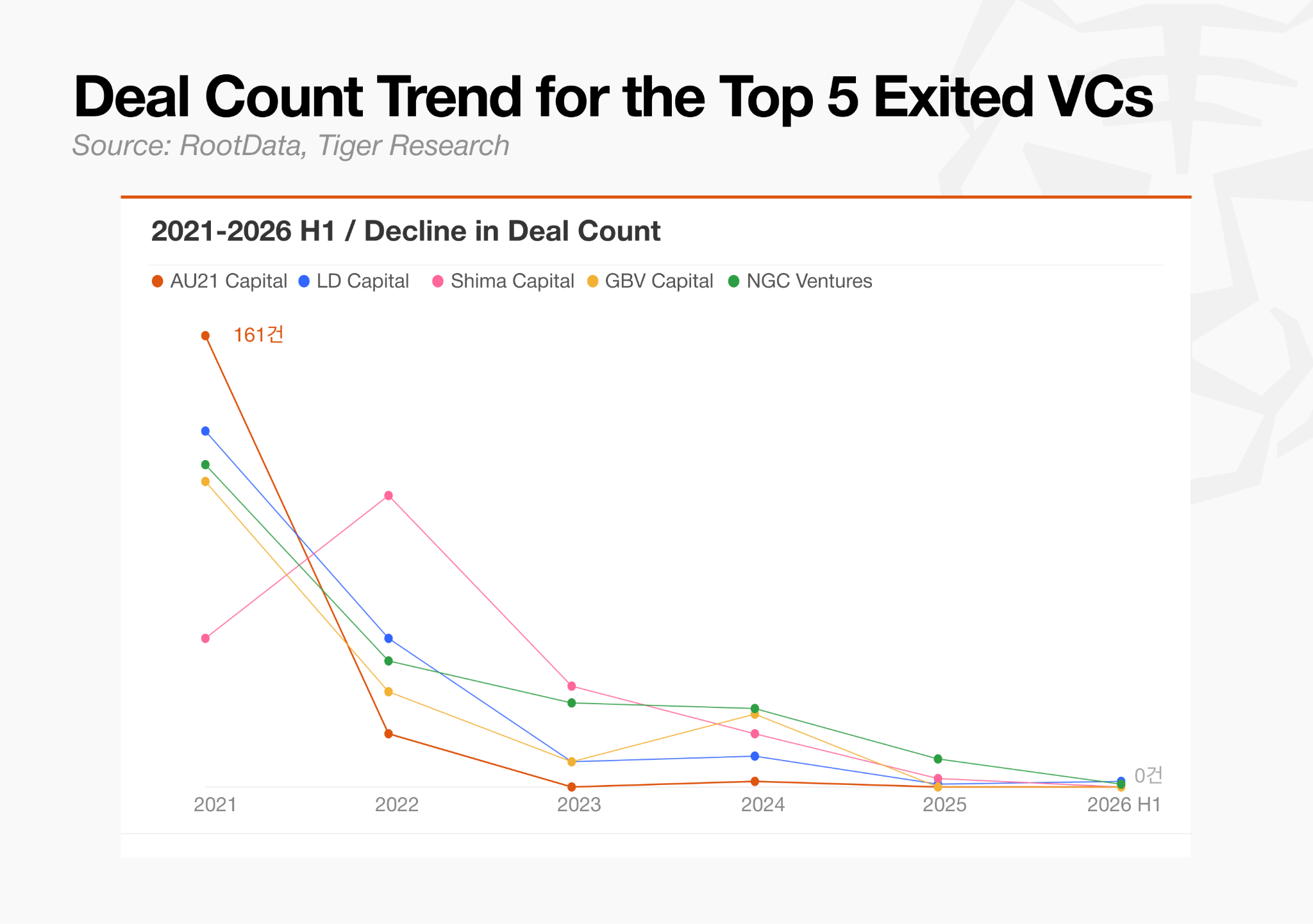

2.3. The VCs That Left: The End of Spray and Pray

Most VCs that built broad portfolios during the last bull market by relying on quick token liquidation have since disappeared. AU21 Capital, LD Capital, and Shima Capital saw their deal counts fall by as much as 98.9% and effectively lost their influence in the market. A strategy built on riding short-term narratives no longer worked once a prolonged bear market and tighter regulation set in.

Their failure to develop any real differentiation was the main cause, but it is also worth noting that the broader flow of crypto capital has shifted toward projects that have already reached some degree of maturity, and few new projects requiring early-stage funding are emerging. In other words, the kind of opportunity these VCs depended on has stopped appearing in the market.

3. Investment Rounds: Buying the Fruit, Not the Seed

3.1. The Seed Collapse

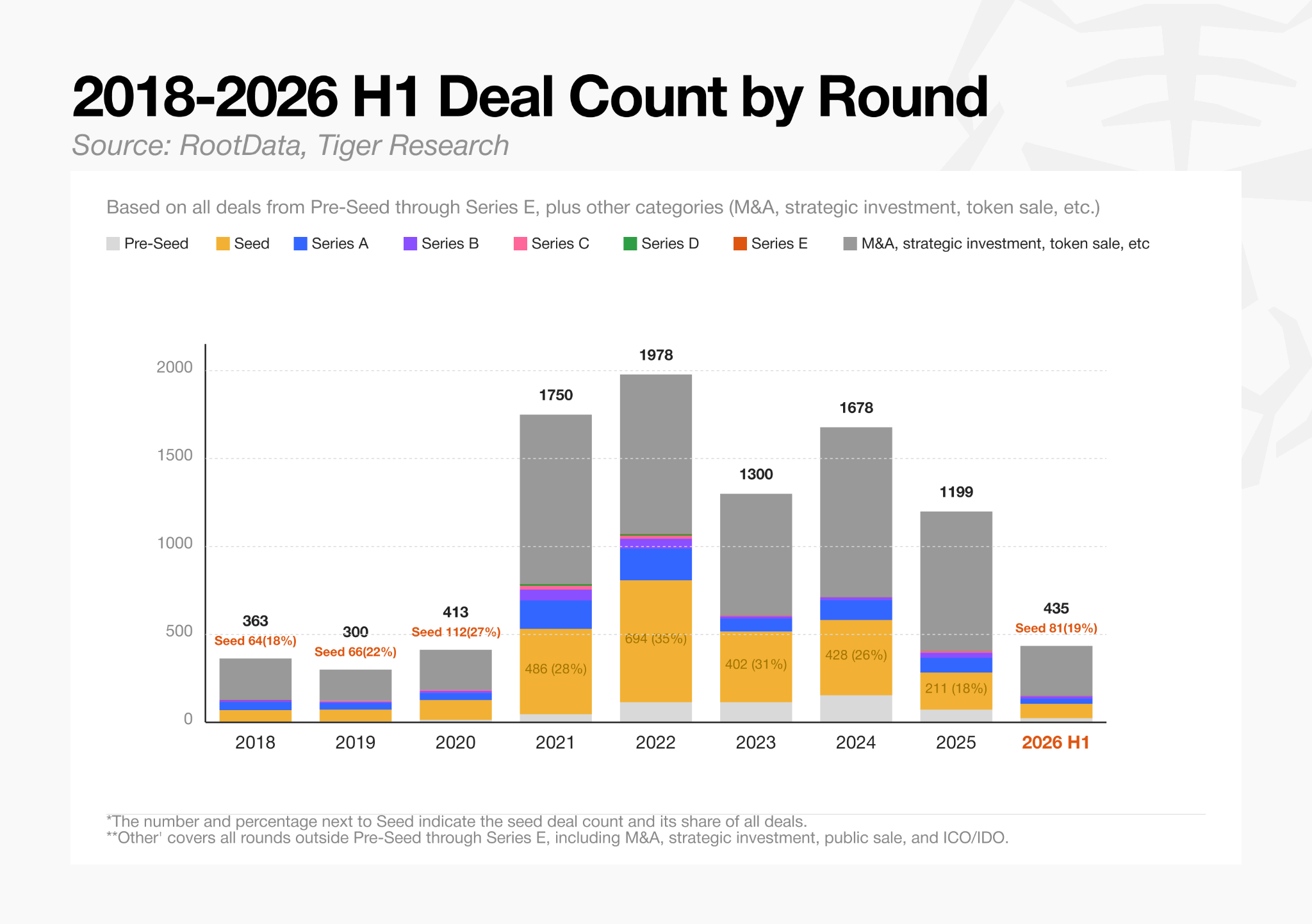

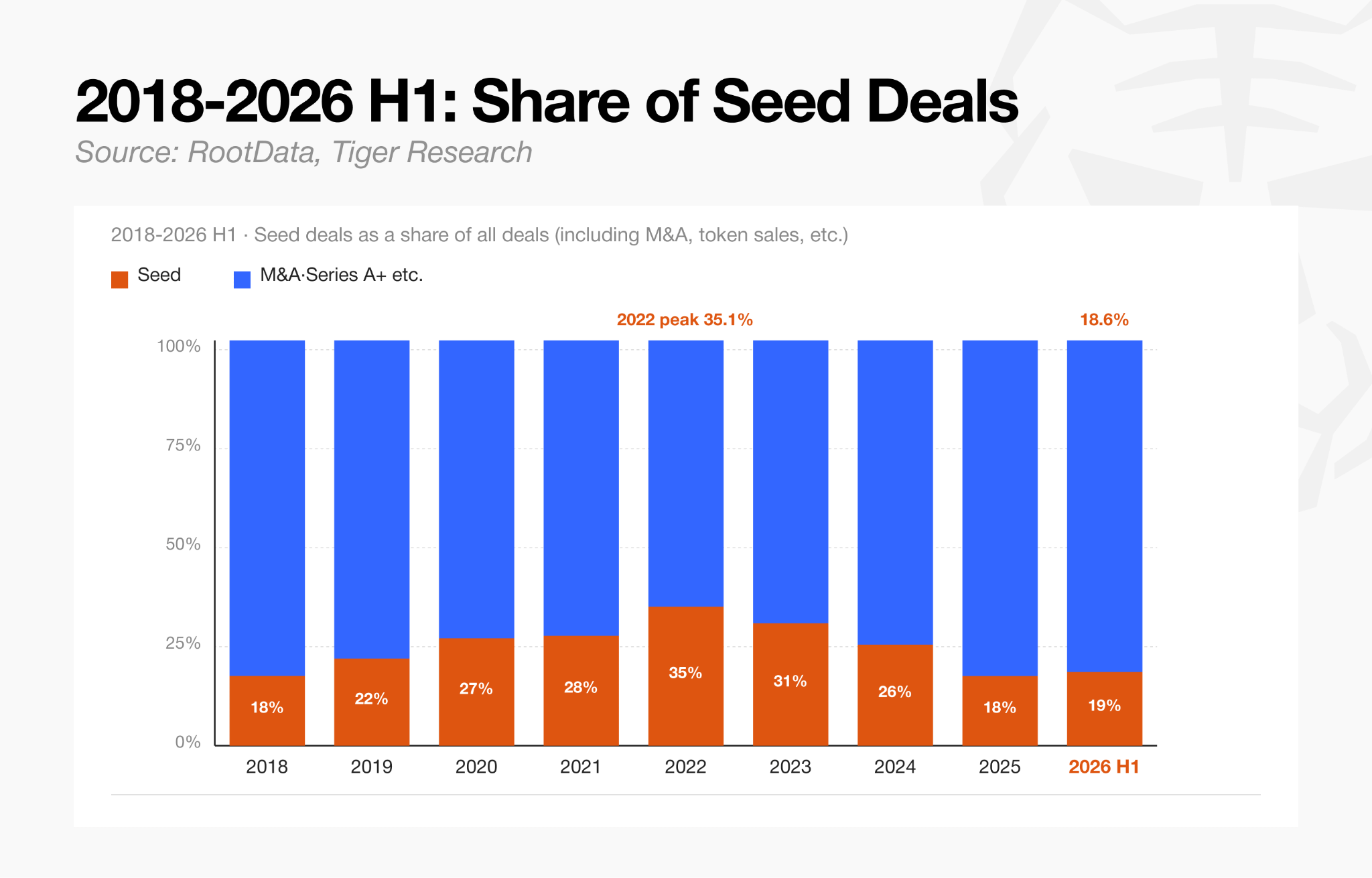

Seed-stage deals totaled 81 in the first half of 2026, down 88% from 694 in 2022. The market’s aversion to early-stage projects with unproven business models and higher risk is clearly evident. This decline also shows up in the overall structure of funding rounds: seed rounds accounted for 35.3% of all deals in 2022, a share that fell to 18.7% by the first half of 2026.

The decline in seed rounds can be read as reflecting both investor aversion and a simple shortage of new early-stage projects seeking seed funding. It is a metric that captures market contraction and market maturity at the same time.

3.2. Capital Concentrating in Later Stages

Measured by capital allocation, later-stage rounds, Series A and beyond, now account for 75.2% of total investment. Seed-stage investment briefly held a majority share during the 2023 bear market, but capital quickly reallocated toward well-capitalized companies once the market entered recovery.

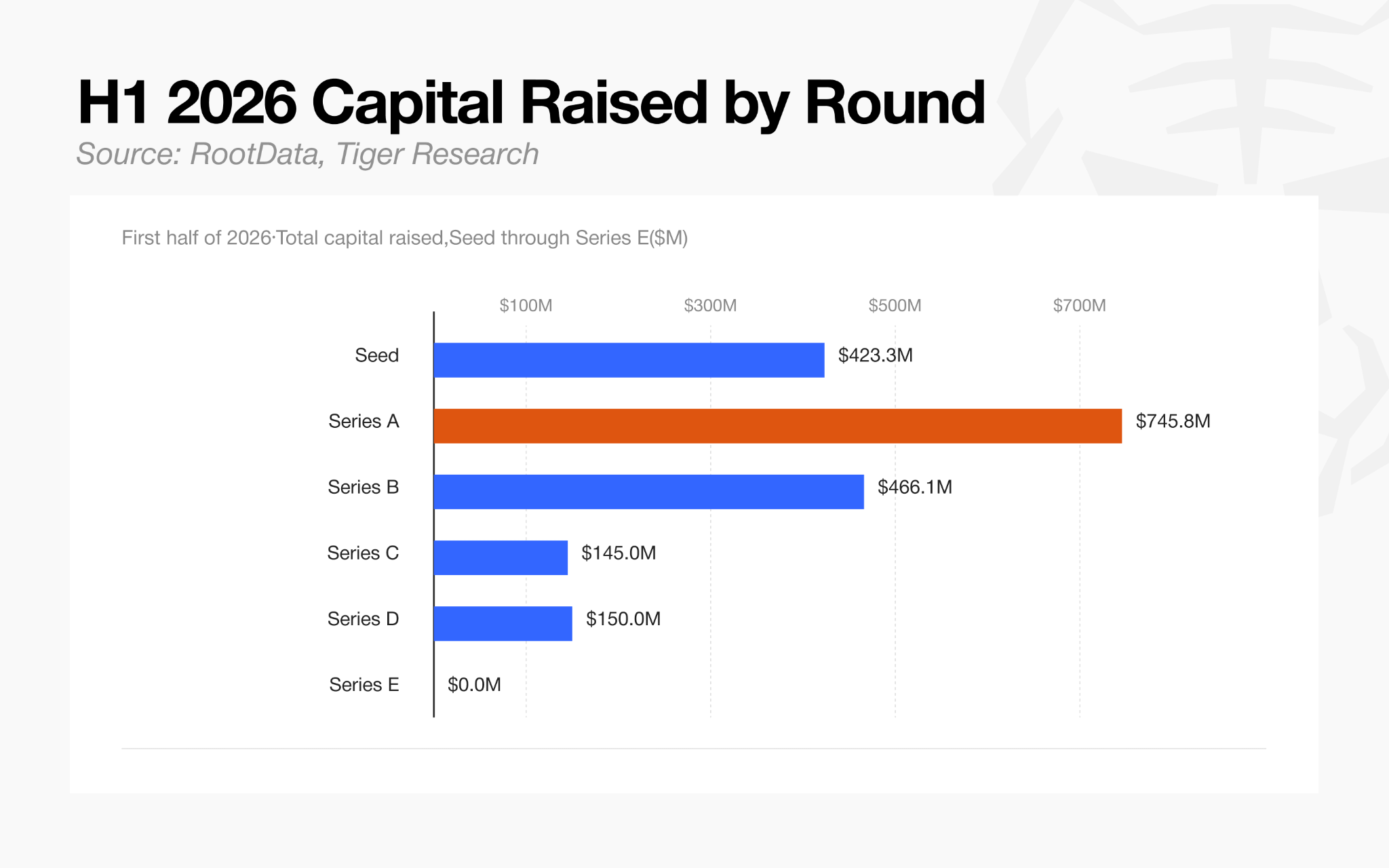

In the first half of 2026, total Series A funding ($745 million) exceeded all seed-stage capital raised ($423 million), making it the largest category of any round.

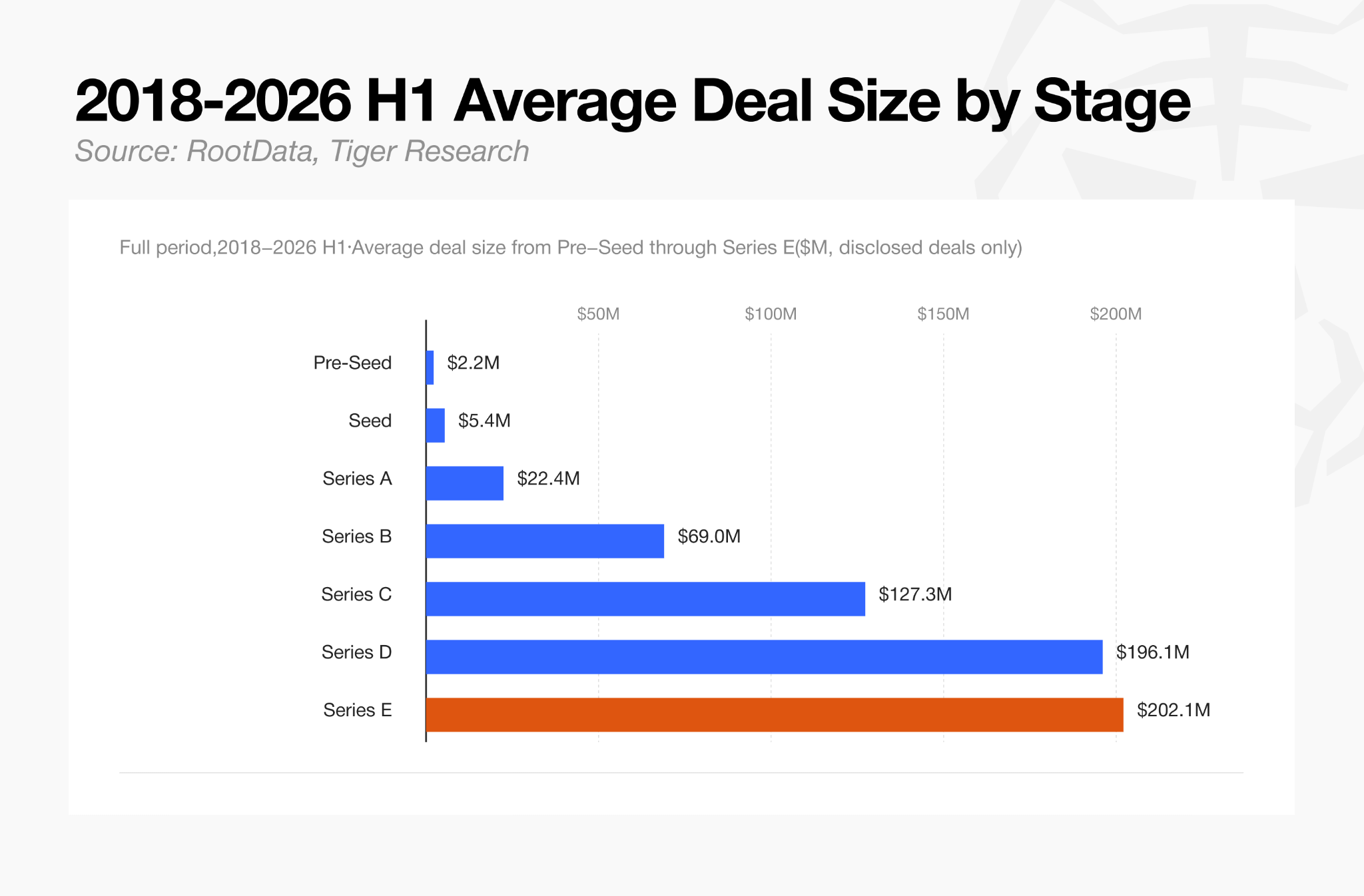

Average deal size rises in a clear step pattern from one stage to the next: $5.4 million at seed, $22.4 million at Series A, $127 million at Series C, and $202 million at Series E. The sample size shrinks at later stages, but .companies that reach those stages have already seen their revenue and valuation increase, so each round involves a correspondingly larger amount of capital.

4. The Market Overall: Capital Concentrates as Deal Count Falls

4.1. Capital and Deal Count Diverge

Total capital inflows reached $13.3 billion in the first half of 2026, while the total deal count of 435 amounted to only 22% of the 1,978 deals recorded in 2022, the year with the highest annual deal count. From 2024 to 2026, capital volume held steady or rose even as it concentrated into a much smaller number of deals.

Small, diversified bets from VCs chasing short-term returns around token liquidity events have declined, while large direct investments from traditional financial institutions have increased. Institutions apply stricter criteria, evaluating not token listing schedules or market narratives but whether a company has an auditable revenue structure and the necessary regulatory licenses.

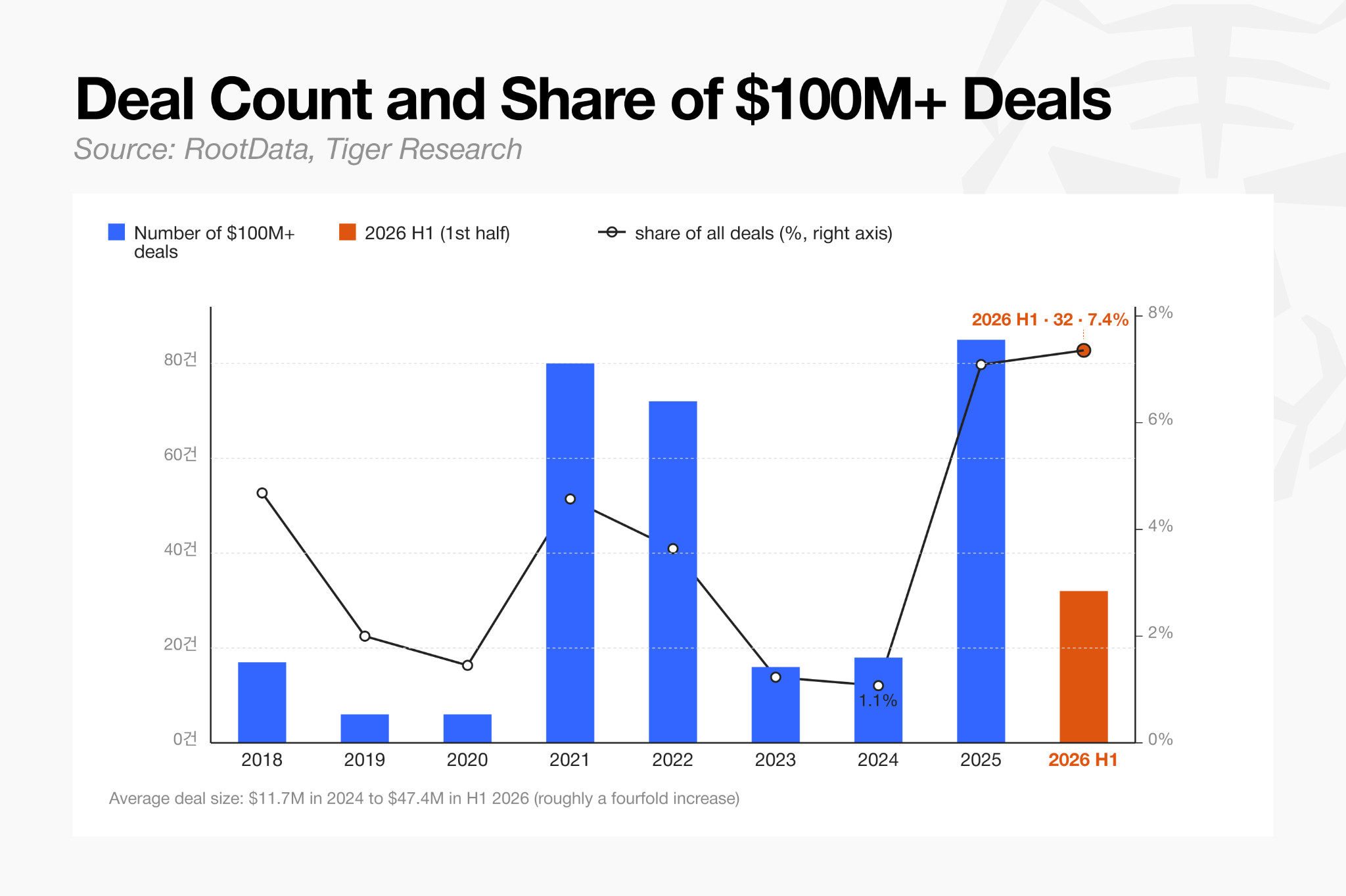

Deals of $100 million or more totaled 32 in the first half of 2026, accounting for 7.4% of all deals, up sharply from 1.1% in 2024. Over the same period, the average deal size roughly quadrupled, from $11.7 million in 2024 to $47.4 million in the first half of 2026.

This rise in share came from two directions at once. The number of large deals itself increased, while the total deal count fell as small deals, including seed rounds, disappeared. A small group of surviving projects began to dominate the market, and as small deals vanished, the already limited pool of large deals also came to represent a larger relative share.

4.2. Direct Participation in Venture Rounds

The share of investment deals involving traditional financial institutions rose from 29.2% in 2018 and first crossed the majority mark, reaching 53.9%, in 2021. Their participation dipped to 45.2% in 2023 during the last downturn, rebounded to 54.4% in 2024 as regulation became more defined, fell back to 50.9% in 2025, and reached 54.5% in the first half of 2026. Participation has remained near its highs ever since first crossing the majority mark in 2021.

In one example, a16z led the $355 million round for Digital Asset, the developer of Canton Network, but core institutional players, including BNP Paribas, HSBC, S&P Global, and Hanwha Investment & Securities, invested directly rather than through a venture subsidiary.

Where investment once entered mostly at the earliest stage, the growth of crypto VC firms and the entry of traditional investors have shifted more capital toward companies that have already reached some degree of maturity.

5. Sectors: Surviving a Changed Environment

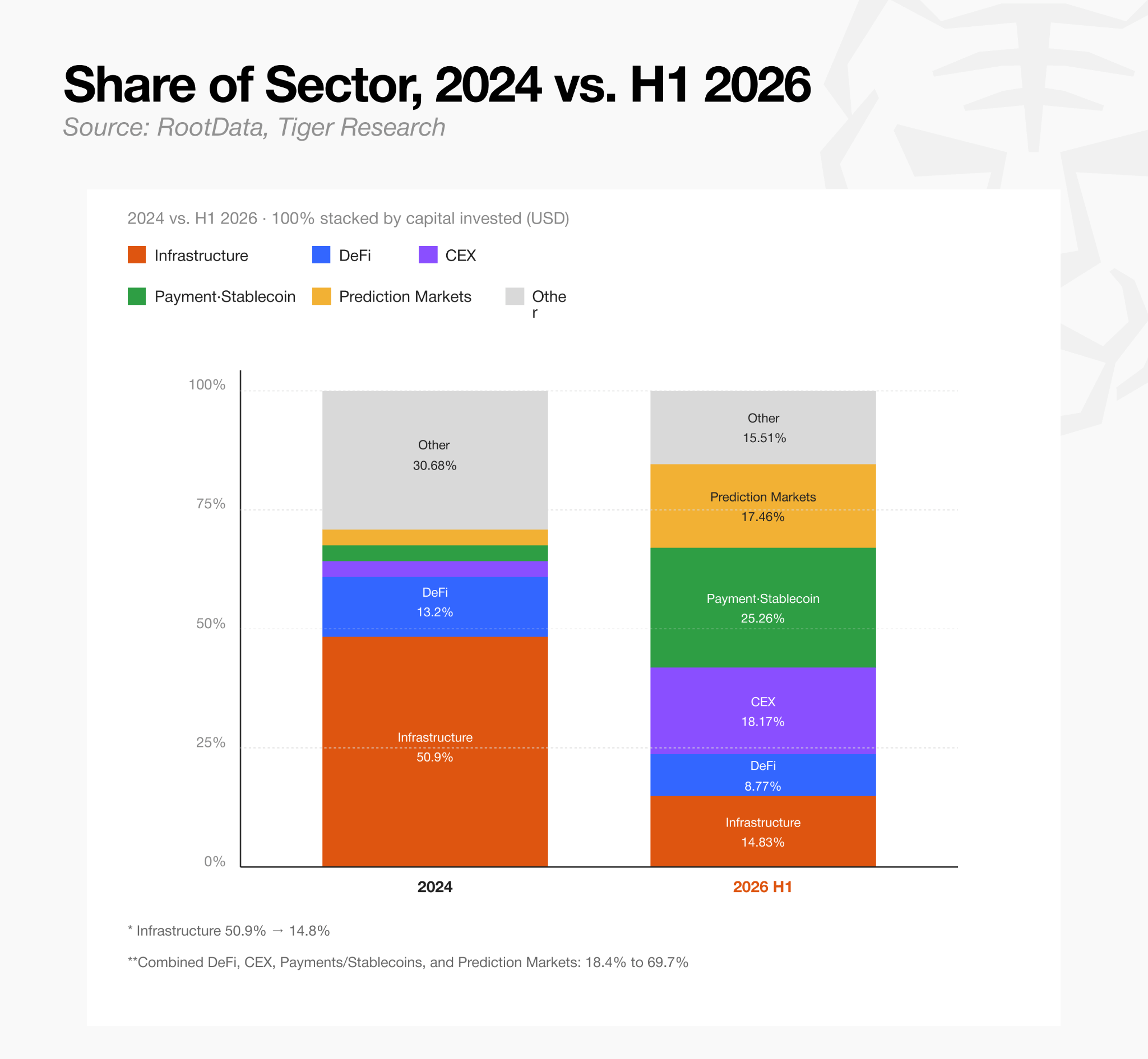

2024 was the year spot bitcoin ETF approval coincided with a more favorable regulatory environment, producing the first clear sector-level capital flows since the bear market, and this analysis uses it as the baseline year for sector comparisons.

In 2024, the year bitcoin ETFs were approved, the infrastructure sector held a majority share of total investment capital at 50.9%. That share had fallen sharply to 14.8% by the first half of 2026. Payments and stablecoins (25.3%), centralized exchanges (18.2%), and prediction markets (17.5%) took the lead instead, reshaping the sector landscape entirely.

This shift suggests that blockchain infrastructure has changed character, from a standalone investment target to a practical platform that institutional businesses put to use. Representative examples include Robinhood running its own layer built on Arbitrum, and Securitize adopting Solana and Avalanche as settlement layers around the same time it listed on the New York Stock Exchange. In other words, the current capital market’s core demand has moved past building new protocol infrastructure from scratch, toward actually operating real-world financial services on top of existing infrastructure layers.

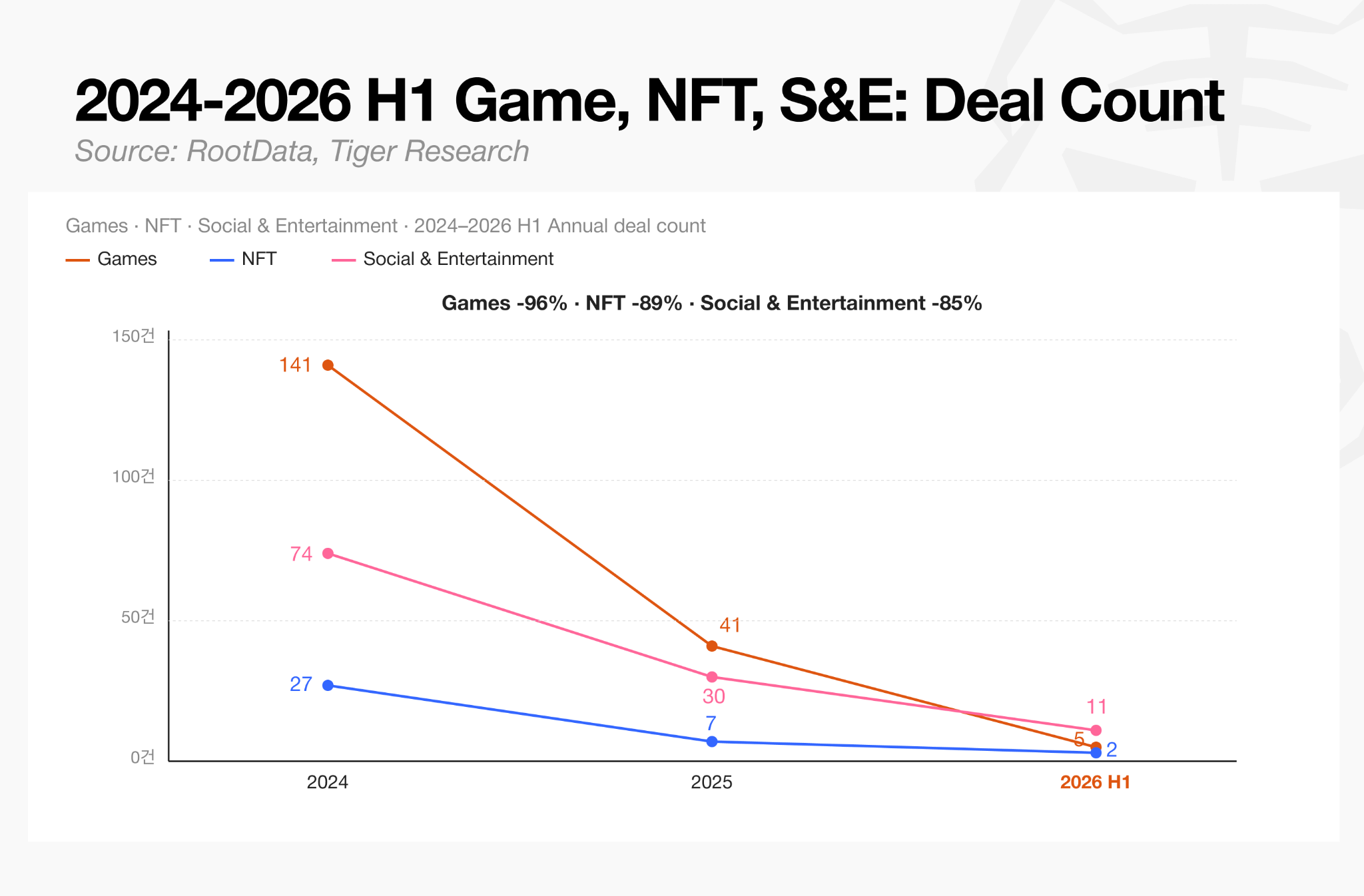

5.1. The Laggards: Gaming, NFTs, and Social

All three sectors saw deal counts fall sharply. Gaming dropped from 141 deals to 5, NFTs from 27 to 2, and social and entertainment from 74 to 11.

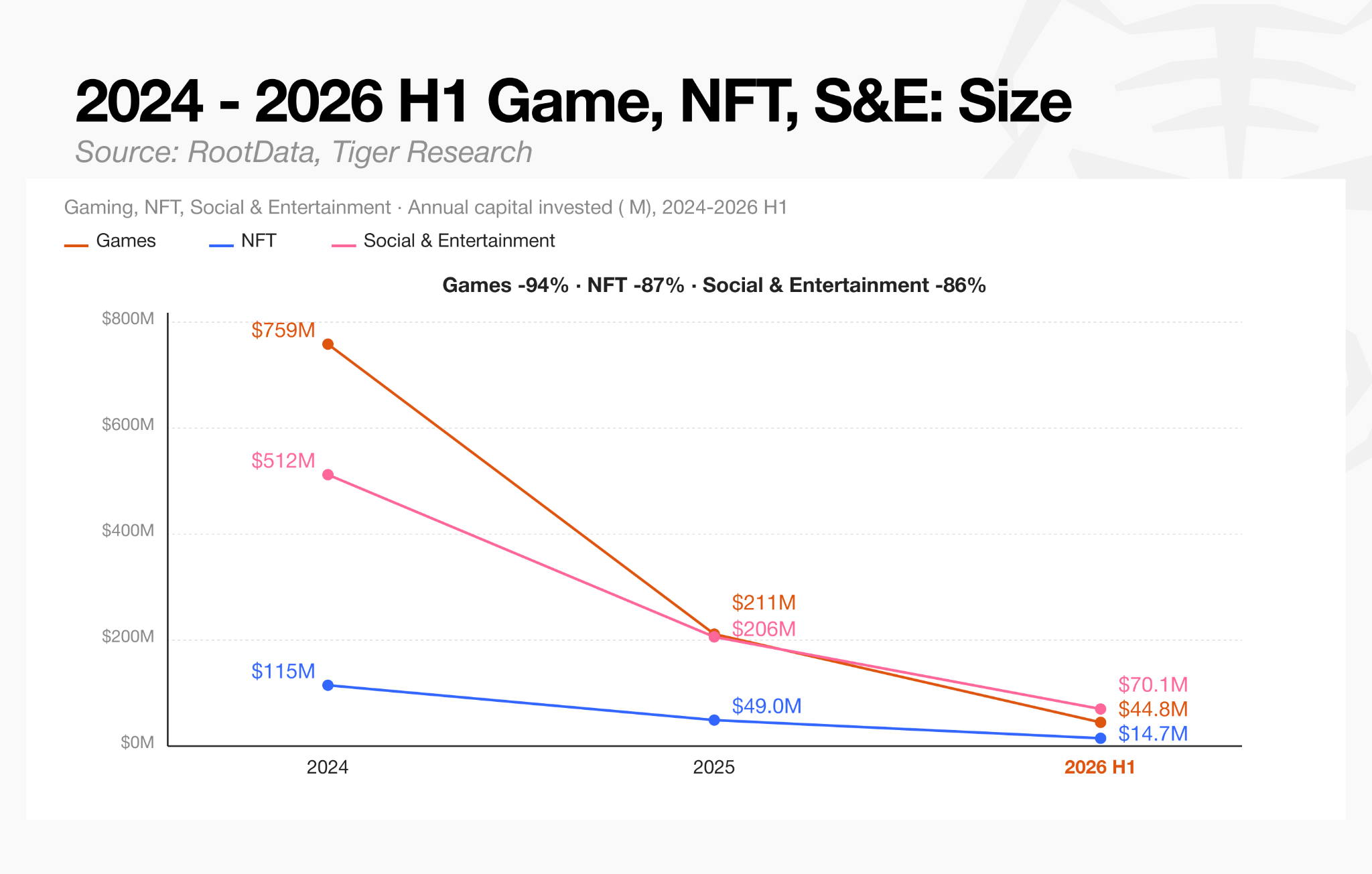

Capital inflows followed the same downward path in all three. Gaming capital fell from $758.6 million to $44.8 million, NFT capital from $114.9 million to $14.7 million, and social and entertainment capital from $512.1 million to $70.1 million.

Gaming showed the steepest decline of the three. The earlier GameFi model, which combined gaming with token-based rewards, tended to lean too heavily on token issuance for financial returns rather than building sustainable gameplay. As soon as new user growth slowed, this model fell into what is known as a death spiral, a structural cycle in which falling token value and user attrition reinforce each other, and it never found a way out. As a result, user traffic data, once a key metric in due diligence, lost its reliability, and capital inflows into the sector were effectively cut off.

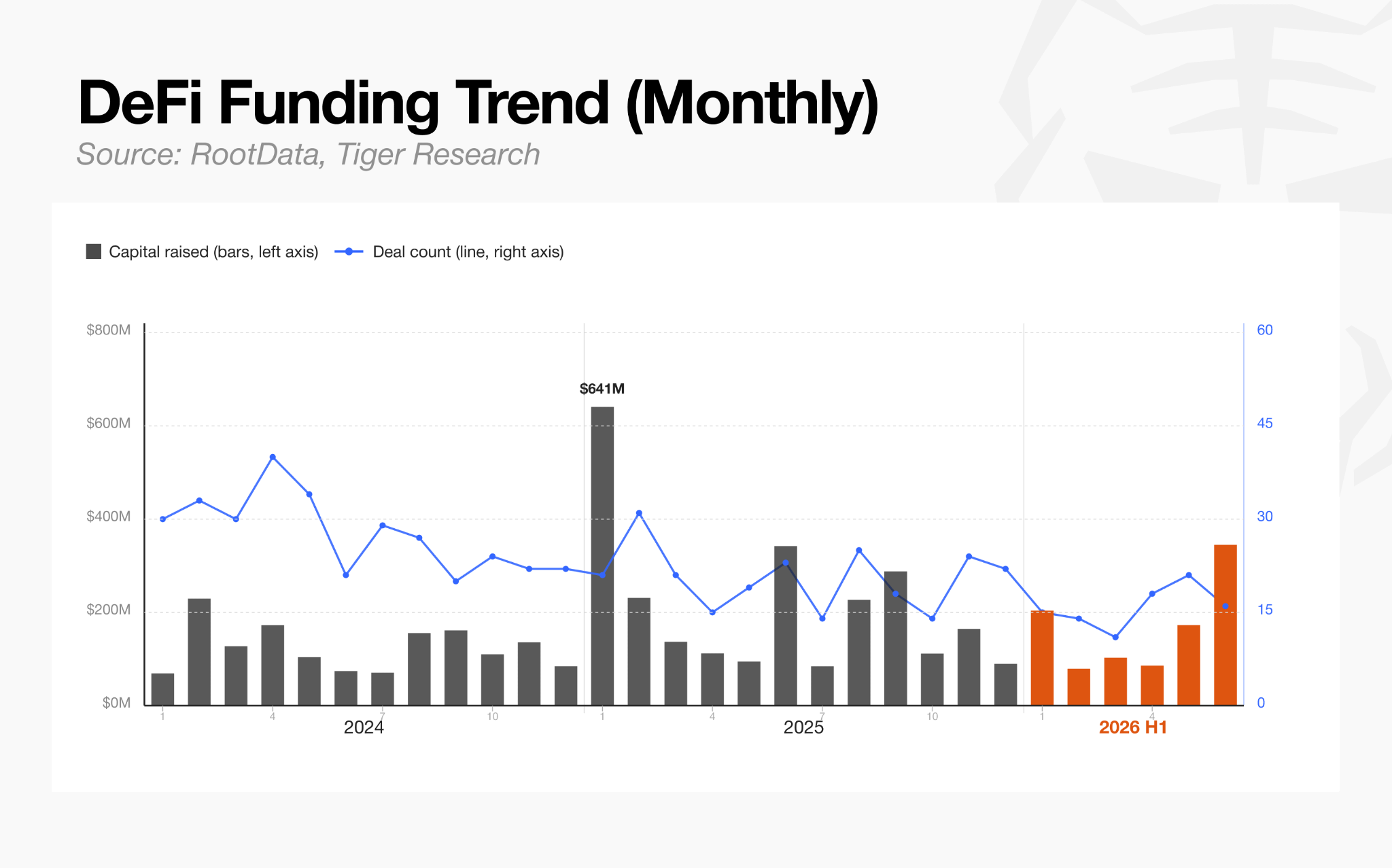

5.2. DeFi: Quiet but Steady

Deal count in the decentralized finance (DeFi) sector fell 71%, but total investment declined by only about 34%. Average deal size actually rose, from $4.5 million in 2024 to $10.4 million in the first half of 2026, showing that as overall deal count contracted, capital concentrated in a small number of large deals.

The main driver of this concentration was a token sale round by the lending protocol Morpho, aimed at institutions and investment firms. Morpho, which used its modular lending protocol to open the DeFi vault market to institutions and redefine DeFi risk standards, raised $175 million in a token round led by a16z crypto, Paradigm, and Ribbit Capital on June 9, 2026. That single round accounted for 17.7% of all DeFi investment in the first half of 2026, a clear reflection of how concentrated the market has become.

The DeFi sector, in other words, has moved away from broad-based ecosystem growth, with capital instead shifting toward a small number of protocols that the market has already validated.

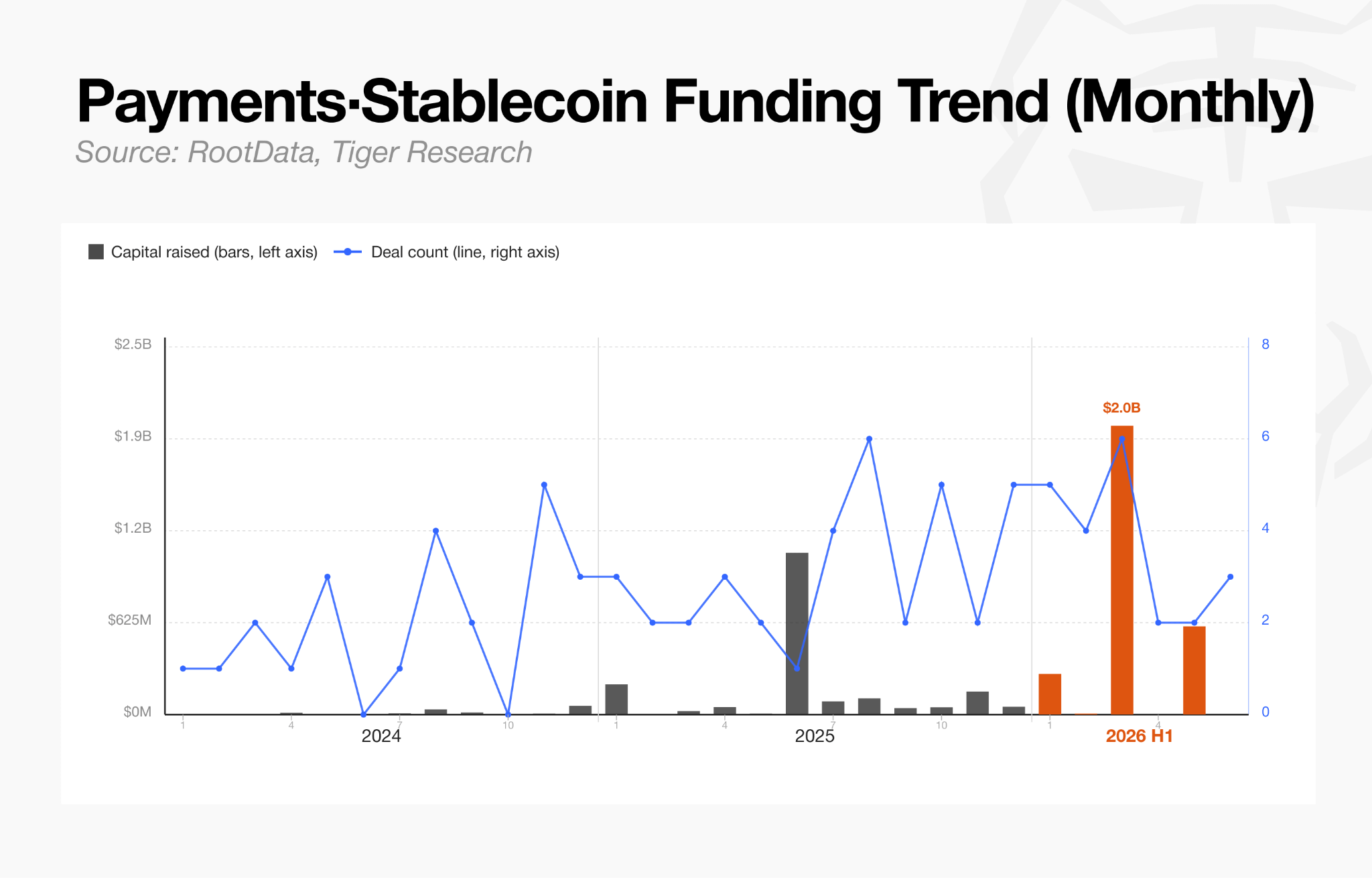

5.3. Payments and Stablecoins: The Fastest-Rising Sector

Deal count in the payments and stablecoin sector has kept accelerating on a monthly average basis. Total investment over the same period jumped roughly twentyfold, from $143.9 million to $2.85 billion in the first half of 2026. Much of this increase, however, is attributable to a handful of large M&A transactions.

The largest deal in the first half of 2026 was Mastercard’s acquisition of BVNK for $1.8 billion in March, followed by Payward’s (Kraken’s parent company) acquisition of Reap for $600 million in May. These two transactions alone accounted for about 84% of total sector investment in the first half of 2026. Cross-border payment and crypto card issuers, including Rain ($250 million) and KAST ($80 million), also raised capital steadily, supporting the sector’s growth.

These recent large-scale M&A deals indicate that traditional payment companies and major Web3 institutions have moved beyond simple business partnerships and are now acquiring and directly controlling stablecoin infrastructure. Stripe offers the clearest example of this race to set the ecosystem standard, beginning with its acquisition of Bridge in October 2024.

After acquiring Bridge, Stripe partnered with Paradigm to build Tempo, a blockchain dedicated to stablecoin payments, and successfully launched its mainnet in March 2026. That June, Bridge co-founder Zach Abrams became interim head of the entity operating Open USD (OUSD), a global consortium stablecoin project with more than 140 participating companies.

The OUSD project has adopted Bridge, which Stripe acquired and continues to develop, and Tempo, which Stripe is building, as its core initial infrastructure. The technology and talent Stripe gained through acquisition now control both pillars at once: its own proprietary platform and the industry consortium meant to set the standard. This shows that competition over stablecoin infrastructure has moved fully past company-level acquisitions and into a contest over setting the global standard for the entire market.

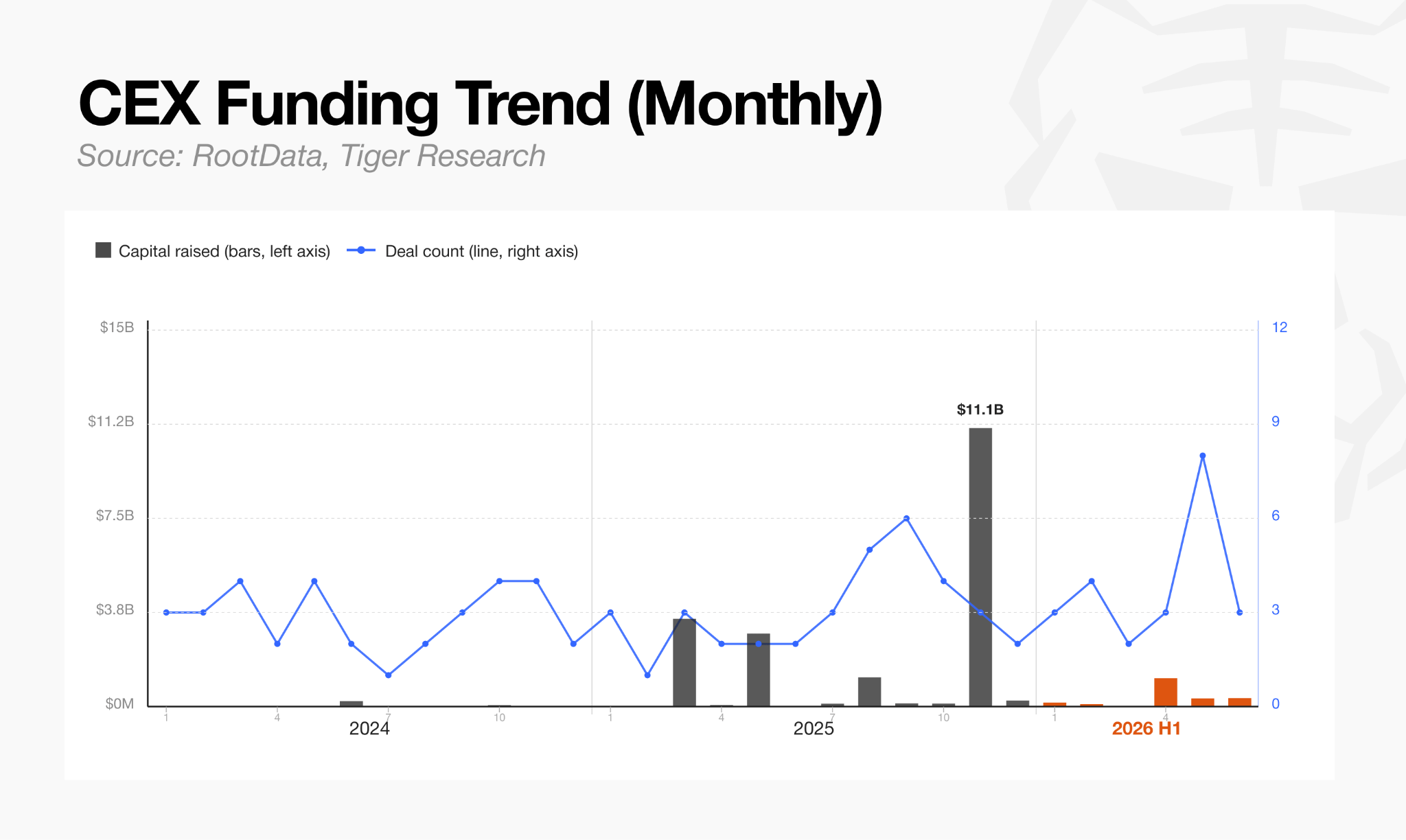

5.4. CEX: Venture Capital No Longer Needed

The centralized exchange (CEX) sector’s share of total investment jumped from 3.0% in 2024 to 18.2% in the first half of 2026. This increase, however, is difficult to read as an expansion of traditional venture investment into new exchanges, since M&A alone accounted for 75.5% of all CEX sector investment recorded from 2024 through the first half of 2026. That share climbed from 58.8% in 2024 to 78.9% in 2025, reflecting an overwhelming degree of concentration.

Overall capital inflows declined from the prior year’s peak of $19.4 billion, when large M&A deals were concentrated, but remained more than six times the 2024 level of $340 million. Deal count has not slowed either, holding a steady pace on a half-year basis. The 23 deals recorded in the first half of 2026 averaged 3.8 per month, faster than the pace of 2.8 per month in 2024 and 3.0 per month in 2025.

What the CEX investment market is showing, in other words, is a reshuffling centered on a small number of large operators. Naver’s acquisition of a stake in Dunamu remains under regulatory review but was the largest deal announced during the period, followed by Coinbase’s acquisition of Deribit for $2.9 billion and Kraken’s acquisition of NinjaTrader for $1.5 billion.

Abu Dhabi’s sovereign wealth fund MGX’s $2 billion strategic investment in Binance fits the same pattern. At the same time, venture arms of existing large exchanges, such as OKX Ventures and HashKey Capital, are participating more actively in investment rounds and acquisitions of their own. As a result, CEX players are increasingly taking on a dual role, acting as both investment targets and strategic investors.

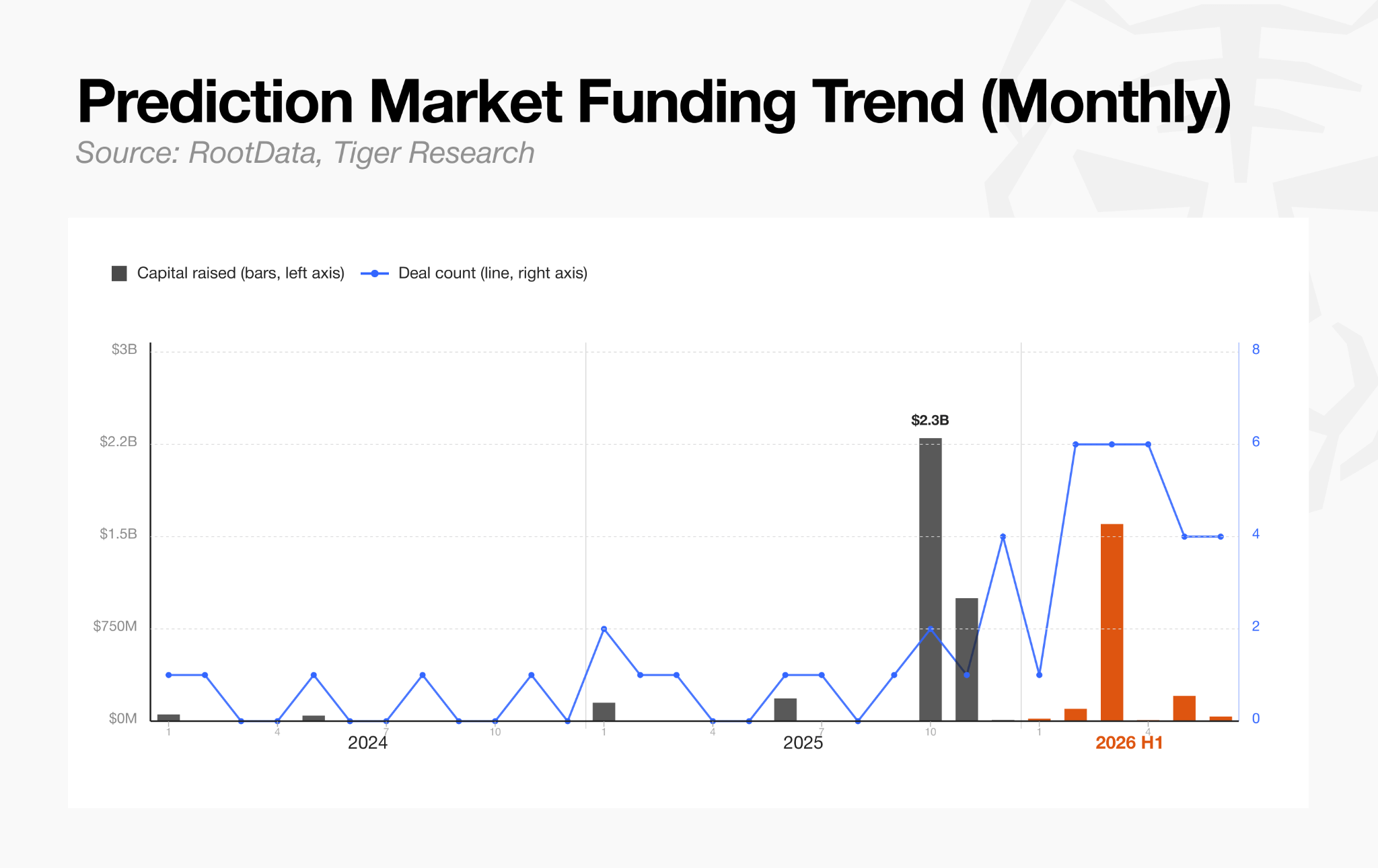

5.5. Prediction Markets: A New Sector Emerges

Prediction markets have emerged as a sector that provides liquidity for real-world macro indicators such as economic data, elections, and policy decisions. The trigger for the sector’s growth was formal regulatory approval from the Commodity Futures Trading Commission (CFTC) in May 2025, which opened the door for large-scale capital inflows from hedge funds and asset managers as the sector entered the regulated mainstream.

Kalshi surpassed $100 billion in cumulative trading volume in June 2026. It had already raised $1 billion in a round led by Paradigm in December 2025, followed by another $1 billion led by Coatue.

Polymarket raised capital from Intercontinental Exchange (ICE), the operator of major traditional exchanges. In October 2025, ICE committed up to $2 billion, of which it actually deployed $1 billion, and it added another $600 million in March 2026, bringing its cumulative investment to about $1.6 billion.

Rather than a field of many competing new projects, the prediction market sector is settling into a structure in which traditional financial institutions and top-tier institutional capital repeatedly funnel large rounds into the two players that secured regulatory approval first.

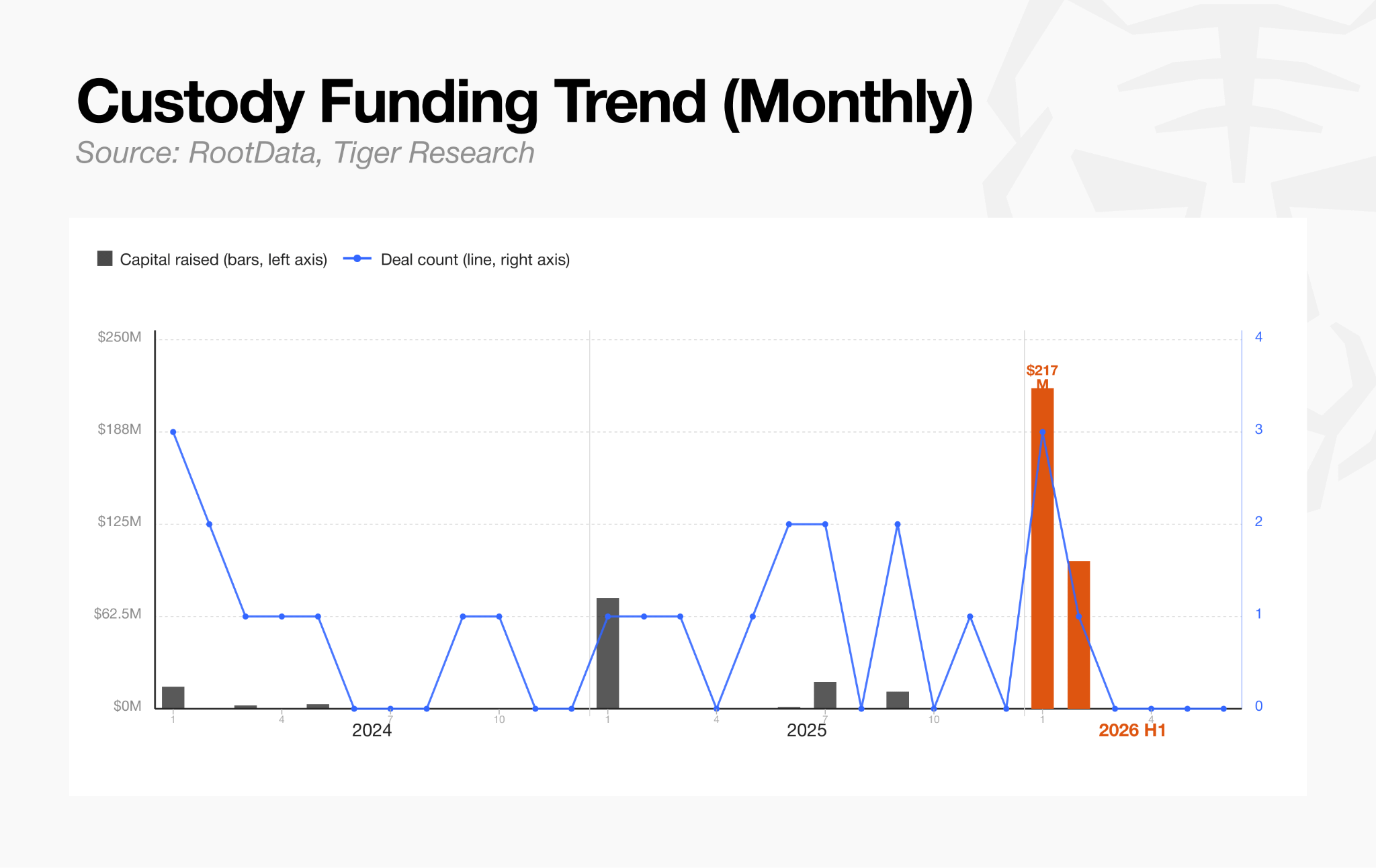

5.6. Custody: Quiet but Powerful

The custody sector grew fifteenfold, from $20.4 million in 2024 to $317.1 million in the first half of 2026. In the first half of 2026, Anchorage raised a $100 million strategic investment, meaning Anchorage alone accounted for roughly a third of all sector investment during that period.

For institutional asset managers to hold crypto directly, custody infrastructure that meets regulatory requirements is essential. This sector grew alongside rising institutional demand for asset management and crypto custody services.

The sectors discussed above share one common thread: each has kept a stable base of capital flow through the funding rounds described here, and in every case, that infrastructure demand was created by institutions’ need to enter the market.

6. A New Standard for Crypto Capital: From Betting to Control

Overall, the center of gravity in crypto investment has shifted from planting short-term seeds to owning a stake in infrastructure and protocols.

Before bitcoin ETF approval and the improved regulatory environment of 2024, the crypto market was a realm of indiscriminate betting, dominated by small, narrative-driven investments spread across many projects. That strategy ultimately led to the collapse of the gaming and NFT sectors and the elimination of the VCs that kept pursuing it.

Today’s capital, by contrast, aims not at short-term bets but at gaining long-term control over both its investment targets and on-chain infrastructure. It concentrates large sums in a small number of targets that have secured auditable revenue structures and regulatory licenses, or it acquires equity outright to control the infrastructure itself.

In the past, an investment in an early-stage project functioned as a signal a VC sent to the market. The act of investing was read as smart money moving in, which lifted token prices or drew retail users to participate early. Today’s structural capital, which acquires infrastructure directly and secures licenses, sends no such signal for retail to follow.

Retail investors no longer react strongly to news of VC investment, fundamentally because market capital itself has undergone this structural change. Retail investors, too, now need to weigh potential investments with the same caution VCs now apply. The old betting strategy no longer serves either retail investors or VCs.

About RootData

RootData is a Web3 asset data platform launched in early 2022 that provides a systematic investment and funding database for crypto investors and founders. It now processes more than 3.4 million search queries a month and is used by more than 2 million crypto users. RootData’s data and research have been cited by major media outlets and institutions, including The Wall Street Journal, Cointelegraph, Binance Research, and The Block. The platform structures the information investors need for decision-making, from discovering crypto projects to tracking funding and profiling investors.

🐯 More from Tiger Research

Read more reports related to this research.DeFi Lending Is Modularizing: The Risk Management War Among Morpho, Euler, and Aave

Still 1990: Crypto Cards: $1.5 Billion a Month, but Not Yet Infrastructure

Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.