Much of the attention remains fixed on stablecoin issuance, but the greater opportunity lies beyond it. Together with EastPoint, we analyzed the key opportunities across the five-stage value chain: on-ramp, transfer, payment, and yield.

Key Takeaways

Beyond the limits of an issuance market where Tether and Circle hold an oligopoly, this report analyzes the actual business structures that arise across the value chain’s five stages, including on-ramp, remittance, payment, and yield generation.

Rather than “building the system anew,” the mainstream strategy, as with Stripe’s acquisition of Bridge, layers stablecoin efficiency (instant settlement, low-cost remittance) onto already-established traditional financial infrastructure. Yield generation, however, is an area traditional finance has difficulty accessing, and requires separate expertise.

As rate cuts reduce the appeal of issuance revenue and competition intensifies, the market’s value is shifting toward the “underlying settlement layer.” Rather than replacing traditional finance, stablecoins show a pattern of vertical integration with the regulated financial system.

1. Time to View the Full Stablecoin Value Chain

Discussion of the stablecoin industry has so far been concentrated on the issuance stage. The performance of major issuers such as Tether and Circle, along with regulatory responses by country, has been treated as the market’s key indicator, but this is only the starting point of the stablecoin value chain.

The stablecoin industry’s full value chain includes the economic “flow” through which tokens circulate after issuance. It is defined as a five-stage value chain: issuance, followed by on-ramp, transfer, payment, and yield generation.

Analyzing the industry from this value chain perspective makes clear that while the issuance market has an oligopoly structure held by a small number of players, the downstream layers that follow it involve a larger number of competitors creating market opportunities.

2. Issuance to Yield: Tracking $1,000

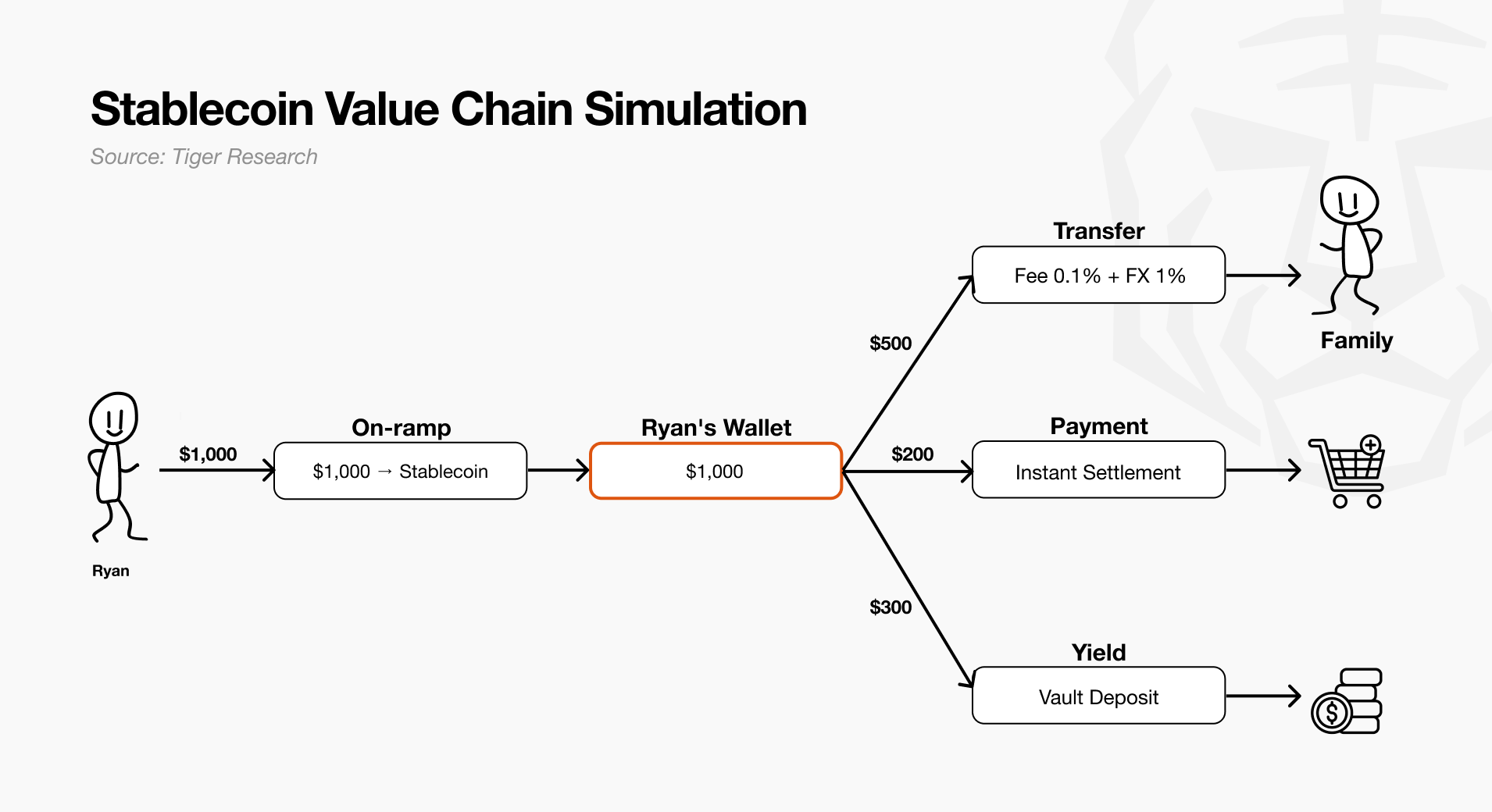

Consider how the $1,000 in Ryan’s bank account circulates through the stablecoin ecosystem. Understanding this requires examining the five-stage value chain in order, from issuance to yield generation.

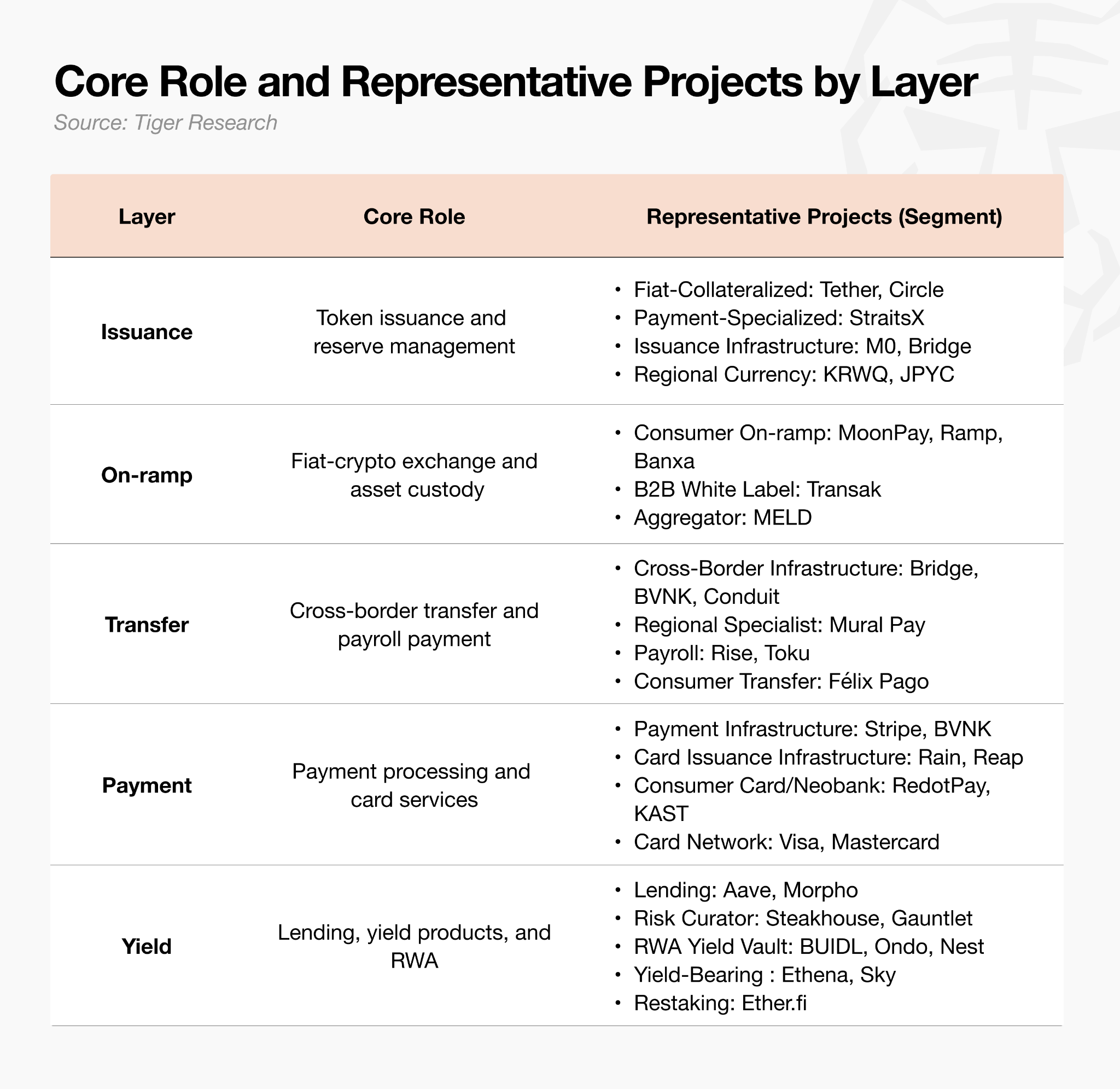

Issuance: Major issuers mint stablecoins backed by collateral such as U.S. Treasuries, supplying the market with sufficient liquidity.

On-ramp: When Ryan requests conversion of his $1,000 into stablecoins through an on-ramp service, the on-ramp provider processes the request and sends the tokens to his wallet. At this point, the asset exits the fiat currency system and converts into on-chain liquidity.

Transfer: Ryan sends $500 to family in Mexico to cover living expenses. The transfer infrastructure processes this instantly, and the recipient converts the funds into local currency to spend.

Payment: Ryan then uses the remaining $200 to pay at a grocery store. Here, the payment infrastructure carries out settlement instantly.

Yield: The final $300 remaining in his wallet is not left idle. Instead, it is deposited into a yield protocol’s vault, where it is managed as a financial asset that generates returns.

Through this process, Ryan’s $1,000 converted from fiat currency into stablecoins and evolved into a cross-border means of payment and asset management. Every layer through which Ryan’s funds moved corresponds precisely to the stablecoin industry’s value chain.

2.1. Issuance

The issuance market is an economies-of-scale market, with barriers to entry built on trust and liquidity. Established first-mover issuers, Tether and Circle, hold an oligopoly, and later entrants require a differentiation strategy that moves beyond the reserve-interest model.

1) Industry Structure

Stablecoin issuance is the process of minting and burning tokens against reserves, primarily U.S. Treasuries, to fix their value. The total market is approximately $300 billion, of which dollar-pegged assets account for 99.99%. Tether and Circle together hold roughly 83% of the market, and an economies-of-scale dynamic has become entrenched in which deeper liquidity increases both trading convenience and trust.

As the industry matures, functions once monopolized by a single issuer are undergoing specialization and unbundling. An issuer may appear to be a single entity on the surface, but internally, four functions, licensing (regulatory qualification), reserve management and custody, token minting and burning, and distribution, are divided among separate parties. Through this process, issuers are distributing much of their actual operational responsibility.

Circle, for example, delegates a substantial share of distribution to Coinbase, and Tether entrusts much of its reserves to the custodian Cantor Fitzgerald.

2) Business Model Types

Reserve Interest: Revenue comes primarily from returns on reserve management, an advantage for leading issuers with large liquidity pools (Tether, Circle).

Payment Fee: Revenue comes from fees generated when the token is used for payment and settlement. Profitability is determined by transaction velocity rather than market cap (StraitsX).

Issuance-as-a-Service: Instead of issuing tokens directly, providers lease infrastructure and licenses and collect a spread. Growth comes through network effects rather than scale (M0, Paxos, Bridge).

Regional: Providers secure exclusive liquidity by moving first into regions without clear regulation or into non-dollar currency markets (KRWQ, JPYC).

3) Case Study: Circle

When institutional clients deposit dollars into Circle Mint, Circle’s on-ramp and off-ramp platform, Circle mints USDC at a 1:1 ratio. Because Circle’s primary revenue comes from interest earned on these deposits, it charges no separate minting fee at issuance, and the core of its operation is maximizing the size of this interest-free float. The deposited dollars are held in the Circle Reserve Fund, an SEC-registered money market fund managed by BlackRock, along with cash and cash equivalents, and are invested primarily in short-term U.S. Treasuries.

Circle distributes this interest income through agreements with its distribution channels. Under the Collaboration Agreement signed in August 2023, Circle and Coinbase split interest earned on USDC reserves as follows:

USDC held on Coinbase’s platform: Coinbase receives 100% of the interest income generated on the corresponding reserves.

USDC held on Circle’s own platform: Circle keeps 100% of the interest income generated on the corresponding reserves.

USDC held outside both platforms (residual interest income): interest earned on reserves backing USDC that circulates outside both platforms, including third-party exchanges, individual and institutional wallets, and DeFi, is split 50:50 between Circle and Coinbase.

This reflects a deliberate strategy. By carefully structuring on-platform and off-platform incentives with its core distribution partner, Circle shares part of its issuance revenue in exchange for maximizing USDC’s distribution base and share of the ecosystem.

4) Key Implications

Stablecoin issuance is an economies-of-scale market where the advantages of having entered early and the scale of available liquidity are decisive, making entry barriers extremely high for latecomers pursuing a direct issuance model. New entrants should therefore focus on the value chain’s functional unbundling rather than becoming fixated on issuance itself.

A more effective strategy is to build unmatched expertise in a specific layer of the value chain, such as licensing, asset custody, settlement infrastructure, or distribution channels, and establish a position as irreplaceable middleware that other players cannot substitute. The nature of future competition, in other words, will come down not to who issues the largest volume of stablecoins, but to which players capture value within the full flow through which stablecoins move and are consumed, and secure a strategic position there.

2.2. On-ramp

On-ramp revenue comes from fees and spreads charged on transaction volume. The fee a consumer actually experiences varies widely by payment method, running 2-4% for bank transfers and 4-7% for cards, but the net take rate providers actually capture is approximately 3%, based on Banxa’s figures. The conversion function itself is difficult to differentiate, and competition is intense enough that aggregators exist to route transactions to the lowest-cost option.

1) Industry Structure

This layer consists of on-ramp services, which exchange fiat currency for tokens, and wallets and custody providers, which hold the resulting assets. The two are closely linked, since one handles conversion into stablecoins and the other handles their storage.

On-ramp revenue comes from fees and spreads tied to transaction volume, and margins vary considerably by payment method. The conversion function itself, however, is difficult to differentiate, so multiple providers compete with largely similar offerings, and net take rates are converging around 3%.

2) Business Model Types

Consumer On-ramp: Provides currency conversion directly to end users and collects transaction fees and spreads. Since differentiation is difficult, competitiveness comes down to license coverage, the breadth of payment networks, and reputation, reflected in conversion rates (MoonPay, Ramp Network, Banxa).

B2B White Label: Embeds on-ramp rails into wallets and apps and shares a per-transaction fee, approximately 1%, with partners. This secures distribution without a consumer-facing brand, and the deeper the integration with a large partner, the more switching costs function as a moat (Transak).

Aggregator: Routes transactions across multiple on-ramps to find the optimal path and earns an intermediation fee. Its value grows as the number of individual on-ramps increases, although dependence on its partner network is also a limitation (MELD).

3) Case Study: MoonPay

MoonPay is a non-custodial on-ramp platform where users buy tokens with fiat currency and have them sent directly to their wallet. Its primary revenue comes from per-transaction fees and trading spreads, which range from 1% for bank transfers to 4.5% for cards, with a minimum of $3.99 on small transactions. The published fee structure is organized into three tiers, which reflect how MoonPay allocates revenue and structures distribution.

MoonPay’s revenue structure splits into two channels: direct traffic and embedded transactions through partners. Its model of embedding the solution into more than 500 wallets and apps, in particular, lets partners set their own rates and functions as the core driver behind MoonPay’s ability to secure large-scale distribution efficiently while sharing revenue with those partners.

4) Key Implications

Fee revenue from simple on-ramp services faces severe margin pressure as the service becomes commoditized and price competition intensifies. Building a sustainable business therefore requires converting a one-time fee structure into steady, recurring revenue.

Consumer on-ramp providers are accordingly expanding into downstream layers of the value chain, such as issuance and settlement infrastructure. MoonPay’s acquisition of Iron and its move into branded issuance services are examples of this shift, though the financial results of this recurring-revenue strategy have yet to be verified.

The “embedded” strategy, in which providers integrate their services into a larger platform, has produced two distinct outcomes. Some providers build independent competitive strength and remain a standalone moat (Transak, Turnkey), while others are acquired by larger payment and custody companies, as with Privy’s acquisition by Stripe and Dynamic’s acquisition by Fireblocks.

It is too early to determine which outcome will become the dominant pattern, but the on-ramp and wallet layer clearly plays a pivotal role within the industry.

2.3. Transfer

Transfer is the layer responsible for the movement of stablecoins. It includes transfers by individuals and businesses, as well as payroll payments to global workforces.

This segment draws attention because it demonstrates stablecoins’ cost advantage in its most concrete and measurable form. Traditional cross-border transfers cost an average of more than 6%, while using stablecoins substantially reduces that cost.

1) Industry Structure

Fees and FX spreads arise at both ends of the process, converting dollars into tokens and tokens back into local currency, but the on-chain movement of the tokens themselves is effectively free.

Revenue, in other words, is concentrated not in the transfer itself but in the conversion at both ends and in the licensing required to process transfers legally. Because obtaining a Money Transmitter License (MTL) in individual U.S. states takes 12 to 24 months, leasing the license itself as infrastructure, a “compliance-as-infrastructure” model, has become a powerful revenue model.

2) Business Model Types

Cross-Border B2B Infrastructure: Orchestrates cross-border payments and settlement between businesses, typically earning a transfer fee (on the order of 5–10 bps) plus an FX spread (tens of bps up to around 1%, depending on corridor and volume). Some go further and issue their own stablecoins to capture reserve interest income as well, as with Bridge’s Open Issuance (Bridge, BVNK, Conduit).

Payroll: Specializes in salary payments and owns the end relationship with both workers and employers. On top of SaaS subscription fees (a flat monthly rate per contractor, with off-ramp fees of about 25 basis points), this model layers a second revenue stream by investing float, funds awaiting payroll disbursement, and capturing the interest, as with Rise Earn (Rise, Toku).

Consumer Transfer: A model that specializes in person-to-person cross-border transfers, uses stablecoins to lower backend costs, and expands its own margin by maintaining a flat fee cheaper than legacy providers (Félix Pago).

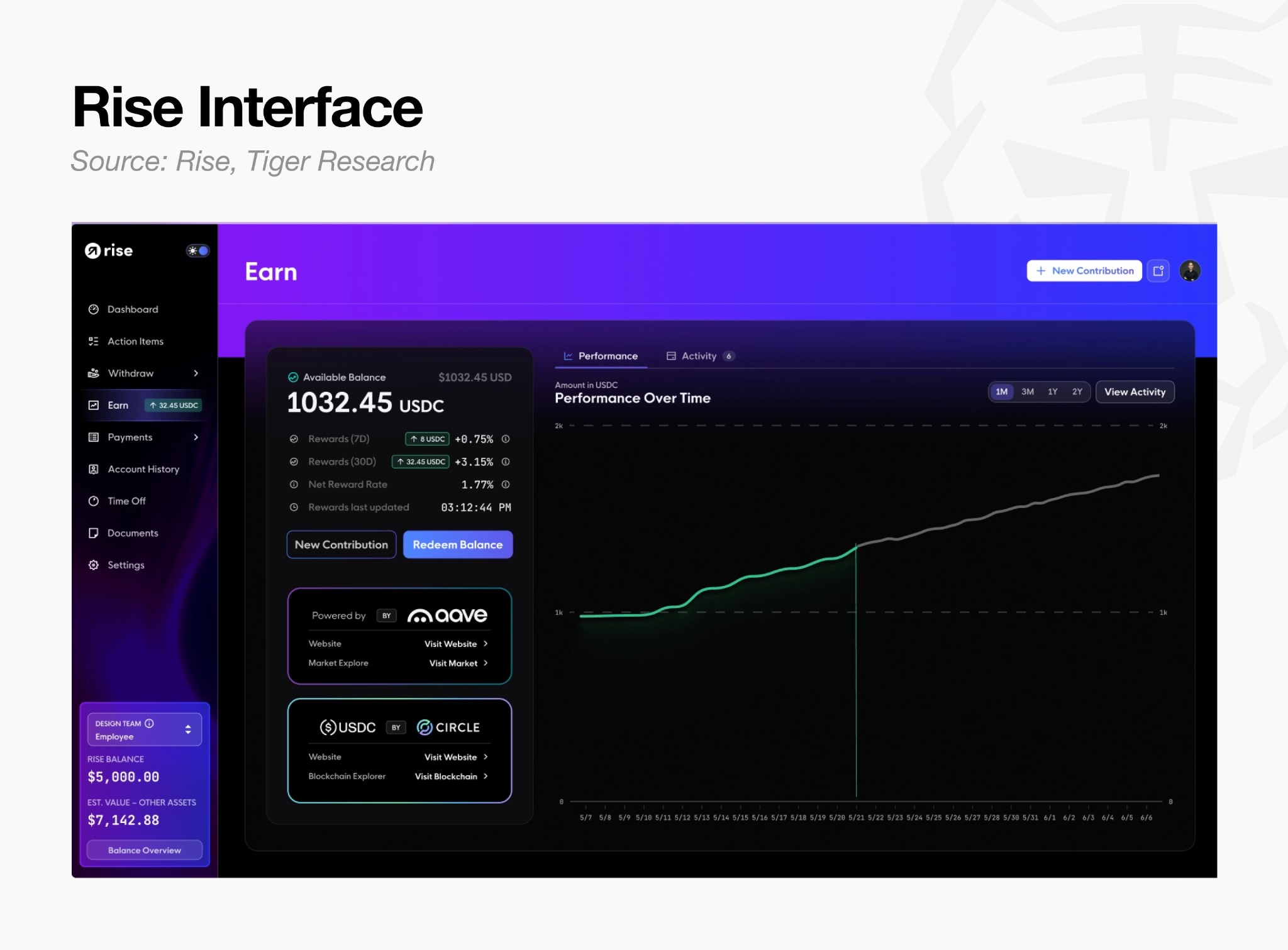

3) Case Study: Rise

Rise is a stablecoin payroll platform through which companies pay wages in either fiat currency (USD) or USDC. Workers select their own payout method each pay cycle from more than 90 local currencies and stablecoins, and more than half of recent withdrawals, out of a cumulative $1.5 billion processed, have been made in stablecoins. What Rise actually charges for, however, is not token transfer but management of the employment relationship. The platform automates KYC and AML screening, generates country-specific contracts, and issues tax documents, and charges recurring fees for this service.

Rise’s revenue builds in three layers that follow the flow of payroll funds.

Subscription and Transaction Fees: Employers choose between a flat $50 monthly subscription per contractor or 3% of the payment amount, plus a $2.50 transfer fee per transaction. Because payroll recurs by nature, this revenue is recurring rather than one-time.

Assumption of Legal Liability (EOR/AOR): A premium offering in which Rise itself becomes the legal contracting party and absorbs the risk of worker misclassification. Employer of Record (EOR) service costs $399 per worker per month. The eightfold price gap versus simple payment processing comes from compliance liability, not the transfer function.

Float Management (Rise Earn): Rise invests funds companies have set aside before payroll disbursement, as well as USDC balances workers have not yet withdrawn after receiving payment, in Aave lending pools on Arbitrum. It charges no deposit or custody fee and instead takes a 1% commission on the interest generated, collected at the time of withdrawal (launched March 2026).

Because payroll is a cash flow that recurs every month without exception, balances naturally accumulate on the platform both before disbursement and after workers receive but don’t withdraw their funds. Rise’s three-layer structure monetizes exactly this characteristic. In an environment where on-chain transfer is effectively free, this can be read as a deliberate strategy of expanding the charging point sequentially, from the employment relationship (subscription) to legal liability (EOR) to idle funds (yield), rather than charging for movement itself.

4) Key Implications

The winner in the transfer market will not simply be the provider that moves tokens most cheaply. It will be a comprehensive player that secures conversion and licensing at both ends (Mural Pay, Yellow Card) to control the customer touchpoint, owns the substantive customer relationship through payroll (Rise), and layers yield income (Rise Earn) on top of that.

The eventual acquisition of cross-border infrastructure provider BVNK by the card network Mastercard, for up to $1.8 billion, illustrates that the settlement infrastructure underlying the transfer and payment layers will converge into one.

2.4. Payment

Payment is the value chain’s core layer, where stablecoins settle payment for goods and services. Merchant payments and card services are leading this segment, but the economic reality remains immature relative to market expectations. On-chain stablecoins’ retail velocity remains at only about one-twentieth of M1, a measure of the money supply, because users load funds and spend them intermittently rather than following the routine financial cycle in which payroll receipt and regular spending are interlocked.

1) Industry Structure

Interchange, the fee card networks and issuers collect on each transaction, is the core source of payment revenue and scales with payment volume. Low turnover, however, keeps per-card profitability weak, and what revenue exists is split among the card network, the issuing bank, and the payment gateway (PG). The real profit pool therefore sits not with the consumer-facing card brand but with the card issuance and settlement infrastructure behind it.

Most consumer card providers lack their own issuance authority and depend on this infrastructure, leaving them with a limited revenue structure built mainly on swap spreads.

2) Business Model Types

Payment Infrastructure: Orchestrates merchant payment and settlement. Beyond payment fees, providers capture reserve interest income by issuing their own stablecoins. Stripe’s Bridge Open Issuance, which distributes to businesses the same reserve revenue structure Circle has captured, is one of the most profitable businesses in this layer (Stripe, BVNK).

Card Issuance Infrastructure: The backend that supports corporate card issuance. Providers receive a share of interchange fees through principal membership in major networks such as Visa, and generate revenue through program management and FX spreads. The core point of differentiation is USDC-based T+0 on-chain settlement, which cuts collateral requirements by up to 60% compared to existing methods and substantially improves capital efficiency (Rain, Reap).

Consumer Card and Neobank: Provides cards and accounts to end users. Revenue combines a share of interchange and FX spreads with membership subscription fees or margin from managing deposited funds. Because these providers are not issuers themselves, their access to reserve interest is limited, and most depend on issuance infrastructure such as Rain or Reap (Cypher, KAST).

Card Network: The network for payment authorization and settlement. Interchange belongs to the issuer, while the card network benefits from rising transaction volume through a per-transaction network fee. Card networks are incorporating stablecoin settlement as a backend layer, which strengthens lock-in with partner banks (Visa, Mastercard).

3) Case Study: Rain

Rain is B2B backend infrastructure that helps wallets, exchanges, and neobanks issue their own branded consumer cards. Partners design card programs through a single API integration, and Rain, as a principal member of Visa and Mastercard, handles network sponsorship, compliance, and issuance and operations on their behalf.

When a user swipes a Rain-based card at a merchant, processing follows this sequence:

Authorization (real time): The payment is authorized on the Visa or Mastercard network just like any standard card. The experience for both merchant and consumer is identical to a conventional card, and stablecoins remain invisible on the surface.

Balance Deduction and Ledger Management: The user’s on-chain balance is converted and deducted in real time for the authorized amount, and Rain manages the ledger for the entire program.

Network Settlement (daily): Rain settles with the card networks entirely in USDC. Because settlement isn’t constrained by bank cutoff times, it occurs every day of the year, including weekends and holidays, so payment funds from weekends and holidays aren’t held up for days.

Fund Recovery and Working Capital: In a credit structure, user repayment arrives later than settlement, so the issuer has to fund that gap. Rain tokenizes card receivables and uses them as collateral for on-chain loans, raising settlement funds before it collects from users, with cumulative borrowing and repayment exceeding $175 million. As a result, its collateral requirement is up to 60% lower than that of traditional issuers.

In short, when a consumer uses a Rain-based card, Rain is the one handling everything behind the scenes, from authorization through settlement and funding.

4) Key Implications

The core of payment revenue is not the visible card payment fee but the reserve interest that comes with issuer status and the capital efficiency gained through T+0 settlement. Most consumer card brands are merely the front-end customer touchpoint layered on top of this infrastructure.

Major card networks have moved to directly acquire cross-border payment infrastructure such as BVNK, while Visa, Mastercard, Stripe, and Google are pursuing a joint stablecoin coalition, Open USD. This reads as a vertical integration strategy, bringing the platform in-house to defend their exclusive reserve interest income.

2.5. Yield

Yield is the value chain’s endpoint, and the layer where the most sophisticated business structures form. The interest that issuers are unable to pass on to holders ultimately returns to users here, and this lending business is evolving into a full asset management industry.

1) Industry Structure

Early on-chain lending combined all assets into a single large pool, so that a default in any one asset could spread as risk across the entire system. This structural limitation has since been addressed by the introduction of an isolated, or modular, model that keeps collateral and loan terms separate by market, clearly dividing the core infrastructure, the immutable lending protocol, from the yield-management layer, run by risk curators.

This structural separation gave rise to a genuine on-chain asset management industry. Risk curators, like traditional asset managers, earn performance fees, up to 50%, and management fees, up to 5% annually, on the vaults they run, and the top four players together control roughly 65% of total curating TVL, the total value locked across all vaults, giving this segment an oligopoly structure.

On top of this yield infrastructure sits a layer of financial products that end users actually consume, including real-world asset (RWA) products that tokenize U.S. Treasuries and private credit, interest-bearing synthetic dollars, and restaking.

2) Business Model Types

Lending Infrastructure: Captures a portion of the interest spread between deposits and loans, the Reserve Factor, or takes protocol revenue from interest generated by issuing its own stablecoin, such as Aave’s GHO. A different model, exemplified by Morpho, turns off its own protocol fee and instead redirects that value to downstream curators and the token ecosystem to grow the network (Aave, Morpho).

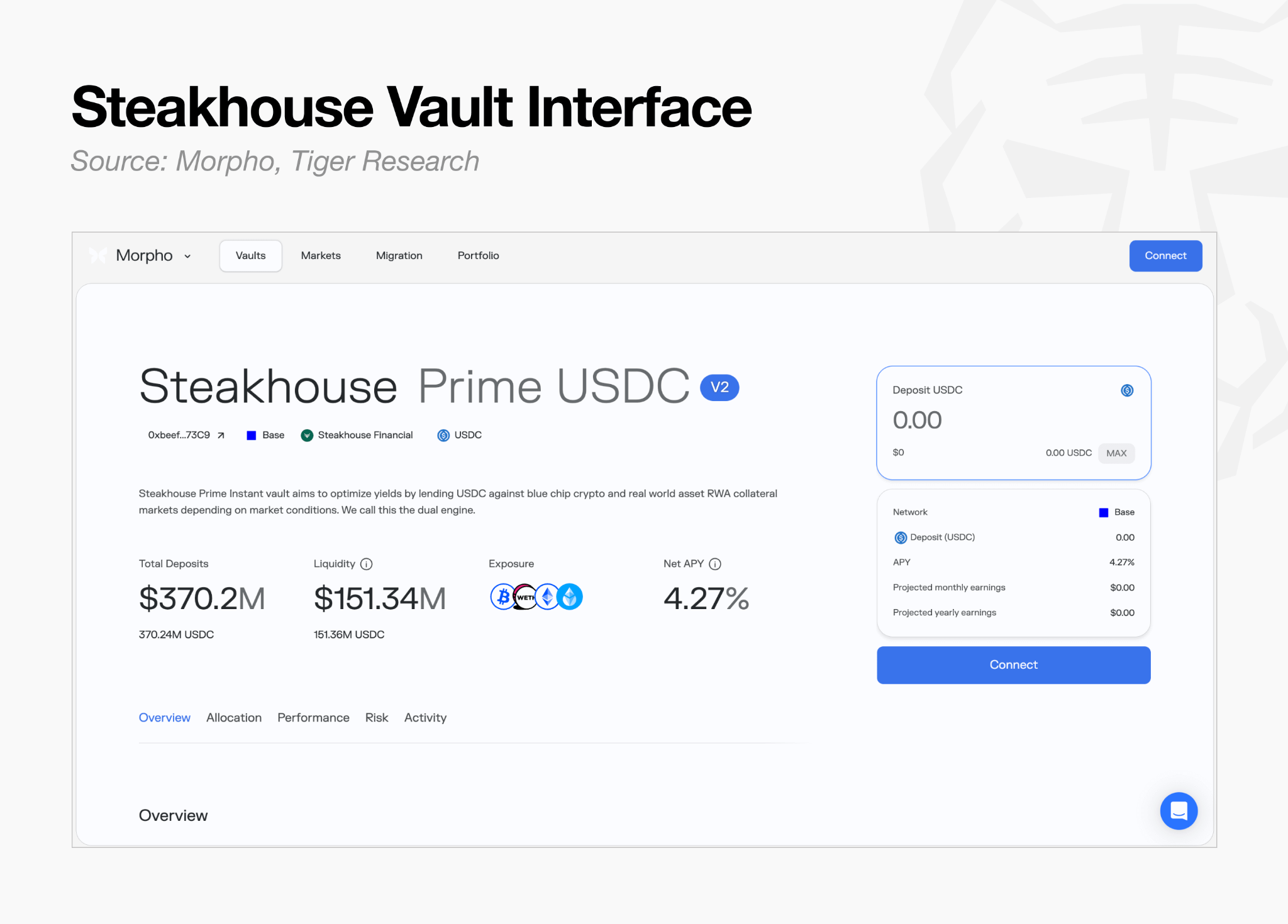

Risk Curator: Designs asset allocation and risk models on top of lending protocols and collects a vault management fee. Steakhouse, for example, manages approximately $1.7 billion in assets with a team of fewer than 20 people and takes about 5% of the interest generated. It exemplifies the on-chain asset manager, an operating model whose cost structure is far more efficient than that of traditional financial institutions (Steakhouse, Gauntlet).

RWA Yield Vault: Issues and distributes tokenized U.S. Treasuries or money market funds (MMFs) and earns a management fee of roughly 0.15% to 0.5% annually. BlackRock’s BUIDL serves as the underlying asset, Ondo Finance repackages it for the decentralized finance (DeFi) ecosystem, and Plume Nest distributes it through a Layer 1 blockchain built specifically for RWAs (BUIDL, Ondo, Nest).

Interest-Bearing and Synthetic Dollar: Generates returns through delta-neutral basis trades or a managed-rate net interest margin (NIM), then pays that return to token holders as interest. This category divides into two types, models that rely on crypto-native derivatives yield and models that rely on stable Treasury collateral (Ethena, Sky).

Restaking: Makes already-staked assets liquid again, a process known as restaking, to capture additional yield. Some providers take this further, vertically integrating across the value chain, from collecting DeFi vault management fees to linking directly with consumer card payments (Ether.fi).

3) Case Study: Steakhouse

Steakhouse Financial is a risk curator, a type of on-chain asset manager. Rather than building its own lending protocol, it operates on top of existing infrastructure such as Morpho, taking on a sub-advisory role: selecting collateral assets, designing risk parameters such as loan-to-value ratios, and allocating capital across markets.

Its revenue structure also resembles traditional asset management, collecting a portion of the interest generated as performance and management fees. Because lending protocols such as Morpho handle the operational infrastructure, accounting, settlement, and custody, curators can scale their operations efficiently on risk-design expertise alone, without bearing separate infrastructure costs.

4) Key Implications

The assets currently managed by on-chain curators, approximately $7 billion, amount to roughly one twenty-thousandth of the global traditional asset management market, approximately $147 trillion. This wide gap represents a long runway for the on-chain asset management market to expand.

High yields, however, only matter if the underlying system remains stable. Several recent depegging incidents and a chain of shocks across the restaking sector have exposed operational risks and tail risk, extreme scenarios that fall outside normal expectations, which simple smart contract audits alone cannot detect.

Capital in the market is therefore shifting from high-yield synthetic dollars to Treasury-collateralized products with comparatively lower returns, because what institutional investors fundamentally want is not a high annual percentage yield (APY) but predictability, the ability to control risk.

3. Where the Stablecoin Value Chain Is Headed

Success in the stablecoin market depends not on scaling issuance alone, but on which player controls a specific customer segment. Building infrastructure from scratch in a crypto-native way, however, is slow and carries a heavy cost burden.

The most realistic and executable strategy is to layer stablecoin efficiencies, such as same-day settlement, 24/7 operation, low-cost transfers, and programmable yield, onto already-established traditional financial infrastructure (rails). Recent major M&A activity, including Stripe’s acquisition of Bridge and Mastercard’s partnership with BVNK, all point toward this combination of traditional financial infrastructure and stablecoin efficiency.

This opportunity is being amplified by two broad trends working together: the spread of regional currencies and convergence with regulated finance.

Spread of Regional Currencies: Governments and institutions preparing stablecoins denominated in their own currencies are more likely to adopt already-proven issuance infrastructure and local banking corridors than to build a system from the ground up.

Convergence with Regulated Finance: Regulated financial institutions such as JPMorgan, Visa, and BlackRock also show a clear preference for proven infrastructure over developing their own technology.

As a result of these trends, the market opportunity in card issuance and settlement, custody infrastructure, and asset management, the gateway institutional finance must pass through to enter the market, is set to expand further going forward.

This is because stablecoins function essentially as money and serve as a powerful “technological upgrade” that maximizes the efficiency of existing financial rails.

The issuance market is an oligopoly that requires substantial capital and trust, while the layers that follow issuance, including on-ramps, payments, and asset management, carry comparatively low barriers to entry, allowing a much broader range of business models to emerge.

Because this market is still at an early stage where integration with traditional financial rails is just beginning, the players that come to dominate it will be determined by what form of integration and replacement they lead.

This shift has become an unavoidable, large-scale challenge of the era. EastPoint: Seoul 2026, taking place on September 28, will serve as a forum for an in-depth discussion of this industry-wide shift. With traditional financial institutions and the digital asset industry gathering under one roof to cover the stablecoin ecosystem and beyond, the event is positioned as a substantive first step toward genuine convergence across existing boundaries.

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.