News of a U.S. strategic Bitcoin reserve has been circulating for nearly two years. The original BITCOIN Act, introduced in 2024, centered on active government purchases. ARMA contains no such provision. Whether the market should treat this as positive news is an open question.

Key Takeaways

The executive order Trump signed in March 2025 was a commitment not to sell the bitcoin the federal government already holds. It was not a purchase mandate. The market had expected something more, and when the order was announced, the bitcoin price fell 5.7% immediately.

The legislative effort that began in 2024 has retreated substantially over two years, from a bill requiring the purchase of one million BTC to a custody bill that contains no purchase obligation at all.

The American Retirement and Monetary Advancement Act (ARMA), the bill with the strongest current prospects for passage, is not a purchase bill. It prohibits the government from selling the bitcoin it already holds for at least twenty years.

ARMA is unlikely to have a material short-term effect on the bitcoin market. Over the longer term, however, establishing bitcoin’s legal status as a national reserve asset could reopen the debate over mandatory purchases, which would be a positive for the market.

1. Background: What the U.S. Has and Has Not Done

Throughout the 2024 presidential campaign, Trump repeatedly promised a bitcoin strategic reserve. Markets read this as a signal that the federal government would become a direct buyer.

After the election, on March 6, 2025, Trump signed an executive order designating bitcoin seized through criminal investigations and civil forfeitures as a strategic reserve and directing that it be held permanently. The order contained no instruction to acquire new bitcoin. It was a pledge not to sell what the government already owned. The price fell from roughly $92,000 to below $85,000 when the order’s contents became clear.

At the time of signing, the federal government held approximately 190,000 BTC, equal to about 0.9% of the total supply of 21 million. Every coin in that holding had been accumulated through criminal and civil proceedings. Not a single bitcoin was purchased.

The position today remains unchanged. Beyond the executive order, nothing has been codified into law.

2. Legislative History

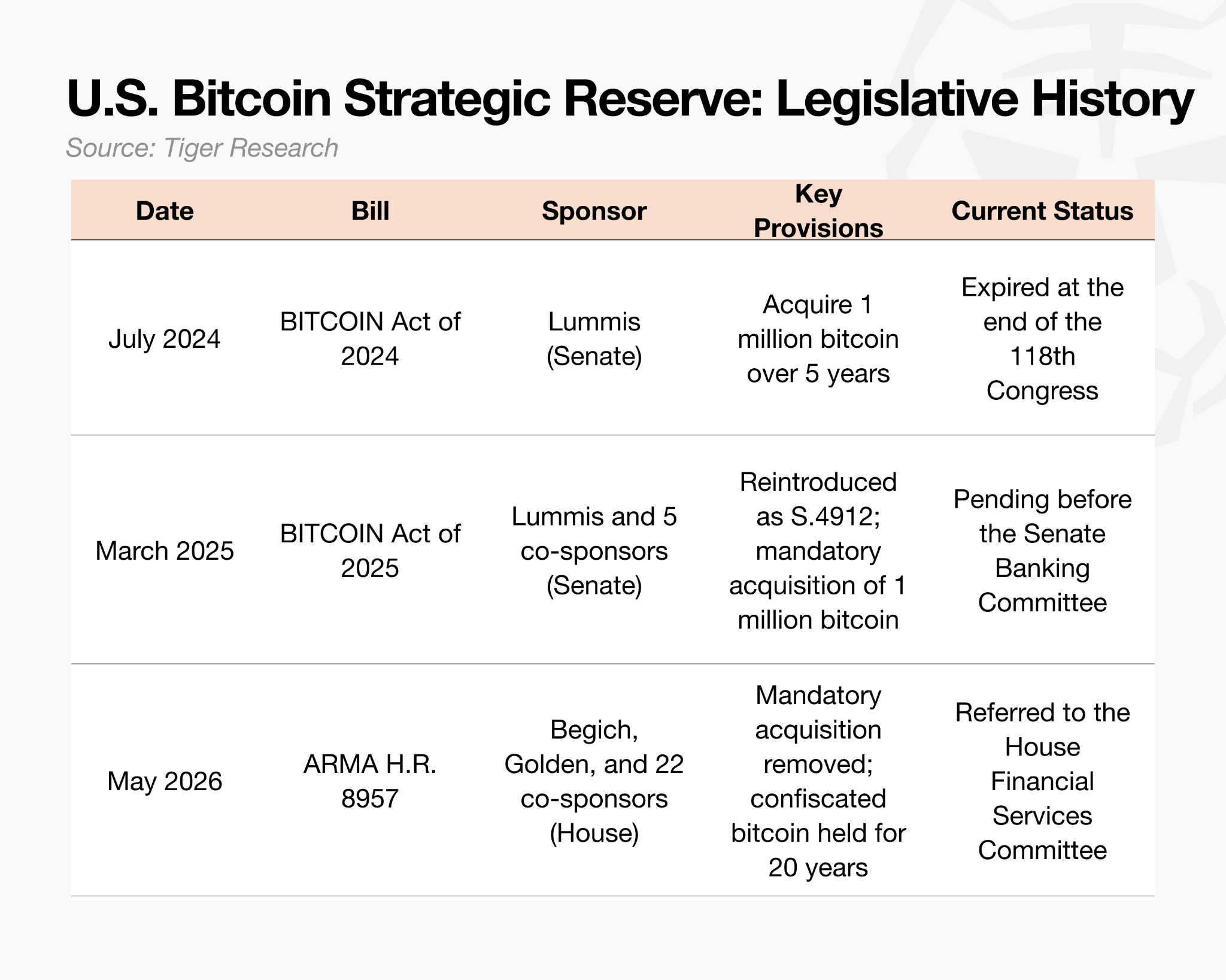

Discussions that began in 2021 produced the first concrete bill in 2024, which was reintroduced in 2025 and then restructured as ARMA in 2026. The through-line in that progression is a pattern of accommodation to political reality: mandatory purchase volumes were maintained, then eliminated. Each revision made passage more plausible but reduced the market impact.

2.1. 2024: The Original Bill

Senator Lummis had been publicly calling for bitcoin to be incorporated into federal reserves since she entered the Senate in 2021. At the time there was no consensus within Congress for such a step, and the crypto winter of 2022 and 2023 together with the collapse of FTX made the environment more hostile still.

The mood shifted in 2024, when bitcoin crossed $100,000 and spot ETFs received regulatory approval. In July of that year, Lummis introduced the first specific legislation: a bill requiring the purchase of one million bitcoin over five years, to be held for at least twenty years, funded from Federal Reserve surplus accounts.

One million BTC represents 4.76% of total supply and exceeds Strategy’s reported holdings of approximately 840,000 BTC. The bill died automatically when that congressional session ended.

2.2. 2025: Reintroduction and Stalled Progress

In March 2025, the same month as the executive order, Lummis reintroduced the BITCOIN Act as Senate Bill 954. The core structure was unchanged: purchase 200,000 BTC annually for five years to accumulate one million, with a twenty-year holding requirement. The revised version removed certain exemptions from the disposal ban, tightening the hold obligation, and added four co-sponsors.

Market reaction was broadly positive, but the bill faced substantial headwinds on three fronts.

First, the fiscal cost. One million bitcoin at prevailing prices represents hundreds of trillions of won. Fiscal conservatives within the Republican Party argued that gold is a stable store of value whereas bitcoin is a speculative asset, and opposed any mandatory purchase structure on those grounds.

Second, dollar hegemony. Led by Representative Maxine Waters, Democratic critics argued that treating bitcoin as a reserve asset would effectively undermine the dollar’s status as the global reserve currency.

Third, the Treasury Secretary’s position. In August 2025, Secretary Bessent stated publicly that the administration would not pursue additional bitcoin purchases. The official who would be responsible for executing the law had gone on record against it.

The bill has remained in committee in the Senate Banking Committee since.

2.3. 2026: ARMA as a Legislative Compromise

In May 2026, Representative Nick Begich introduced the American Retirement and Monetary Advancement Act (ARMA). Democratic Representative Jared Golden signed on as a co-sponsor. The change of name was itself strategic: it was designed to shed the associations that had made the earlier legislation difficult to advance and to widen the coalition of supporters.

ARMA does two things. It consolidates all bitcoin currently held or seized by the federal government into a single reserve under Treasury administration, and it prohibits the sale of that bitcoin for at least twenty years. The only permissible exception to the disposal ban is the retirement of national debt.

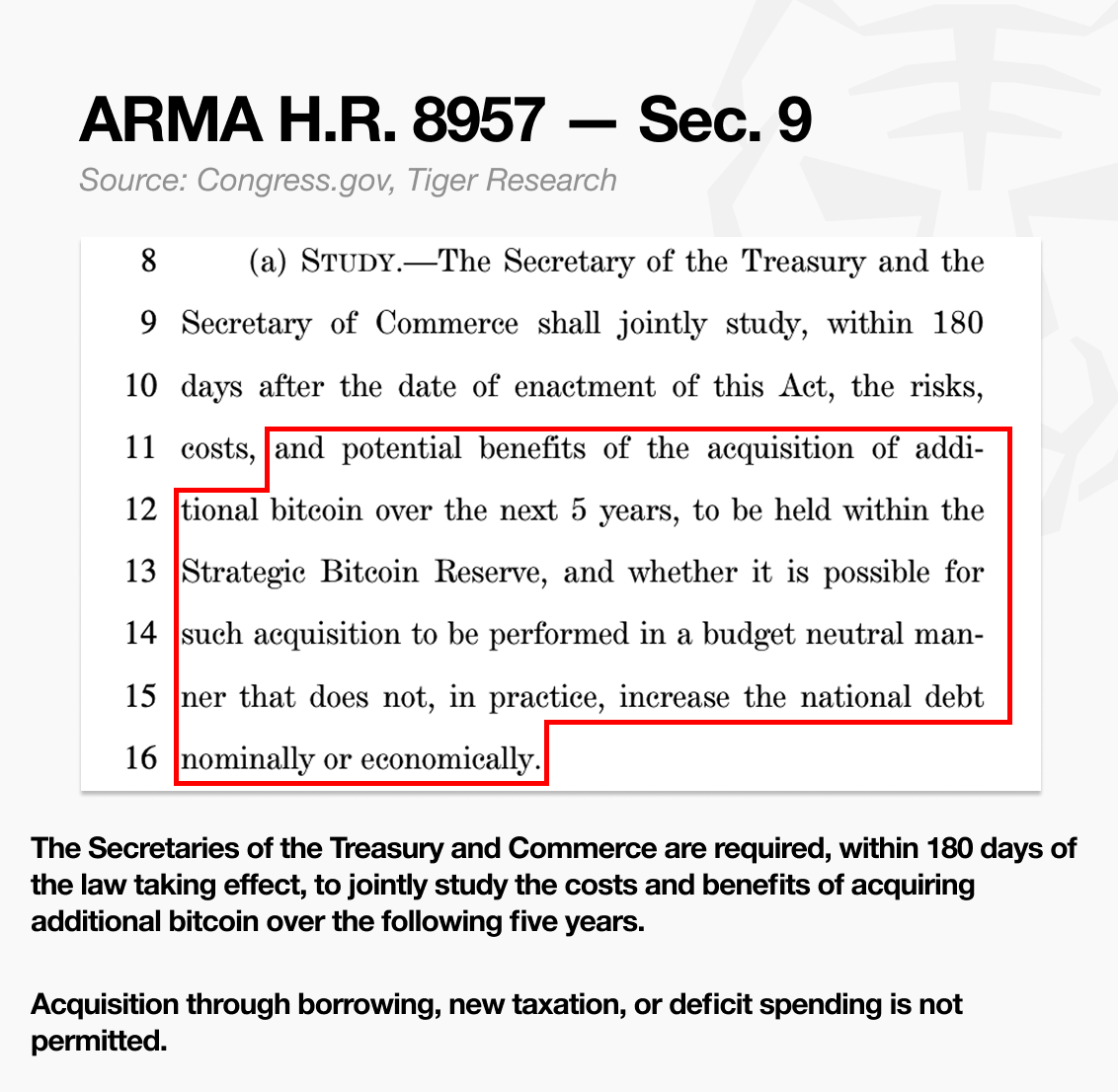

The decisive difference from its predecessor is what ARMA does not contain. The BITCOIN Act imposed an obligation to purchase 200,000 BTC per year. ARMA removes that obligation entirely. In its place, it instructs the Treasury and the Commerce Department to study and report within 180 days on whether additional purchases could be achieved in a budget-neutral manner. A study mandate is not a purchase mandate.

ARMA is, in substance, a custody and holding bill rather than an acquisition bill. Its purpose is passage, and it is structured accordingly.

3. Near-Term Outlook: Limited Market Impact

Two bills are currently moving in parallel through Congress. The BITCOIN Act (S.954) is before the Senate Banking Committee; ARMA is in the House. Their objectives differ. The BITCOIN Act is an acquisition bill; ARMA is a custody bill.

ARMA has the higher probability of moving first. The BITCOIN Act has been held in committee for over a year, weighed down by its fiscal cost and its Republican-only sponsorship. ARMA carries Democratic support and imposes no purchase obligation, which removes the most common basis for opposition.

That said, ARMA’s passage would not itself constitute a near-term positive for the bitcoin market. If ARMA is enacted, the approximately 320,000 BTC currently held by the federal government would be legally prohibited from entering the market for at least two decades. The overhang from potential government selling would disappear. The problem is that without any purchase obligation, there is also no new demand. What markets have wanted is the government buying bitcoin directly; ARMA does not deliver that. Its practical effect is closer to elevating the March 2025 executive order to statutory status.

What matters is what could follow ARMA. Nick Begich has held bitcoin since 2013, and was one of the House co-sponsors of the BITCOIN Act in March 2025. He is on record supporting bitcoin as a strategic asset. The structure of ARMA suggests a sequenced approach rather than a single-step attempt: establish the legal framework first, then build the acquisition mandate on top of it.

If ARMA passes and bitcoin acquires a formal legal status as a national reserve asset, the debate over mandatory purchases is likely to resume on firmer ground. The pathway to that outcome is longer than markets had initially priced in when Trump made his campaign promises, but the direction has not changed.

In short, ARMA’s passage would have limited near-term price impact. Over the longer term, it remains a constructive factor for the market, and if ARMA passes, the probability of eventual purchase legislation becomes more visible.

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.