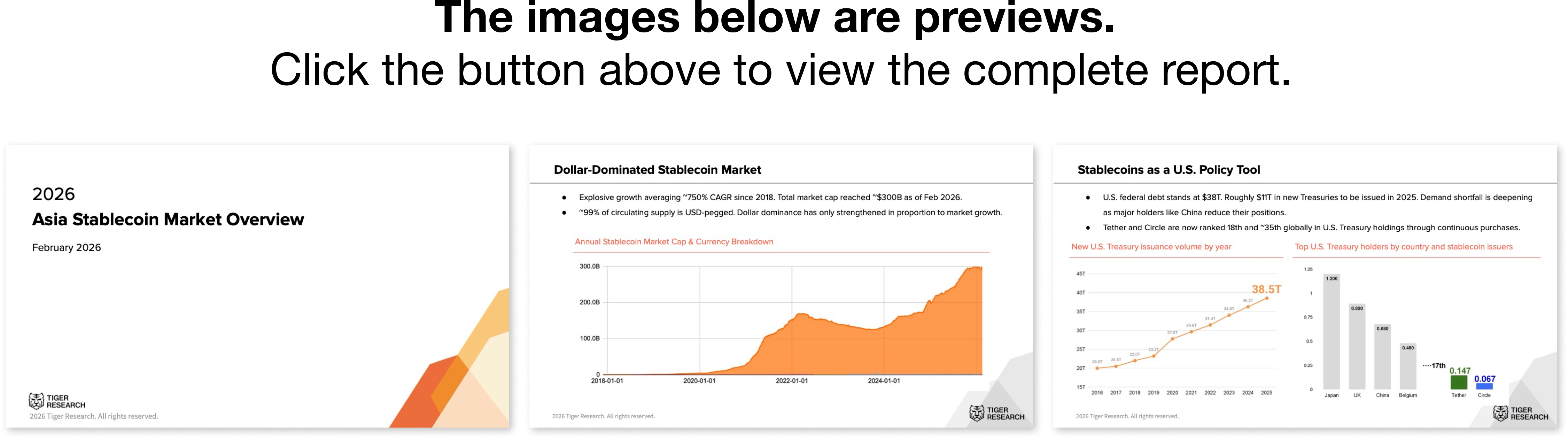

Every Asian nation is preparing for the stablecoin era. But the reality is that 99% of the market remains dominated by the dollar. How is each country navigating this challenge?

💡 We recommend reading the PDF report first for a foundational overview. For those seeking additional insights and context not covered in the report, please explore the detailed analysis below.

1. USD Dominance in the Stablecoin Market

The stablecoin market has grown rapidly. As of February 2026, total market capitalization stands at approximately $300 billion (rwa.xyz), reflecting an average annual growth rate of roughly 750% since 2018. Yet about 99% of this market is pegged to the U.S. dollar.

The market has expanded, but the dollar effectively monopolizes it.

Understanding this dominance requires looking at U.S. Treasury dynamics.

Stablecoin issuers do not simply vault deposited dollars. They invest reserves in safe assets such as short-term Treasuries and earn interest income. As the stablecoin market grows, so does the volume of Treasuries these issuers purchase. Today, stablecoin issuers collectively rank as the 17th-largest holder of U.S. government debt worldwide.

The U.S. has every reason to welcome this.

Geopolitical tensions have driven major holders like China to reduce their Treasury positions, while federal fiscal conditions have grown more strained. The U.S. government carries over $38 trillion in debt and needed to sell roughly $11 trillion in new Treasuries in 2025 alone.

If demand falls short, interest rates must rise, and rising rates push debt-servicing costs toward levels rivaling defense spending.

Against this backdrop, the U.S. enacted the GENIUS Act in July 2025, mandating that stablecoin reserves be held in U.S. Treasuries. Washington is actively shaping the stablecoin narrative.

For the U.S. government, dollar-pegged stablecoins serve not only as a new digital payment channel but also as a Treasury distribution mechanism and a policy tool for sustaining dollar hegemony.

2. Why Asia Is Issuing Local-Currency Stablecoins Anyway

For Asia, the dollar-dominated stablecoin structure carries the opposite implication. The more that local citizens and businesses use dollar-pegged stablecoins, the more domestic capital flows out of local financial systems and into the infrastructure of U.S. dollar hegemony.

The core issue is not technology. It is the fear of ceding monetary sovereignty. That anxiety is the most fundamental driver behind local-currency stablecoin issuance.

That said, stablecoins do offer clear technical advantages. They eliminate intermediaries, lower transaction costs, and operate around the clock regardless of banking hours. The gains are especially visible in cross-border payments, where transfers that once took days can settle in minutes. For trade-dependent Asian economies, this translates into real cost savings and speed improvements.

However, these same strengths are a double-edged sword. Once a local-currency stablecoin is placed on a blockchain, conversion paths to dollar stablecoins open simultaneously. Even if a won-denominated stablecoin exists, users can swap it into USDT with a few clicks on a decentralized exchange (DEX). Capital outflows could actually accelerate. A tool designed to protect the local currency could paradoxically strengthen the dollar.

This is precisely why each jurisdiction invests heavily in regulatory design while permitting stablecoins. The strategy is to open the door to the technology without surrendering control over capital flows.

In this context, major Asian markets initially favored central bank digital currencies (CBDCs) over private stablecoins. Central bank control over issuance and distribution can block conversion paths and capital flight at the source.

But reality moved faster than regulation. Dollar stablecoin adoption was already underway, and a consensus emerged that legislation alone could not reverse the trend. A more fundamental shift in thinking followed: rather than fearing dollar stablecoin expansion, the real solution lies in making local currencies more attractive in their own right.

At this point, Asian strategies pivoted. Instead of blocking dollar stablecoins, jurisdictions chose to selectively adopt stablecoin technology while enhancing the competitiveness of their own currencies. Concerns over capital outflows have not disappeared. Each jurisdiction is building institutional safeguards, including issuance requirements and reserve regulations, to find a balance between openness and control.

This is why regulators across the region are accelerating efforts to strengthen local-currency stablecoins. The issue is not simply a technology race. It is a matter of economic security.

What strategies are individual jurisdictions actually pursuing? The following sections examine the cases of Japan, Singapore, Hong Kong, South Korea, and China.

3. Asia’s Stablecoin Landscape in 2026

3.1. Singapore

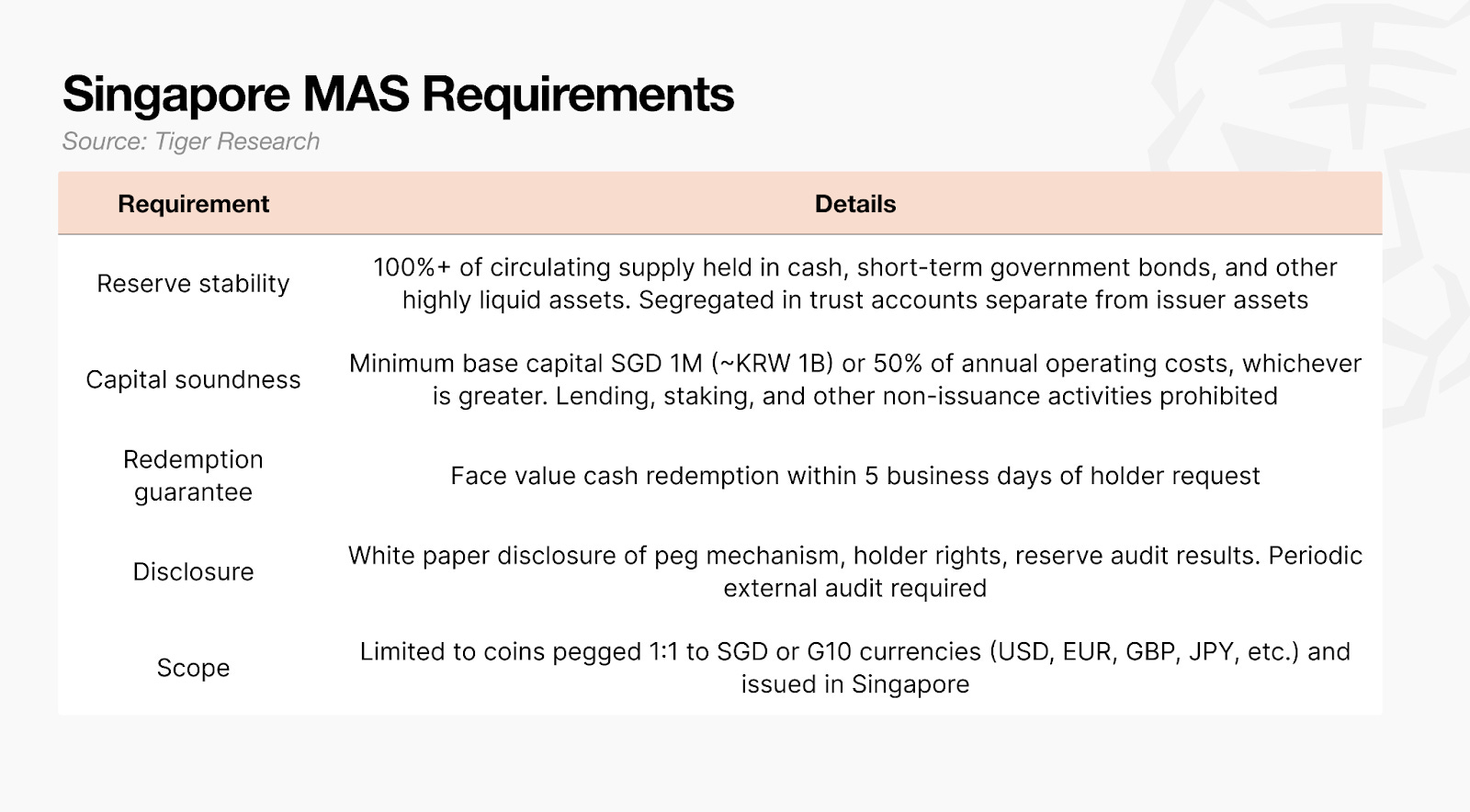

Singapore has recognized stablecoins as a regulated activity under the Payment Services Act (PS Act) since 2020. In 2023, it finalized a dedicated framework that added “Stablecoin Issuance Service” as a distinct service category within the PS Act.

What sets Singapore’s strategy apart is that it permits issuance of stablecoins pegged not only to the Singapore dollar (SGD) but also to USD and other G10 currencies. Countries like Japan and South Korea have large domestic-currency economies where local-currency stablecoins are a goal in themselves. Singapore, a city-state of six million, cannot build a global ecosystem on SGD stablecoins alone.

Singapore therefore chose to compete as a regulatory jurisdiction. Whether the stablecoin is pegged to USD or SGD, the goal is to have it issued under MAS oversight in Singapore, attracting issuers, capital, and talent. The strategy is working. StraitsX, Paxos, Ripple, Circle, and others have obtained Major Payment Institution (MPI) licenses, with six to eight core stablecoin operators active as of January 2026.

Regulation: A systematic design dating back to 2019

Singapore’s stablecoin regulation builds on the PS Act (Payment Services Act 2019), a single legislative framework that governs seven major payment service types, including remittance and digital payment tokens (DPT). It took effect in 2020.

The key concept is DPT. Section 2 of the PS Act defines a DPT as “a cryptographically secured digital representation of value used as a medium of exchange.” The term “stablecoin” does not appear in the statute itself, but MAS has consistently treated stablecoins as DPTs in its guidelines and annual reports. Stablecoin issuance was therefore already a legally regulated activity from 2020 onward, classified as a form of DPT service.

However, the PS Act’s DPT regime focused on operational resilience and customer asset protection: how to segregate and safeguard customer assets in the event of exchange hacks or operator insolvency, and how to ensure technical stability. It did not address the risk most fundamental to stablecoins: value stability.

This gap became reality with the TerraUSD collapse in May 2022. TerraUSD, which relied on an algorithm to maintain its dollar peg, lost that peg overnight. A wave of redemption requests followed, wiping out tens of billions of dollars in value. The event demonstrated that as stablecoins become widely used for payments, a value collapse can transmit shocks beyond a single coin to the broader financial system.

MAS responded quickly. In August 2022, it launched a public consultation to formalize a stablecoin-specific regulatory review. A public consultation is a process through which regulators officially solicit feedback from the industry, experts, and the general public before introducing a new framework.

Incorporating feedback from that process, MAS finalized and published its Single-Currency Stablecoin (SCS) regulatory framework on August 15, 2023.

The central change was to separate stablecoin issuance from the existing DPT category and establish “Stablecoin Issuance Service” as a standalone service type within the PS Act. If DPT regulation represents operational oversight of crypto assets broadly, the SCS framework represents a value guarantee regime for stable assets used as payment instruments.

The “MAS-regulated” label

Only stablecoins that meet all SCS requirements may carry the official “MAS-regulated stablecoin” label. Unauthorized use of this designation is subject to fines or criminal penalties, making it effectively a government-backed certification mark.

Stablecoins issued offshore can still circulate and trade within Singapore, but they fall under existing DPT rules only and cannot use the label. Users of such coins operate without the reserve and redemption protections that the SCS framework provides.

The SCS framework has been finalized and published, with legal enforcement expected by mid-2026. In the current transitional period, MPI-licensed operators are voluntarily complying with framework requirements while issuing and operating stablecoins.

Case Study 1: StraitsX

Market response following the framework’s finalization was swift. As of January 2026, 36 entities hold MPI licenses for DPT services from MAS, with six to eight directly involved in stablecoin issuance.

The leading example is StraitsX, a stablecoin brand created by Singapore fintech group Xfers. It received in-principle approval (IPA) from MAS in November 2023, and three of its subsidiaries obtained full MPI licenses in July 2024. StraitsX currently issues XSGD, pegged 1:1 to the Singapore dollar, and XUSD, pegged to the U.S. dollar. Reserves are held at 100% in DBS trust accounts and subject to monthly external audits.

StraitsX stands out because it offers the most concrete demonstration of how a regulated stablecoin can function in everyday life. XSGD is already accepted as a payment method at Grab merchants and Alipay+ stores in Singapore. Under MAS-led Project Orchid, a programmable money initiative, purpose-bound money built on XSGD was piloted for Amazon vouchers and Grab payments.

Cross-border use is expanding rapidly. In May 2025, a partnership with Ripple brought XSGD natively onto the XRP Ledger (XRPL). XUSD is being used for peer-to-peer overseas remittances with Ant International and Grab, as well as on-chain SGD-USD conversion. With cumulative transaction volume of $1.8 billion, StraitsX is establishing itself as treasury management infrastructure for ASEAN enterprises.

Case Study 2: USD-based issuers (Paxos, Ripple, Circle)

Global operators handling USD stablecoins are also entering Singapore at pace. Their individual positioning varies, but all share a common thread: they are using Singapore as their Asia-Pacific (APAC) base.

Paxos Digital Singapore is the local subsidiary of Paxos, the global issuer behind PYUSD (PayPal’s stablecoin). It received IPA alongside StraitsX in November 2023 and obtained its full MPI license in July 2024. A key element is its selection of DBS Bank as its reserve custodian, a structure in which a major traditional bank directly manages a crypto issuer’s reserves, designed to build institutional investor confidence. Following the U.S. and UAE, Singapore is Paxos’s third issuance hub, with a Singapore-issued USD stablecoin planned for 2026 launch. As the first foreign MPI-licensed stablecoin issuer, Paxos is considered a leading candidate for the “MAS-regulated” label.

Ripple (Ripple Markets APAC) expanded its existing MPI license to cover stablecoin services in December 2025. It issues RLUSD, a USD-pegged stablecoin, natively on the XRP Ledger. Its key advantage is direct integration with Ripple’s existing cross-border payment network, On-Demand Liquidity (ODL). The integration of StraitsX’s XSGD onto XRPL in May 2025 was also a product of this Ripple partnership. The primary targets are inter-enterprise remittance and treasury management across APAC.

Circle, the issuer of USDC, obtained an MPI license in Singapore in September 2024. However, since USDC is issued in the United States, it is classified as a general DPT rather than falling under the SCS framework. Circle’s Singapore entity focuses on APAC institutional settlement, cross-border remittance, and USDC-SGD liquidity pool provision, using Singapore as its APAC expansion base. The “MAS-regulated” label does not apply, but Circle represents a notable case of an offshore issuer participating in the Singapore market through an MPI license.

Additional operators joining the stablecoin ecosystem on an MPI basis include XREX, NIUM, Thunes Asia, HashKey, and dtcpay.

3.2. Hong Kong

Hong Kong enacted the Stablecoins Ordinance in August 2025, becoming the second major Asian jurisdiction after Japan to implement a standalone stablecoin law.

Unlike Singapore, which embedded stablecoin provisions within its existing Payment Services Act, Hong Kong created an entirely separate statute. The scope also differs. While Singapore limits coverage to SGD and G10 currencies, Hong Kong places no restriction on reference currencies. Stablecoins pegged to HKD, USD, EUR, or any other fiat currency all fall within the regulatory framework.

Where Singapore’s strategy is to attract global issuers by competing as a regulatory jurisdiction, Hong Kong leads with an open framework unrestricted by currency and the institutional clarity of standalone legislation. By not specifying reference currencies, Hong Kong leaves room for stablecoins based on a wide range of fiat currencies to be issued locally. This open structure also provides a legitimate pathway for large Chinese firms that are effectively barred from issuing stablecoins on the mainland. The participation of a JD.com subsidiary in the sandbox illustrates this point.

Regulation: From sandbox to standalone law

Hong Kong’s stablecoin regulation originated with a 2022 HKMA discussion paper. In December 2023, the Financial Services and the Treasury Bureau (FSTB) and HKMA jointly conducted a public consultation, publishing their conclusions and confirming the legislative direction in July 2024.

The timing mirrors Singapore, where MAS launched its regulatory review immediately after the TerraUSD collapse in 2022. Hong Kong, however, added one extra step: it launched a stablecoin issuer sandbox in March 2024. In July 2024, HKMA selected three initial participants:

RD InnoTech (Hong Kong blockchain firm)

JINGDONG Coinlink Technology Hong Kong (JD.com subsidiary)

A consortium of Standard Chartered Bank, Animoca Brands, and HKT (Hong Kong Telecom)

The formal legislation, the Stablecoins Ordinance (Cap. 656), passed the Legislative Council on May 21, 2025, and took effect on August 1, 2025.

The core regulatory target is fiat-referenced stablecoins (FRS): coins that peg their value 1:1 to a fiat currency such as USD, HKD, or EUR.

A notable feature is how unlicensed issuers are restricted. FRS issued without an HKMA license cannot be sold to retail investors in Hong Kong; distribution is limited to professional investors only. This is more conservative than Singapore, where offshore-issued stablecoins can circulate as general DPTs even without the “MAS-regulated” label.

The supervisory structure is also split across two bodies. HKMA oversees stablecoin issuance, while the Securities and Futures Commission (SFC) regulates virtual asset exchanges. Issuance and distribution are governed by separate regulators.

Since the August 1, 2025 effective date, numerous institutions have expressed interest, but only 36 are known to have filed formal applications. As of February 2026, no licenses have been granted. HKMA has stated only that it is “reviewing applications from multiple institutions,” and the first license is expected in H1 2026.

This contrasts sharply with Singapore. There, StraitsX and Paxos received in-principle approval shortly after the SCS framework was finalized in August 2023 and obtained full MPI licenses by July 2024, with stablecoins already in operation. Hong Kong has the law in place, but no regulated stablecoin is yet active in the market.

Case studies: The three sandbox participants

With no formal licenses issued, the three sandbox participants provide the clearest picture of Hong Kong’s emerging stablecoin ecosystem. However, most remain at the testing stage, with limited publicly available detail on real-world use cases.

RD InnoTech: digital asset trading and cross-border trade payment proof of concept

JINGDONG Coinlink Technology (JD.com): supply chain finance and cross-border payment efficiency (targeting 90% cost reduction)

Standard Chartered / Animoca Brands / HKT consortium: Web3 payments, metaverse economy, and telecom payment simulation

3.3. Japan

Japan was the first country in Asia to legislate stablecoin regulation. A revised Payment Services Act, enacted in 2022, took effect in June 2023, granting stablecoins the legal status of “Electronic Payment Instruments.”

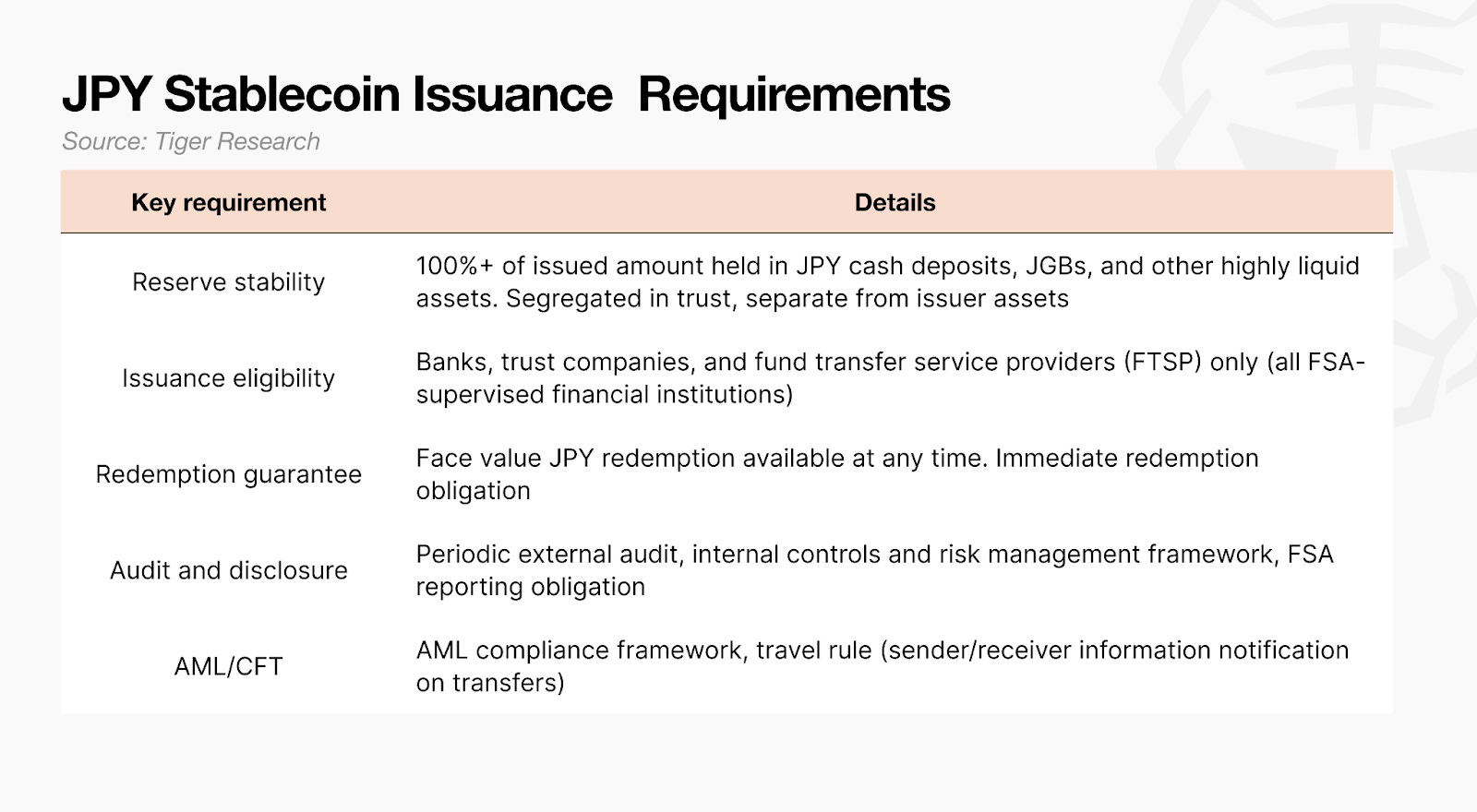

The most distinctive feature of the Japanese model is its restriction on who may issue stablecoins. While Singapore opens issuance to any entity that obtains an MPI license, whether fintech startup or global operator, Japan limits issuance to three categories: banks, trust companies, and registered fund transfer service providers (FTSPs). All three are existing financial institutions already supervised by Japan’s Financial Services Agency (FSA). In practice, this amounts to a bank-exclusive model.

This structure is a deliberate choice. The underlying rationale is to place stablecoins on an extension of the existing financial system rather than treating them as a new form of financial innovation. By entrusting issuance to institutions that already meet capital requirements and maintain internal control systems, regulators can reduce supervisory costs while securing stability from the outset.

Regulation: Payment Services Act revision and dual regulatory structure

The starting point is the June 2022 revision to the Payment Services Act. The law defines as “Electronic Payment Instruments” any digital assets that peg their value 1:1 to a fiat currency such as the yen and guarantee holders the right to redeem at face value in cash at any time.

Stablecoins that maintain their value through crypto-asset collateral, such as MakerDAO’s DAI (backed by Bitcoin, Ethereum, etc.), do not qualify under this category and are classified as general crypto assets.

Issuer type determines legal character and usage limits

Only banks, trust companies, and fund transfer service providers (FTSPs) licensed by the FSA may mint, burn, and hold 100% reserves in trust. Notably, the legal classification and usage restrictions of a stablecoin depend on who issues it:

Banks: classified as deposits; no transfer limits

Trust companies: structured as trust beneficiary rights; no transfer limits

FTSPs: treated as claims (debt instruments); subject to a JPY 1 million per-day cap on issuance and redemption (peer-to-peer transfers excluded)

Distribution (secondary market) is handled separately. Buying, selling, exchanging, and custodying already-issued stablecoins requires a separate registration as an Electronic Payment Instrument Transaction Business Provider (EPITB). Binance Japan, for example, obtained EPITB registration to facilitate user-to-user trading and transfer of JPYC. Existing crypto exchanges can offer stablecoin trading services by adding EPITB registration.

2025 reserve rule relaxation

A significant regulatory easing took place in 2025. Previously, trust-type stablecoin reserves had to be held entirely in bank deposits. The revision now allows up to 50% of reserves to be invested in low-risk assets: Japanese or U.S. government bonds with a residual maturity of three months or less, or early-terminable time deposits.

This change directly affects issuer revenue models. Just as issuers in Singapore and Hong Kong earn interest by investing reserves in short-term U.S. Treasuries, Japan has now explicitly permitted the same practice by law. For yen stablecoin issuers, however, Japanese government bonds are the more rational choice due to currency mismatch risk and hedging costs. The intent is to improve issuer economics and accelerate ecosystem growth.

For FTSPs like JPYC, the situation differs. FTSPs safeguard reserves through official deposit, bank guarantees, or trust agreements. Under the trust agreement option, cash, bank deposits, and government bonds are permitted with no separate cap on investment ratios. JPYC has announced plans to allocate 80% of reserves to Japanese government bonds and 20% to bank deposits, enabling the issuer to earn roughly 3-4% annually while remaining compliant.

Case Study 1: JPYC

The first mover in Japan’s yen stablecoin market was not a megabank but a startup. JPYC Inc. registered with the FSA as a fund transfer service provider and officially launched JPYC, a 1:1 yen-pegged stablecoin classified as an Electronic Payment Instrument, in October 2025.

The operational flow works as follows: a user deposits yen through the dedicated platform JPYC EX, and an equivalent amount of JPYC is minted and sent to the user’s blockchain wallet. To redeem, the user returns JPYC and receives yen in their bank account. Reserves are fully backed by yen deposits and Japanese government bonds. Identity verification uses My Number Card (Japan’s national ID) based e-authentication.

JPYC matters not only as the first FSA-regulated private yen stablecoin but because it shows how the regulatory framework actually functions in practice. A startup, not a bank, entered the market first by using the FTSP license path. Within the bank-exclusive model’s broad framework, the FTSP registration window provides a viable entry point for non-bank operators.

Case Study 2: The three megabanks and Progmat Coin

If the startup was the first mover, banks are driving the scale play. In late 2025, Japan’s three megabanks, MUFG (Mitsubishi UFJ), SMBC (Sumitomo Mitsui), and Mizuho, announced a joint blockchain-based stablecoin initiative.

The core infrastructure is Progmat Coin, developed by an MUFG affiliate. Progmat is a modular platform designed to allow multiple banks to issue their own stablecoins, handling issuance, custody, and settlement within a single architecture. The three banks plan to issue stablecoins pegged to both yen and U.S. dollars on this platform. The FSA approved the initiative as a Payment Innovation Project pilot, with testing underway since November 2025.

The combined assets of Japan’s three megabanks run into hundreds of trillions of yen. Their direct entry into stablecoin issuance signals that blockchain-based payments are shifting from an experiment outside the banking system to a strategy within it.

A separate project worth noting is DCJPY (Digital Currency JPY). Unlike stablecoins, DCJPY tokenizes bank deposits themselves into a “digital yen.” Multiple banks, including GMO Aozora Net Bank, are participating, with the goal of applying it to inter-corporate settlement and supply chain finance. Japan is pursuing stablecoins and tokenized deposits in parallel, designing its digital payment infrastructure in multiple layers.

3.4. South Korea

South Korea is the only major Asian jurisdiction that still lacks a dedicated stablecoin law. As a result, no KRW-pegged stablecoin has received regulatory approval as of February 2026.

However, activity outside the regulatory perimeter is already underway. KRWQ, issued by IQ and Frax, supplies KRW liquidity in global DeFi markets. BDACS’s KRW1 is at the proof-of-concept stage, demonstrating institutional infrastructure. Within the regulated sphere, major players such as the Naver Pay/Upbit consortium and Kakao Bank are positioning to launch stablecoins as soon as legislation is in place. This creates a unique situation in which the market is ready to open the moment the law does.

Regulation: Phase 1 complete, Phase 2 is the real battle

The Digital Asset Basic Act (DABA) was passed in 2025 as the overarching framework for the virtual asset market, establishing asset definitions and classifications, an operator licensing system, and the allocation of supervisory authority. That was Phase 1.

DABA, however, does not include detailed stablecoin issuance rules. Issuer eligibility and reserve management requirements are to be finalized through subordinate regulations and supplementary legislation during 2026. The central debate in Phase 2, how broadly to open issuer eligibility, is growing more contentious rather than less.

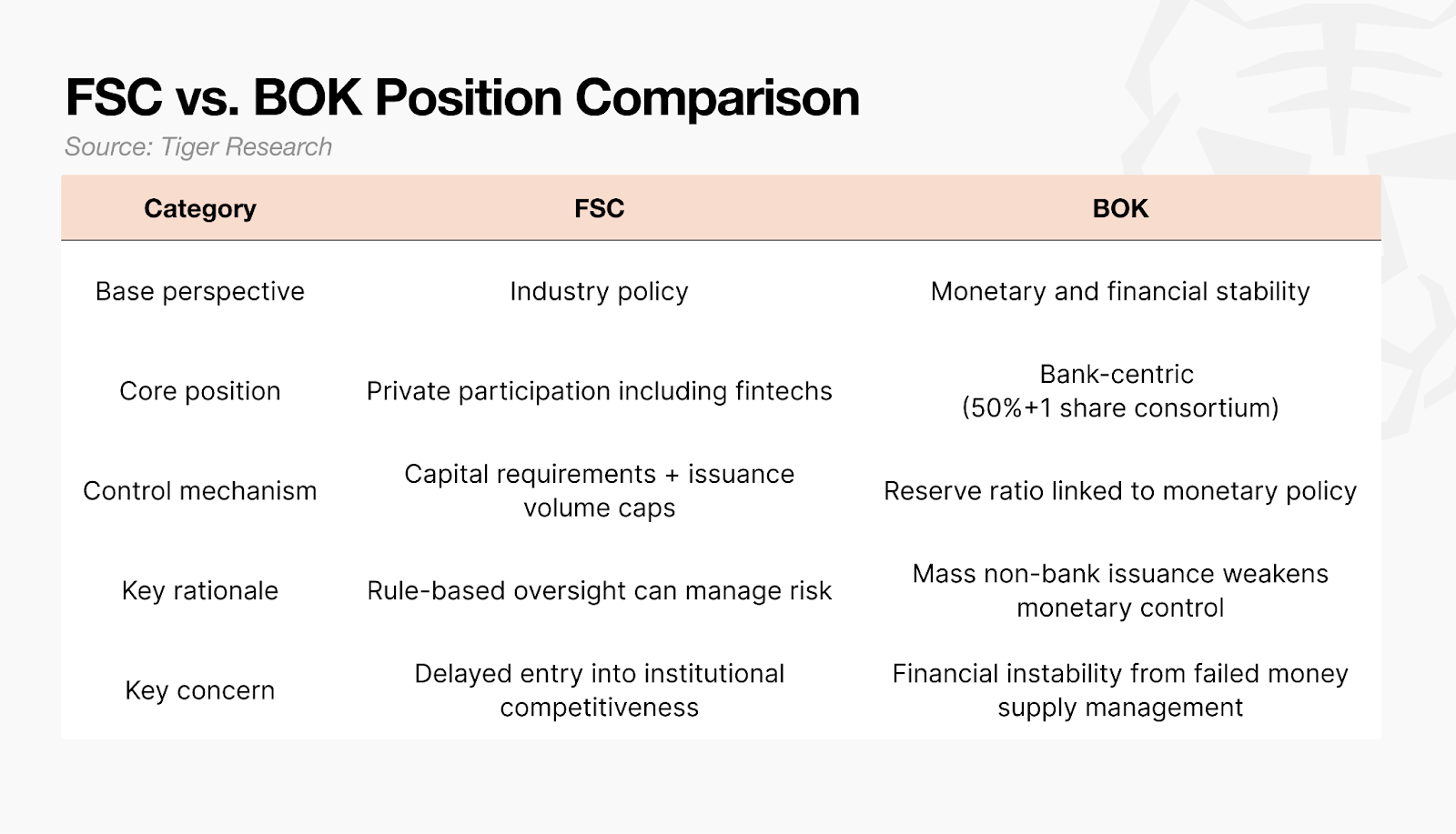

The Financial Services Commission (FSC) takes an industrial policy view. It argues that any entity meeting capital and technical requirements should be eligible, including internet-only banks, fintech firms, and consortia, not just traditional banks. The FSC sees aggregate issuance caps and rule-based oversight as sufficient risk controls, and warns that excluding private-sector participants will delay the integration of industry innovation into the regulated system.

The Bank of Korea (BOK) draws its line on monetary and financial stability grounds. Because stablecoins function much like deposits, large-scale issuance by non-bank entities would compromise the central bank’s ability to manage money supply through reserve requirements. The BOK therefore advocates a consortium model requiring banks to hold a majority stake (50% + 1 share), an approach that aligns closely with Japan’s bank-exclusive model.

The debate is structural, not bureaucratic

This is not a simple turf war between agencies. The scope of issuer eligibility will determine the market’s very structure. Restricting issuance to banks secures stability but slows innovation. Opening it to fintech increases competition, but whether non-bank issuers have sufficient safety nets in a large-scale redemption event (bank run) remains unproven.

The debate is live in the National Assembly as well. The substantive design of Phase 2 legislation is being led by the Democratic Party’s Digital Asset Task Force (TF). As the ruling party holds a parliamentary majority, the TF’s draft carries significant weight in setting the legislative direction, though the final bill requires agreement with financial regulators.

As of February 11, 2026, the TF is scheduled to hold a final meeting with advisory committee members on the 24th to finalize the ruling party’s proposal. The internal mood within the TF diverges from the BOK’s 50%+1 share rule. TF chair Rep. Lee Jeong-mun stated that the prevailing view favors designating issuers as ordinary corporations under commercial law rather than requiring 50%+1 bank ownership. Nine advisory committee members also raised constitutional concerns in a written opinion, arguing that retroactively restricting existing shareholding structures could conflict with shareholder capitalism principles.

Financial regulators, meanwhile, have signaled that if no agreement is reached with the ruling party, they may pursue the 50%+1 rule through government-initiated legislation. Because government bills typically take longer to process than legislator-initiated bills, both sides face pressure to negotiate. Where they find common ground will determine the structure of South Korea’s stablecoin market.

Case Study 1: Pre-regulatory issuance

No KRW stablecoin has received regulatory approval, but projects outside the regulatory perimeter are already demonstrating technical feasibility.

KRWQ, co-developed by IQ and Frax, launched on Base network in October 2025 as the first multichain KRW stablecoin. It is pegged 1:1 to the won using Frax infrastructure (including BlackRock’s BUIDL fund). Minting and redemption are restricted to KYC-verified institutions such as exchanges and market makers. It is not sold to Korean residents; the purpose is to supply KRW liquidity to global DeFi markets. Cumulative trading volume exceeded KRW 1 billion within one month of launch.

BDACS’s KRW1 takes a different approach. It deposits 100% of KRW reserves in a Woori Bank escrow account and is currently at the proof-of-concept stage. Technical validation is being conducted with internal capital only, so retail distribution and commercial transactions are not available. However, integration with the Plume mainnet provides an environment for developers and institutions to test KRW-based RWA payments and investments. Commercial launch is planned for after the Digital Asset Basic Act takes effect.

Both projects are attempts to prove the technical viability of KRW stablecoins through offshore structures or PoC pathways before Korean regulation is finalized.

Case Study 2: Major players waiting for legislation

On the regulated side, preparation by large operators is well advanced. A distinctive feature of the Korean market is that multiple players are ready to begin issuance immediately upon legislative enactment.

The most closely watched initiative is the Naver Pay-Upbit consortium. Naver Pay, the payments subsidiary of Korea’s largest portal, and Upbit (operated by Dunamu), the country’s largest crypto exchange, are planning joint issuance of a KRW stablecoin. Dunamu is developing a purpose-built, regulation-friendly blockchain infrastructure called GIWA. The GIWA chain incorporates identity verification (Dojang) and transaction privacy (Bojagi) features required by financial institutions, designed to support stablecoin issuance and distribution within the regulated system. Naver Financial’s payment network and Naver’s AI and IT infrastructure are layered on top.

Tech companies and exchanges are not alone. Traditional financial institutions including Shinhan Bank, IBK, NongHyup, and K Bank are also forming their own consortia. The final outcome of the 50%+1 rule debate could alter the structure and participation scope of these consortia, leaving arrangements fluid until regulation is finalized.

3.5. China

China is the only jurisdiction covered in this report that has imposed a blanket ban on private stablecoins. While Singapore, Hong Kong, Japan, and South Korea are debating the conditions under which private issuance should be permitted, China has already concluded that there is no reason to permit it at all. Instead, its strategy is to replace the functions of stablecoins with the digital yuan (e-CNY), issued directly by the central bank.

This approach stems from the Chinese government’s view of monetary sovereignty. As discussed earlier, the moment a local-currency stablecoin is placed on a blockchain, a conversion path to the dollar opens with it. For China, which relies on capital controls as a core policy instrument, that path becomes an uncontrollable channel for capital flight. If the private sector were to issue a yuan-pegged stablecoin, there would be no technical way to prevent that coin from being swapped into USDT on an offshore exchange and ultimately converted to dollars.

Regulation: One line says it all

China’s stablecoin regulation needs no lengthy statute. A 2021 joint notice issued by ten government agencies, including the People’s Bank of China (PBoC), classified all virtual asset-related activities as “illegal financial activities.” That stance remains unchanged as of February 2026. Exchange operations, mining, and token issuance (ICOs) are all prohibited, and stablecoins are no exception.

In February 2026, enforcement went a step further. A new joint notice from the PBoC and seven agencies on “Further Prevention and Handling of Risks Related to Virtual Currencies” explicitly banned unauthorized issuance of yuan-pegged stablecoins both domestically and offshore. The key language states that yuan-pegged stablecoins perform functions similar to legal tender in circulation and pose a direct threat to monetary sovereignty, and that no entity or individual, domestic or foreign, may issue such stablecoins without legal authorization from the relevant authorities.

Critically, this notice targets offshore issuance as well. Chinese firms issuing yuan-pegged stablecoins abroad, or tokenizing yuan-denominated assets via real-world asset (RWA) structures on blockchain, also fall within scope. Even a yuan-pegged coin issued in Singapore or Hong Kong could expose mainland Chinese operators involved in the process to penalties.

Offshore-issued dollar stablecoins (USDT, USDC, etc.) are not classified as “illegal financial activities” per se, but their integration into domestic payment infrastructure, including QR code payments and online payment channels, is prohibited. In effect, no legitimate pathway exists for private stablecoins to enter the Chinese financial system.

4. In the End, It Comes Down to Speed

The question facing Asian markets on stablecoins converges on a single point: whether their national currencies can secure a place in the future of digital payments.

Singapore has assembled global issuers by positioning itself as a regulatory jurisdiction. Hong Kong has enacted its law but has yet to grant its first license. Japan saw a startup open the market ahead of banks, even within a conservative framework. South Korea has major players on standby, but the debate over issuer eligibility is dragging on. China has shut out the private sector entirely and chosen direct state control. Even the frontrunners, Singapore and Japan, are only at the starting stage of real-world use for local-currency stablecoins.

Everyone agrees on the potential of stablecoins. The problem is time. The global stablecoin ecosystem is hardening rapidly around the dollar. Infrastructure built on dollar stablecoins as the base currency is emerging at pace, such as Circle’s on-chain FX platform ARC. These networks concentrate liquidity and use cases around the currencies that join first. Japan has already entered through JPYC, but South Korea, without a KRW stablecoin, cannot participate at all. Joining a network after it has solidified is a fundamentally different game from securing a position at the outset.

The fact that local-currency stablecoins from across Asia account for less than 1% of the $300 billion market tells the story. Most legislation only took effect between 2023 and 2025, so this is partly to be expected. But dollar stablecoins did not pause in the interim. Transaction volumes have reached multiples of Visa’s, and use cases are expanding daily into B2B payments, cross-border remittance, and AI agent transactions.

As discussed, local-currency stablecoins carry a double-edged quality. The moment they go on-chain, conversion paths to the dollar open alongside them. Without careful institutional design, pursuing speed alone risks triggering capital outflows. That is why Asian jurisdictions are proceeding cautiously.

Yet if caution becomes delay, the very position these currencies are meant to protect will disappear. Asia is building highways for its national currencies. Some countries are still arguing over the blueprints. Others are installing guardrails and traffic lights. Even the leaders are still in test-drive mode. Meanwhile, the dollar is a sports car in the next lane, running at full speed. No matter how well the road is built, it means nothing if there is no vehicle to put on it.

Perfection is not an option. In the end, it comes down to speed.

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.