In 2026, the global crypto ETP market is gradually diversifying. While the U.S. spot ETP market remains the most active, a wide range of other crypto ETP products is also emerging. What other types of ETP products are available, and how are they structured?

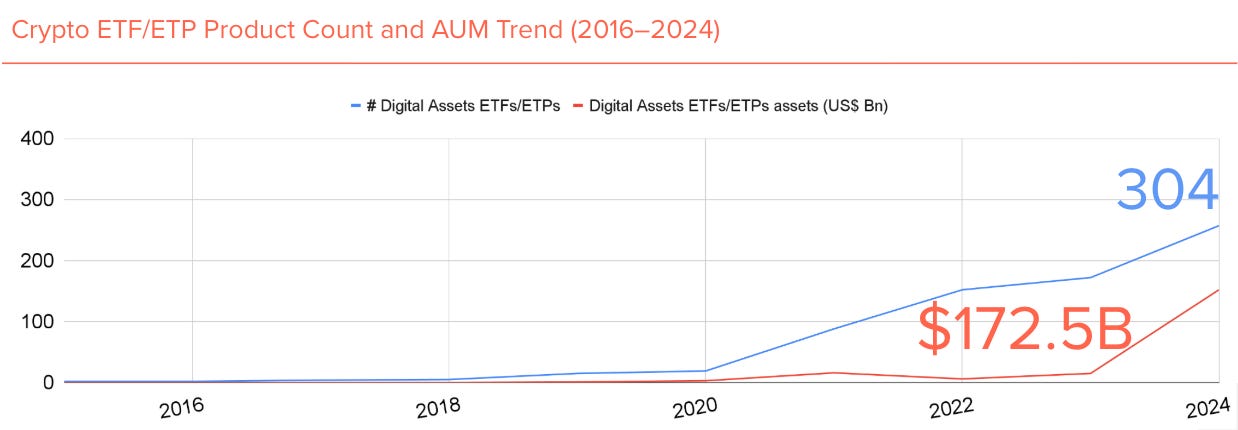

Global Crypto ETP Market Status

Global crypto ETP total AUM reached $172.5B as of 2025, with 85% concentrated in U.S.-listed products

Notably, the number of U.S. registered investment advisors allocating to crypto ETFs surged from under 200 in 2024 to over 2,000 in 2025, a 10x increase, driving market growth

Outside the U.S., Europe accounts for approximately 11% of total market AUM; Canada, Hong Kong, and others represent the remaining ~4%

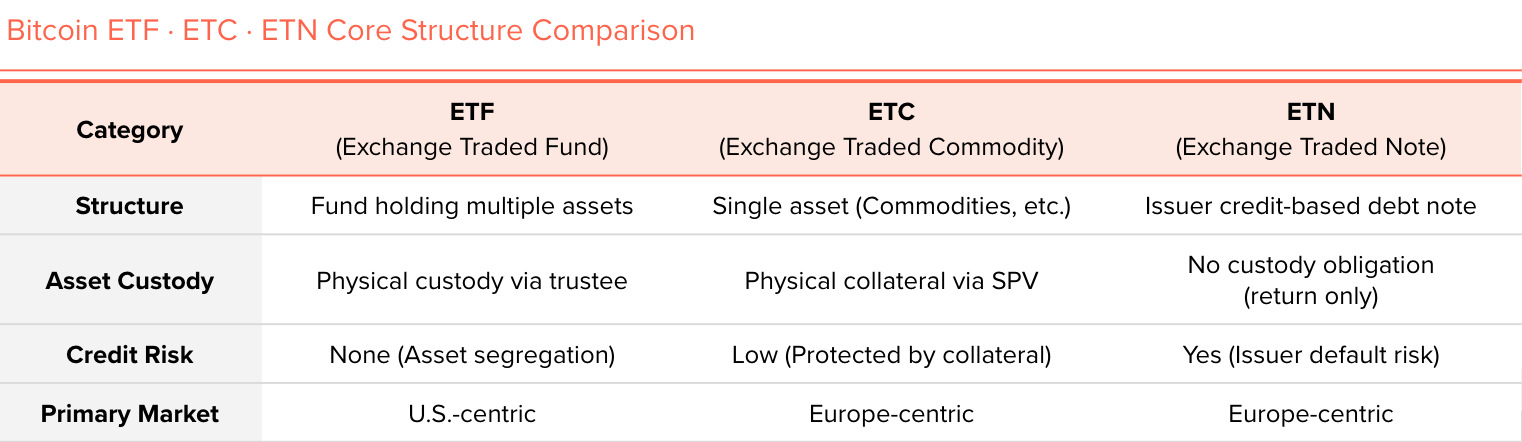

Products Divided by Regulation: ETF, ETC, ETN

In Europe, funds are legally required to hold a diversified basket of assets under the diversification rule, making the ETF label unavailable for single-asset products such as Bitcoin

As a result, European markets list and trade ETC structures, which treat Bitcoin as a commodity, and ETN structures, which are debt instruments backed by issuer credit, as alternatives to ETFs

Unlike ETFs and ETCs, which hold actual coins as collateral, ETNs only promise returns based on issuer creditworthiness, carrying principal loss risk in the event of issuer insolvency

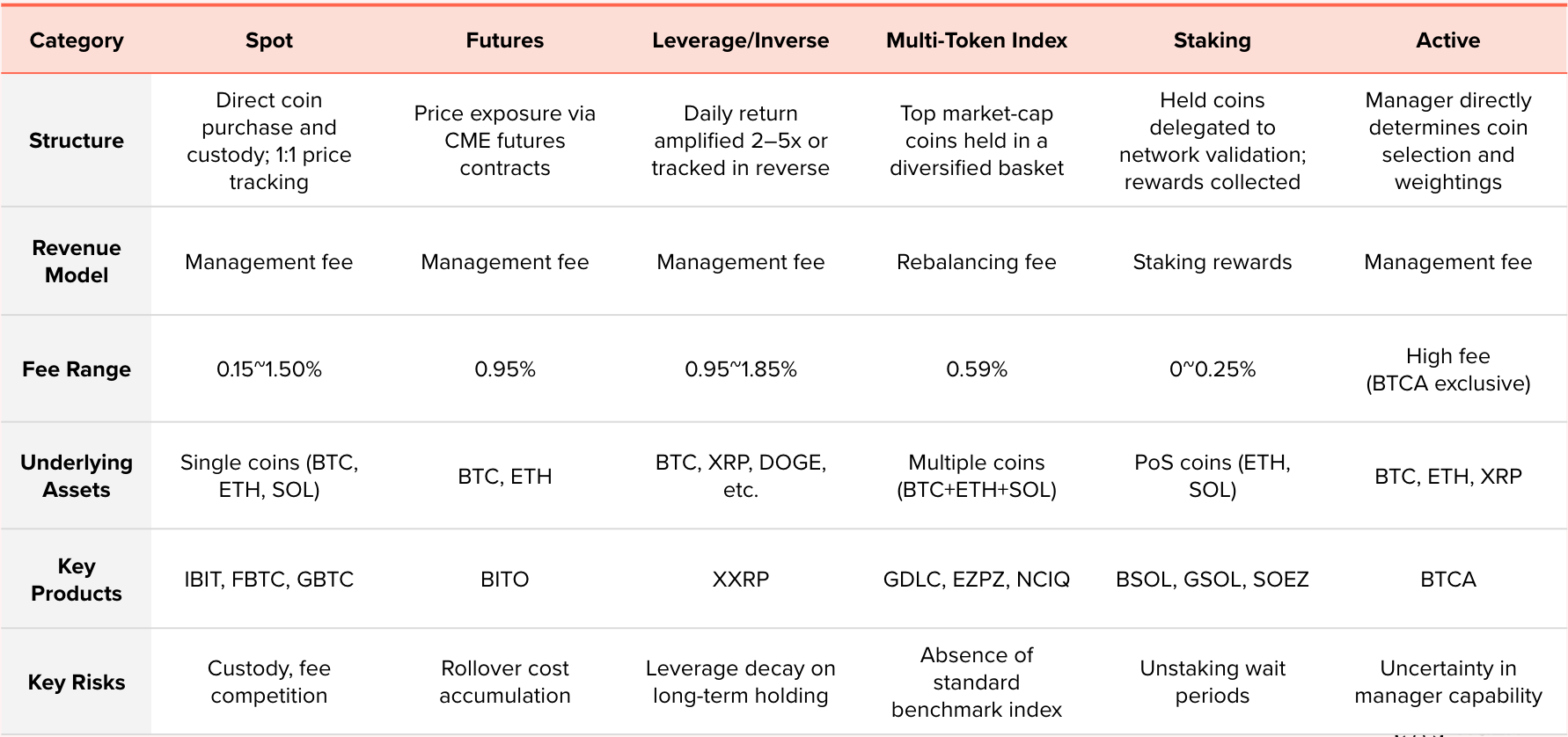

Global Crypto ETP Products

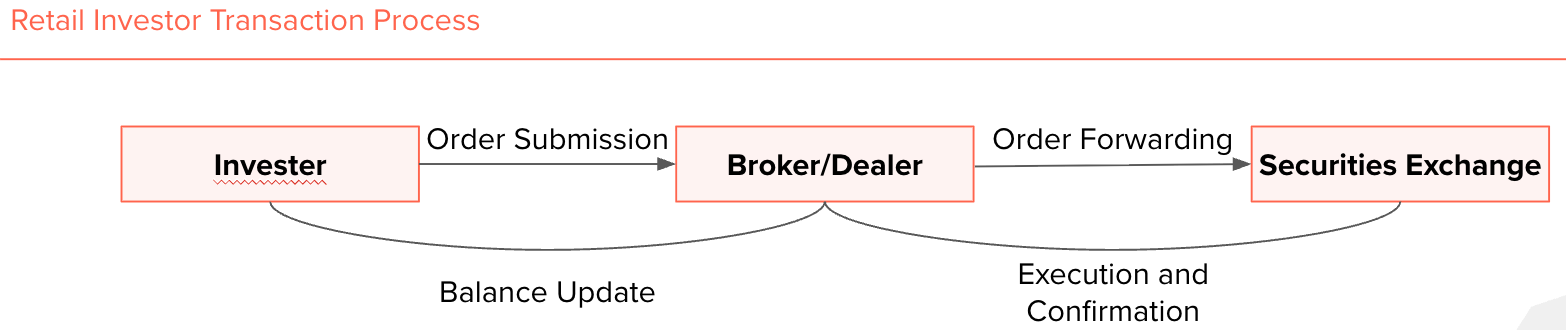

What Is a Spot ETP?

The issuer directly purchases cryptocurrency and holds it with a custodian, tracking the asset’s price on a 1:1 basis — the most straightforward and fundamental ETP structure (commonly referred to as a “spot ETF”)

Investors gain price appreciation exposure based on coin price movements, while the issuer’s sole revenue source is the annual management fee charged proportionally to AUM

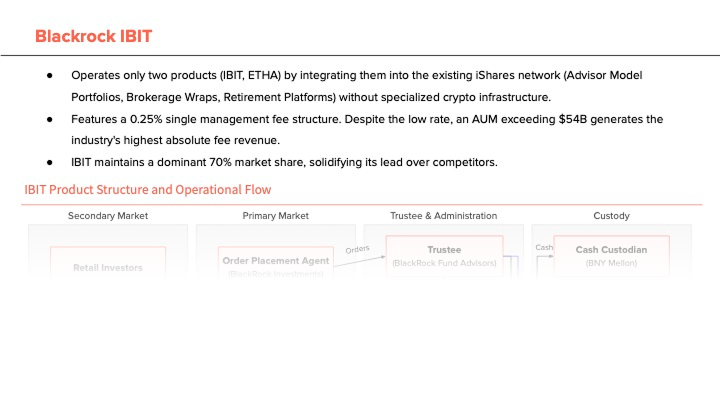

The simple 1:1 tracking structure leaves no room for product differentiation among issuers, driving intense fee competition to attract investor capital (e.g., BlackRock 0.25% → Franklin Templeton 0.19% → temporary 0% promotional fee waivers for early market capture)

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.