In February 2026, gold rose and Bitcoin plunged following the Iran strikes. Can we still believe Bitcoin is “digital gold”? We examine the conditions Bitcoin must meet to become the “next gold.”

Key Takeaways

In every geopolitical crisis, gold rose and Bitcoin plunged. Across past tests, the “digital gold” narrative was never once proven by data.

Nations stockpile gold yet keep Bitcoin out of reserves. For investors, Bitcoin is asymmetric: it falls with equities but fails to rise with them.

Three structural asymmetries shut Bitcoin out of safe-haven status: derivatives overhang (market structure), leverage-trader dominance (participant mix), and no repeated behavioral track record (behavioral accumulation).

Bitcoin is not a safe haven, yet it is a “crisis-useful asset” that actually works where borders close and banks shut down.

If the three asymmetries narrow, Bitcoin can become not a gold replica but a new category of “next gold.” Generational shift and algorithmic adoption are the variables that could accelerate it.

1. Is Bitcoin Really “Digital Gold”?

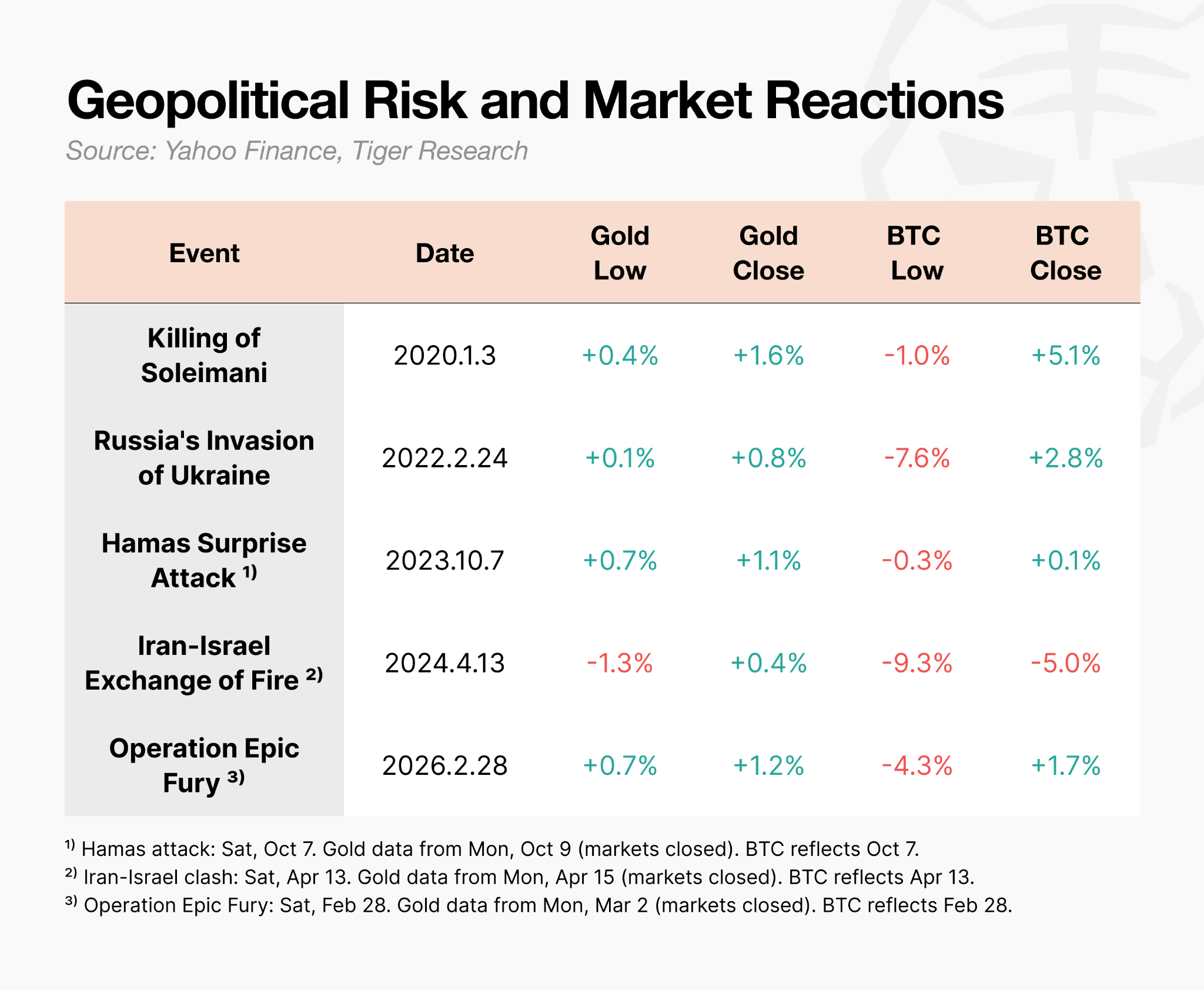

On February 28, 2026, the U.S. and Israel struck Iran. When Operation Epic Fury was announced, gold prices rose immediately. Bitcoin, by contrast, plunged to $63,000 intraday before recovering within a day.

Same event, opposite reactions.

Bitcoin moves differently from gold during geopolitical shocks like war.

It tends to recover relatively quickly after the initial drop, but cascading forced liquidations of leveraged traders make the drawdown far deeper. The intraday decline reached -9.3% during the Iran-Israel strikes and -7.6% during the Ukraine invasion. Gold rose at those same moments, a stark contrast.

Can we really call Bitcoin “digital gold” when it is the first asset to fall the moment a crisis hits?

2. Bitcoin Is Not “Digital Gold” for Nations or Investors

Bitcoin was never designed to be “digital gold.” The title of Satoshi Nakamoto’s 2008 whitepaper was “Bitcoin: A Peer-to-Peer Electronic Cash System.” The starting point was a transfer mechanism, not a store of value.

The “digital gold” narrative we know today gained traction during the zero-rate, quantitative-easing era of 2020. As fears of currency devaluation peaked, Bitcoin drew attention as a store of value. In practice, however, neither nations nor investors treat Bitcoin as “digital gold.”

2.1. Nations: Stockpiling Gold, Only Considering Bitcoin

World Gold Council data show that central banks have never stopped buying gold year after year. Yet not a single major central bank has incorporated Bitcoin as a full reserve asset.

Some may counter that the U.S. formalized a “Strategic Bitcoin Reserve” by executive order in March 2025. The order’s text even states that “Bitcoin is often referred to as ‘digital gold.’” But the details tell a different story. The scope is limited to assets seized through criminal and civil forfeiture. The government is not purchasing new Bitcoin but simply holding what it already confiscated instead of selling it.

Notably, as U.S. Treasuries lose appeal, Europe and China are actively buying gold, but Bitcoin has not made it onto their list of alternatives.

2.2. Investors: Falls Together, Fails to Rise Together

The second half of 2025 was decisive. While the Nasdaq hit all-time highs, Bitcoin plunged more than 30% from its October peak of $125,000. The two assets began moving apart.

But the real problem is not the decoupling itself. It is the direction. Bitcoin falls alongside equities when they drop, yet fails to rise when they rally. For investors, this is the worst possible combination. There is no reason to hold an asset in a portfolio that shares the downside risk but misses the upside. Far from being a safe haven, Bitcoin’s appeal even as a risk asset is now in question.

3. Why Bitcoin Failed to Become “Digital Gold”

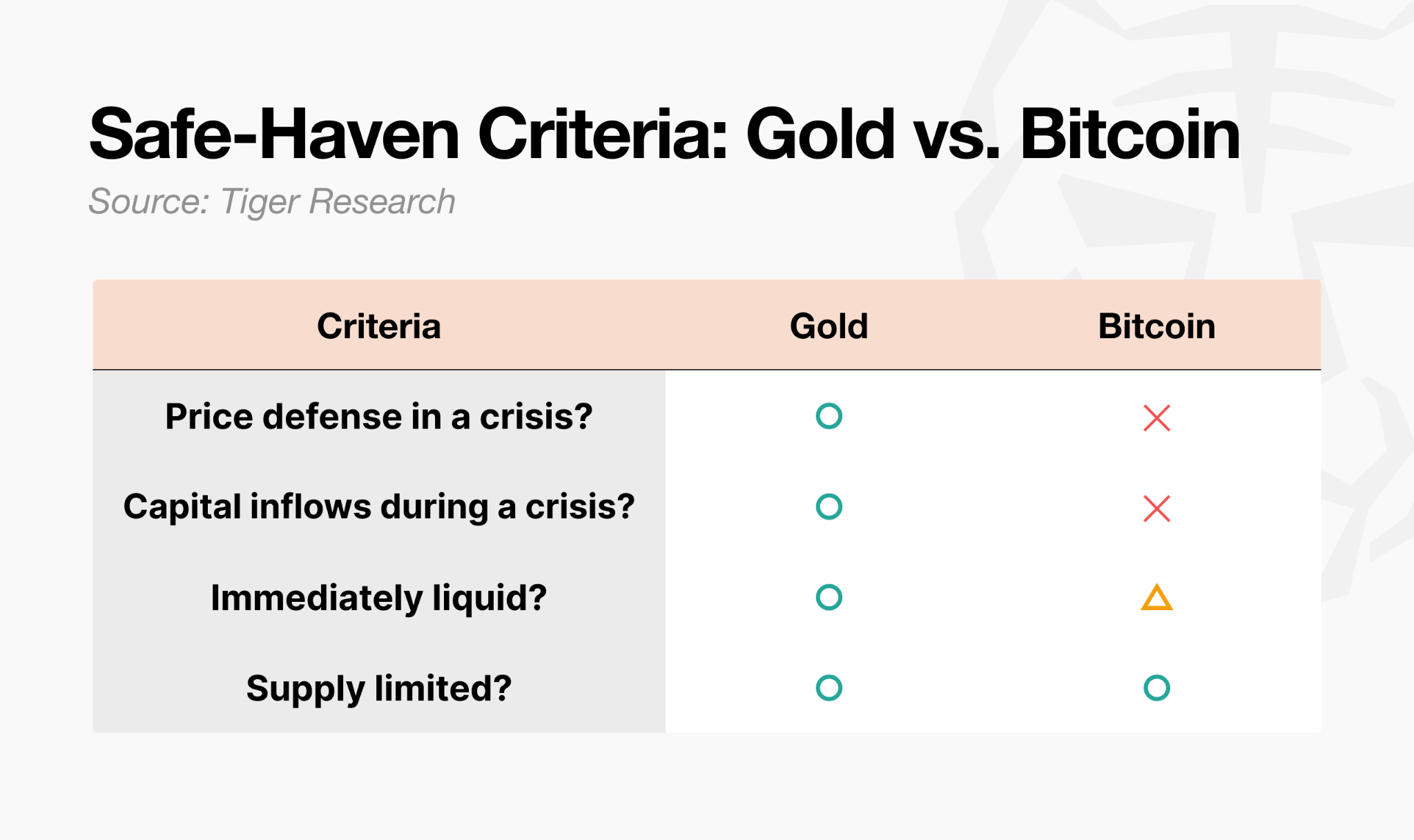

A safe-haven asset is not simply one that rises in price. Academically, it is an asset whose correlation with other assets falls to zero or turns negative during extreme downturns. The key question is whether it reacts predictably in a crisis. By this standard, the gap between gold and Bitcoin is clear.

Gold meets all four requirements. Bitcoin clearly meets only one: fixed supply. Liquidity is conditional. The remaining two are unmet. Three structural asymmetries explain this gap.

Market structure asymmetry: Gold has physical demand that supports a price floor, and its futures leverage ratio is low. Bitcoin’s derivatives volume runs roughly 6.5 times its spot volume, and its market trades around the clock, making it the first asset sold when a crisis hits.

Participant asymmetry: The crisis buyers of gold are patient capital such as central banks, pension funds, and sovereign wealth funds. The dominant participants in Bitcoin’s market are leveraged traders and hedge funds, the very capital that exits first in a crisis.

Behavioral accumulation asymmetry: “Buy gold when crisis hits” is a behavioral pattern repeated over decades until it became a formula. Bitcoin needs time to earn the same trust.

4. Not Safe, but Proven Useful

It is hard to call Bitcoin “digital gold” when it comes to safety. But its proven utility in crisis is real.

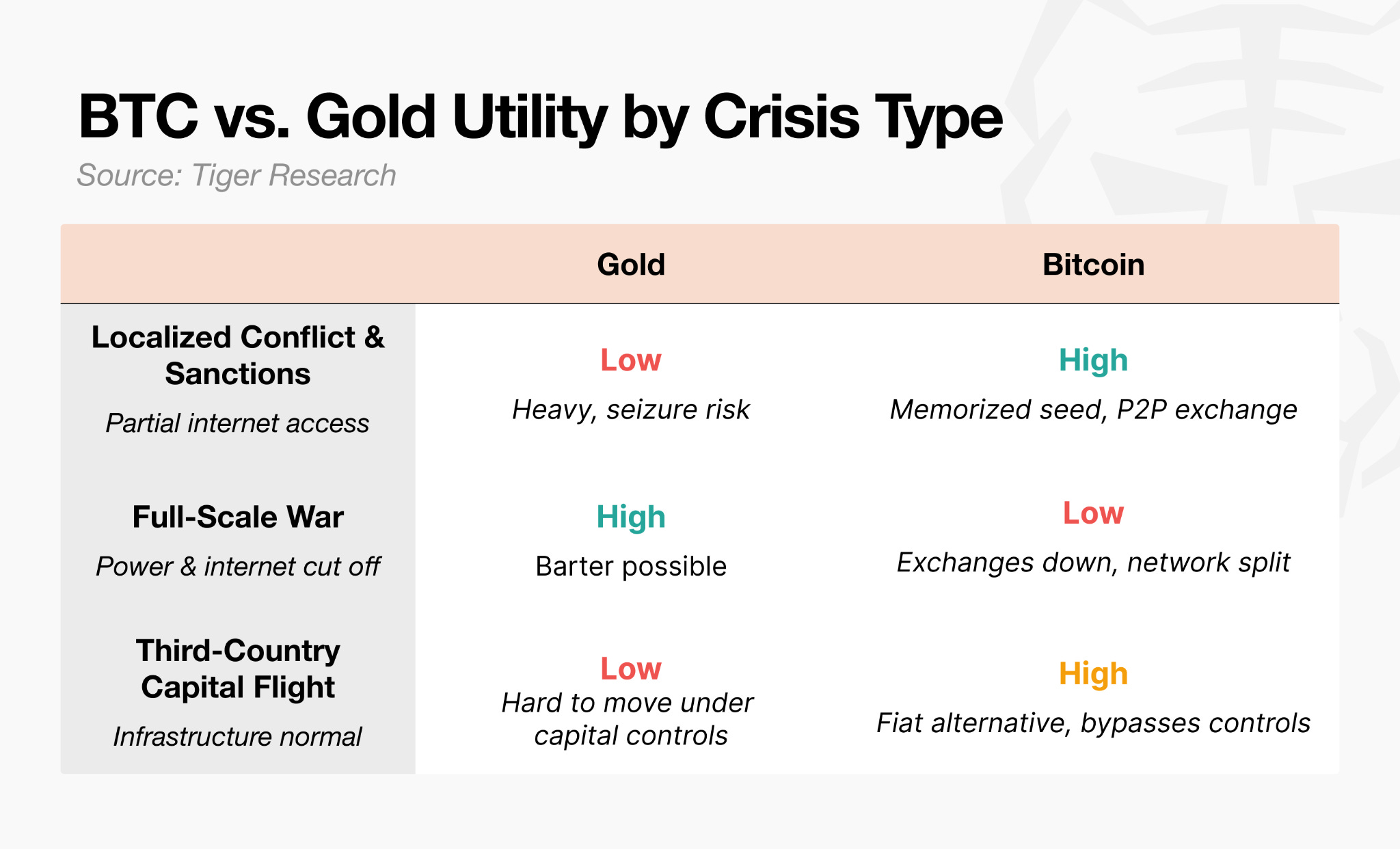

Right after Russia’s 2022 invasion, Ukraine’s central bank restricted electronic transfers and capped ATM withdrawals. Bank branches closed and citizens could not even access their own deposits. Some refugees carried Bitcoin seed phrases on USB drives across the border. Once in Poland, they reportedly converted Bitcoin to local currency through Bitcoin ATMs or P2P trades to cover living expenses.

UNHCR took it a step further, distributing the stablecoin USDC to displaced people and running a program that let them exchange it for local currency at MoneyGram locations. During Operation Epic Fury in 2026, outflows from Nobitex, Iran’s largest crypto exchange, surged 700% right after the strikes.

These cases show that people turn to Bitcoin not because it is a safe haven but because it works when the financial system does not.

In finance, “safe haven” means an asset whose price holds up during a crisis. That is a different concept from an asset you can use in a crisis. Bitcoin clearly offers functional value for movement and transfer in wartime, but it cannot defend its price. What makes a safe haven is not utility but predictable price behavior. Bitcoin delivers the former but not the latter.

5. The “Next Gold” Scenario for Bitcoin

Bitcoin has moved opposite to gold in every crisis. Neither nations nor investors treat it as “digital gold.” Yet its utility in places where borders close and banks shut down is hard to deny. Given that potential, if the three asymmetries narrow, the path to “next gold” opens up.

5.1. Market Structure Shift

Derivatives volume at 6.5 times spot triggers cascading liquidations in every crisis. Recently, futures open interest has declined and price discovery is showing signs of shifting toward spot and ETFs. But the real test is whether leverage rebuilds in the next bull market.

5.2. Participant Shift

After spot ETF approval in 2024, institutional capital flowed in and Bitcoin became a mainstream financial asset. But this created a paradox. The more institutions add Bitcoin to their portfolios, the more it gets sold alongside equities in risk-off episodes. Accessibility improves while independent price movement disappears. This is the financialization paradox.

Gold ETFs are also mainstream, yet gold moves opposite to equities in a crisis because “buy in a crisis” is a pattern built over more than half a century. To escape this paradox, the participant base must shift from leveraged traders to patient capital.

There is one overlooked variable here: generational turnover. When Gen Z begins inheriting and managing real wealth, gold may feel like their parents’ safe haven. This generation’s first investment account was not a brokerage but a crypto exchange. A generation whose first asset experience was Bitcoin may instinctively reach for it before gold when a crisis hits. The participant shift may start not with institutional decisions but with a generational change in behavior.

5.3. Behavioral Accumulation Shift

It took roughly 50 years after the Nixon Shock for gold’s “buy in a crisis” pattern to become a formula. Does Bitcoin need the same amount of time? Not necessarily. Epic Fury was the last test, and the result was the same again. An intraday crash, then recovery. As this pattern repeats, the belief that “it drops but always comes back” is building.

The more important variable is algorithms. A significant share of Bitcoin trading volume now comes from AI agents and algorithmic trading. If “buy Bitcoin in a crisis” strategies are embedded in these algorithms, the pattern can form without human behavioral accumulation. A scenario where trust is built in code before it is built in people.

Bitcoin is not “digital gold” today. But if market structure, participant composition, and behavioral accumulation shift on the foundation of its proven utility, it can become the “next gold.” Not a replica of gold, but the birth of an entirely new category.

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.