Digital Assets: From “Why” to “How”

The global financial landscape is already shifting.

PayPal issued PYUSD, a dollar-pegged stablecoin, and integrated it into its payment services. BlackRock launched BUIDL, a tokenized money market fund, surpassing $3B in AUM. JP Morgan, Fidelity, and Goldman Sachs followed. Wall Street, which was watching from the sidelines just two to three years ago, is now entering the market directly.

The reason is simple: structural inefficiency in legacy finance. Every transaction carries intermediary fees. Settlement takes days. When markets close, trading stops. Digital assets change this at a fundamental level. Lower cost, faster speed, no time constraints. The result is a more flexible, scalable market. Digital assets are no longer a question of “why” but “how.”

But “how” is harder than it looks. When finance shifted online, the challenge was not the technology. It was maintaining trust and control in a new environment. Same applies here. Issuance, custody, transfer, settlement must operate reliably on-chain, while integrating with legacy financial systems and regulation.

The core challenge is clear: make digital assets function as finance within the existing system. This report examines the key requirements and approaches financial institutions should consider when adopting digital assets.

1. A New Order in Global Finance

Digital assets have moved beyond speculation into an institution-led market. Institutional stance was long conservative, but accelerating regulation, led by the U.S., is shifting the view. Institutions now see digital assets as a new opportunity to explore and capture early.

This shift is most visible in the actions of major financial institutions. BlackRock, for example, did not stop at tokenizing its money market fund. It began enabling trading of the fund on UniswapX, a decentralized exchange. This signals that global financial institutions now view digital assets not merely as investment products, but as new infrastructure capable of extending the functions and reach of traditional finance. It also marks a symbolic convergence, where digital assets and traditional finance are crossing into each other's domains and forming a single ecosystem.

The market itself is expanding rapidly. In 2025, annual stablecoin transaction volume reached approximately $33 trillion, a 72% increase year-over-year. The real-world asset (RWA) tokenization market surpassed $25 billion, with tokenized U.S. Treasuries alone accounting for $10 billion. Digital assets have reached a scale that institutions can no longer overlook.

2. What Digital Asset Infrastructure Requires

Digital assets are no longer a matter of choice. The question is how to adopt them. The starting point is a clear understanding of blockchain’s role and its limits. Blockchain is an effective ledger technology for securely recording and verifying transactions. Blockchain’s role is exactly that.

To function as financial infrastructure, separate operational systems for processing, managing, and controlling transactions must be built on top. Before adoption, financial institutions must first assess three areas: regulatory compliance, technical compatibility, and operational reliability.

2.1. Regulatory Compliance

| Key Question: Can blockchain-based transactions meet the regulatory requirements set by financial authorities?

Regulatory compliance is the first checkpoint for digital asset infrastructure. As digital assets enter regulated finance, they face the same obligations as traditional finance. Yet the environment in which these rules must apply is fundamentally different and still unfamiliar.

Regulations such as AML, FDS, and KYC remain fully in effect. The challenge is how to apply them. In traditional finance, real-name accounts allow consistent identification of counterparties and fund flows. On blockchain, transactions center on wallet addresses, where the link between address and actual user is not automatically visible. Identifying counterparties and tracing fund flows becomes significantly more complex.

The core of regulatory compliance lies in whether blockchain-based transactions can be made identifiable and manageable within existing regulatory frameworks, so that counterparties and fund flows remain traceable and regulations enforceable.

2.2. Technical Compatibility

| Key Question: Can legacy back-office operations and blockchain-based transactions connect within a single workflow?

For digital assets to function as financial infrastructure, blockchain-based transactions must be processed within existing back-office workflows. They cannot operate in isolation from legacy systems.

The challenge is that blockchain operates outside the internal systems of financial institutions. The two environments record and process transactions differently. Blockchain data is not structured in a format that legacy systems can directly read. Data structures and interpretation methods also vary across networks. As the number of supported chains grows, integration scope and operational complexity increase in parallel.

Technical compatibility depends on whether blockchain data can be transformed into formats that existing systems process, and whether on-chain transactions can be embedded into institutional workflows. Issuance, settlement, and clearing must flow seamlessly between legacy back-office and blockchain-based operations.

2.3. Operational Reliability

| Key Question: Can blockchain infrastructure operate at the reliability level financial services demand?

Operational reliability matters because digital asset services run on infrastructure that operates 24/7/365. In traditional finance, fixed operating hours and scheduled maintenance served as natural buffers. On blockchain, even minor delays or outages can lead directly to transaction delays and erosion of institutional confidence.

The challenge is that blockchain-based services do not simply process transactions. Data collection, transaction processing, and system integration occur simultaneously. A failure in any one component can affect the entire service. Transaction delays, data gaps, or network outages can cascade into settlement errors or reporting failures.

Reliability is not just uptime. It requires maintaining transaction continuity, data consistency, incident response capability, and security controls together. Digital asset infrastructure must go beyond connection. It must sustain that connection as a stable, production-grade service.

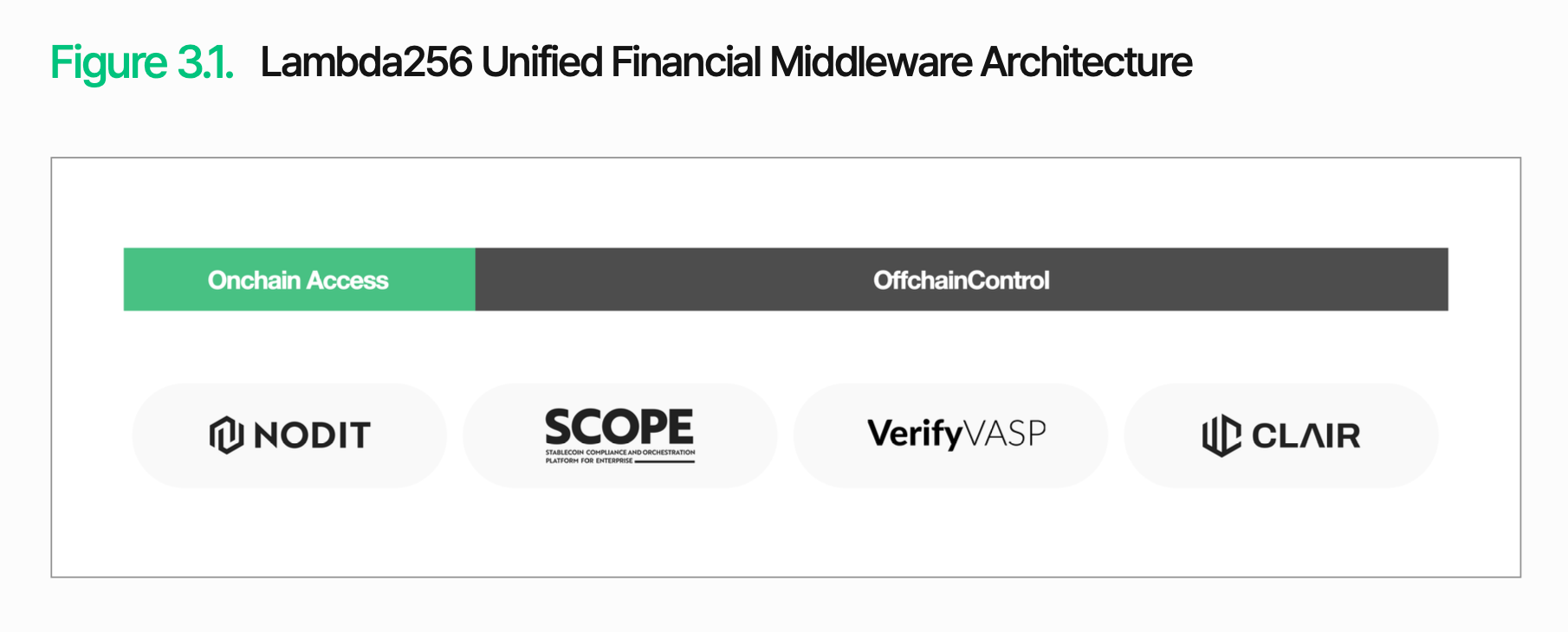

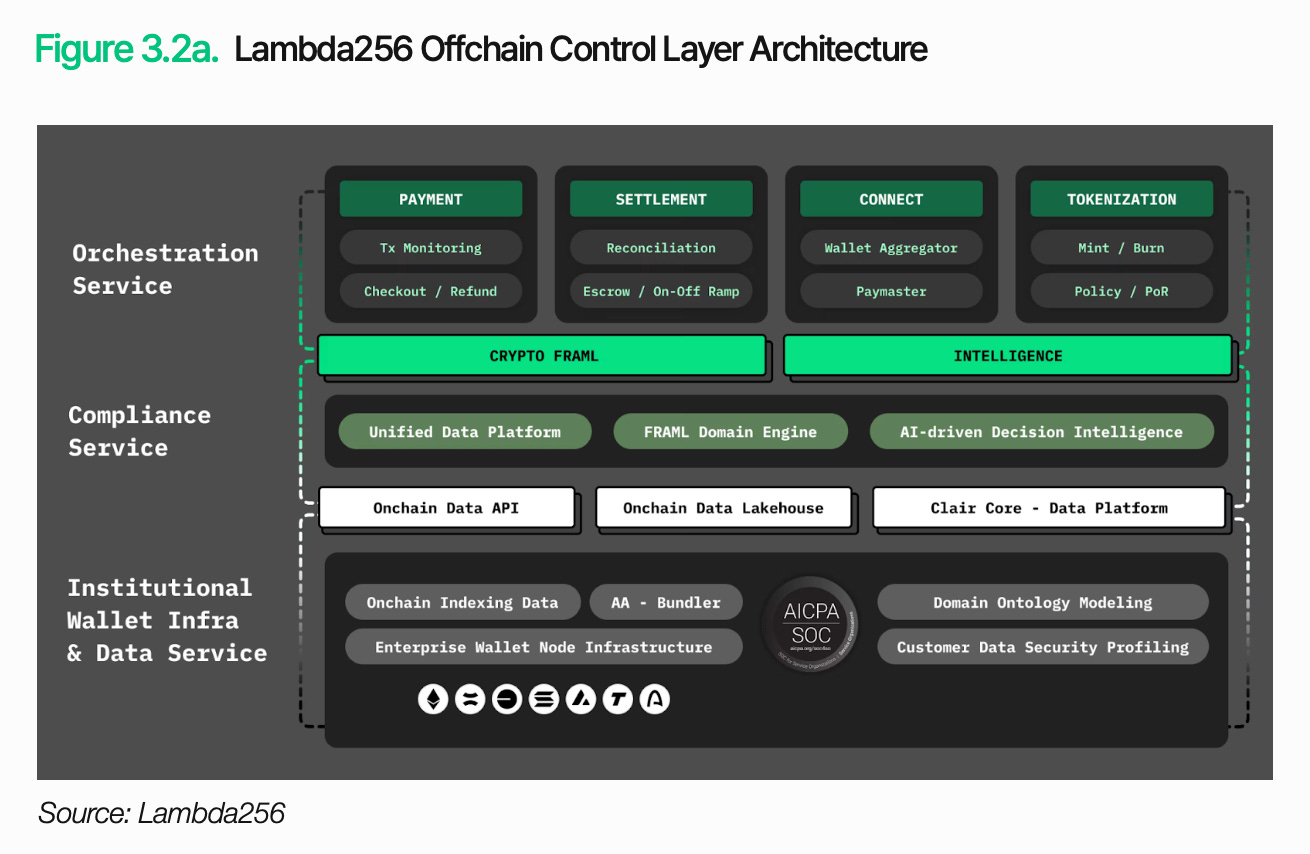

3. Lambda256: Unified Financial Middleware for Digital Asset Adoption

As discussed, the core challenge of digital asset adoption is enabling blockchain-based transactions to be processed and managed within existing financial systems. Lambda256 provides unified financial middleware for this purpose. A blockchain technology subsidiary of Dunamu, operator of Upbit, Lambda256 has built a unified technology stack for digital asset adoption, backed by large-scale infrastructure operations and extensive PoC experience.

Lambda256’s technology stack consists of two layers: Onchain Access and Offchain Control. Onchain Access collects and refines data and transactions from multiple blockchains into formats that existing systems can use. Offchain Control processes and manages them within traditional financial operations. The core of this architecture is connecting blockchain transactions into institutional workflows.

By delivering these capabilities as middleware, Lambda256 enables financial institutions to adopt digital asset infrastructure by integrating it with existing systems. Institutions can leverage on-chain advantages while maintaining operations and controls within their current framework, reducing infrastructure burden and allowing greater focus on core business.

3.1. Onchain Access

Onchain Access refers to the foundation for reliably connecting to blockchain networks, retrieving necessary data, and processing transactions. Basic functions such as balance inquiries, transaction status checks, and asset transfers all depend on this layer.

However, onchain access is not simply a matter of connecting to a blockchain. While on-chain data is public, it is not structured in a form that existing systems can directly read and use. Checking a specific wallet’s balance or asset status requires retracing related transactions and assembling the needed information. This burden grows as data structures differ across networks.

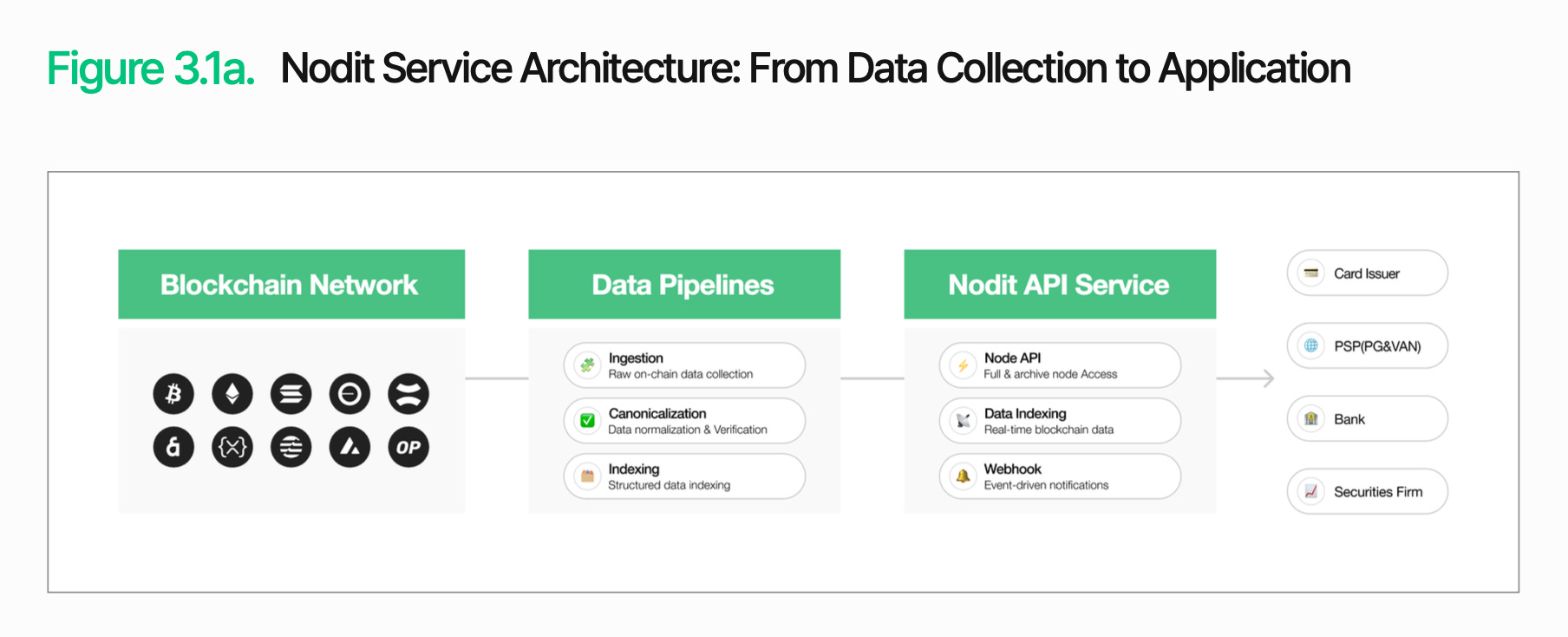

Nodit is an institutional-grade blockchain data infrastructure built to solve this. It collects and processes data from multiple blockchain networks and delivers it in formats that existing systems can immediately use. Financial institutions can leverage on-chain data within their systems without operating complex nodes or handling raw data processing.

Processing stability is equally critical. Digital asset services operate continuously, and any disruption in data retrieval or transaction verification leads directly to service delays and operational overhead.

Nodit maintains stable processing under heavy traffic through its Elastic Node architecture, which auto-scales nodes based on traffic volume, and its HyperNode engine, which distributes requests across multiple nodes. Combined with 24/7/365 monitoring, automated failover, dedicated node support, and SOC 2 Type 2 certification, this provides a trusted access foundation for financial institutions.

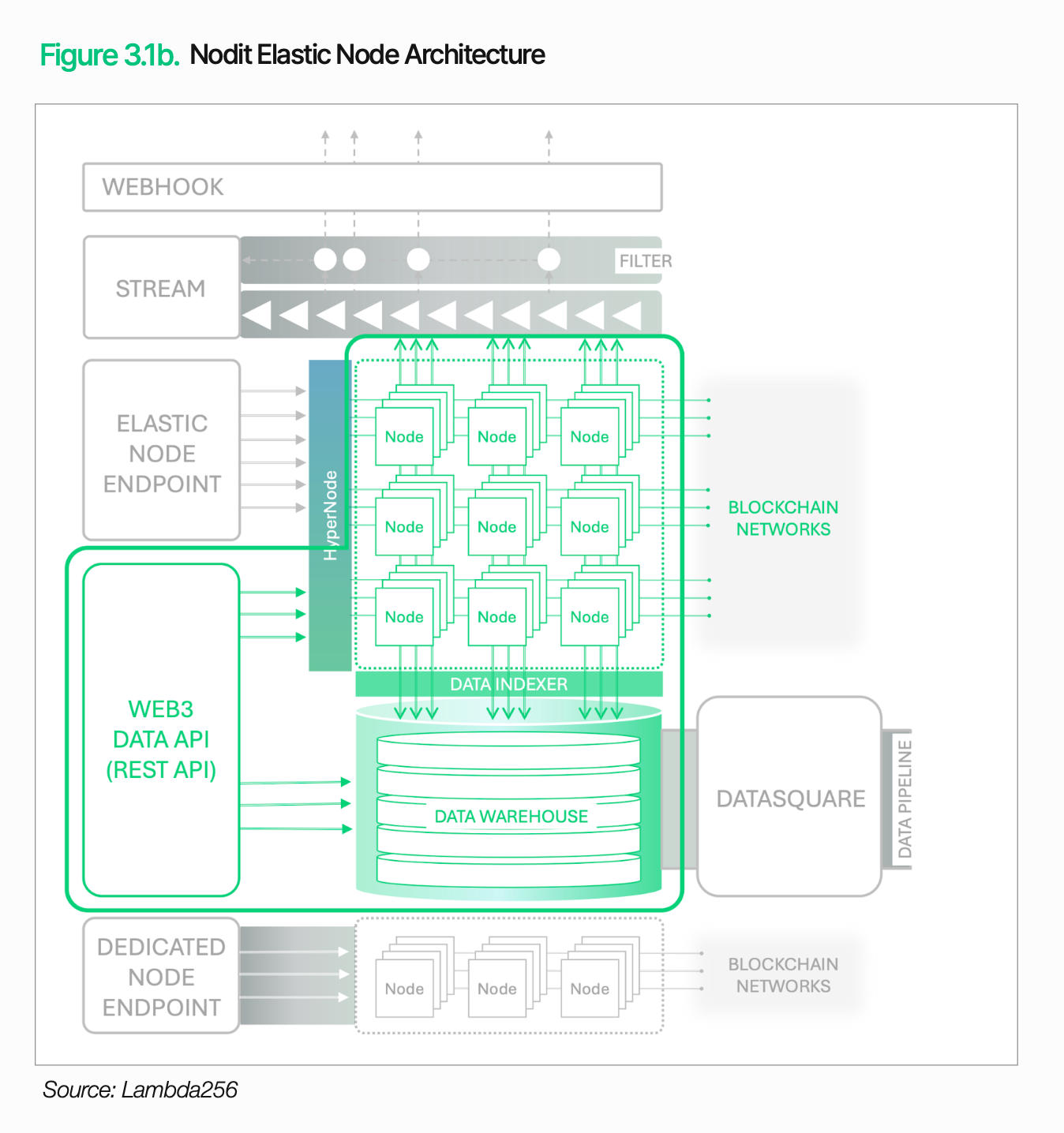

Among Korea’s top five digital asset exchanges, Upbit, Coinone, and Korbit operate on Nodit’s infrastructure. Daily API requests exceed 100 million, with approximately 1,700 active nodes. This demonstrates capacity in environments that demand high-volume traffic handling and operational stability.

The onchain access layer extends beyond data retrieval. The data and transaction information secured at this stage serve as a shared foundation for downstream functions including issuance, settlement, clearing, and compliance, all operating within the same architecture. Financial institutions can extend digital asset services incrementally by integrating required functions into existing systems and workflows, rather than building separate infrastructure for each.

3.2. Offchain Control

Establishing onchain access does not complete a digital asset service. An additional step is needed to connect on-chain transaction results and status data into traditional financial workflows. Blockchain transactions must be processable within existing operational procedures and internal controls to function as financial services. Offchain Control serves this role.

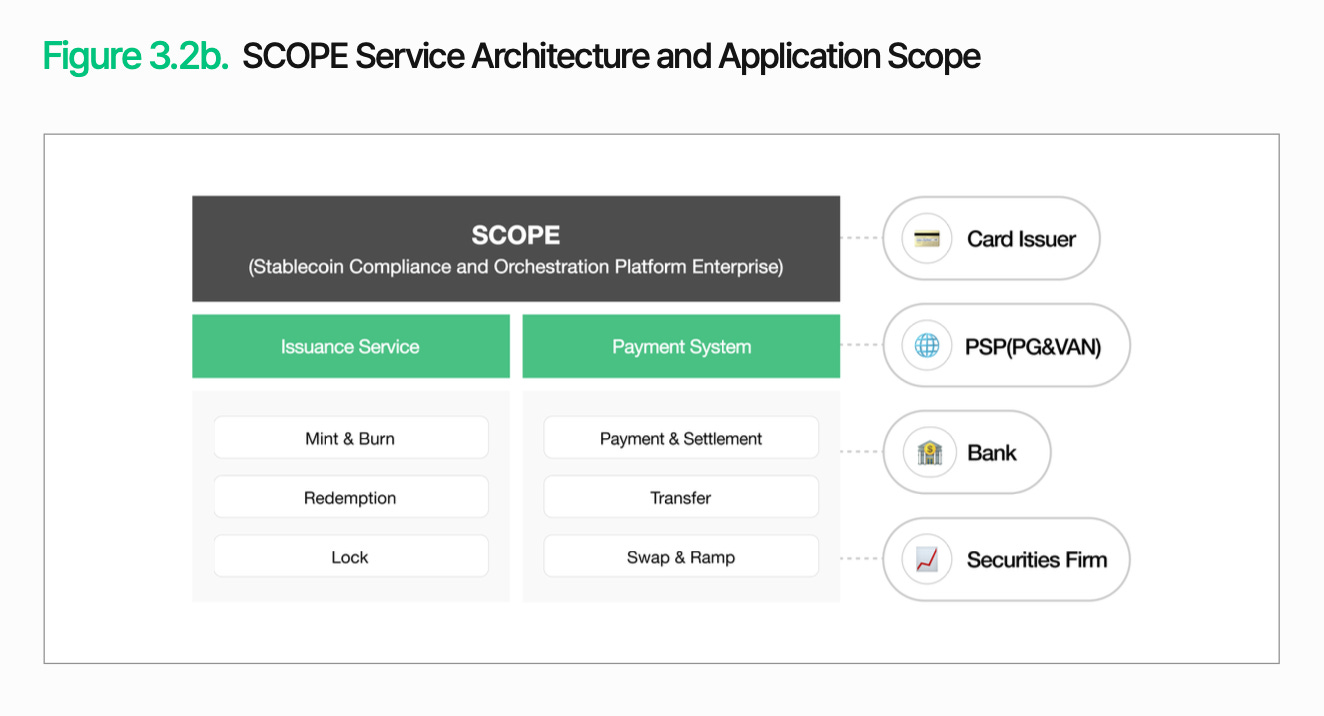

The core of offchain control is incorporating blockchain transactions into existing financial operations. SCOPE manages issuance, distribution, settlement, and clearing within a single structure, connecting blockchain-based transactions to traditional back-office workflows. Importantly, this does not require full replacement of existing systems. Institutions can integrate required functions into current workflows incrementally.

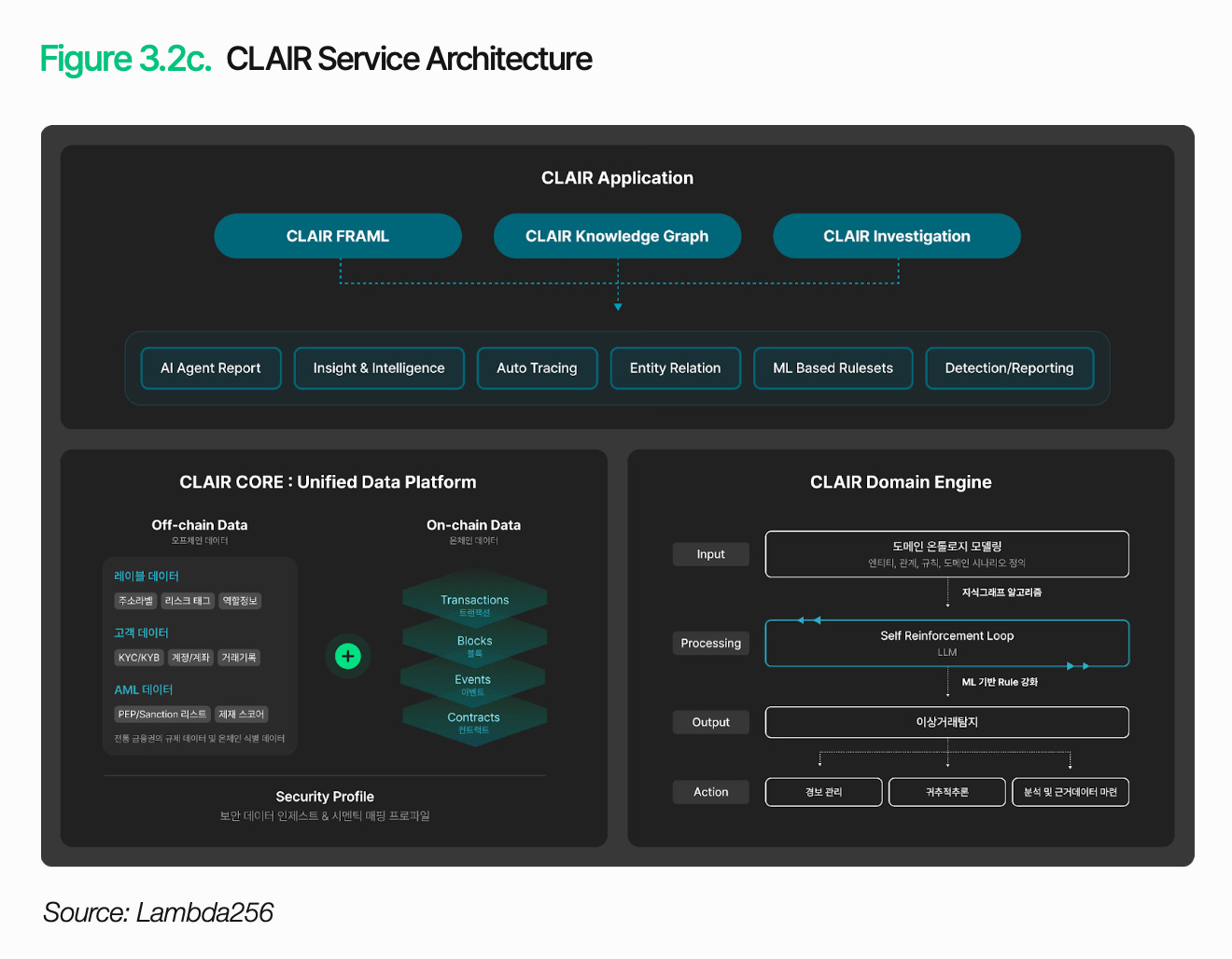

Incorporating transactions into operations is not sufficient. Institutions must also interpret the context and risk of each transaction. CLAIR analyzes fund flows and identifies risk signals. It maps wallet relationships through an ontology-based knowledge graph and reads transaction pattern context, enabling tracing beyond simple anomaly detection to the full flow of funds.

This capability is validated in practice. Over ten overseas law enforcement agencies and exchanges have adopted CLAIR as a white-label solution for their own analytical tools. Domestic partnerships with security, audit, and regulatory solution providers continue to expand.

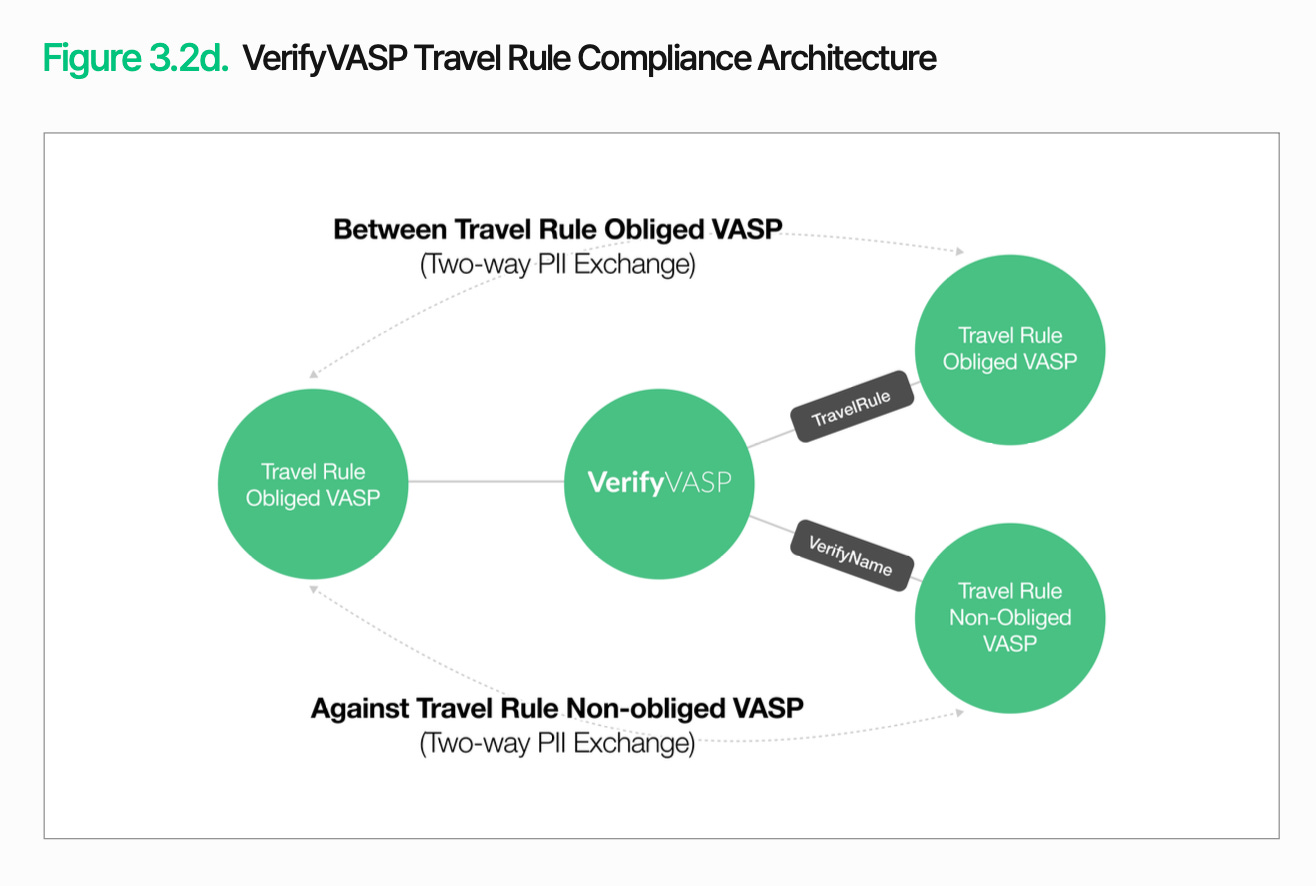

Alongside transaction monitoring, counterparty verification is also required. VerifyVASP handles this function. For financial institutions to manage on-chain transactions within existing controls, they must verify not only fund flows but also counterparty information. This enables institutions to manage counterparty risk consistently, regardless of specific regulatory mandates.

The core of offchain control is making on-chain transactions manageable within traditional financial operations and controls. Transaction execution, fund flow interpretation, and counterparty verification must connect within a single structure for digital asset services to function as financial services. Institutions can maintain existing systems while integrating required functions incrementally.

4. Key Digital Asset Adoption Scenarios

Digital asset adoption does not follow a single path. Banks, card companies, and securities firms each approach adoption differently based on their business objectives and operational structures. Infrastructure requirements and priorities vary accordingly. The following sections examine major scenarios by sector, identifying the challenges that arise and how they can be addressed.

4.1 Stablecoin Payment Adoption

Assume a major domestic card company, TigerPay, introduces stablecoin payments for foreign visitors.

As inbound tourism grows, the limitations of existing payment infrastructure become clearer. Cross-border card transactions incur intermediary fees and exchange rate margins, and merchant settlement takes time. Tourists also bear the cost of currency conversion and opaque exchange rates. To reduce this friction, TigerPay aims to accept direct payments in dollar-based stablecoins from tourists, while merchants receive settlement in KRW or KRW-pegged stablecoins.

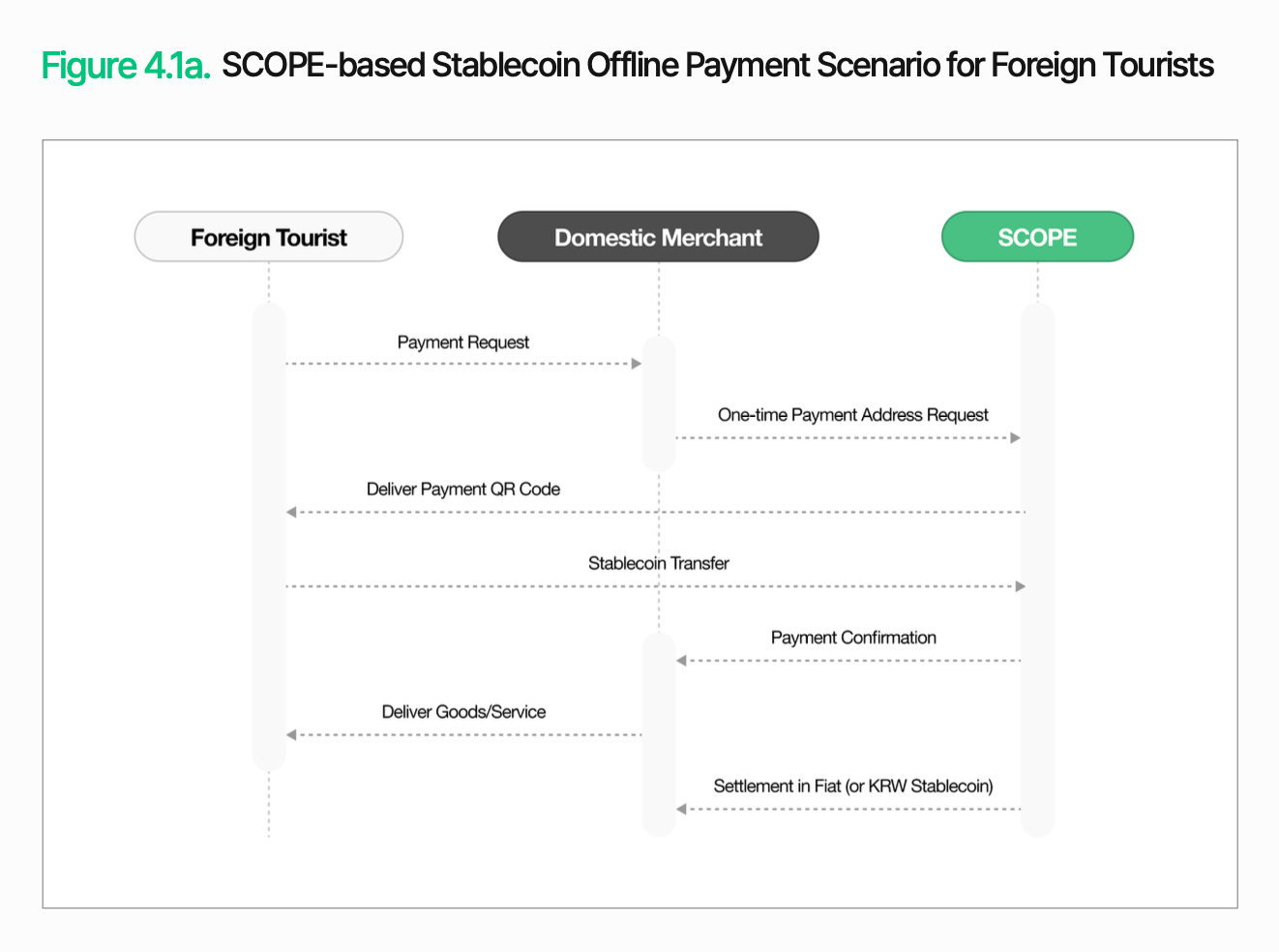

Offline payment is relatively straightforward. When a domestic merchant initiates a payment, SCOPE generates a one-time payment address and delivers it to the tourist as a QR code. The tourist sends stablecoins from their wallet to that address. Once confirmed, the merchant provides the goods or service. The merchant is then settled in fiat or KRW stablecoins. Tourists pay with familiar digital assets, and merchants maintain their existing settlement process.

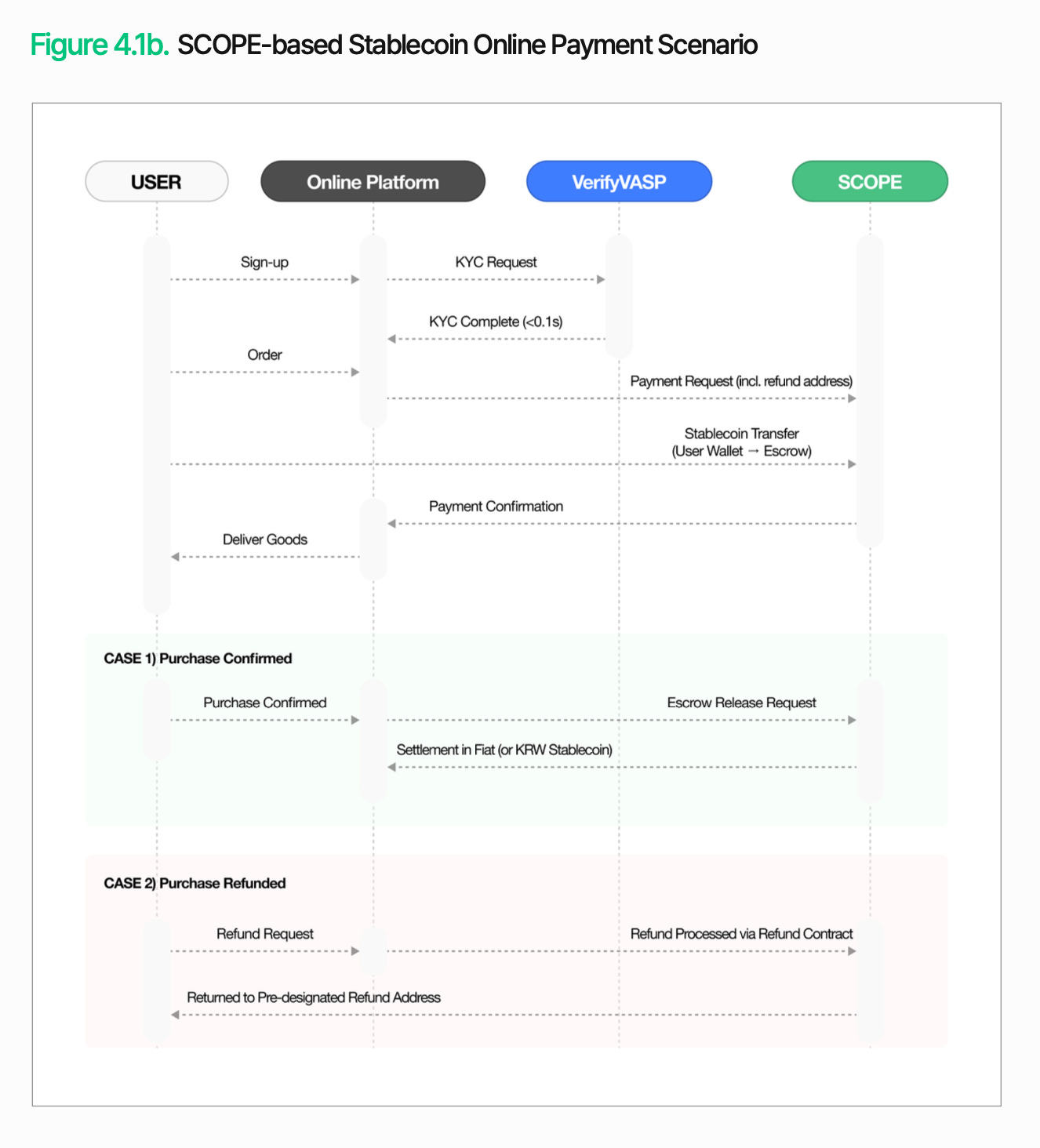

Online payment differs structurally. Because delivery and potential refunds occur between order and settlement, funds need to be held rather than transferred immediately to the seller. When a user initiates payment, VerifyVASP performs KYC, and funds are deposited into SCOPE’s escrow structure. Once predefined conditions such as delivery confirmation are met, settlement proceeds. If a refund is required, funds are returned to a pre-designated refund address. This enables payment, settlement, and refund to be handled within a single flow, even for online transactions.

4.2 Security Token Issuance Platform

Assume a domestic securities firm, Tiger Securities, tokenizes a commercial real estate fund.

As security token regulation takes shape, building STO platforms has become a practical priority for securities firms. Tiger Securities aims to tokenize an existing commercial real estate fund to open it to smaller investors. Under the current structure, minimum investment thresholds are high, redemptions take time, and transferring shares between investors involves complex procedures. Tokenization transforms this into a structure that enables smaller-denomination issuance and more flexible trading.

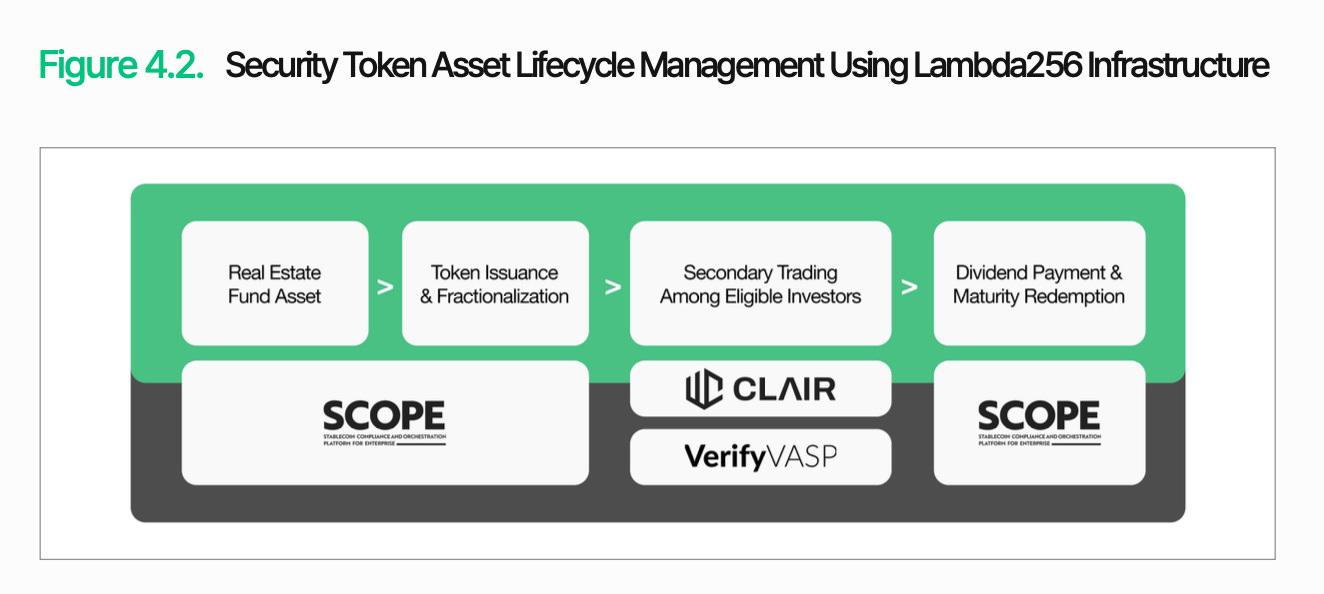

The core challenge lies not in issuance itself, but in post-issuance management. Security tokens are classified as securities, requiring lifecycle-wide controls over holding eligibility, trading conditions, and transfer restrictions. SCOPE provides the foundation for this lifecycle management. It structures functions such as issuance, supply management, redemption, burn, and transfer restrictions as modules. Policies like whitelist-based investor restrictions and transfer blocks during lock-up periods can also be configured.

For this structure to become an operational service, data integration and regulatory response must also be in place. Nodit synchronizes on-chain data such as token balances, dividend records, and transaction histories with existing securities systems in real time. CLAIR tracks fund flows and monitors for anomalous transactions. VerifyVASP handles investor KYC and counterparty identity verification. At the dividend and redemption stages, SCOPE’s batch disbursement function enables efficient fund distribution to investors.

This structure is not limited to a single product. Whether the tokenized asset is bonds, private equity, or commodities, the same infrastructure for issuance, management, and regulatory compliance applies. The platform Tiger Securities builds is not a one-time system for a single product, but a scalable foundation capable of supporting a range of security tokens.

5. Conclusion

The shift has already begun. What creates the gap in digital asset infrastructure is no longer whether blockchain technology has been adopted. What matters is whether blockchain-based transactions can actually work within the operations and controls of existing finance. The challenges financial institutions face ultimately converge on three areas: regulatory compliance, technical compatibility, and operational reliability.

Lambda256 offers a unified financial middleware solution to address these challenges. Nodit delivers blockchain data in formats existing systems can use. SCOPE connects the issuance, transfer, and settlement of assets. CLAIR and VerifyVASP complement control and regulatory response through transaction flow analysis and counterparty verification. The significance of this architecture is not in listing individual functions, but in enabling financial institutions to integrate digital asset capabilities into existing workflows incrementally.

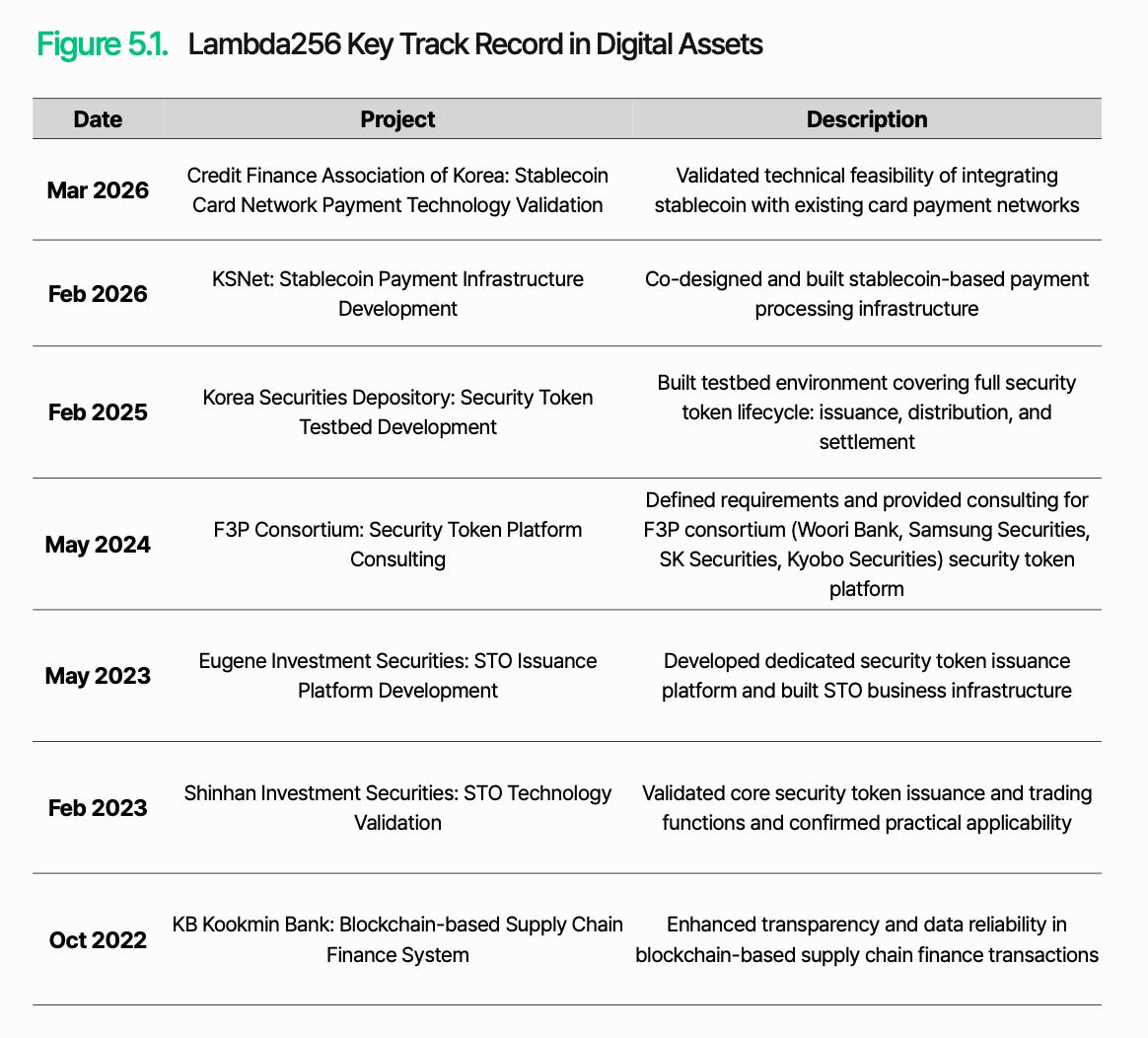

This framework is not a finished answer to digital asset infrastructure. As regulation and markets evolve rapidly, regulatory alignment, system integration, and operational reliability must continue to be refined and validated through real-world application. Still, collaboration with institutions such as the Credit Finance Association of Korea and Korea Securities Depository demonstrates that this approach is not a concept on paper but one being reviewed and tested in actual financial environments.

Ultimately, the gap in digital asset infrastructure is not determined by who adopted new technology first, but by who can design it into an operable structure within the existing financial system and execute a stable transition.

Disclaimer

This report was partially funded by Lambda256. It was independently produced by our researchers using credible sources. The findings, recommendations, and opinions are based on information available at publication time and may change without notice. We disclaim liability for any losses from using this report or its contents and do not warrant its accuracy or completeness. The information may differ from others’ views. This report is for informational purposes only and is not legal, business, investment, or tax advice. References to securities or digital assets are for illustration only, not investment advice or offers. This material is not intended for investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo following brand guideline. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.