Ethena’s declining sUSDe share does not signal a failure of the protocol. It reflects a structural shift in the market. This piece examines how the DeFi landscape is changing.

Key Takeaways

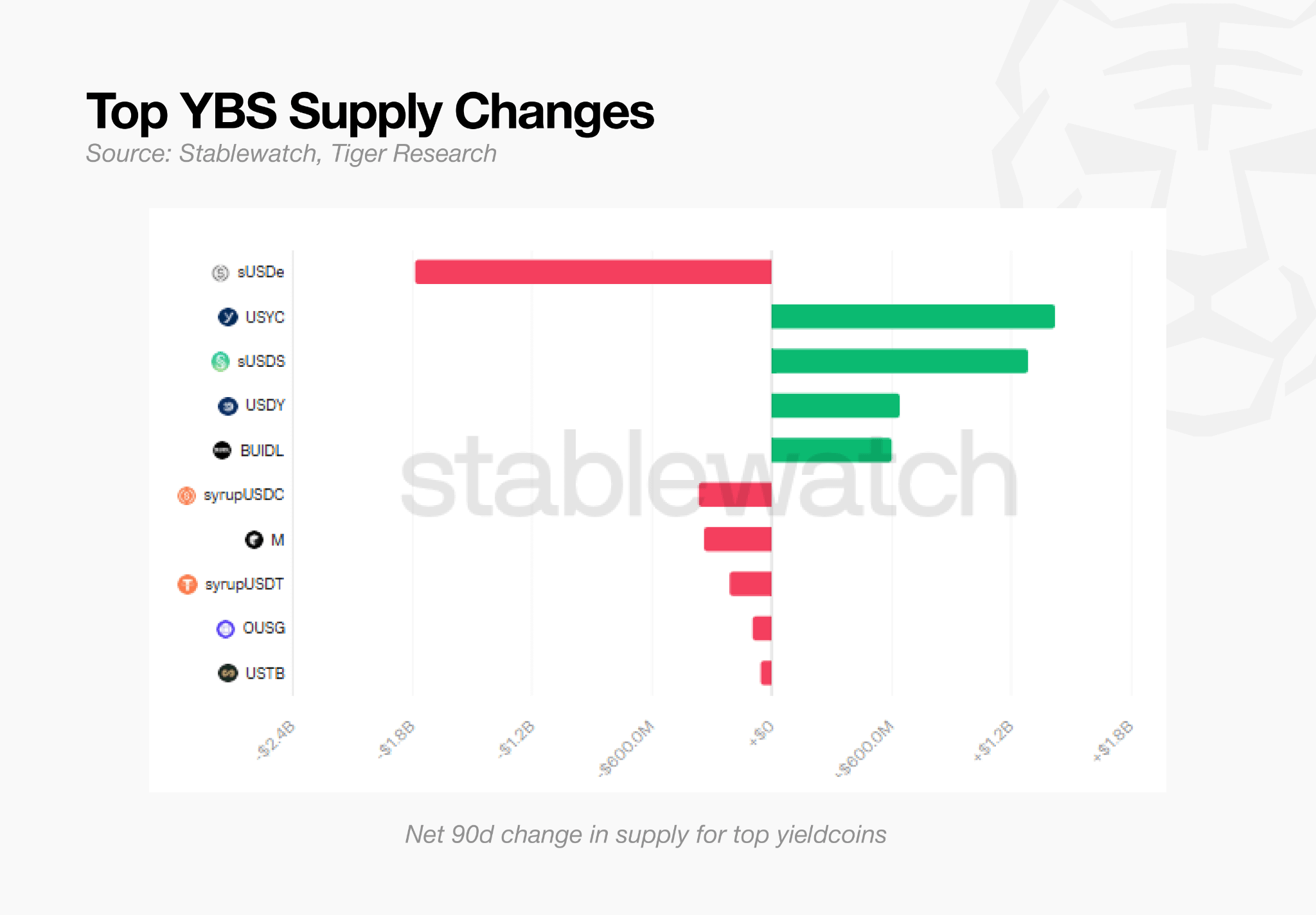

sUSDe supply halved while capital moved into USYC and sUSDS, both offering lower yields. This is not capital flight from the market, but a change in selection criteria within it.

APY is no longer the line that separates assets. What matters more is whether they can be adopted as collateral, savings products, or reserves.

S&P assigned Sky the first credit rating ever given to a DeFi protocol.

Ethena is overhauling its collateral structure in April 2026, shifting from a synthetic model to a hybrid one. A single yield source is no longer enough to survive in the YBS market.

DeFi is shifting from a market that produces yield to one that imports and distributes yield from traditional finance. The stronger the base, the stronger the structures built on top.

1. What’s Behind sUSDe’s Decline

A Yield-Bearing Stablecoin (YBS) is a dollar-pegged token that accrues interest simply by being held. USDC and USDT work like cash. A YBS works like a deposit. Its value rises with an interest rate.

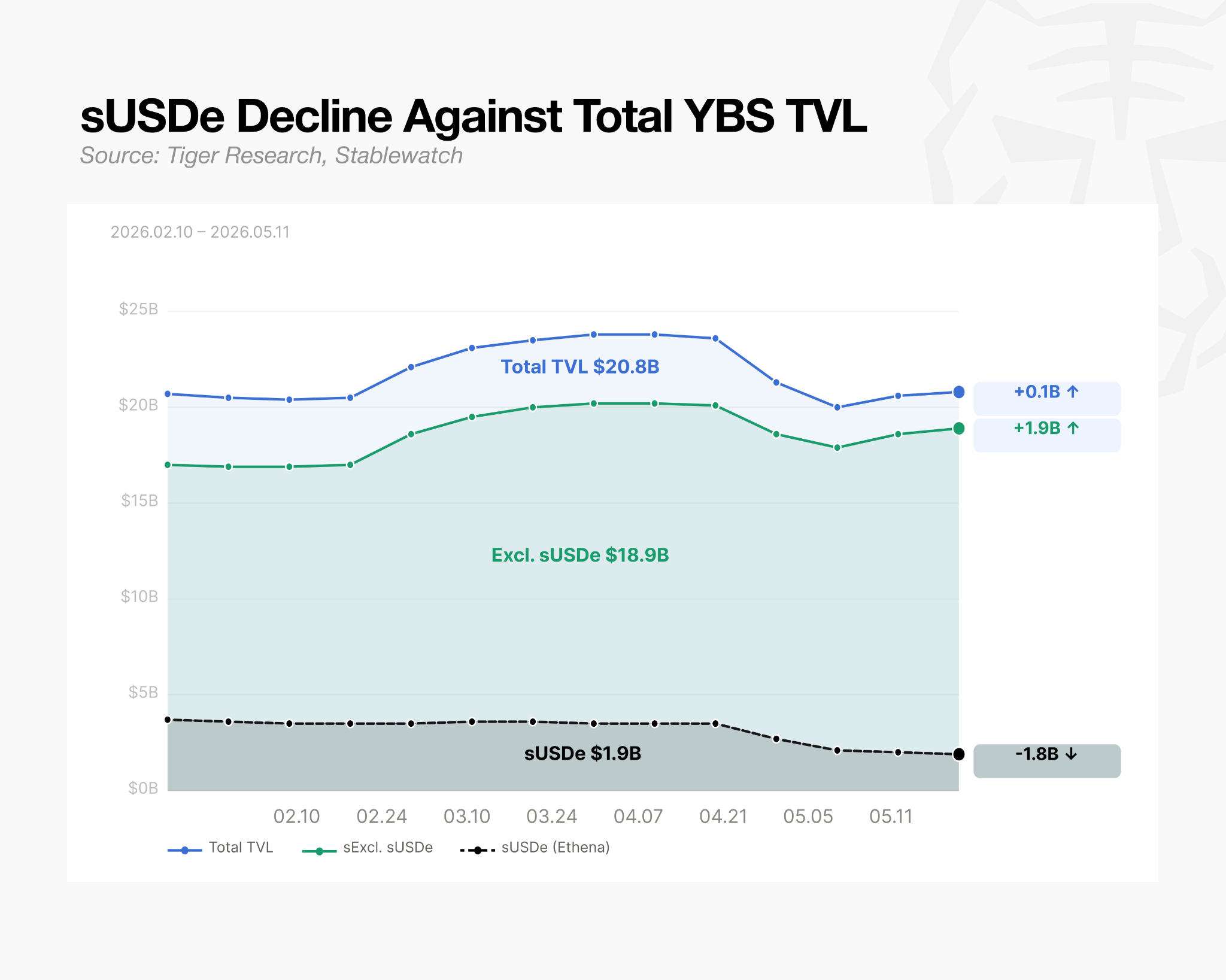

Something unusual is happening in this market. Ethena’s flagship product sUSDe, which once held more than 30% of the YBS market, has seen its supply decline by roughly $1.8B over the past 90 days, about 49% off its peak. No hack. No protocol issue.

The market itself did not shrink. Total YBS TVL actually rose during the same period. Over 90 days, USYC (Circle’s Treasury-backed stablecoin) drew $1.4B in inflows and sUSDS (Sky’s hybrid stablecoin) drew $1.2B. Combined, those inflows were larger than the decline in sUSDe.

The flows alone tell a different story. Capital hasn’t left. It’s rotating within the same market.

2. What Matters More Than APY, the Holder Base and the Underlying

On APY alone, there is no reason for capital to move. On a 30-day basis, USYC sits at around 3% and sUSDS at around 3.6%. sUSDe is actually higher at around 4%. If yield were the driver, capital should have concentrated in sUSDe. The shift appears to come not from yield, but from two other factors. (1) the holder base, (2) the underlying assets.

2.1. Retail and Institutions

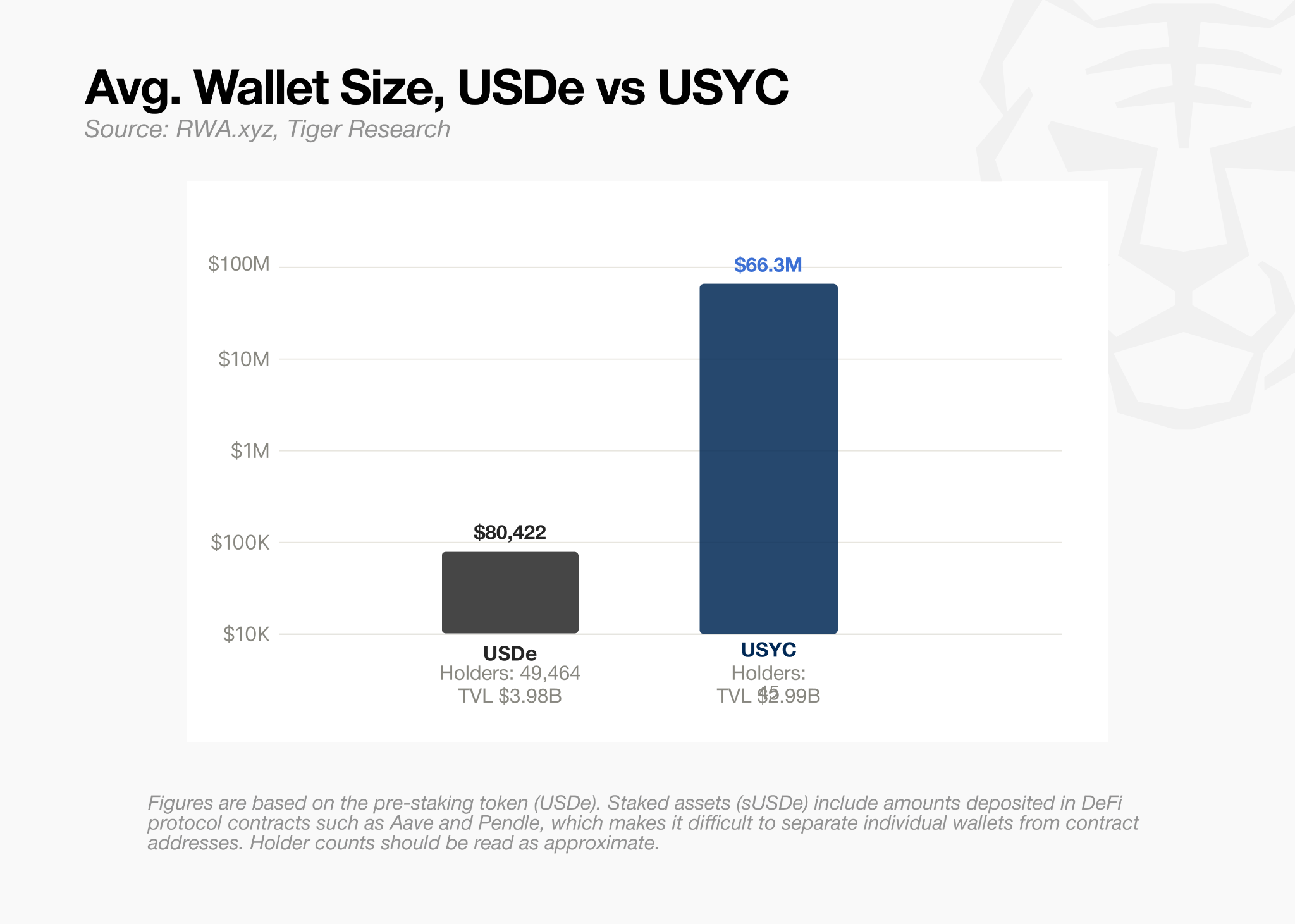

By average holdings per wallet, a USDe holder is roughly 1/800 the size of a USYC holder. Strip out the large block purchases and the gap widens further. USYC was structured from the start to attract only large capital. USDe leaned heavily on retail.

USDe and USYC diverge on holder base.

For USDe, the investment thesis of both retail and institutional holders centers on yield. They enter for the APY and exit when it slips. USYC takes a different approach. No retail, institutional utility at the core.

USYC is open only to qualified investors and carries a $100K minimum purchase. In July 2025, Binance adopted it as collateral for institutional derivatives. Once traders could post a yield-bearing asset on the largest exchange, demand followed. $2.54B has been issued on BNB Chain alone.

2.2. Delta-Neutral vs. RWA

The difference between USDe and USDS comes from their reserve assets. What institutions want is predictability, in both how the yield is generated and how it moves.

USDe runs a delta-neutral structure. Crypto collateral on one side, perpetual futures shorts on the other, offsetting price moves. Yield ties to perpetual funding rates. In the 2024 bull market, sUSDe APY exceeded 47%. As the market turned sideways, it eased into the 3% range. The swing was more than tenfold in just a few months. Yield moves in step with market conditions.

USDS is backed by short-duration US Treasuries and money market funds. Yield ties to real-world interest rates. APY sat in the 9% range in late 2024 and took more than a year to ease into the 3% range.

This difference shows up in S&P’s assessments as well. In August 2025, S&P Global assigned Sky Protocol a B- credit rating, the first ever issued to a DeFi protocol. The grade itself is not high. What matters is that a DeFi protocol received a credit rating at all.

For institutions, predictability matters as much as yield. sUSDe can deliver higher returns depending on market conditions, though institutional desks may find it harder to underwrite.

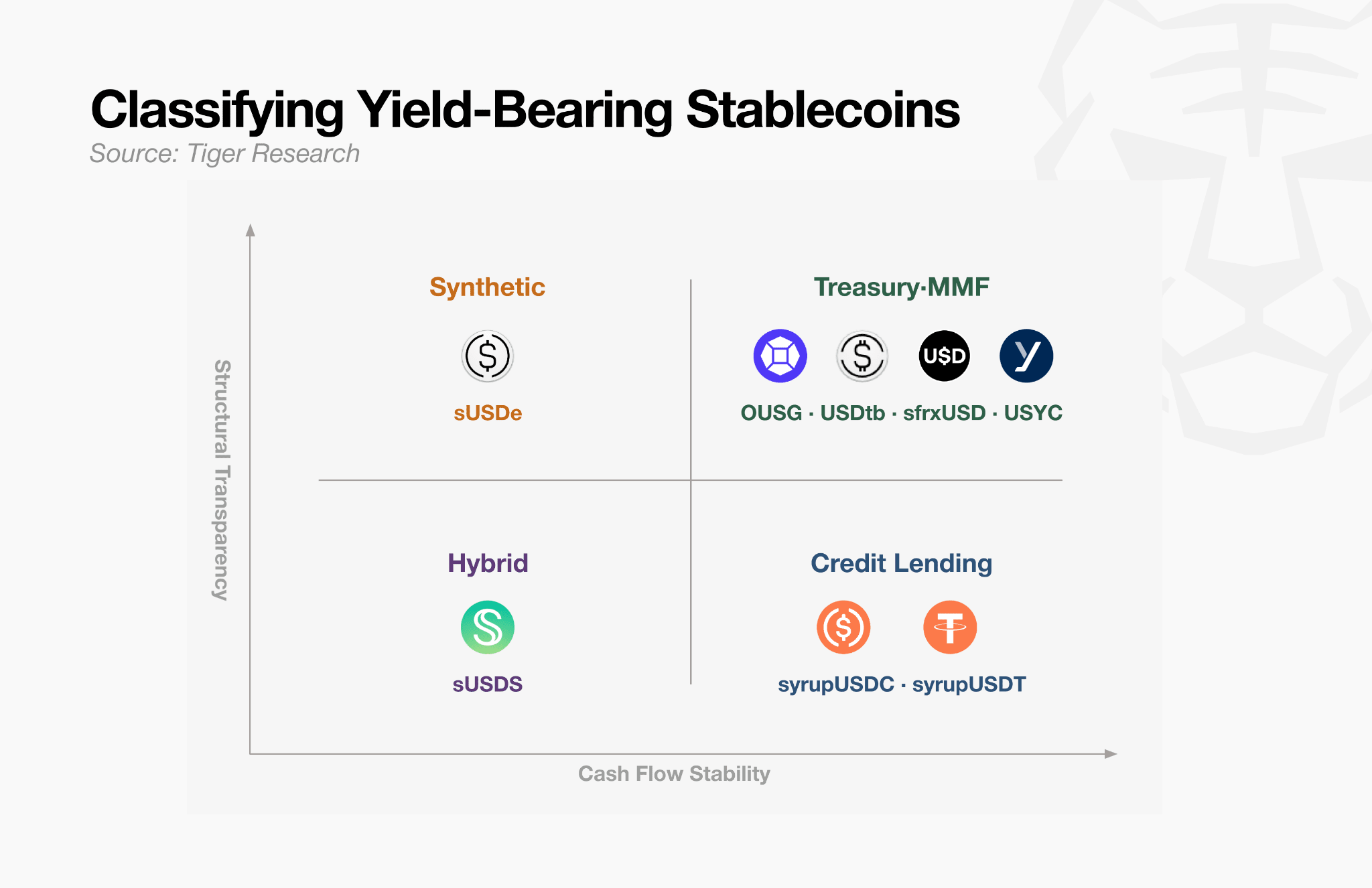

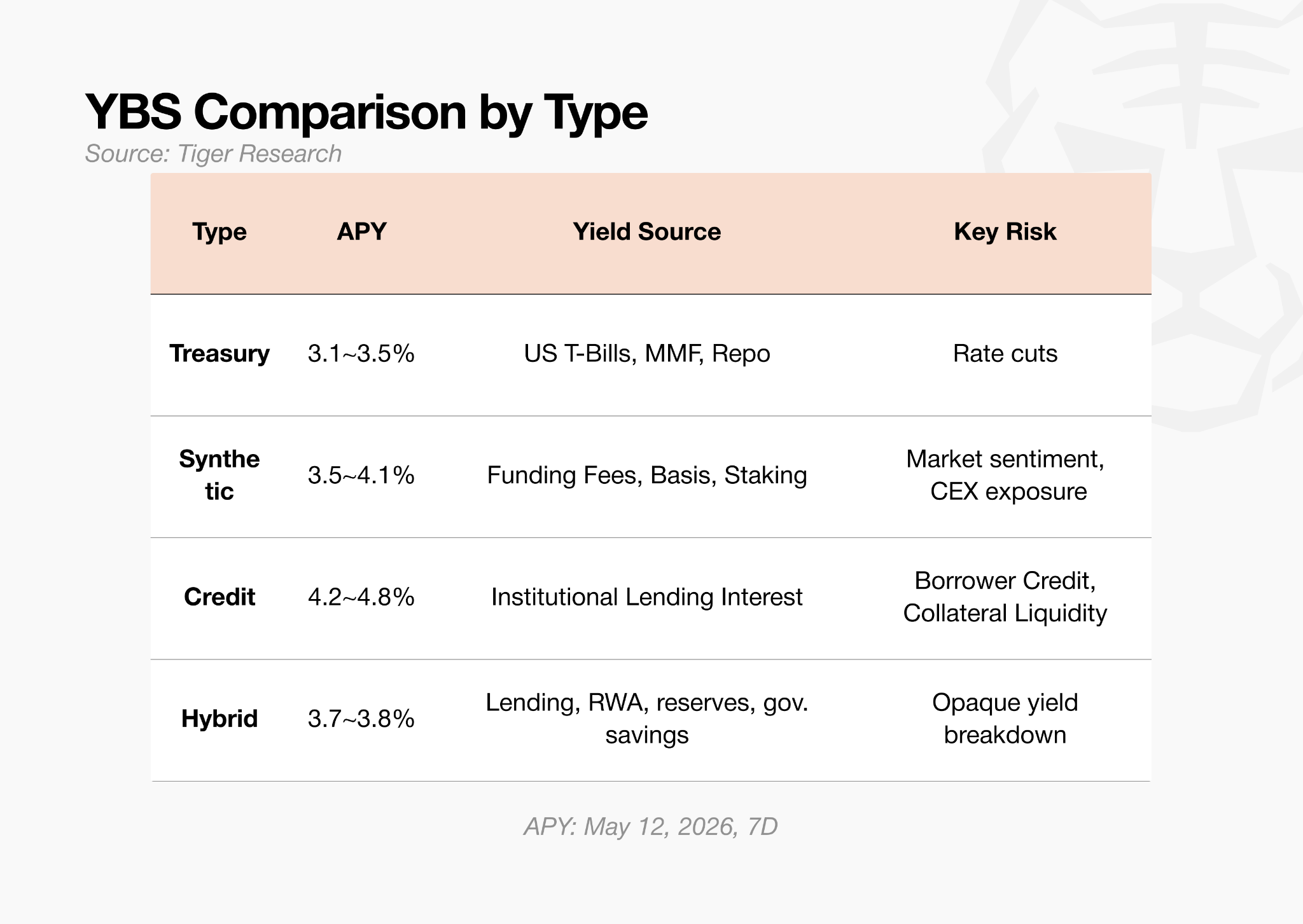

3. The YBS Market’s Direction

YBS assets sort along two axes. “How stable is the yield”, and “can the yield source be verified”. A 4% APY is not always the same 4%. The kind of risk depends on who’s paying the interest. And most capital is moving toward the more predictable side.

Treasury-backed YBS (OUSG, sfrxUSD, USYC) is the easiest to describe.

Short-term Treasury yield flows from the issuer to the holder through the operating layer. As of May 2026, the average APY ranges from 3.1% to 3.5%. The constraint is that yield is tied to Treasury rates.

Synthetic YBS (sUSDe) offers transparent yield sources but is sensitive to market conditions.

Perpetual futures funding fees are the primary revenue stream. The yield is verifiable on-chain, but it swings hard with market conditions. APY exceeded 15% in September 2025 and sits in the 4% range on a 7-day basis as of May 12, 2026.

Credit-based YBS (syrupUSDC, syrupUSDT) is high on yield stability but low on verifiability.

Through Maple Finance, interest paid by hedge funds and trading firms flows back to holders. The fixed-rate structure in the 4% range keeps volatility low. Borrower credit and collateral values are hard to inspect from outside.

Hybrid YBS (sUSDS) sits at neither extreme.

The yield blends Spark lending fees, RWA returns, reserve management, and the governance-set Saving rate. The 7-day rate stands at 3.6%, below sUSDe. On the risk side, the lack of a single point of failure helps. The trade-off is that decomposing the yield structure from outside is difficult.

The classification points to a single pattern. With the exception of Ethena’s synthetic model, every category is bringing traditional finance’s yield sources on-chain.

4. Ethena Already Knows

The first signal that Ethena recognized its structural limits came with the launch of USDtb. USDtb is a Treasury-backed dollar that uses short-term US Treasuries as its reserve. It was built to cushion USDe during periods when funding rates flip negative.

In April 2026, Ethena went a step further. It overhauled USDe’s collateral structure outright. Ethena cut the perp share to 11% of total collateral and added new categories. Stablecoin reserves, DeFi lending, CLOs, investment-grade corporate bond funds, short-term credit.

Ethena is also studying a plan to fold a gold-perp-based delta-neutral strategy into USDe’s collateral. The structure applies the same approach used for BTC and ETH to gold (PAXG, XAUT). The Risk Committee has completed its formal review.

This was the largest structural change since launch. In effect, Ethena acknowledged that a delta-neutral strategy built on crypto assets alone no longer holds.

USDe and sUSDe started as synthetic but are evolving into a hybrid. The shift confirms that a single yield source is no longer enough to remain competitive in the YBS market.

5. Foundations First

The idea of DeFi importing yield from traditional finance, rather than generating it natively, can feel at odds with the philosophy of decentralized finance. That does not mean DeFi is finished.

Blockchain set out to build a decentralized internet and ended up running on the internet itself. Without the internet, there would be no blockchain. Stablecoins set out to replace the dollar and ended up running on the dollar. They went on to drive DeFi’s rise. A traditional foundation has never blocked innovation in the layers built above it.

YBS can follow the same path. BUIDL is already collateral for USDtb. USDtb has become the reserve for USDm, MegaETH’s native stablecoin. New money legos are already stacking on top of Treasury-backed YBS.

As Treasury-backed YBS settles into infrastructure, yields will compress and the range of underlying assets will narrow. The alpha available from any single asset will keep shrinking. Just as the internet became infrastructure and access costs converged to zero, YBS will follow the same path. Stability and composability will matter more than yield.

As infrastructure matures, the experiments built on top of it can run on stronger fundamentals. Early synthetic dollars were unsustainable because their underlying assets were unstable.

Earlier DeFi yield structures were built on sand. They leaned on altcoin prices, token incentives, and leverage demand. Now verified yield sources are forming the base, with on-chain financial structures being built on top.

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.