The DeFi market spent years stacking yield on top of yield, riding a sugar rush of artificially high returns. That era is over. Now, DeFi is plugging into real-world assets (RWA) as its actual power grid, opening a new chapter.

Key Takeaways

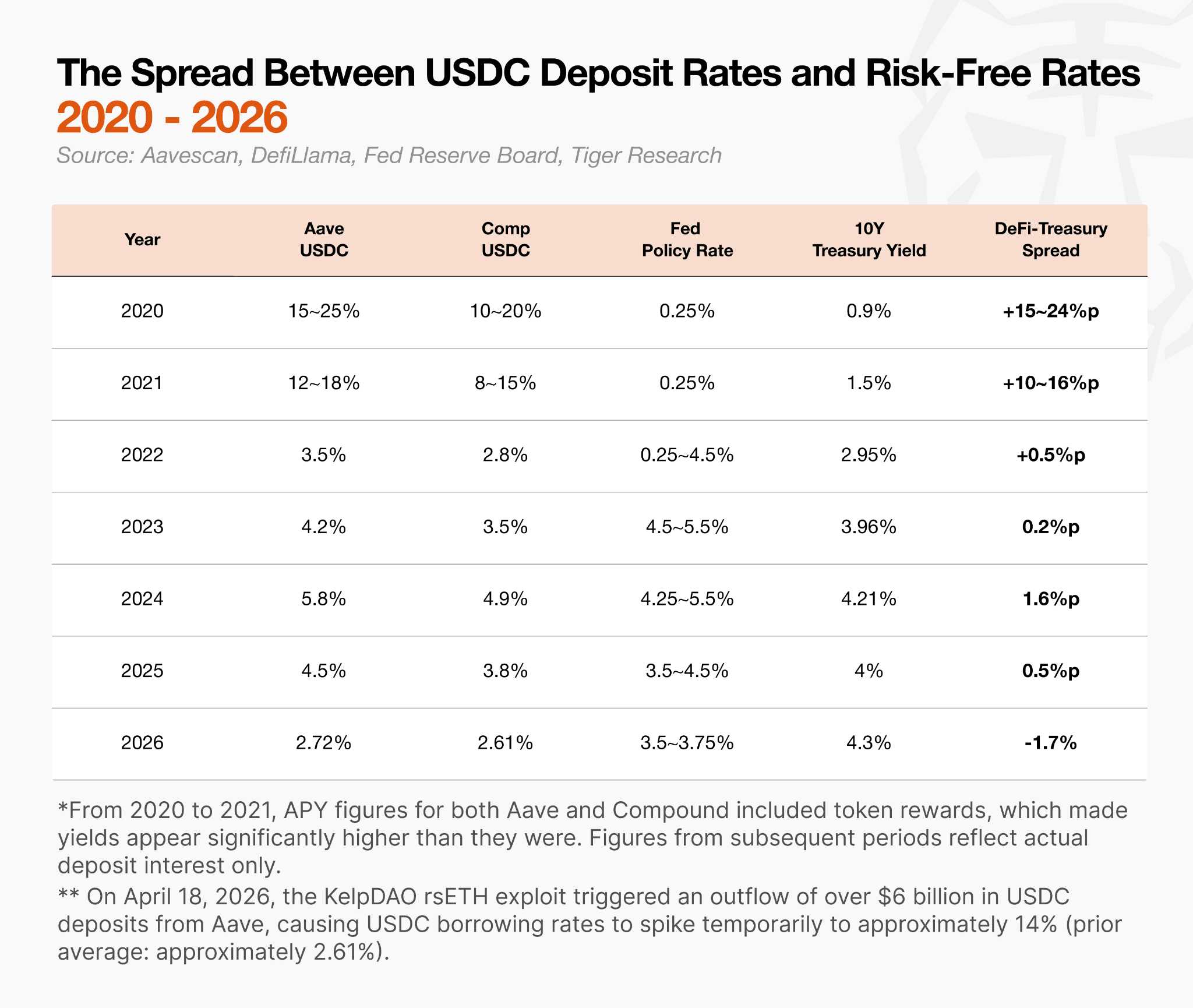

Aave V3’s USDC deposit rate stands at 2.7%, below the U.S. 10-year Treasury yield of 4.3%. DeFi’s dopamine hit is fading.

The market is not dead. Yields have fallen, but RWA and stablecoins have grown into a multi-hundred-billion-dollar market, evolving in a new direction.

The failures of Compound, Curve, and Olympus share a common lesson. Any structure where tokens prop up other tokens collapses the moment external capital stops flowing in.

DeFi was a power strip with no outlet. RWA connects that circuit to a real external power grid.

The market is maturing. It is anchoring to real underlying assets (RWA) and showing signs of coordinated accountability, as seen in initiatives like DeFi United.

1. Falling Yields, Growing Market

DeFi is no longer a high-yield product.

Since 2022, the spread between DeFi and government bonds has narrowed toward zero and, in some periods, inverted. As of April 2026, Aave V3’s USDC deposit rate of approximately 2.7% sits below both the Fed funds rate (3.5%) and the 10-year U.S. Treasury yield (4.3%).

There used to be a clear reason to take on risk.

On-chain yields were incomparably higher than bank deposits. That is no longer the case. If the returns on DeFi, after absorbing all on-chain risks such as hacks and depeg events, fall below those of traditional finance, retail users have less reason to actively engage with DeFi.

Yet the market itself is growing in a different direction. DeFi yields have fallen, but RWA and stablecoin markets, converging with traditional finance, are scaling into the hundreds of billions. Institutional entry has played a major role in this shift.

However, institutions often overlook DeFi’s history and existing community, bringing in the conventions of traditional finance wholesale. Before institutional entry, DeFi was an incentive-driven market. Some protocols gained market recognition through incentive strategies and, in doing so, shifted the market paradigm. That model persists in DeFi today, and Aave, a protocol that emerged during DeFi Summer, now serves as the benchmark rate provider for DeFi protocols.

Understanding the players who have remained in the market is essential groundwork for new institutional entrants. This piece traces the protocols that drove DeFi’s defining narratives across its lifecycle, and the lessons the market drew from them.

2. DeFi’s History: From Experiment to Collapse to Reinvention

DeFi did not begin as a market built on incentive promises. The starting point was simple: “Can we lend, exchange, and use assets as collateral on a blockchain, without intermediaries?”

The early phase was closer to financial experimentation. What mattered was the fact itself: loans without banks, exchange without exchanges, liquidity created by anyone with collateral. But after 2020, the market moved quickly in a different direction. Token incentives became the primary mechanism for attracting capital. Countless protocols and ideas emerged, but only a handful survived. The market learned from each narrative and kept adjusting course.

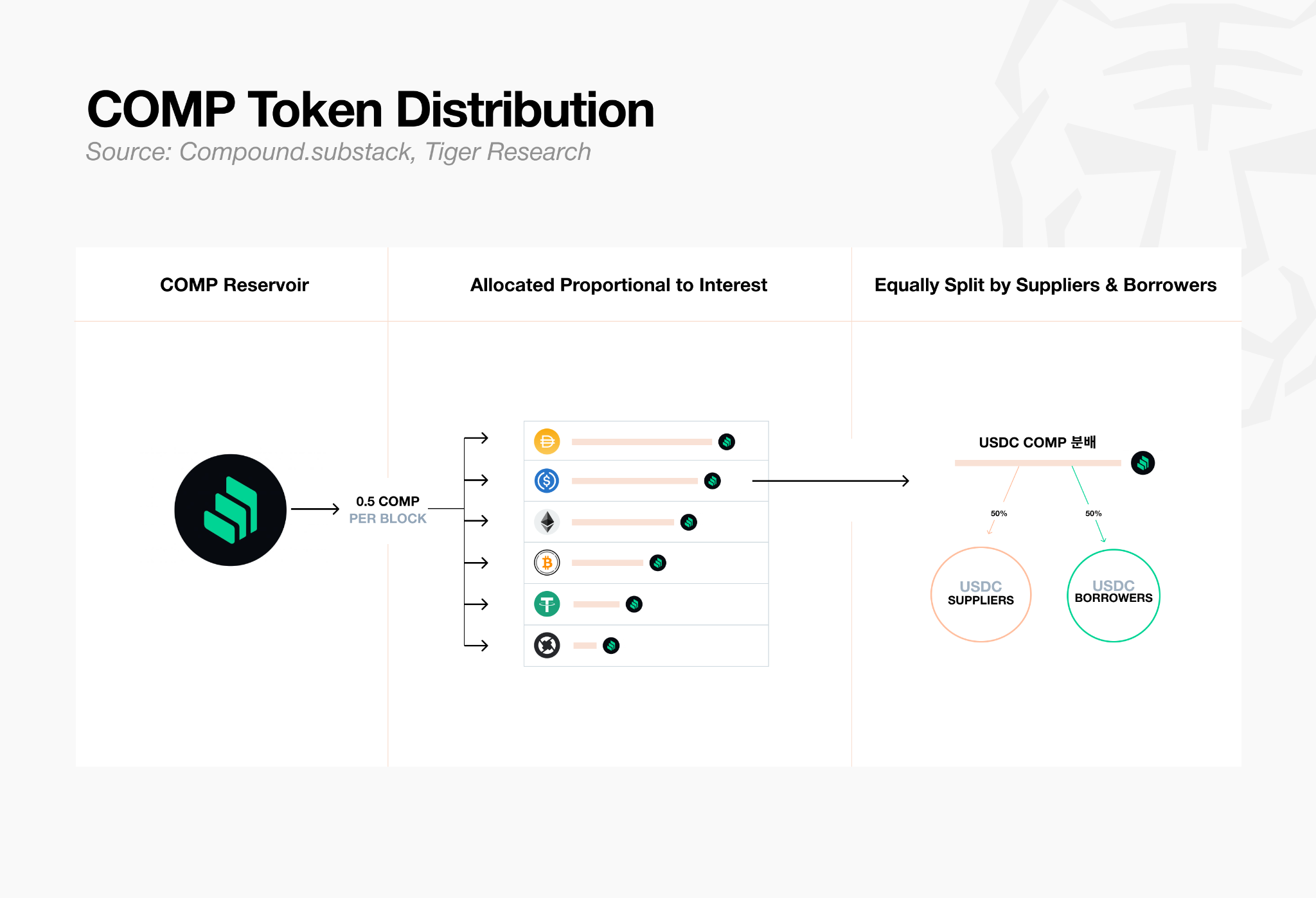

Compound incorporated its native token ($COMP) into yield incentives to attract large-scale liquidity. But when other projects replicated the same playbook, new inflows dried up and the structural fragility was exposed.

Curve transformed governance voting into a contest over which pools received yield, turning yield competition into a war over protocol control. The market learned that DeFi governance, too, can become a target for monopolization of power and incentives.

OlympusDAO was the most extreme case. It used high APY to demonstrate the possibility of DeFi owning its own liquidity without relying on external capital. However, much of its yield depended on new token issuance and incoming capital rather than real cash flow. When inflows slowed, both the price of its governance token OHM and confidence in the protocol collapsed together.

The lesson the market drew from all three: “When the source of yield is the protocol’s own token, the structure does not last.” This experience changed how users, builders, and institutions view DeFi.

And into that gap, new movements began to emerge: EigenLayer, Pendle, YBS, and RWA.

2.1. Compound: The Bubble Built by Token Distribution

In June 2020, Compound began distributing its governance token, $COMP, to users. Both depositors and borrowers received token rewards. In some periods, $COMP rewards exceeded borrowing costs, creating a situation where “borrowing money actually made you money.”

It was a new paradigm. As users flooded in, Ethereum gas fees surged, and paying tens of dollars for a single transfer became routine. Depositing and borrowing were no longer simple financial acts. They became tools for farming rewards, and yield-seeking capital moved rapidly between protocols.

This period is known as DeFi Summer. Uniswap, Aave, and Yearn Finance rose in quick succession, and on-chain finance solidified as an independent market. But what Compound ultimately built was a structure that attracted capital through token-dependent incentives, and where that capital in turn pushed up token prices. The tendency of DeFi users today to react sharply to yield rates, liquidity, and reward structures was formed in this period.

2.2. Curve and veCRV: The Opening of the Curve Wars

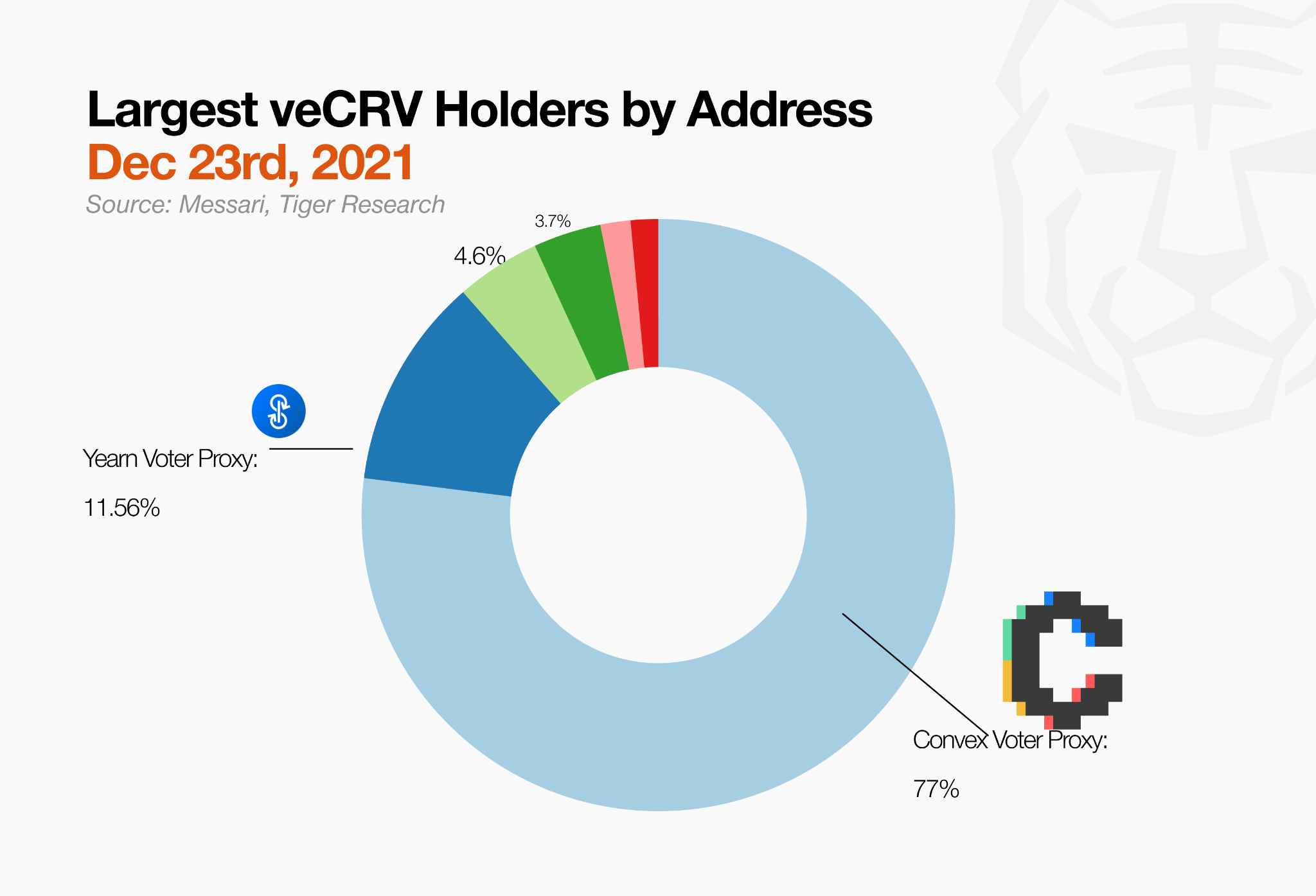

Curve began as something close to a stablecoin exchange. But the introduction of veCRV changed its character entirely. The longer users locked up CRV, the more veCRV they received, and that veCRV carried voting power over gauge weight allocations, determining how CRV rewards were distributed across pools.

From this point, the focus of competition shifted from yields themselves to the power to move them. Those with more veCRV could direct more incentives toward their own pools. Protocols naturally began competing to accumulate veCRV, and that competition became the Curve Wars.

Initially, the structure appeared attractive to both retail users and builders. Retail users earned higher rewards the longer they locked, while builders could reduce circulating supply and direct liquidity to target pools. This is why similar models spread across the ecosystem, including Balancer’s veBAL and Frax’s veFXS.

Over time, however, that power did not remain with individual users. Meta-protocols like Convex aggregated and locked CRV on behalf of users, offering boosted rewards in exchange for accumulating veCRV voting power. The Curve Wars expanded to Convex as its new battlefield.

What veCRV ultimately demonstrated was that control over yield is a stronger incentive than yield itself. And rather than holding that power directly, users delegated it to more efficient intermediaries like Convex. Curve revealed that governance rights in DeFi can become yield-generating assets in their own right, and that such rights are prone to consolidation.

2.3. OlympusDAO: A Golden Age Built on Game Theory

Even after Curve’s veToken mechanism emerged, liquidity remained DeFi’s most persistent challenge. Externally sourced liquidity left as soon as better incentives appeared elsewhere. This was mercenary capital.

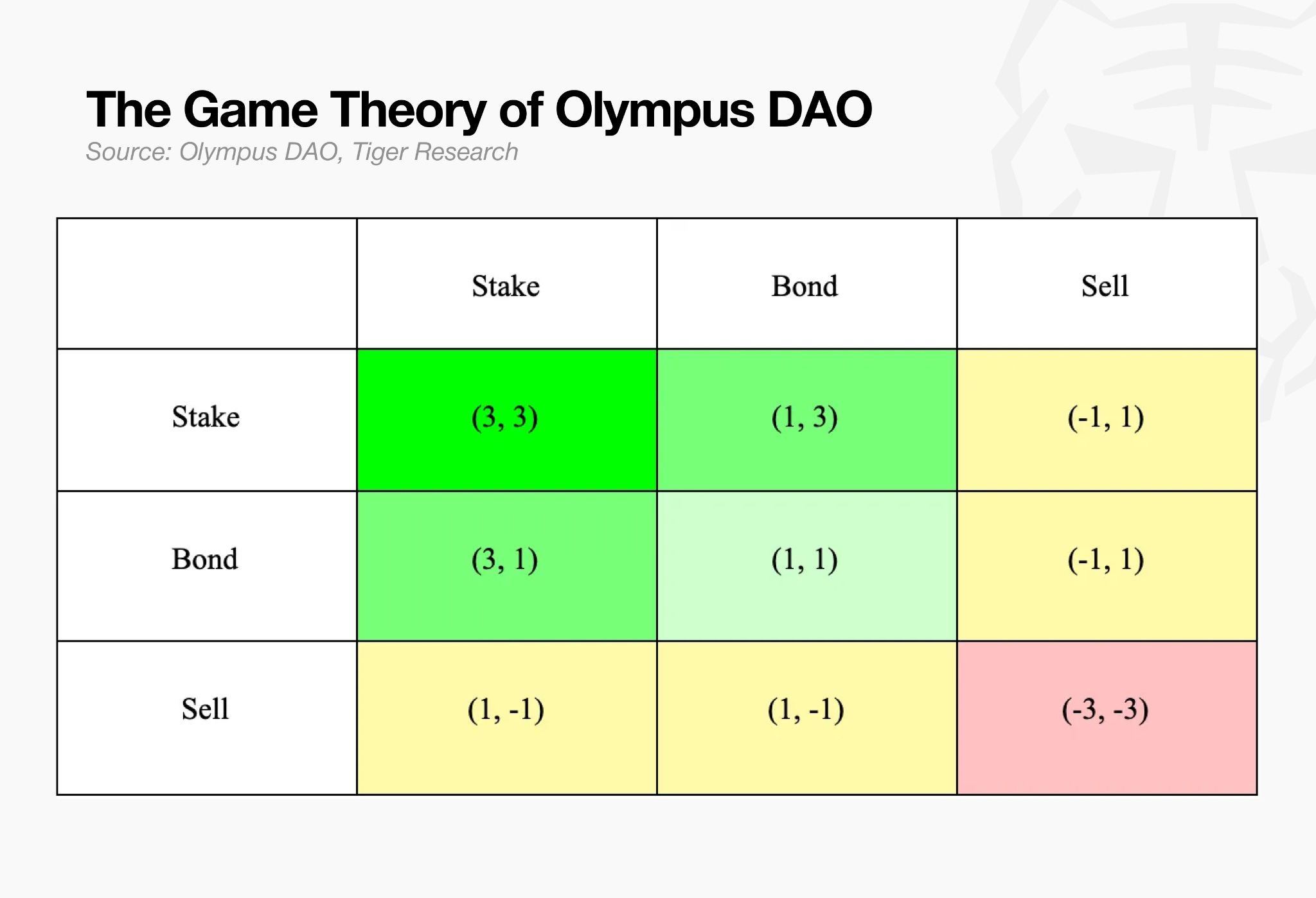

OlympusDAO, which emerged in the second half of 2021, drew attention as a proposed solution. Its core had three elements: Protocol-Owned Liquidity, where the protocol itself owns its liquidity; the (3,3) game theory framework, which holds that the best outcome emerges when all participants choose to stake; and an extreme APY that exceeded 200,000% at launch.

But the structure did not hold. OHM’s returns relied heavily on new token issuance rather than real cash flow. The bonding mechanism spawned dozens of fork projects, but OHM’s price ultimately fell more than 90%. After this, builders began asking “where does the yield actually come from” before asking “how high can the yield go.”

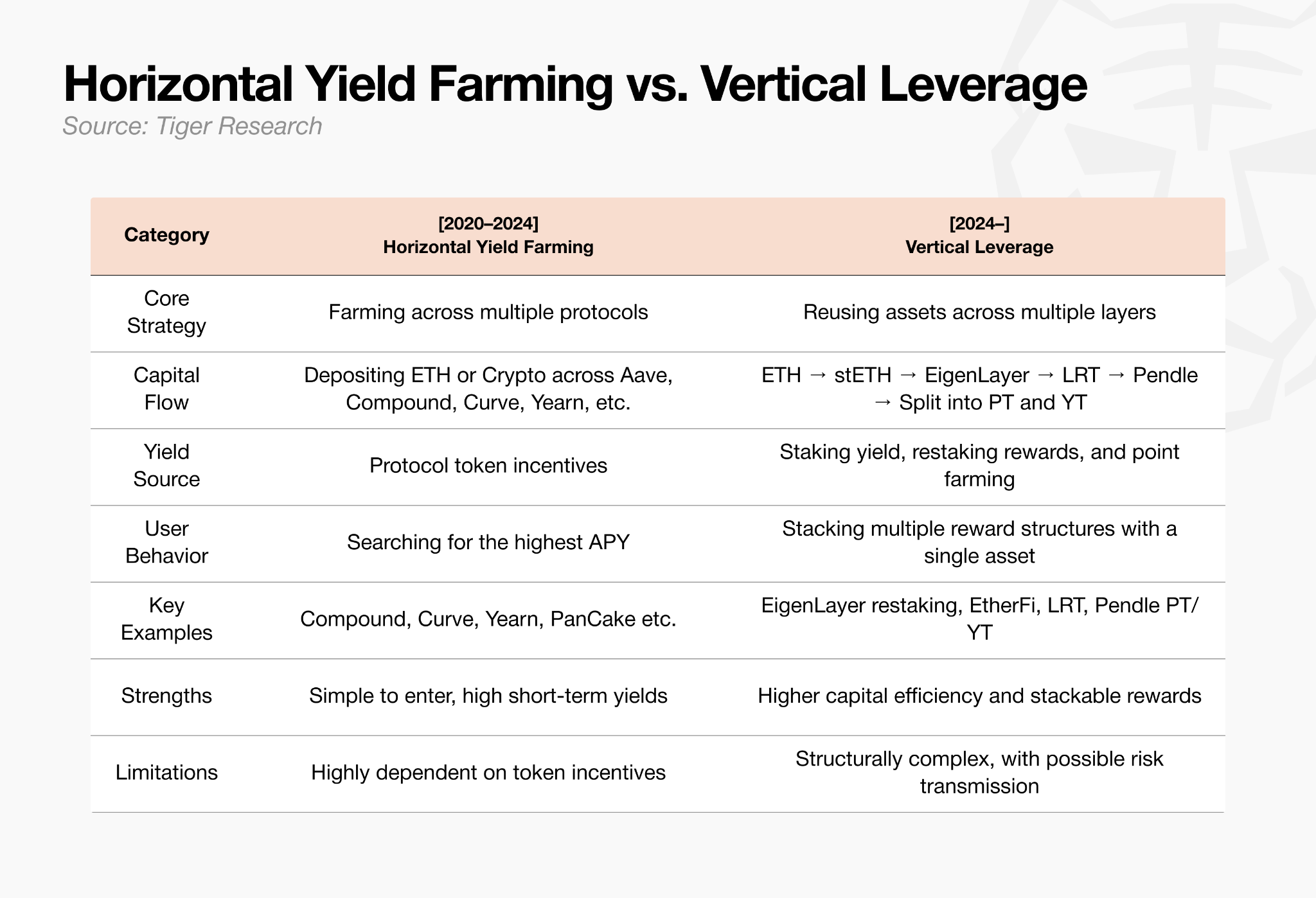

2.4. EigenLayer and Pendle: From Horizontal Farming to Vertical Leverage

The collapse reshaped how retail users behaved. The 2020 to 2022 playbook was simple: farm incentives first, exit first. It was common for a single user to spread funds across multiple protocols simultaneously. Farming in that era was horizontal. Capital moved between protocols chasing higher APY.

After 2022, this approach lost efficiency. Token incentives proved unsustainable, and airdrop competition intensified. Simply depositing across multiple venues yielded diminishing returns. Capital began moving toward stacking multiple layers of yield from a single asset: restaking stETH, redeploying LRTs into DeFi, and splitting yield rights to capture points and future returns.

EigenLayer and Pendle sat at the center of this shift. Starting in 2024, EigenLayer opened a restaking structure that allowed already-staked ETH and LSTs to generate additional rewards. EigenLayer’s TVL grew from under $400 million to $18.8 billion in roughly six months, a clear sign that capital was moving rapidly toward restaking over simple deposits.

Pendle split yield-bearing assets into PT and YT. PT represents a claim close to principal, while YT captures all yield, rewards, and points accrued until maturity. YT goes to zero at maturity, but until then it extracts maximum points and returns. Even without deep structural understanding, buying YT became a farming strategy that leverages both time and capital.

The strategy shifted from scattering capital across protocols to stacking multiple layers of reward from a single asset.

3. Redesigning the Revenue Model: RWA and YBS

Builders once focused on driving TVL through token incentives. As TVL grew, protocols appeared to be scaling, and token prices followed. The problem was that the liquidity never stayed for long.

TVL still matters as a metric. But the emphasis has shifted toward fee-based revenue, real asset backing, and regulatory readiness. The reason is a new variable: institutions. Institutions ask harder questions about where the yield comes from and what assets underpin it.

Products are evolving to absorb both demands at once.

3.1. RWA (Real World Asset): Institutions Enter the Market in Earnest

Since 2024, traditional financial institutions including BlackRock, Franklin Templeton, and JPMorgan have begun entering the on-chain market under the banner of RWA. The approach involves issuing off-chain assets, such as U.S. treasuries, money market funds, private credit, gold, and real estate, as tokens and distributing them on-chain.

The on-chain RWA market has grown from a few billion dollars in 2022 to tens of billions as of April 2026. Tokenized treasuries and private credit are driving that growth.

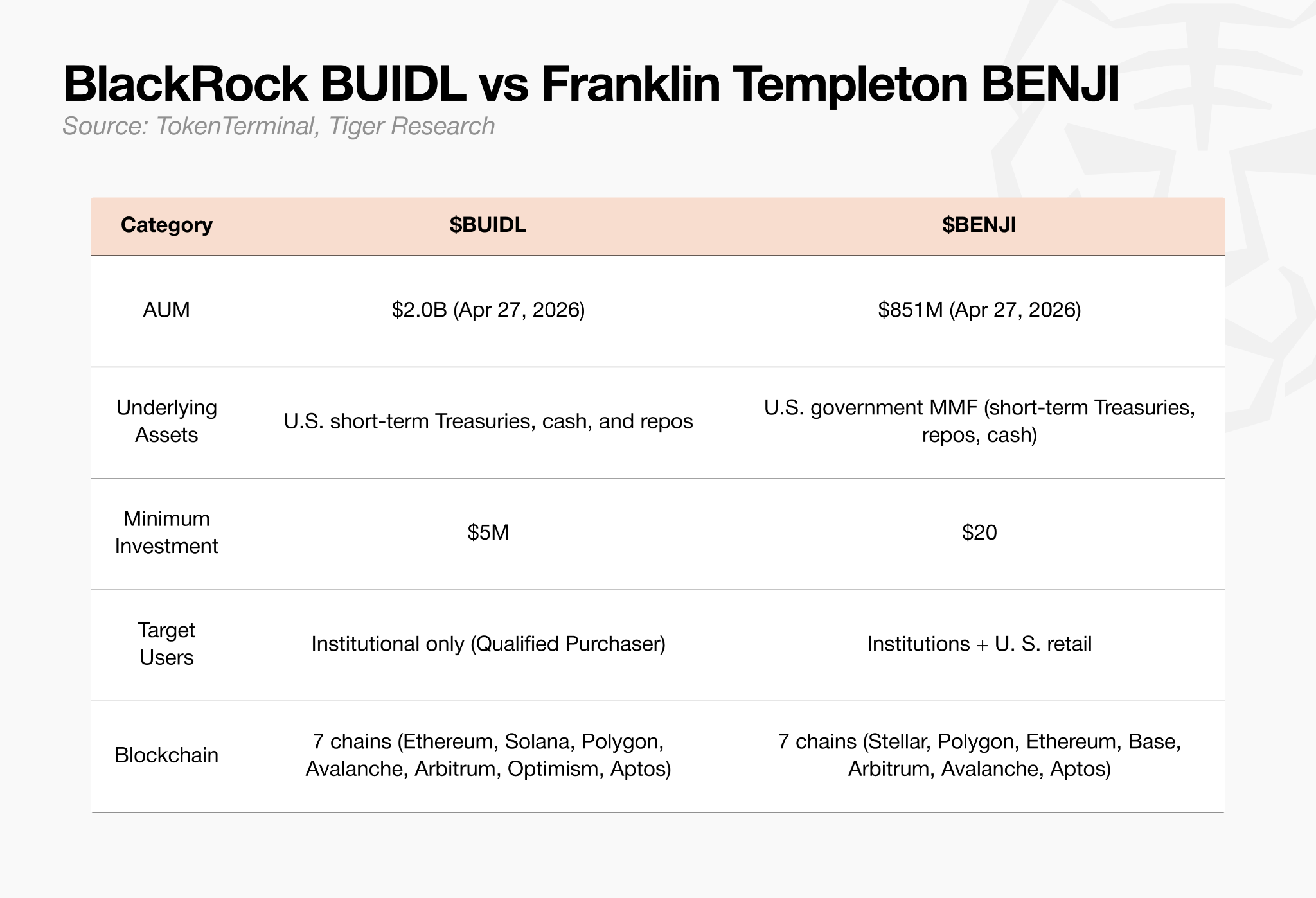

The institutional products currently leading the market are BlackRock BUIDL and Franklin Templeton BENJI. BUIDL and BENJI cover similar asset types but differ in approach. BUIDL is effectively institutional-only, while BENJI is accessible from as little as $20, making it open to U.S. retail as well.

Beyond these, Apollo, Hamilton Lane, and KKR are accelerating the tokenization of private funds and private credit in partnership with on-chain issuance platforms such as Securitize.

For institutions, the on-chain market is less a new frontier to explore than a new distribution channel. Accordingly, protocols serving institutional participants are building out the requisite KYC and AML frameworks, custody infrastructure, legal jurisdiction coverage, and risk management frameworks to match.

3.2. Yield-Bearing Stablecoins (YBS): A Dollar with Yield Built In

The segment worth watching here is YBS. Yield-bearing stablecoins (YBS) are stablecoins with yield embedded directly into the token itself. Ondo USDY, Sky sUSDS, Ethena sUSDe, and the previously mentioned BlackRock BUIDL and Franklin BENJI all fall into this category.

Simply holding these assets causes yield generated from the underlying to accumulate. The underlying assets include U.S. treasuries, funding rates, staking interest, and money market funds. The structure closely resembles a traditional finance MMF migrated on-chain.

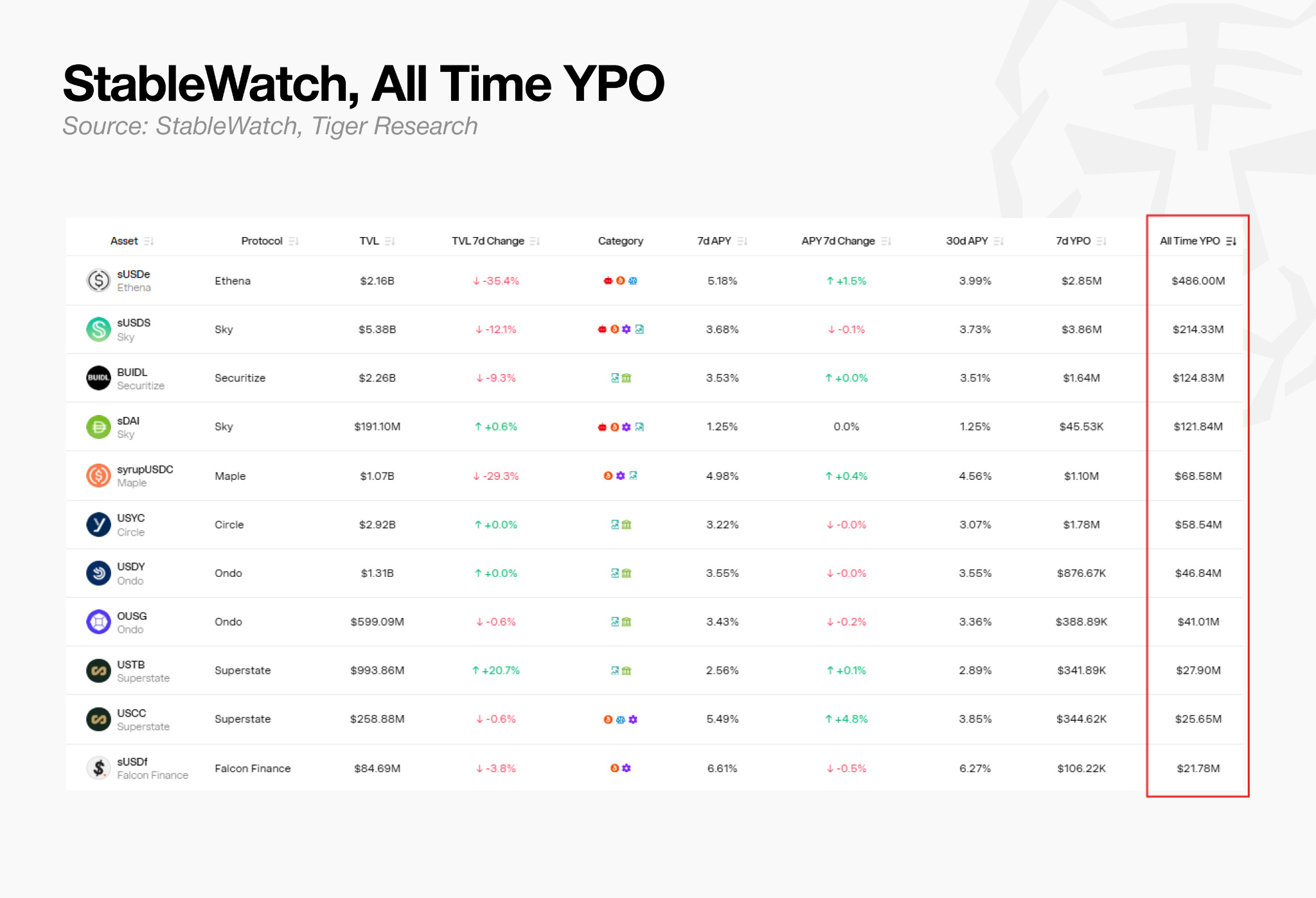

Based on YPO data from StableWatch, Ethena sUSDe, Sky sUSDS, BlackRock BUIDL, and Sky sDAI rank among the top products by cumulative yield paid out. Figures vary depending on how each product is counted, but YBS has clearly grown beyond a niche experiment into a category where real interest is being distributed.

That said, simply porting an MMF on-chain is not a differentiator on its own. The real differentiator lies in composability. BUIDL makes up 90% of Ethena’s USDtb reserves, and USDtb is used as collateral on Aave.

In other words, what were once base products sitting in the real world as RWA instruments have become stable structural components. This is no longer a market running on a finite internal battery. It has started drawing current from outside.

4. Players Building the RWA Power Grid, Learned from Past Failures

Until now, DeFi kept daisy-chaining power strips plugged back into themselves and called it a flywheel.

Strip on top of strip, with leverage and derivatives plugged in at the end. The problem was that the current never came from outside. It was mostly token incentives that protocols generated themselves. Compound created loans backed by its own token; Curve used its own token to retain liquidity providers.

It looked as if each was supplying power to the other, but in reality it was a structure running on a shared, finite battery. When the market shook, voltage dropped from the bottom up, and the products at the furthest end began to go dark. There was a limit to the load a self-referencing power strip could bear.

RWA connects this structure to a real power grid for the first time. Cash flows generated by the real economy, such as bond interest, real estate rental income, and trade receivables, become the current running through on-chain finance. Interest rates are determined not by internal token incentives but by external market demand, interest rates, and credit risk.

Once the current begins to flow, devices for issuance, custody, collateral, lending, and settlement can be connected in sequence on top of it. Financial products that were difficult to engineer in legacy DeFi become viable on this power grid. The question is not how many more strips to plug in, but how stable a current can be drawn.

This is where the core of on-chain RWA lies. Place assets with real underlying value on-chain, and connect financial functions on top of the cash flows they generate. If legacy DeFi borrowed liquidity using token incentives as a temporary battery, today’s RWA market is trying to retain liquidity through the cash flows of the assets themselves.

The players in today’s market are each building this power grid from their own position.

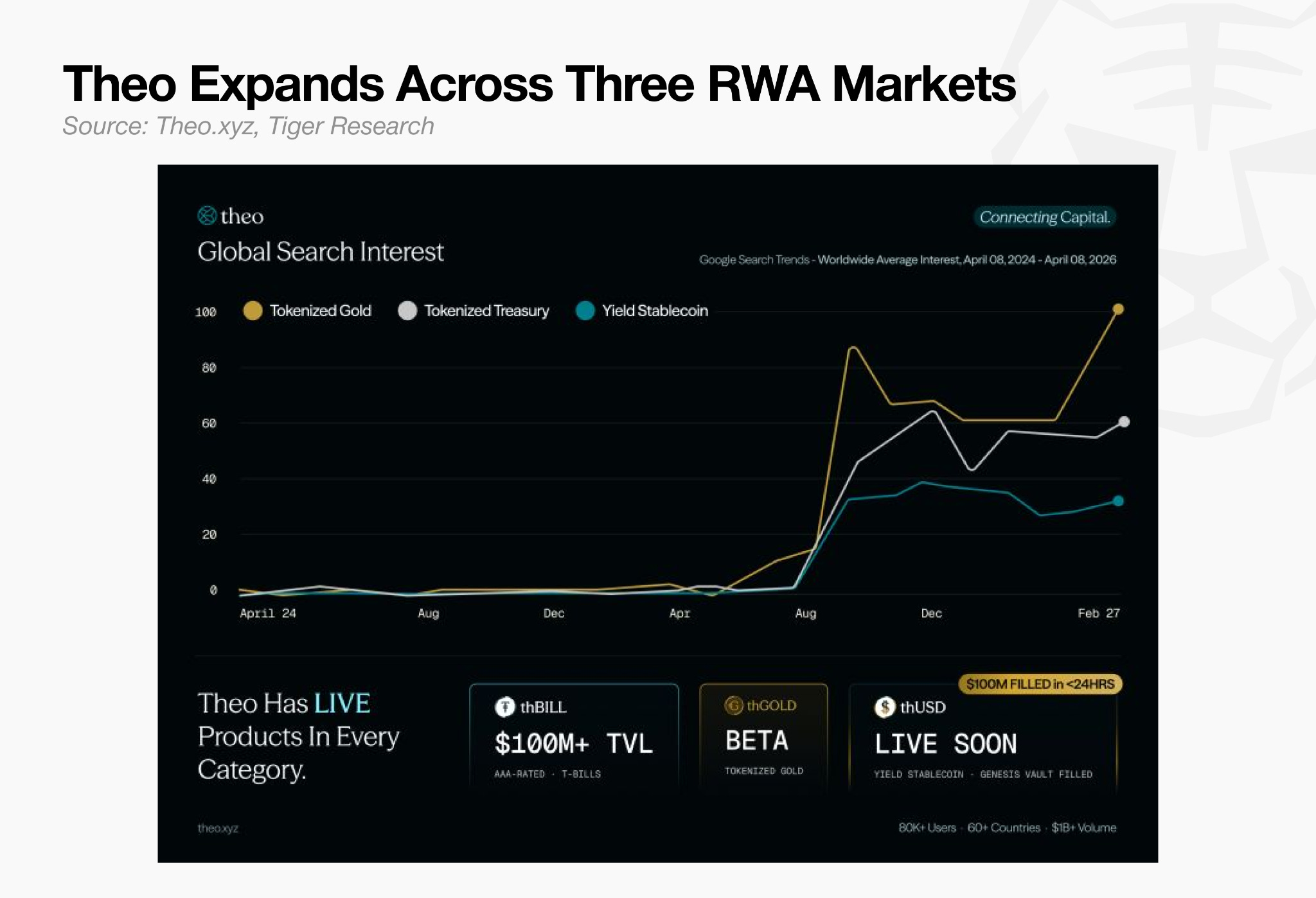

Theo decides which assets to connect on-chain. It selects the assets that will serve as the power source.

Plume builds the infrastructure through which those assets can be issued and distributed. It lays the transmission lines and switching infrastructure through which current can flow.

Morpho uses those distributed assets as collateral to build lending and collateral markets. It is the first financial device on the power grid that actually draws electricity.

No single player owns the entire grid. The new financial circuit called on-chain RWA is only complete when the power source, transmission network, and points of use are all connected.

4.1. Theo: A Case of Repositioning the Customer Base

Theo is a case study in starting from asset selection and rebuilding the customer base from the ground up.

Theo’s flagship product was once strategy vaults. But as the market shifted, what retail wanted and what institutions wanted began to diverge. Theo accepted that transition and redefined its customer base entirely.

The core product is thBILL. It is a basket of institutional-grade tokenized U.S. short-term treasuries sourced from regulated issuers, designed to generate stable yield as a core asset within the Theo ecosystem. The roadmap has since added thGOLD, with thUSD, a YBS issued against thGOLD as collateral, also set to launch shortly.

It is not just the product that changed. This demonstrates that a player which started with retail incentives can simultaneously be architected to speak the language of institutions.

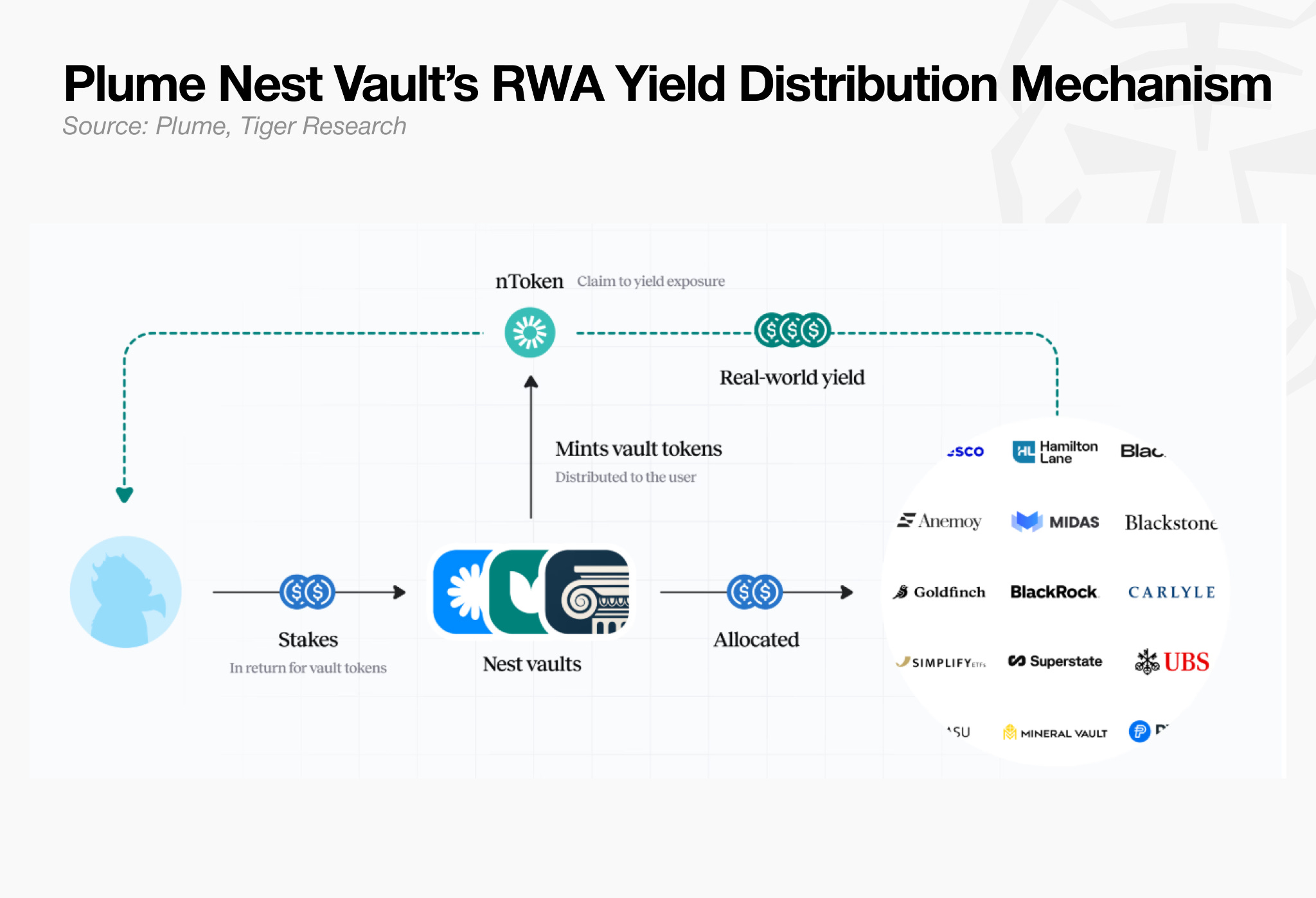

4.2. Plume: Building the Environment Where RWA Operates

Plume is a case study in bundling the infrastructure for asset distribution with the demand sitting on top of it.

For institutions, putting assets on-chain is not enough. What is needed is end-to-end infrastructure spanning issuance, compliance, distribution, and yield productization. For on-chain users, access to institutional-grade assets like treasuries and funds requires a supporting product structure.

Nest is a yield protocol built on top of Plume’s infrastructure. It packages yield generated from institutional-grade RWAs into a format users can access by depositing stablecoins. Each vault, including nBASIS, nTBILL, and nWisdom, delivers yield backed by a different real-world asset, and vault tokens move and circulate freely within DeFi.

WisdomTree has launched 14 tokenized funds, Apollo Global has deployed a $50M credit strategy, and Invesco has migrated a $6.3B senior loan strategy onto Plume. Nest serves as the demand gateway to these institutional assets.

Beyond its own rails, Plume functions as integrated infrastructure that creates a distribution channel between institutional assets and on-chain demand.

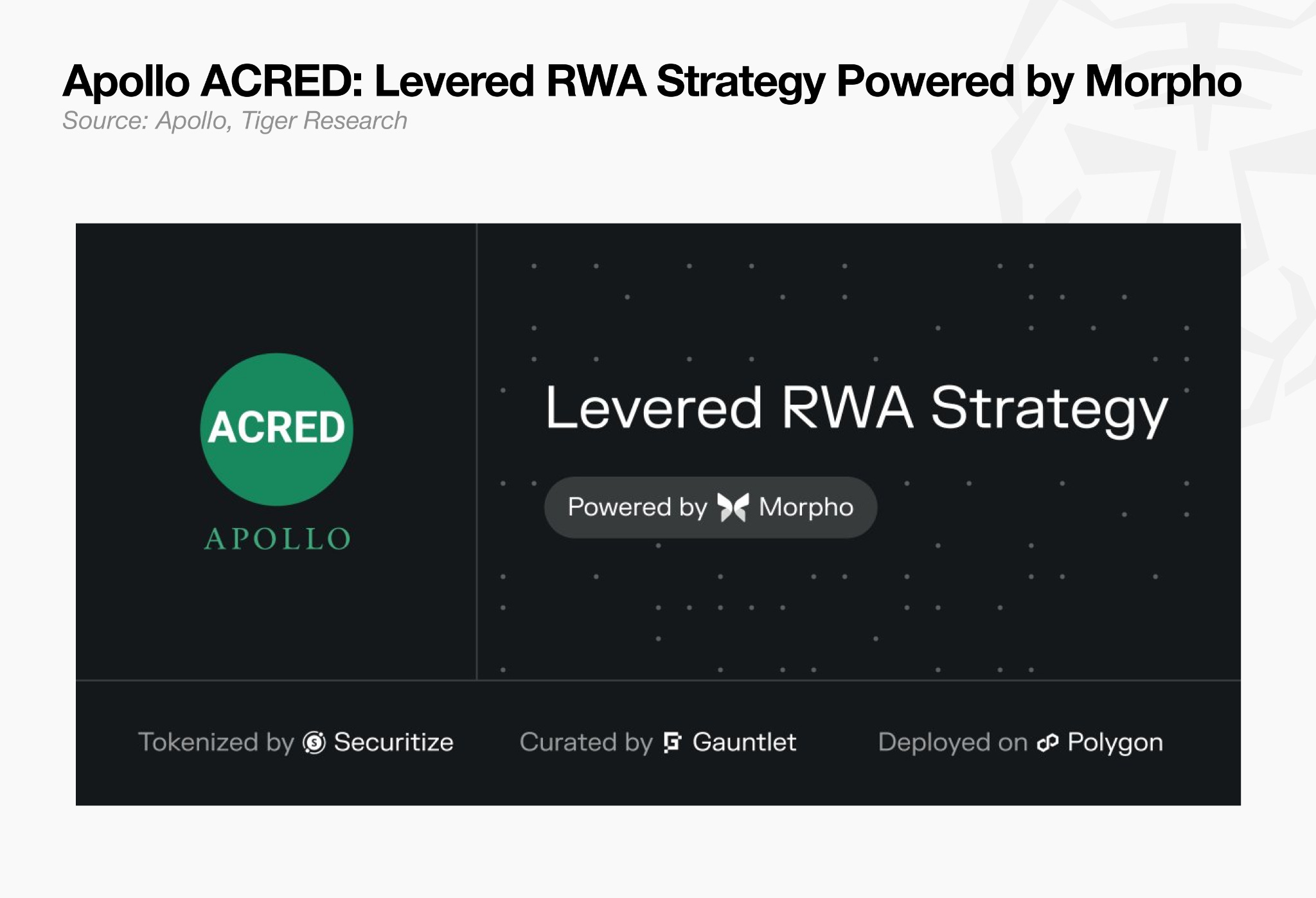

4.3. Morpho: Adding Financial Functionality to Institutional Assets

Morpho is a case study in turning assets into collateral, loans, and liquidity.

For institutions, registering assets on-chain is only the starting point. What matters is whether those assets can be used as collateral, and whether liquidity can be extracted on that basis. Lending terms and risk parameters must be clearly defined, and execution must be viable within custody and compliance frameworks.

The leading example is Apollo ACRED. Apollo not only deployed its credit strategy on Plume, but also enabled ACRED to be used as collateral on Morpho, allowing holders to borrow stablecoins while maintaining their fund position. ACRED is a tokenized private credit fund based on Apollo’s Diversified Credit Securitize Fund, issued on-chain via Securitize.

Only when institutional assets can serve as collateral, generate loans, and produce liquidity do they become usable material for on-chain finance.

5. What Remains After the Dopamine Fades

The golden era of decentralized finance (DeFi), in retrospect, was closer to a mirage built on token incentives and leverage.

Some corners of the market remain skeptical about DeFi’s recovery potential, pointing to the string of hacking incidents.

Yet the recent Kelp DAO rsETH incident and the formation of DeFi United are telling a rather unlikely story that cuts against that view. As of April 28, 2026, Aave and DeFi United have successfully raised over $300M, surpassing the $190M originally drained in the exploit.

This shows that a trust infrastructure and a more mature model of shared accountability are beginning to take shape in the market.

What DeFi’s history has taught us is that it used to be a market where no one was accountable. Fast access to high-yield tokens was users’ sole objective, and builders designed yield mechanisms to match that demand, often walking away once their funding targets were met.

But the market is now shifting toward one where accountability must be deliberately designed into the system. It is not yet a complete financial system, but what is clear is that a movement has emerged to identify shared problems and distribute losses and responsibility.

The reason many feel the market is no longer viable is not just security issues, but also the disappearance of immediate rewards and yields, and the absence of any new narrative or catalyst.

The word “DeFi” is losing its force over time. The market is already fragmenting under more specific labels: lending, stablecoins, RWA, restaking, on-chain credit.

The word is not the point. The experiments that started from it are maturing into structures that put more assets into actual productive motion.

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.