BlackRock’s BUIDL has become an indispensable asset in the digital asset space. Its largest buyer, however, is not traditional institutions. It is DeFi.

Key Takeaways

BUIDL’s on-chain significance is not that BlackRock issued a token. It is that Ethena, Ondo, Frax, and Spark used BUIDL as a building block for their own dollar products, turning an institutional fund into a foundational asset in the DeFi supply chain.

Protocols chose BUIDL not for yield, but because it satisfied three conditions simultaneously: clear legal claims, on-chain composability, and existing regulatory compliance. No other asset offered all three.

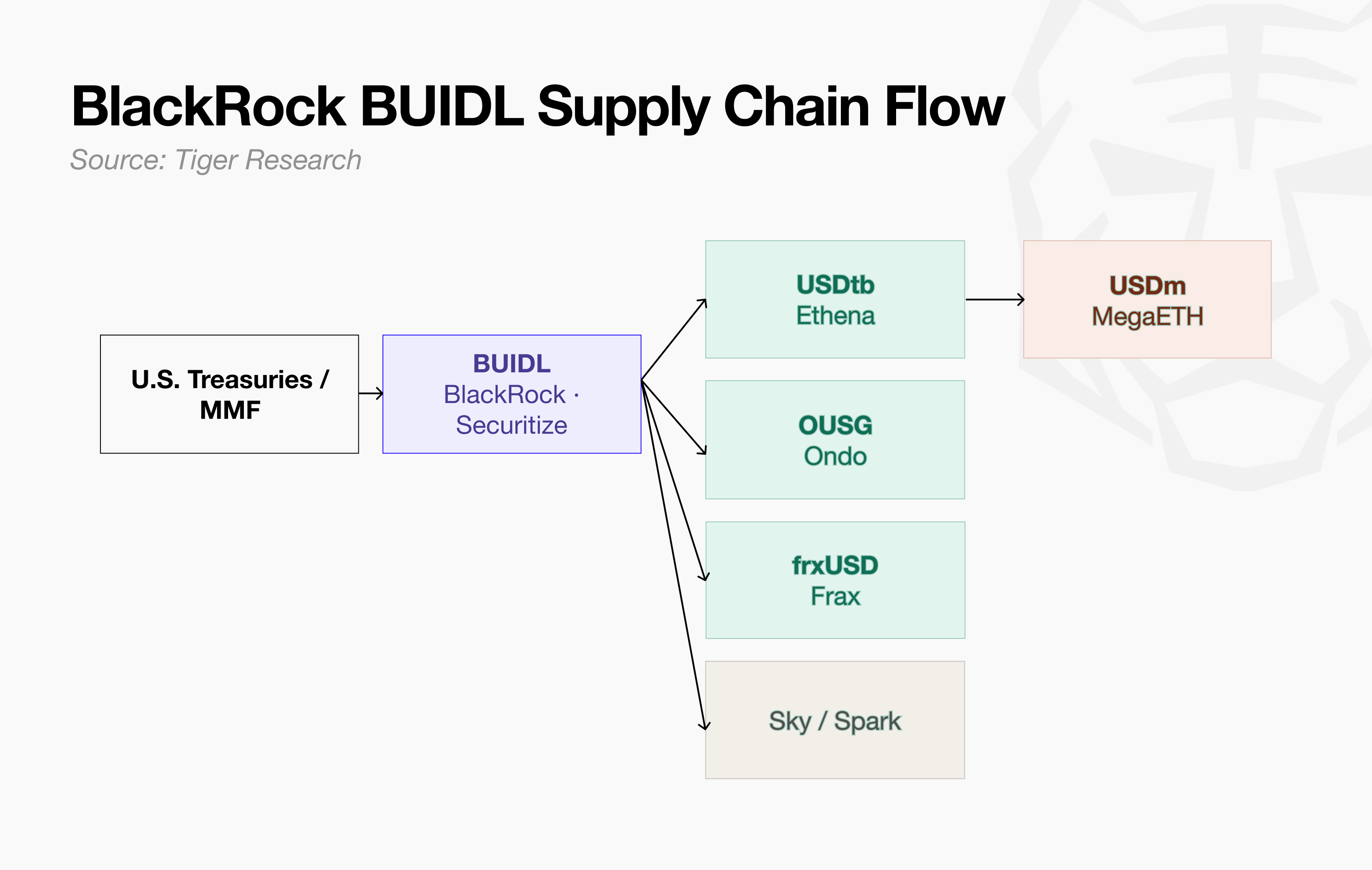

The supply chain does not stop at one layer. As BUIDL is processed into USDtb and then into ecosystem-specific dollar products, demand for the base asset grows with every new ecosystem that emerges.

BUIDL revealed a new distribution channel for tokenized assets. The customer was not found through traditional sales channels, but through DeFi protocols, a client segment that does not exist in traditional finance. Without recognizing this channel, the next BUIDL will not happen.

1. From Institutional Product to Protocol Infrastructure

BUIDL was built for institutions: cash and U.S. Treasury exposure, qualified investors only, $5M minimum subscription.

First movers: DeFi protocols, not institutions. Not buying for yield. Three reasons:

Legal clarity. Issued under Rule 506(c). Investor rights defined under U.S. securities law. Protocols can explain the asset and redemption process in legal terms.

Lower compliance costs. Post-GENIUS Act reserve design is complex. BUIDL already meets institutional collateral standards. Compliance burden transfers, not built from scratch. Advantage grows as regulation tightens.

On-chain composability. Usable as protocol reserve, exchange collateral, or base layer for ecosystem dollar products.

No other asset checked all three. BUIDL became the default base asset.

2. How DeFi Protocols Use BUIDL

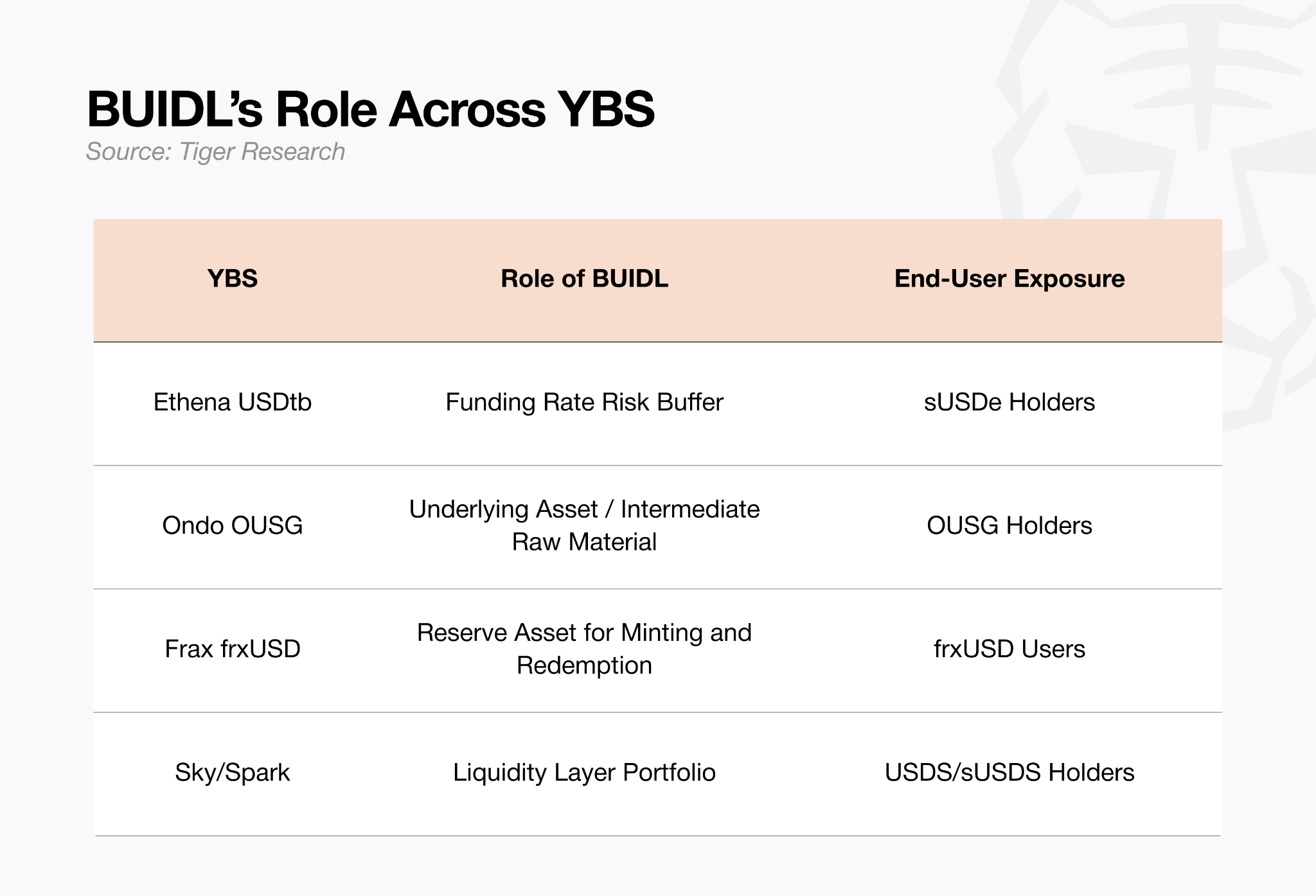

What matters is not simply that protocols hold BUIDL. It is the specific role BUIDL plays within each protocol’s architecture.

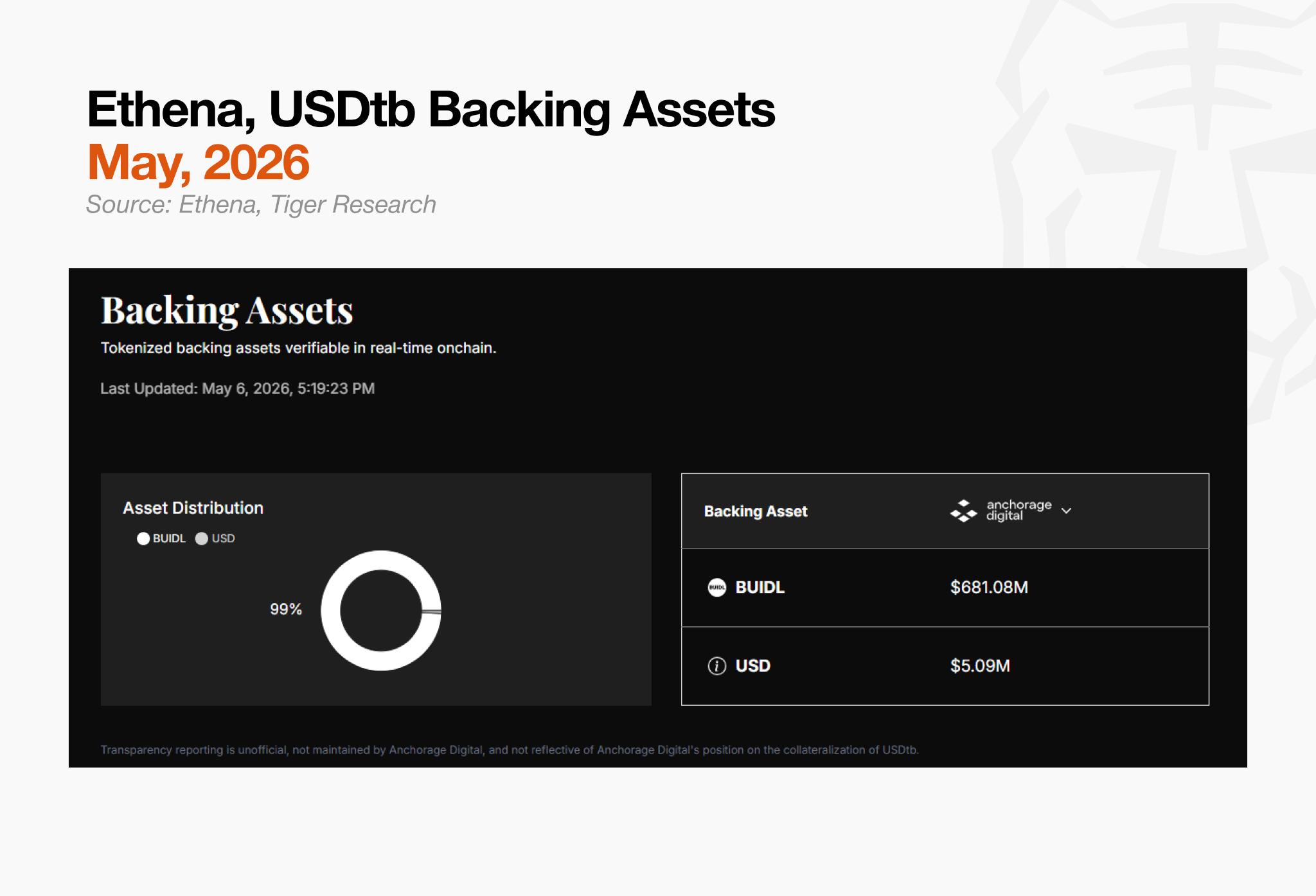

2.1. Ethena (USDtb): Funding Rate Buffer

Ethena‘s flagship products are USDe, a synthetic dollar, and sUSDe,

USDe yield sources:

Staking rewards from collateral assets

Funding fees from perpetual futures (delta-neutral strategy)

The second yield source, funding fees, comes from the delta-neutral strategy. USDe holds a short futures position equal in size to its collateral, offsetting price risk. When long demand dominates, long holders pay funding fees to short holders. Ethena, holding the short, collects that income directly.

The risk emerges when funding rates turn negative. In bear markets, short demand can exceed long demand, requiring short holders to pay funding fees instead. For Ethena, income becomes cost. If this persists, the insurance fund depletes and USDe’s dollar peg comes under pressure.

Ethena needed an asset capable of absorbing this stress. USDtb fills that role, with BUIDL and USDC as its core reserves. The purpose is not yield enhancement. It is a defensive buffer that keeps Ethena’s overall structure stable during periods of negative funding.

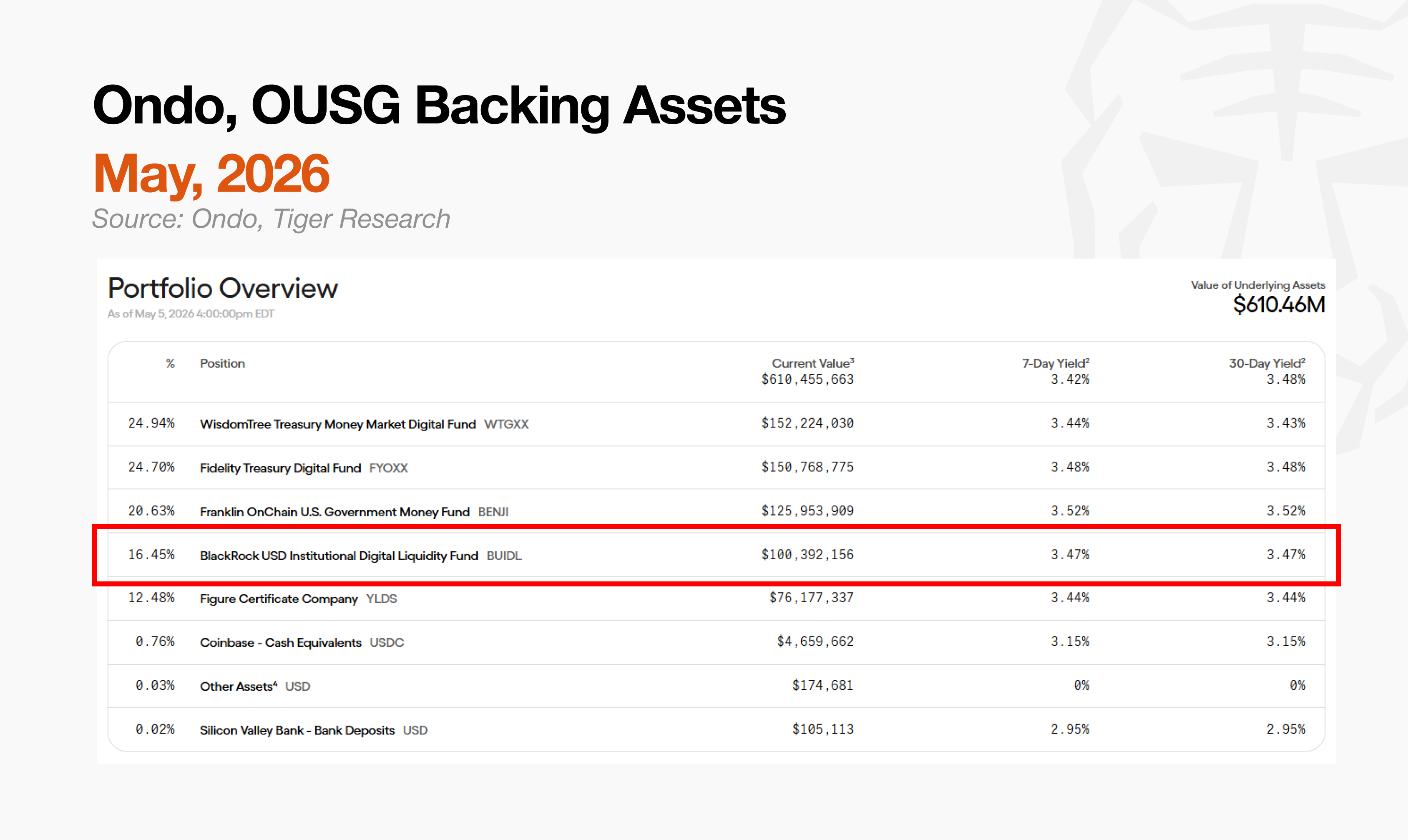

2.2. Ondo (OUSG): BUIDL as Intermediate Input

OUSG(Ondo U.S. Government Bond Fund) is a tokenized fund that brings institutional-grade U.S. Treasury exposure on-chain. Direct access to institutional money market funds such as BlackRock BUIDL or Franklin Templeton FOBXX requires millions of dollars in minimum investment and qualified investor status. OUSG lowers that barrier, serving as an on-chain intermediary that makes these assets accessible to DeFi users.

BUIDL is a core component of OUSG’s reserve composition, alongside Franklin Templeton’s FOBXX and WisdomTree’s WTGXX. OUSG repackages institutional assets that retail users cannot directly access into an on-chain intermediate product.

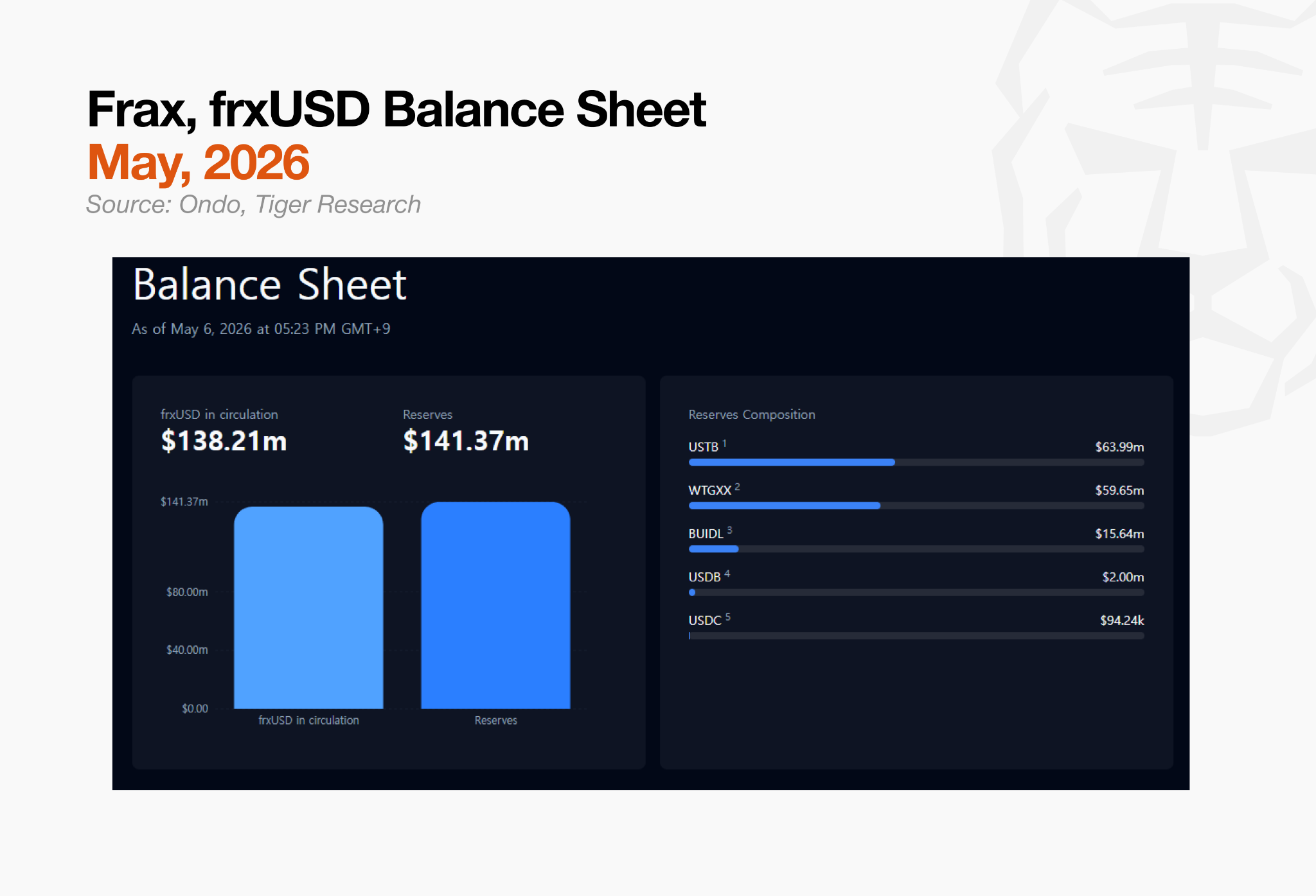

2.3. Frax(frxUSD): Mint and Redemption Reserve

frxUSD is a new dollar stablecoin designed by Frax Protocol, targeting a stable $1 value like USDC or USDT. What sets it apart is its reserve structure.

Existing stablecoins back their reserves with cash or Treasuries held in off-chain bank accounts. Frax replaces that with BUIDL, an on-chain tokenized Treasury. The mechanism is a direct 1:1 exchange: deposit BUIDL to mint frxUSD, return frxUSD to redeem BUIDL.

End users do not interact with this structure directly. They use frxUSD as a stablecoin in payments or DeFi. BUIDL operates in the background, supporting every mint and redemption.

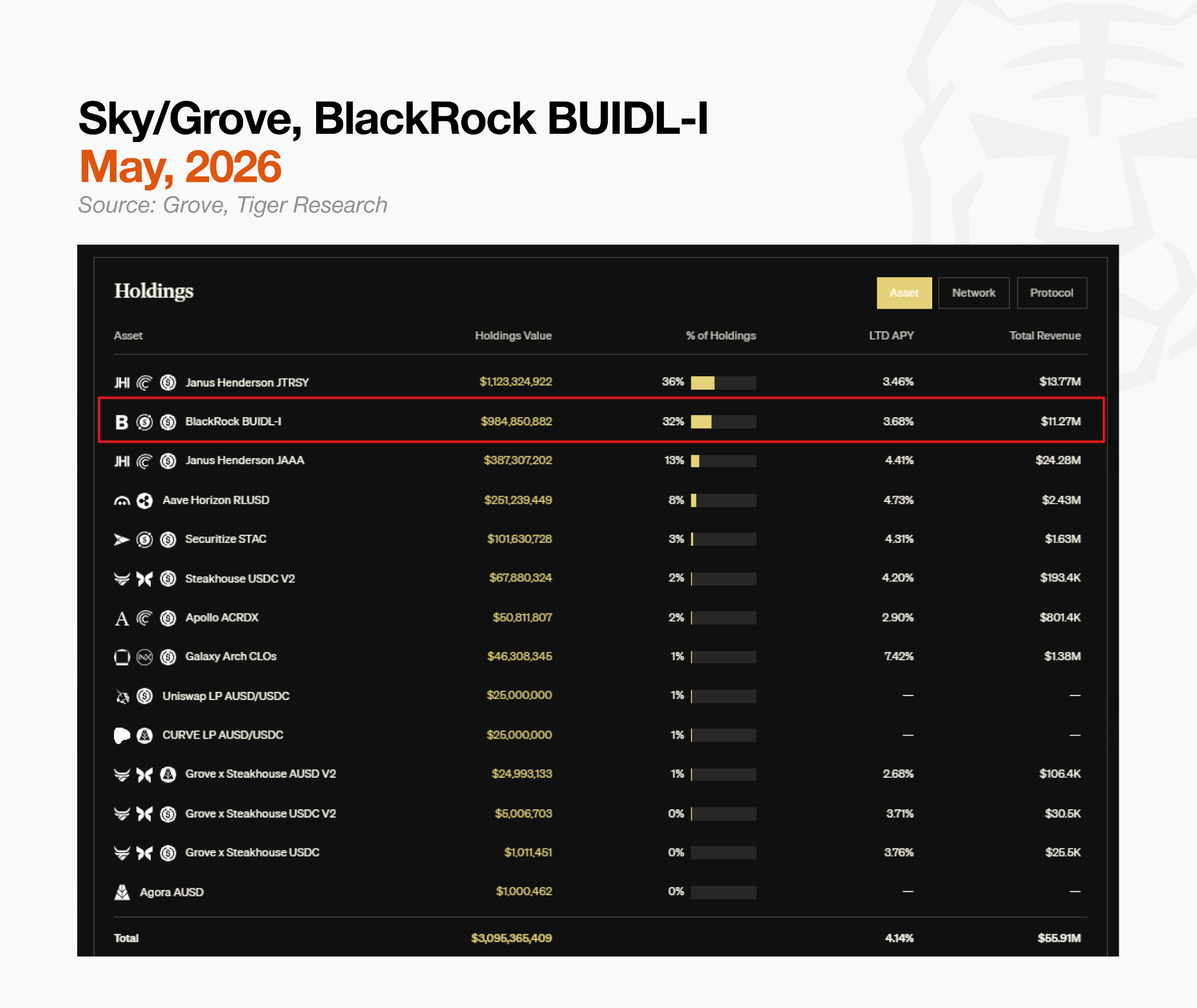

2.4. Spark’s Tokenization Grand Prix(TGP) Allocation and BUIDL’s Common Thread

Spark’s Tokenization Grand Prix(TGP) allocated $500 million of its $1 billion mandate to BUIDL, with the remainder split between Superstate’s USTB and Centrifuge’s JTRSY. Rather than a single reserve asset, Spark constructed a portfolio.

Conventional asset managers blend Treasuries, money market funds, and credit instruments in the same way. What differs here is that this portfolio operates on-chain, redeployed across DeFi rails as collateral and liquidity.

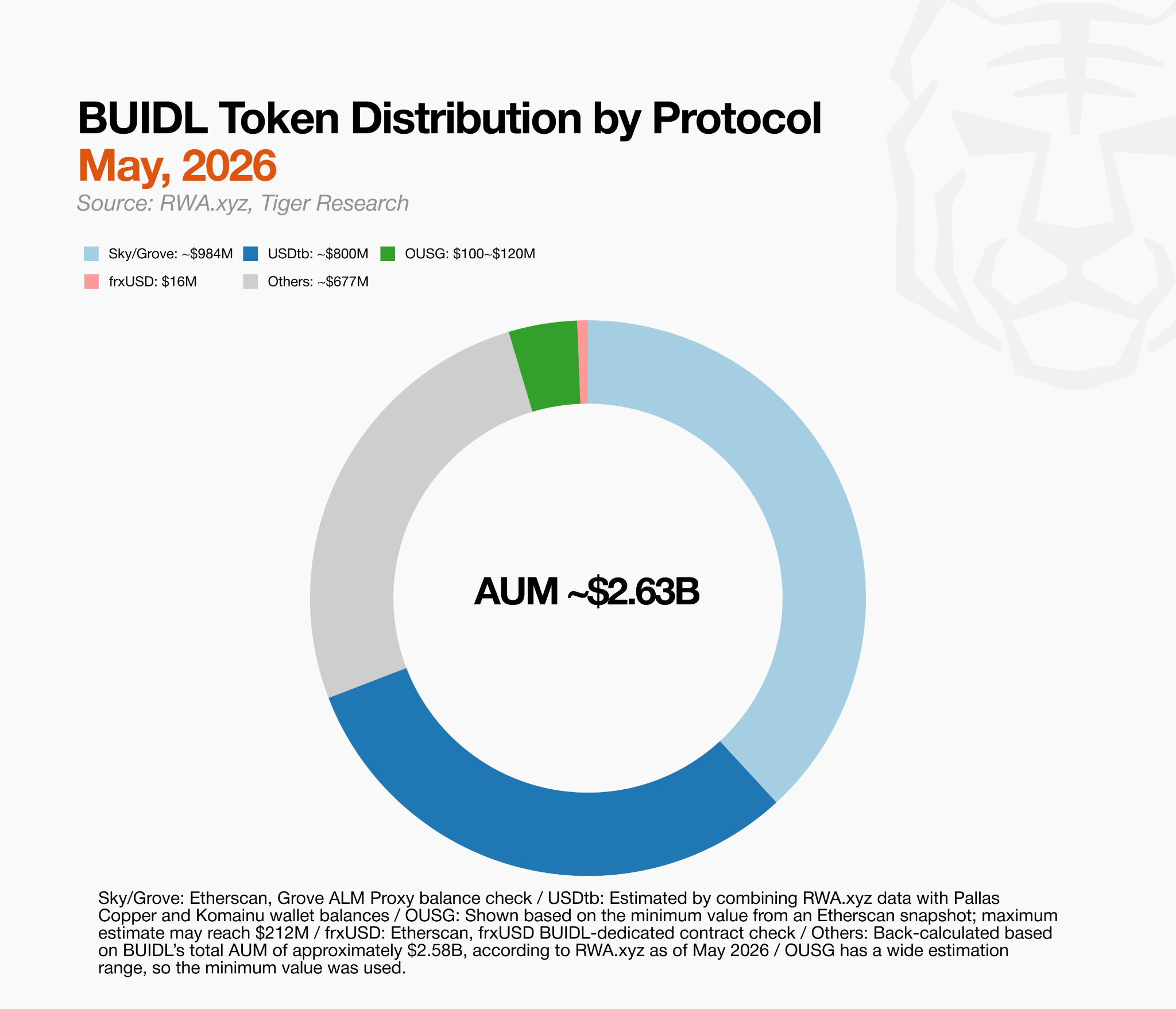

Across the four cases examined, BUIDL played a different role in each: reserve asset, intermediate input, mint-and-redemption backing, and portfolio component. One pattern holds across all of them. In no case was BUIDL the end product. Protocols are buying BUIDL to fill their own systems, and that demand structure is already operating at scale.

3. BUIDL Reprocessed: The Compounding Demand Structure

As shown, protocols have each adopted BUIDL directly as a reserve asset. But the chain does not stop there. Products built on BUIDL are becoming reserves for new products, enabling an expanding layer of derivative structures.

MegaETH’s USDM is the clearest example. USDm is an ecosystem-specific stablecoin developed by MegaETH in collaboration with Ethena. Its reserve is USDtb, and USDtb’s reserve is BUIDL. As USDm demand grows within MegaETH, BUIDL demand rises with it.

Each new ecosystem that enters this structure adds customers, not competitors. Adoption speed is also a meaningful differentiator in on-chain finance. Building an equivalent derivative structure in conventional finance would require months of regulatory review, legal contracting, and custodial arrangement. On-chain, that process compresses significantly. Within a regulatory framework, there is effectively no limit on the range of eligible base assets.

In sum, BUIDL is unlocking compounding demand by anchoring an expanding on-chain structure to a safe, real-world asset base.

4. What Comes After BUIDL?

BlackRock built an institutional fund. Ethena, Ondo, Frax, and Spark adopted it as a base asset. MegaETH layered an ecosystem-specific dollar on top. All of this happened in under two years since BUIDL’s March 2024 launch.

That speed was not driven by BlackRock’s brand alone. Legal clarity, on-chain composability, and regulatory compliance: BUIDL was the only asset that offered all three at the time. That first-mover advantage was substantial, and it compounds as more DeFi protocols integrate BUIDL into their reserves.

The question for teams designing the next tokenized asset is how to enter this market. Most approach it one of two ways: assuming tokenization itself generates demand, or replicating conventional finance distribution through sales teams, broker networks, and existing channels.

BUIDL took neither path. DeFi protocols, including Ethena, Ondo, Frax, and Spark, were the first adopters. Exchanges and institutions such as Deribit, Binance, and OKX followed. BUIDL found a client segment that does not exist in conventional finance.

These clients buy the asset, build their own products on top of it, and those products become the foundation for the next protocol. They are not customers acquired through sales. They are customers drawn in through design. Without identifying this client segment, the next BUIDL will not emerge.

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.