Authority in DeFi lending is shifting from protocols to curators who hold judgment rights. Market entry comes down to one choice: borrow this judgment, supply it, or own it.

Key Takeaways

An asset manager role is emerging in DeFi. The era when protocols and governance decided everything is over.

The market is still early, but capital and distribution already concentrate around top curators. Their track records are becoming the institutional benchmark.

There are three entry paths: Distribution (curator as backend), Supply (post assets onchain), and Operator (become a curator).

The path chosen determines the control gained, the capabilities required, and the risks taken on.

The core question is not whether to enter DeFi, but which judgment rights to delegate and which to keep.

1. Risk Curators: Onchain Asset Management Specialists

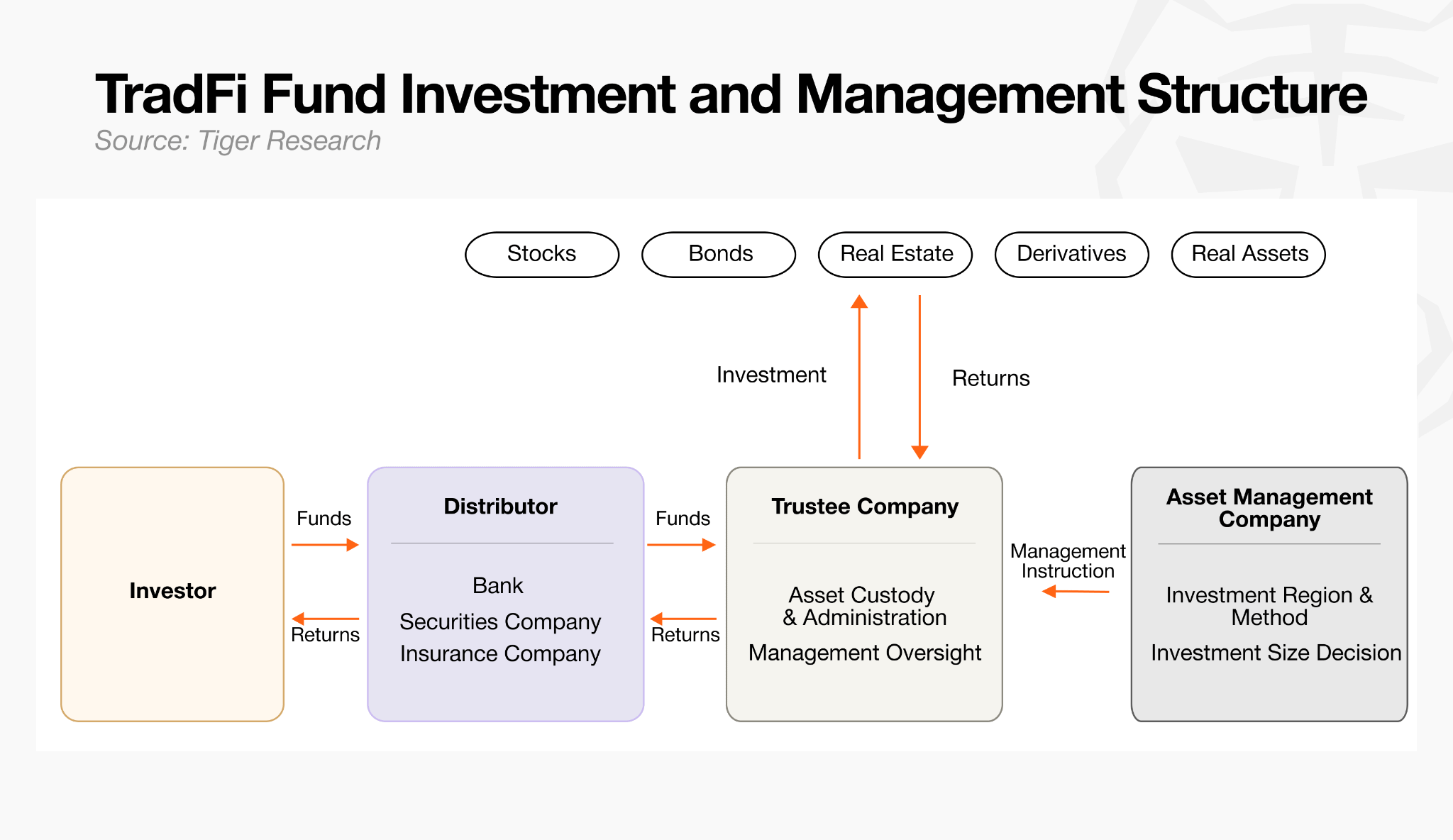

Just as traditional finance has long separated judgment from execution, the crypto market has matured to the point where specialized players own each function. Traditional finance divides the work as follows.

Asset Manager: The fund’s “brain.” Sets strategy and gives specific instructions to the custodian.

Custodian: Holds assets, executes investments per the manager’s instructions, and oversees them.

Distributor: Distributes fund products to investors and gathers capital.

Crypto has its own version of each role. DeFi was originally built to rely entirely on smart contract code, but over time it became clear that code alone cannot fully control onchain risk.

To run onchain lending safely, a new class of specialists emerged to assess and coordinate these complex risks. They are called Risk Curators, and they have effectively taken on the asset manager role in the onchain ecosystem.

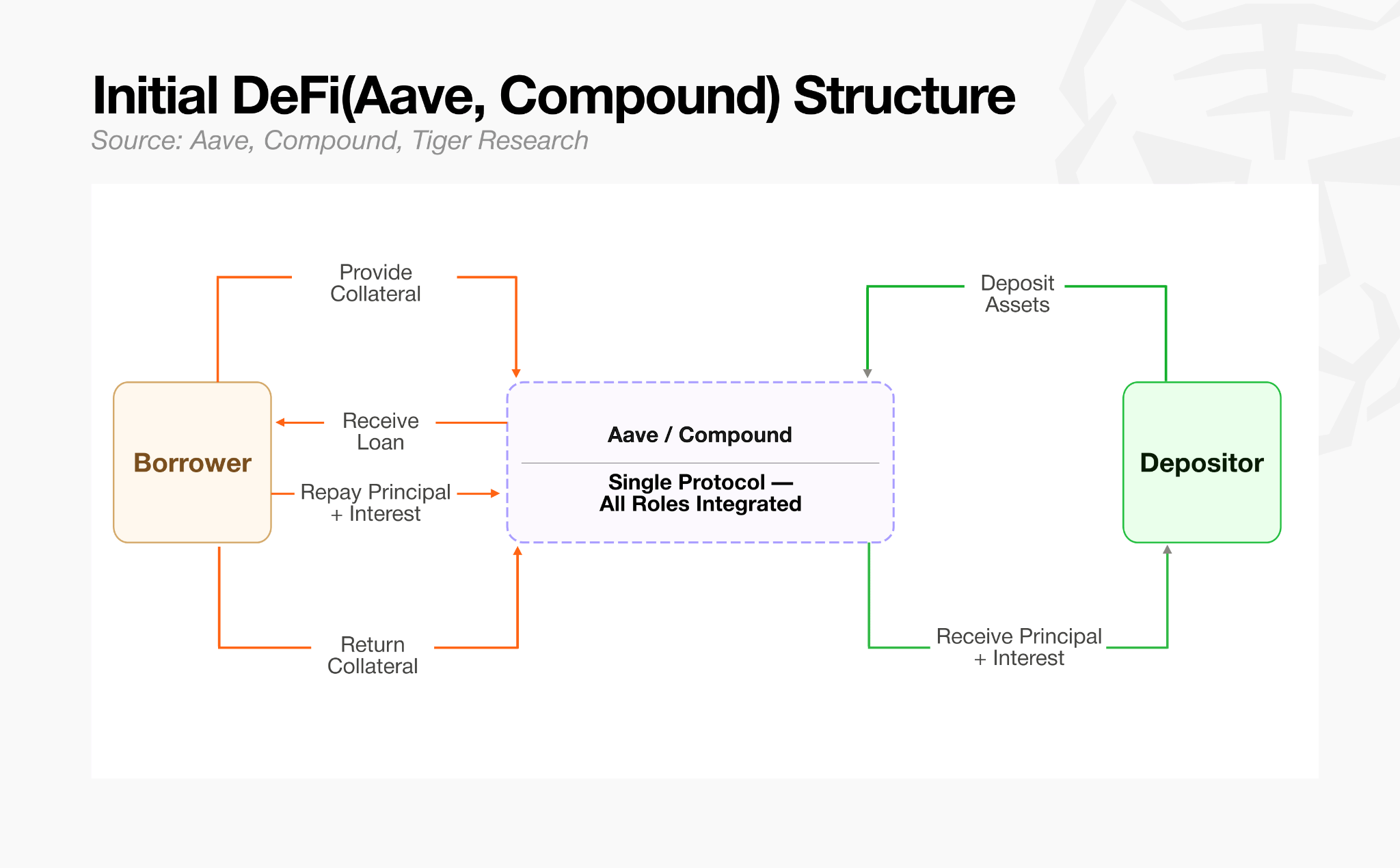

2. Early DeFi Had No Specialists

Early DeFi protocols like Aave and Compound bundled lending infrastructure and risk standards into a single structure. Risk curators existed at the time, but with every asset sitting in one giant pool, their role stayed at the level of a system-wide “risk manager” tuning the protocol’s overall risk parameters. As volatile assets flowed in, the single-pool design meant one bad asset could spread losses across the entire system, and someone had to manage that contagion risk.

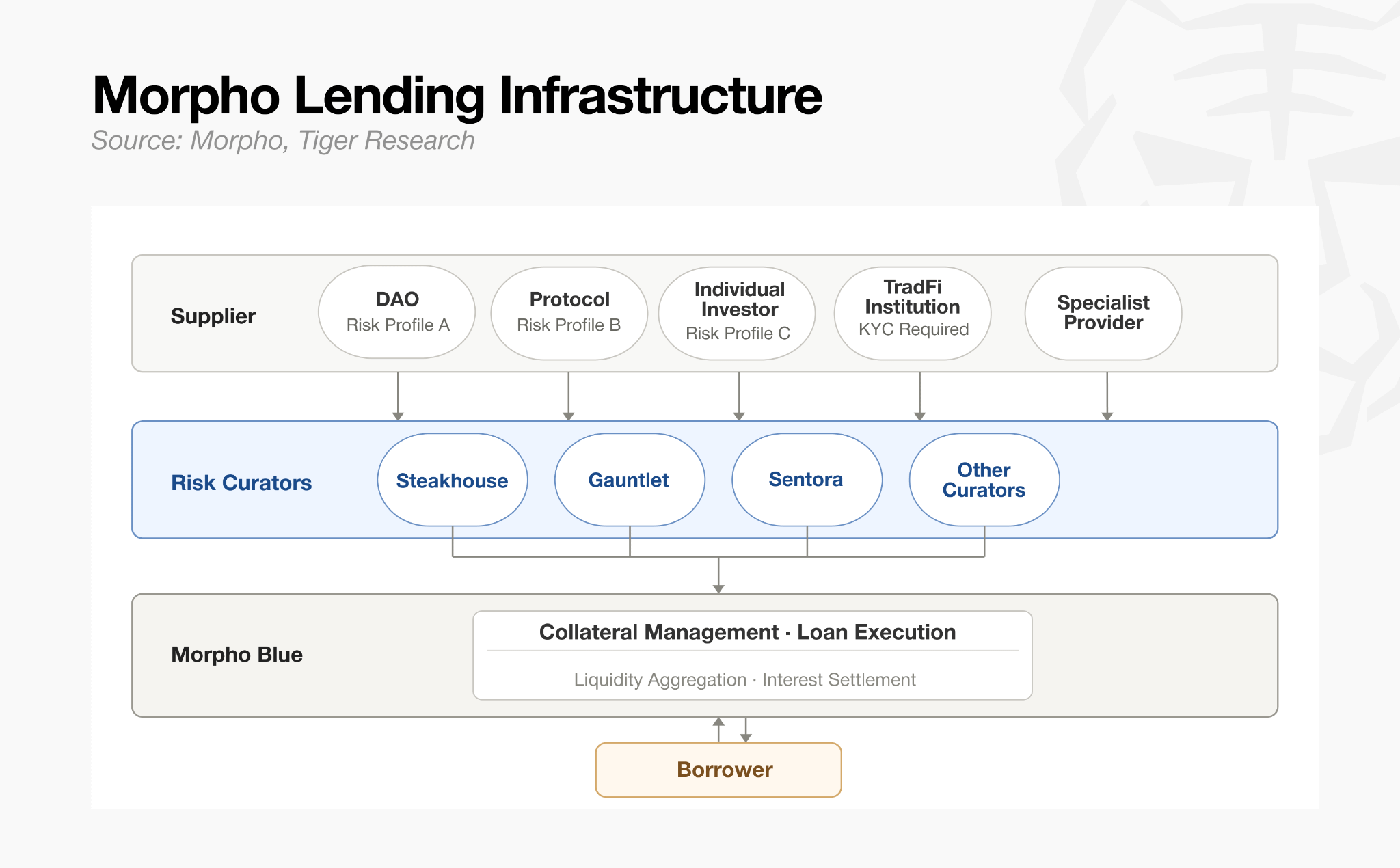

That changed with Morpho, which split collateral assets and lending terms into separate markets. Replacing the single giant pool with a multi-vault structure modularized the asset management strategy, and the role of risk curators flipped entirely. Instead of defensively managing within a single protocol’s fixed framework, external specialists could now design and operate their own independent lending vaults under their own standards.

With infrastructure and risk judgment fully separated, risk curators evolved from system-wide risk managers into the crypto market’s “asset managers,” actively running multiple vaults.

3. Who Leads the Market

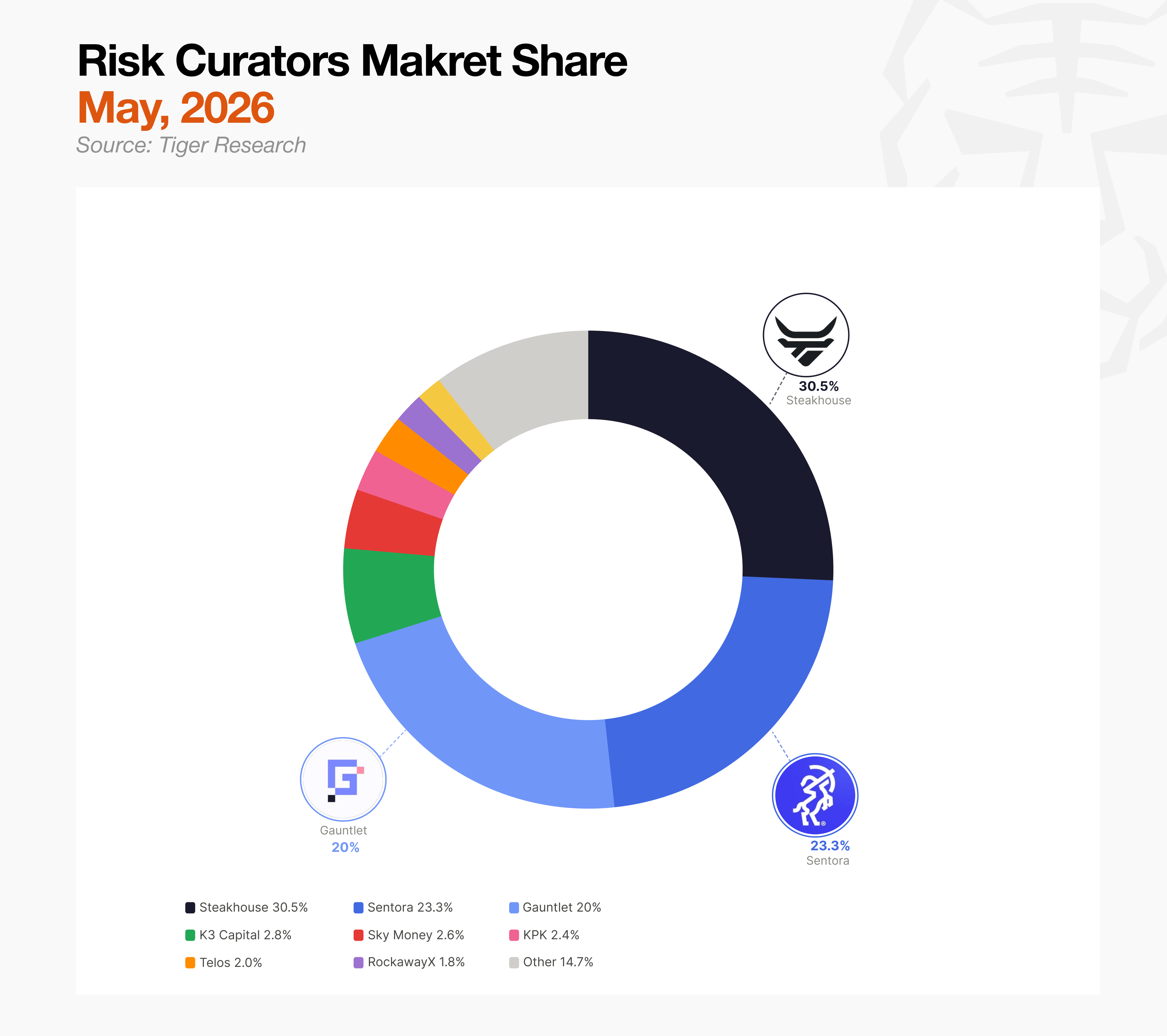

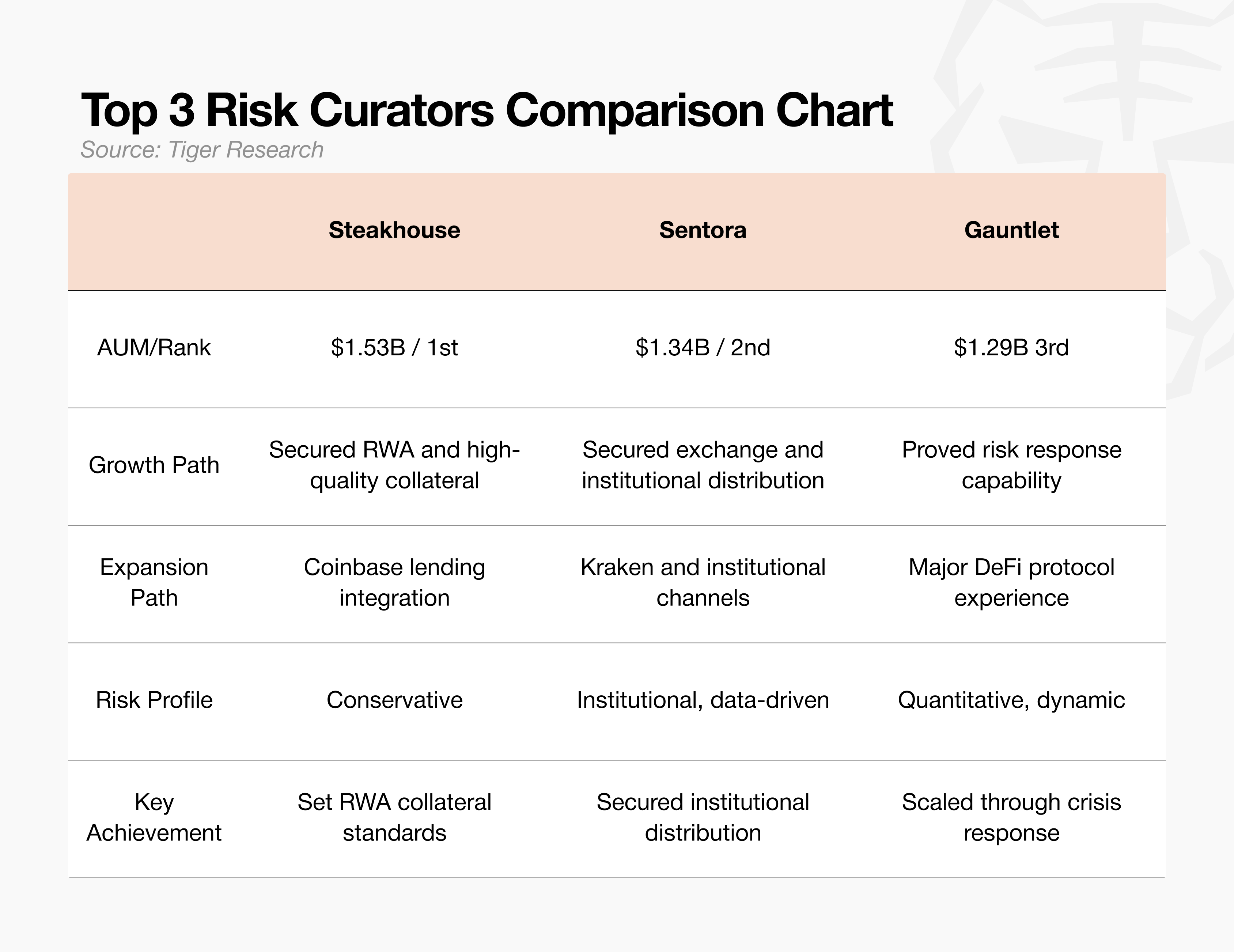

As of May 2026, the risk curator market manages roughly $7B in assets. The top three teams hold 70% of that $7B. The market only took off in 2025, yet capital is already concentrating, a sign that capital is following teams with proven track records. Each of the three reached the top through a different path.

Steakhouse: A conservative curator that has led the adoption of high-grade real-world assets (RWA) such as US Treasuries. It serves as the backend for Coinbase’s lending service, opening a distribution channel, and ranks #1 with $1.53B AUM (as of February 2026). Beyond AUM, this team sets the standard for which real-world assets qualify as legitimate DeFi collateral.

Sentora: A team built on AI risk models and institutional data infrastructure. Wired into Kraken as a backend, it has secured a pipeline for institutional capital. #2 at $1.34B AUM. Won the distribution channel linking exchanges to institutional clients.

Gauntlet: Originally an onchain quantitative analysis firm that simulated risk parameters. In October 2025, when $775M flooded one of its pools, the team normalized the collapsed APY within 10 days, proving its capability. #3 at $1.29B AUM. Recognized as the team with risk defense and crisis response for large capital inflows.

At this stage, the risk curator market is no longer a simple TVL race. It is a fight to claim the standards first: collateral criteria, distribution channels, and risk response capability.

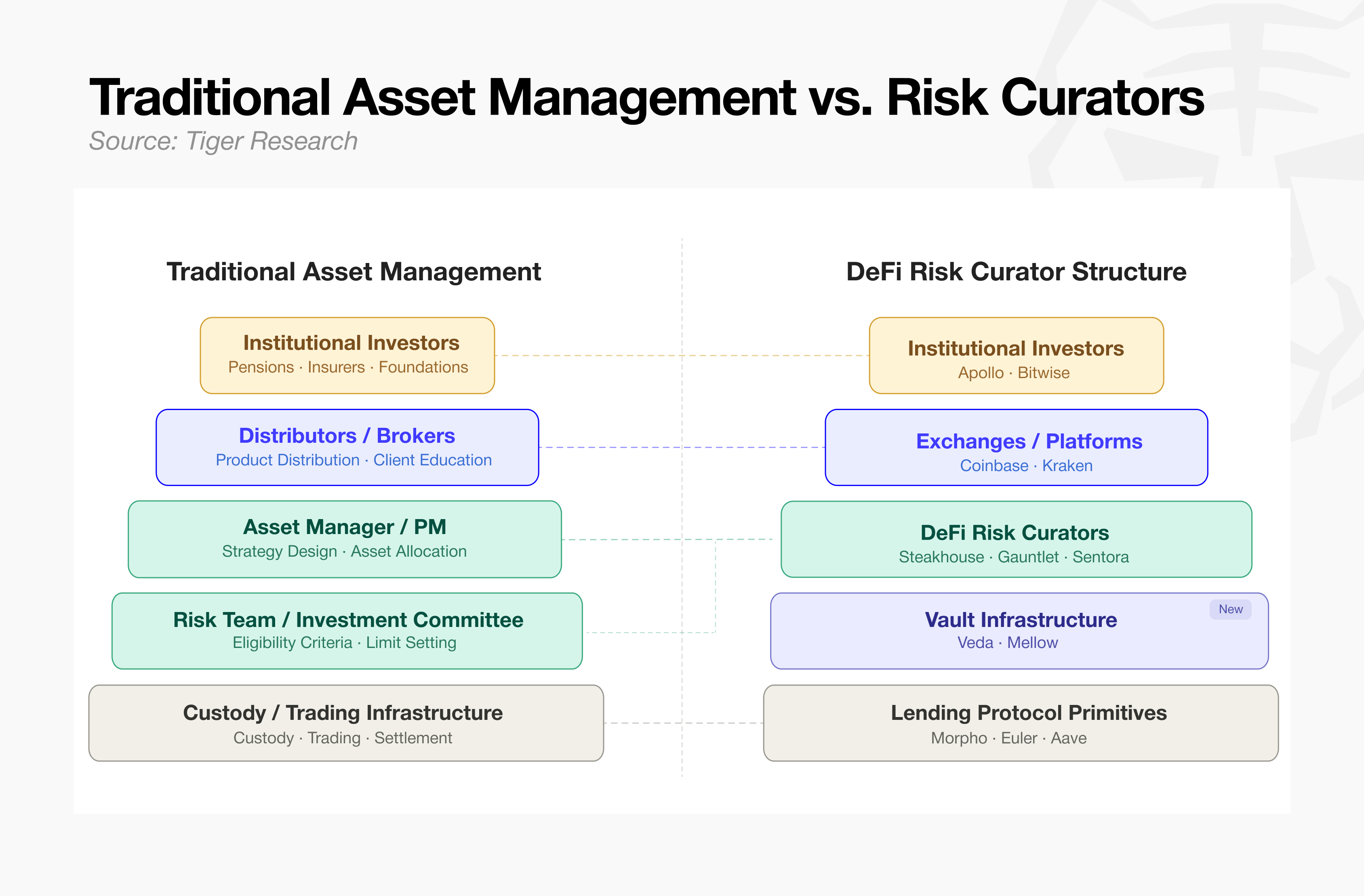

4. Traditional Asset Management vs DeFi Risk Curators

As Morpho fragmented the market, each collateral type needed a specialist to make the call. Professional risk teams like Steakhouse stepped in as DeFi risk curators. Through this shift, DeFi is starting to resemble the traditional asset management process.

Reading the diagram from top to bottom shows how today’s DeFi infrastructure replicates the division of labor in traditional finance onchain.

Capital sourcing and distribution (top): Institutional investors sit at the top as the capital source. Their large pools flow into the onchain ecosystem through major CeFi exchanges and platforms, which take the role of TradFi distributors (brokerages).

Strategy design and risk control (middle): Below sit the DeFi risk curators, who decide how the incoming capital is managed. Like the portfolio managers (PMs) and risk committees of traditional asset managers, they set asset eligibility and limits and design the overall investment strategy.

Product assembly and custody (bottom): The curator’s strategy becomes an investable onchain product through the vault infrastructure beneath it. At the very bottom, the lending protocol primitive holds the assets and executes settlement in code, taking the place of TradFi’s custody and trading infrastructure.

From capital sourcing through management and custody, the entire process now mirrors the division of labor seen in traditional finance. For incumbent TradFi institutions, onchain lending is no longer unfamiliar territory but a structured market they recognize, and the opening for entry follows naturally.

5. A TradFi-Like Industry: Where Is the Opportunity?

As onchain lending infrastructure adopts a division of labor similar to TradFi asset management, the door has opened for institutional entry. But not every layer carries the same barrier.

Distribution layer: Customer-facing market, already saturated by major crypto firms. It is inefficient for TradFi firms to fight head-on at the point of contact.

Management layer: A field driven entirely by financial expertise and manpower. Evaluating, controlling, and packaging asset risk matches the core work of traditional asset managers. Without building complex systems, they can apply their existing risk management capability onto already-built modular infrastructure and immediately secure a business model.

Custody and infrastructure layer: Asset custody and trade processing, a technology-intensive business that demands deep blockchain engineering capability. It is unrealistic for TradFi firms to build their own systems and compete here.

Unlike the other layers, which require technology or platform incumbency, the management layer is the clearest window of opportunity, where TradFi firms can take market leadership using only the risk management capability they already hold.

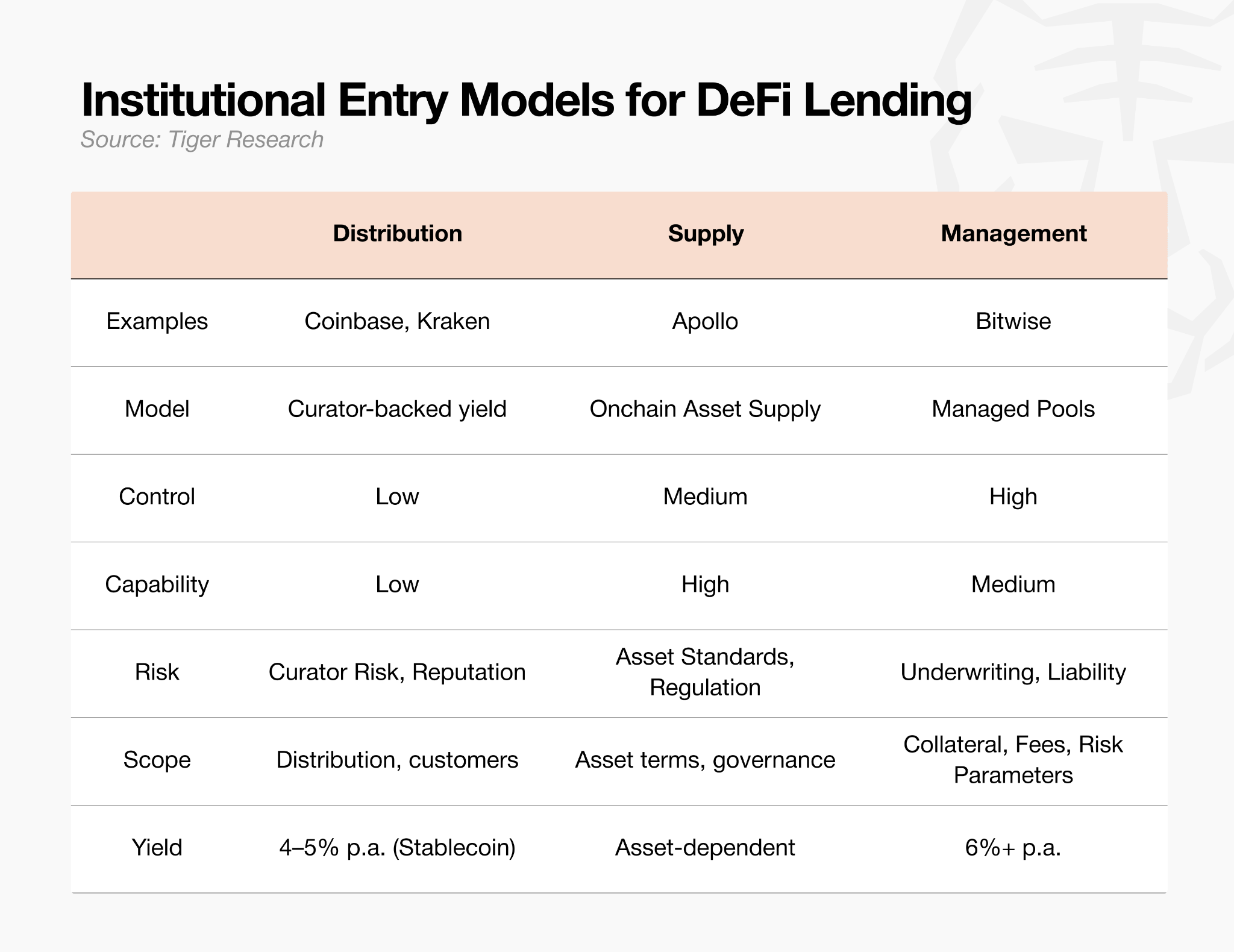

Institutions currently enter the DeFi market through three paths: Distribution, Supply, and Operator. Whichever path is chosen, the engine driving the market is the asset manager’s “risk curation” capability.

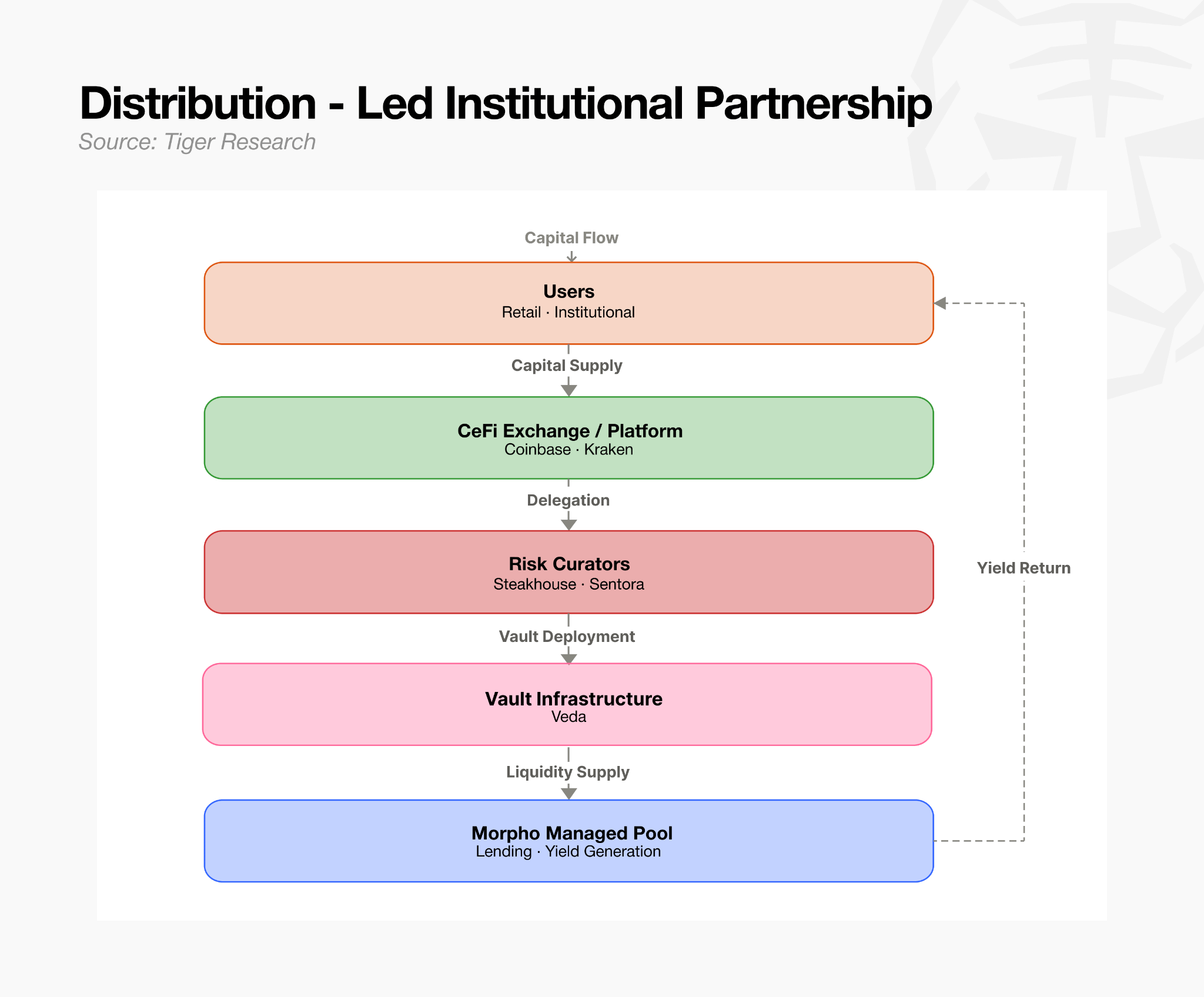

5.1. Distribution: Curator as Backend

Connect a proven external curator as the backend and enter the market quickly. This fits exchanges and fintechs with customer channels but no in-house management capability. Strategy is outsourced, but reputational risk and accountability for the curator chosen stay in-house.

This is the route chosen by centralized exchanges with strong customer touchpoints but no appetite for managing the complex risks of onchain lending directly. They have connected verified external risk curators as the backend and launched lending services. The exchange distributes large pools of capital through its own platform, while collateral evaluation and risk management are handed off entirely to the partner risk curator

5.2. Supply: Push Assets onto Onchain Rails

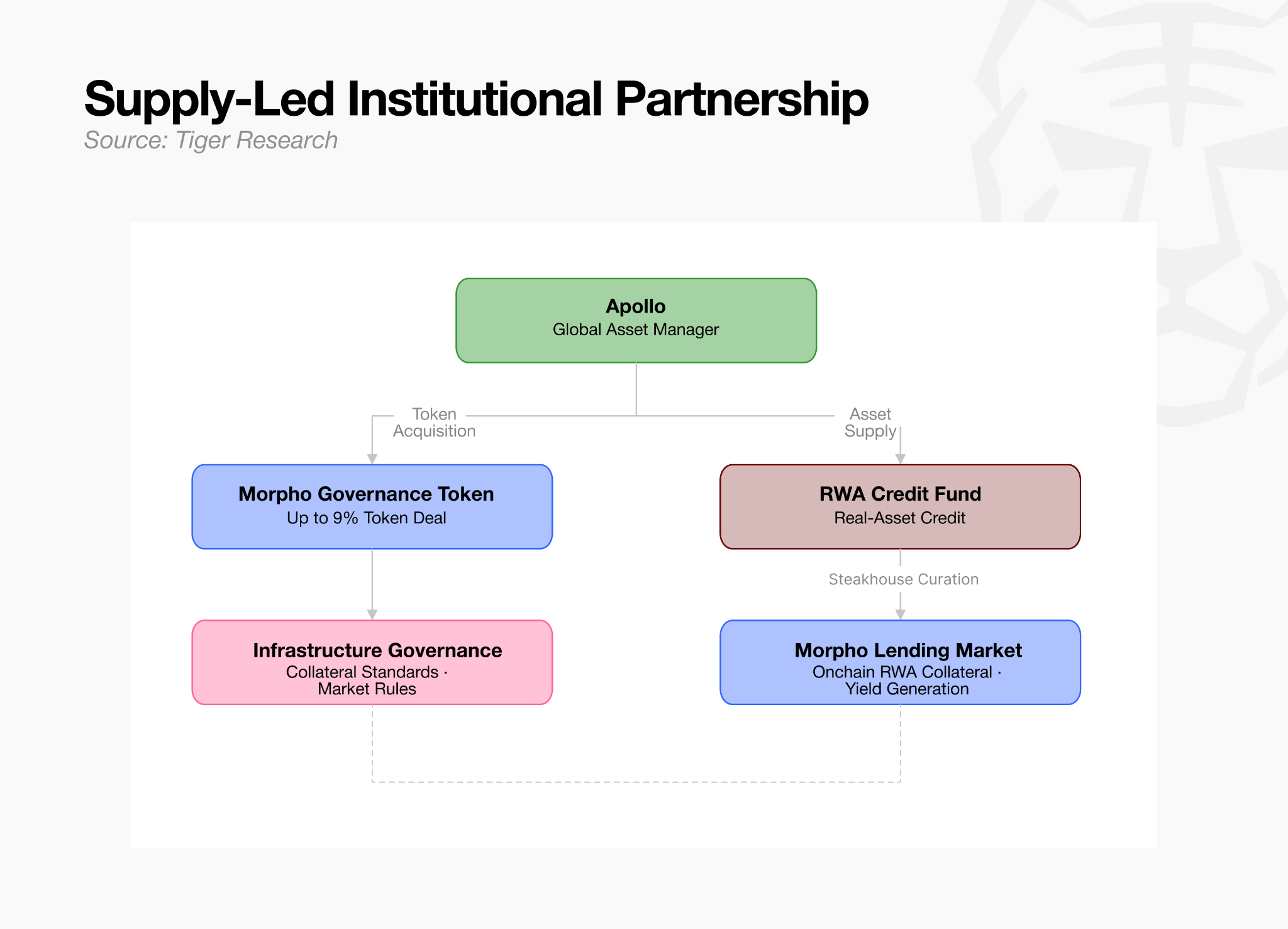

Asset managers holding RWAs or credit assets supply those assets directly to the market. Like Apollo, they can supply assets while acquiring Morpho governance tokens, shaping the standards (such as collateral criteria) of the infrastructure that will carry their assets. The hard parts are asset standardization and regulatory infrastructure build-out.

Large private equity funds or institutions holding real-world assets (RWAs) place their own capital directly onto onchain rails. Apollo went beyond simple asset supply and acquired governance tokens of major lending protocols. The move aims to drive the rules and standards so that its real-world assets are recognized as more favorable and safer “official collateral” in the onchain market.

But asset suppliers cannot register just any asset as collateral. Someone has to coldly assess whether the asset is genuinely safe and whether it can be liquidated immediately when an onchain liquidation event hits. That requires the rigorous evaluation capability of a risk curator who vets and vouches for asset eligibility. In the end, the supply path also stands only when an asset manager’s risk validation capability backs it.

5.3. Operator: Become the Curator (Bitwise)

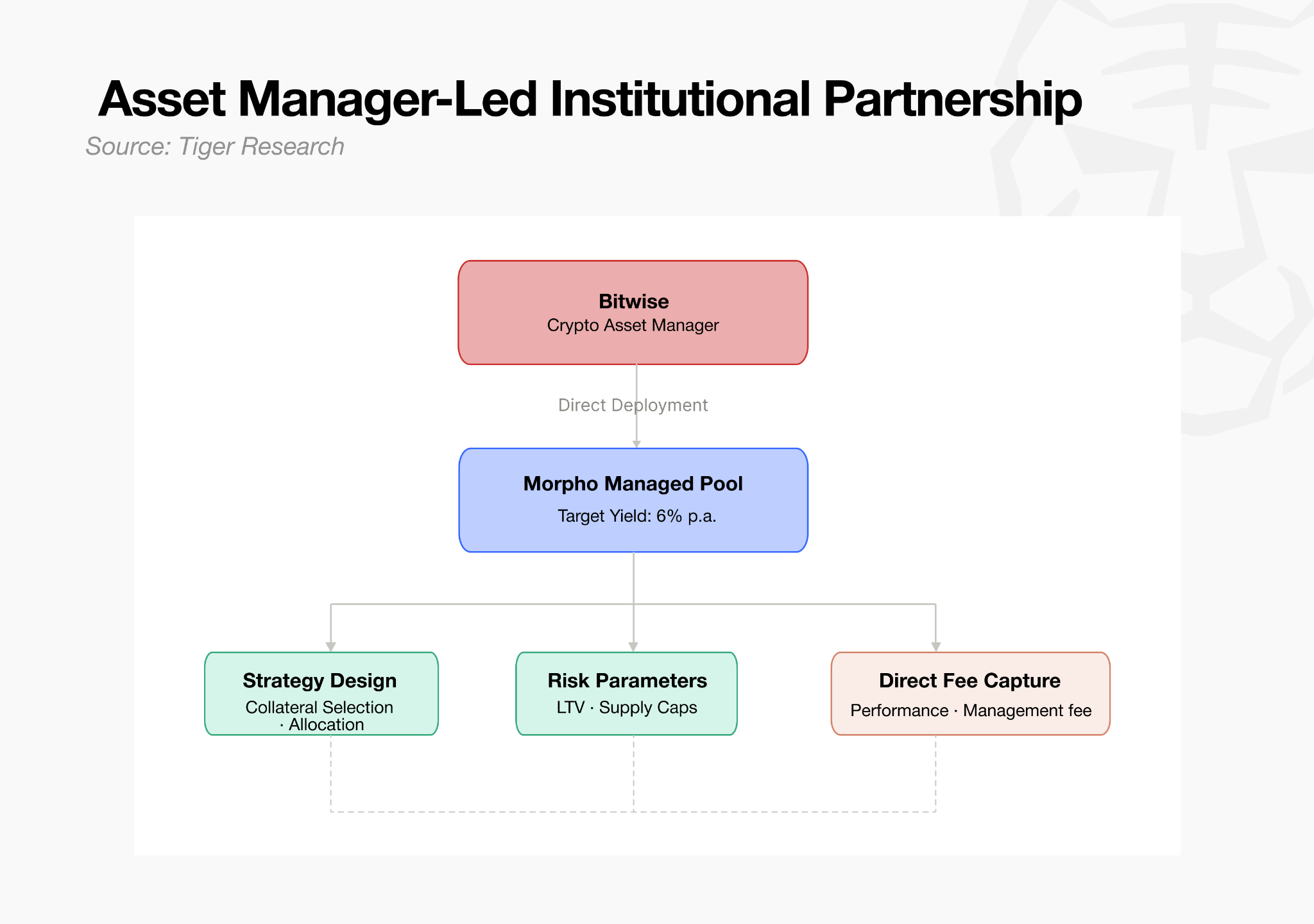

An asset manager designs its own strategy and runs its own vaults. Bitwise defined the onchain vault as “ETF 2.0” and jumped in directly. This path holds the strongest controls over fees and collateral standards, but the manager also bears full responsibility for any operating failure. It fits asset managers with an in-house risk team.

This is the path where a traditional asset manager steps out as a risk curator itself, without relying on external platforms. Bitwise defined the onchain lending vault structure as “ETF 2.0” and entered the market directly. Drawing on its own portfolio construction capability and risk control system, it designs and controls the vaults itself, securing the management fee model directly onchain.

6. Before Big Capital Arrives

Looking at the trajectory so far, traditional asset managers are likely the best positioned as onchain lending matures. As the DeFi ecosystem modularizes and divides labor, the capability the market actually needs has shifted. Not the ability to write code, but the traditional finance expertise of underwriting collateral and setting risk limits. The competitive edge of institutions that have done this work for decades carries over onchain.

But today’s DeFi market is too small for global mega-managers to step in directly. The global traditional asset management market is roughly $147T. BlackRock alone runs $14T in AUM. By contrast, the entire DeFi market is about $80B, and the slice handled by risk curators is just $7B. That is 1/2,000th of BlackRock’s AUM.

But the sheer scale gap is what shows the runway for growth. Institutional capital does not enter places where risk is not controlled. Once risk curators lay rails for capital to run safely onchain and the regulatory outline takes shape, the story changes. Even a sliver of the $147T flowing in expands the $80B market quickly.

Some opportunities exist only while the market is small. The main players in the risk curator market today can be counted on one hand. Rails are required for institutions to come onchain, and the teams that lay them first set the standards.

Institutions that arrive later will get a safer, clearer market. They will also be one of many participating inside standards that have already been set.

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.