The Senate Banking Committee passed the CLARITY Act on May 14. Indirect stablecoin interest has been banned, but activity-based rewards are now permitted. Several other significant provisions were also amended. What business opportunities do these changes create?

Key Takeaways

Stablecoin yield dispute resolved via bipartisan compromise: passive holding interest banned, activity-linked rewards permitted. Largest legislative obstacle cleared.

Senate Banking Committee vote complete. Hard deadline: August recess. Executive pressure: Trump targeting July 4 signing. Final passage expected by July.

Key provisions on enactment: indirect passive interest banned; activity-based rewards (payments, trading) permitted; unregistered token sales allowed within caps; securities reclassification safe harbor established; sufficiently decentralized DeFi protocols exempt from SEC oversight.

Business model implications: activity-based lock-in reward models activated to reduce capital outflow; token IB ecosystem (advisory, investor matching, issuance SaaS) emerges as a new market vertical.

2026: institutional order replaces the ungoverned era as jurisdictions globally benchmark U.S. rules. Dual dynamic: institutional capital drives mass adoption; compliance costs slow early-stage innovation.

1. What Stalled the CLARITY Act?

The CLARITY Act’s core purpose is to codify the jurisdictional boundary between the SEC and CFTC. What delayed it by four months was a single provision: the stablecoin interest ban.

The central dispute: should platforms continue paying 4-5% annual yield to stablecoin holders? Banks demanded a full ban, citing deposit outflows. The crypto industry pushed back, calling it a threat to core business models. Coinbase’s opposition to the full ban stalled negotiations into May.

On May 1, Republican Senator Thom Tillis and Democratic Senator Angela Alsobrooks introduced a bipartisan compromise: ban interest on passive holding, but permit rewards tied to bona fide activity such as payments, trading, and staking. Coinbase, which had blocked the January markup, announced support the same day.

With the White House, SEC, and Treasury aligning behind the compromise, the Senate Banking Committee passed the amended bill 15-9 on May 14.

2. How Long Until Final Passage? (~2 Months)

The May 14 committee vote completed the markup phase. Four steps remain before the bill becomes law:

Consolidation of three bills into one unified text

Senate floor vote

House floor concurrence vote

Presidential signature and enactment

Two factors make July passage the most likely outcome.

First, the August recess is the practical deadline. Approximately 11 weeks remain before Congress breaks. Missing that window means the bill collides with midterm campaign season and the budget cycle, making passage within the 119th Congress uncertain.

Second, the Trump administration is actively pushing. The president has publicly stated a July 4 signing goal, roughly 7 weeks out. The administration has already applied pressure to Congress before, and will again if the schedule slips. Critically, the stablecoin interest provision, which triggered two failed markups over four months, is now resolved.

The hardest part of the negotiation is done.

3. Key Provisions of the CLARITY Act Amendment

Regardless of when the bill achieves final passage, the May 14 markup already signals a significant shift for the U.S. cryptocurrency market. The sections below examine which provisions matter most.

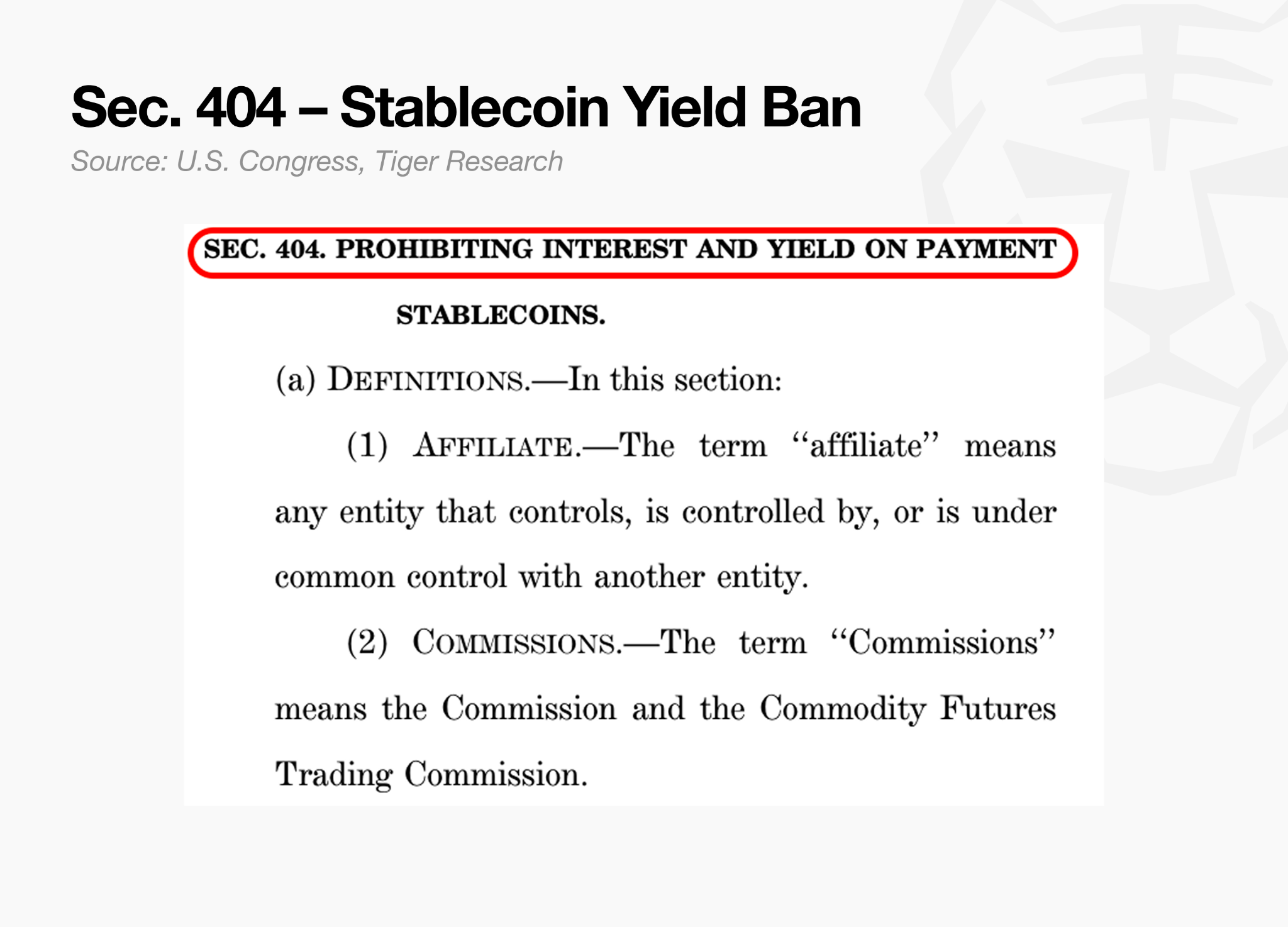

3.1. Prohibition on Indirect Stablecoin Interest (Sec. 404)

Stablecoin yield was the sharpest point of conflict between the banking sector and the crypto industry. Banks called for a complete ban; crypto firms argued that paying yield on stablecoins was fundamental to their business.

Sec. 404 resolves the dispute by prohibiting exchanges from passing interest to users indirectly. The prior arrangement worked as follows: a user holding USDC through Coinbase would earn yield, with funds flowing through issuer Circle into U.S. Treasuries, and the resulting interest returned to the user. From the user’s perspective, this was functionally identical to a bank deposit.

From the bank’s perspective, it represented a direct deposit substitution risk. That is what drove the banking sector’s strong opposition.

The bill bans yield on passive holding and permits only rewards tied to bona fide activity. However, the definition of “activity” remains unspecified in the bill text. Whether payments, governance votes, or app logins qualify is delegated entirely to subordinate rulemaking by Treasury and the CFTC.

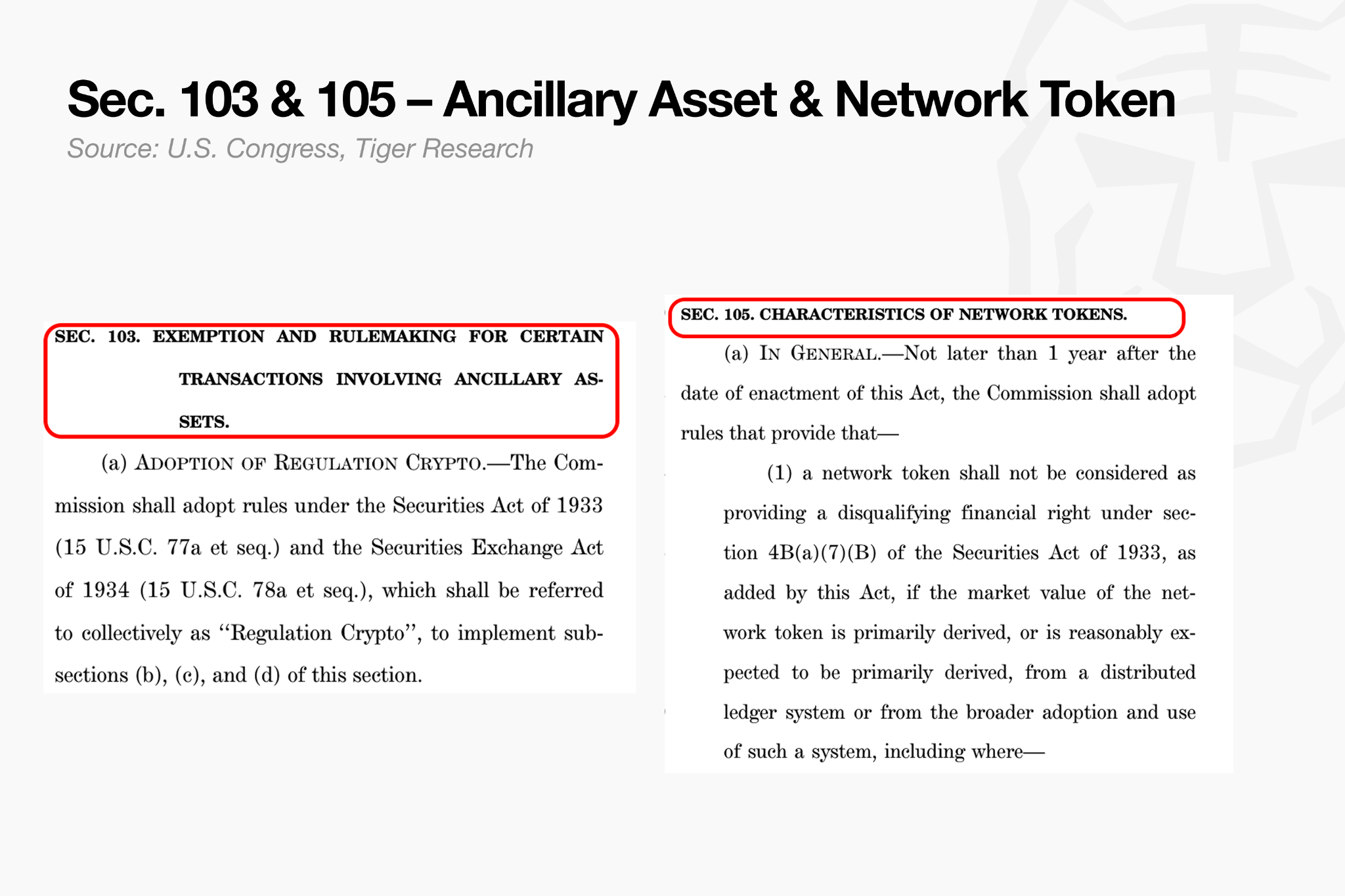

3.2. Legal Token Issuance Pathway (Sec. 103 + 105)

Together, these two provisions establish a legal framework for token sales to U.S. investors.

Sec. 103 (Reg Crypto Exemption): Creates a registration exemption allowing token sales to U.S. users without SEC registration, up to $50M annually or 10% of circulating supply, whichever is greater, with a $200M cumulative cap.

Sec. 105 (Token Design Safe Harbor): Specifies that governance rights or staking rewards alone cannot classify a token as a security. Tokens already ruled non-securities by courts cannot be reclassified by the SEC.

The two provisions serve distinct but complementary roles. Sec. 103 opens the path to selling tokens; Sec. 105 ensures that path remains open by blocking post-sale reclassification. Neither works without the other. Sec. 103 alone leaves issuers exposed to retroactive SEC action. Sec. 105 alone offers classification protection with no route to market.

For the first time, issuers have a genuine alternative to the default practice of blocking U.S. users. The U.S. market is now a viable option to incorporate into issuance design.

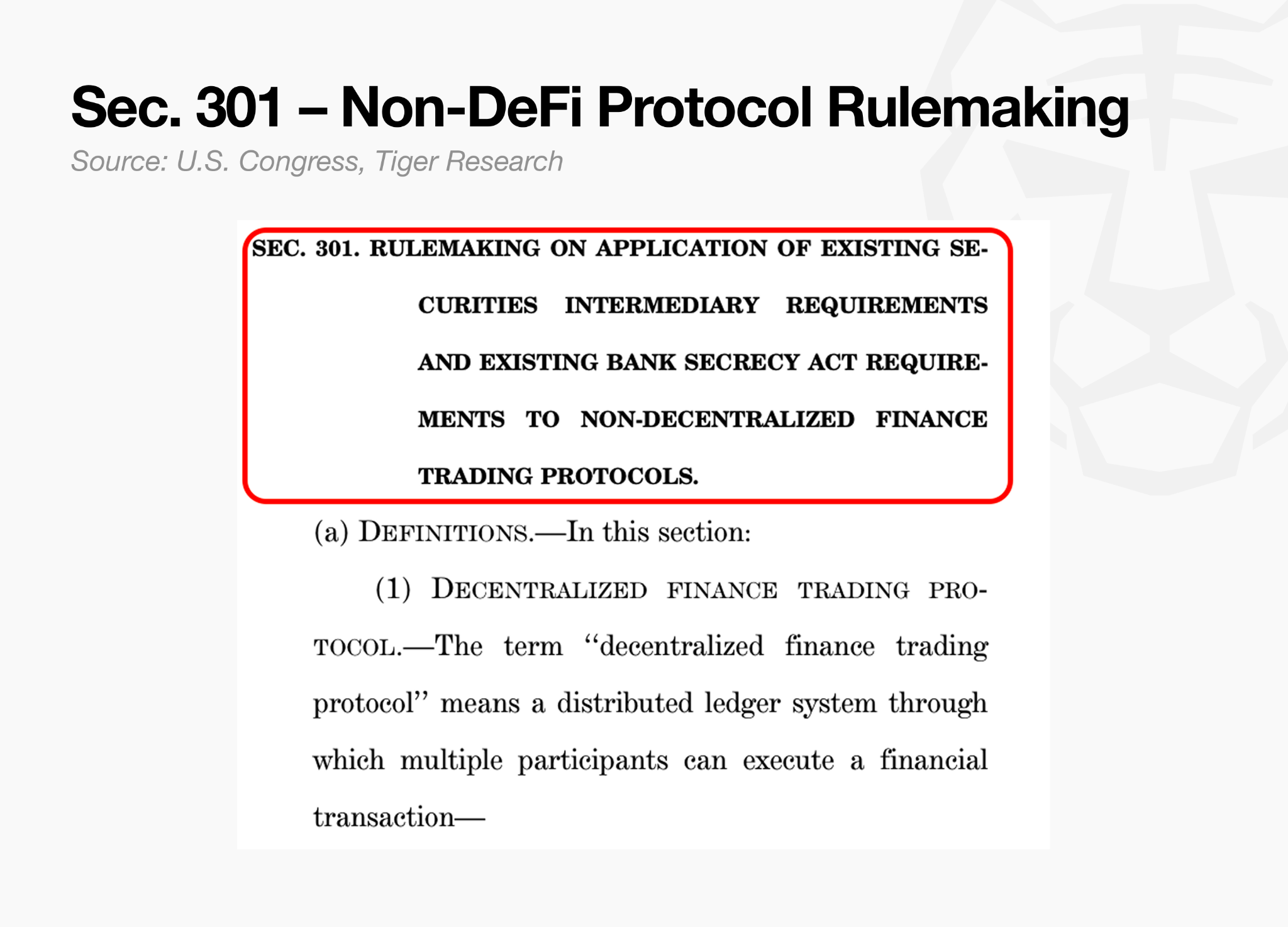

3.3. DeFi Regulatory Exemption (Sec. 301)

For the first time, DeFi protocols have a legal path to exemption from U.S. regulatory oversight. The SEC can no longer require a qualifying DeFi protocol to register as a securities platform.

The exemption is conditional. A protocol must be sufficiently decentralized, meaning no single party can unilaterally modify its operation. Concentration of admin keys, upgrade authority, or security council powers in one entity disqualifies a protocol.

Emergency interventions in response to security incidents, however, are not treated as centralized control. Protocols can maintain decentralization while retaining the ability to respond to exploits and breaches.

Decentralization is no longer a design philosophy. It is now a prerequisite for U.S. market access.

4. Post-CLARITY Strategy

4.1. Activity-Based Reward Businesses

The bill text (Sec. (c)(3)(A)) lists payments, governance voting, staking, and USDC transactions as explicit examples of qualifying activity. Based on this, activity can be broadly defined as specific, utility-driven user actions that contribute to blockchain network or platform activation, as distinct from passive holding.

The mechanics mirror a credit card cashback model. Rather than paying interest on deposits, platforms reward users only when a qualifying action is taken, with rewards accruing proportionally to balance. Three categories of beneficiaries emerge:

Exchanges and crypto apps can move beyond competing on fee reductions. By linking rewards to actual trading or in-app engagement, platforms give users an incentive to keep assets on-platform and remain active, converting idle deposits into locked-in, active capital.

High-traffic platforms and traditional card companies can fund customer reward programs through Treasury yield generated by stablecoin reserves rather than their own marketing budgets. This externalizes reward costs, reduces direct marketing spend, and allows platforms to retain a portion of yield as margin.

DeFi protocols with established staking infrastructure stand to benefit most. Platforms unable to build their own reward systems will rely on institutionally recognized staking providers, likely producing a winner-takes-most dynamic among the most stable and credible protocols.

In summary: strong capital lock-in through activity rewards, marketing cost reduction via yield externalization, and new B2B revenue streams.

4.2. Legal Token Issuance Businesses

Sec. 103 sets a $50M annual fundraising cap ($200M cumulative), and Sec. 105 protects lawfully issued tokens from post-sale reclassification as securities. Together, these provisions are best understood as the legalization of public token sales (ICO/IDO) targeting U.S. investors, and a catalyst for rapid growth in compliant issuance infrastructure demand.

The ecosystem will broadly mirror traditional IPO infrastructure, with three analogous business categories emerging:

Issuance infrastructure platforms will offer modular, SaaS-based systems covering KYC, accredited investor verification, automated disclosure, token lockup management, and treasury administration. Each project using the platform generates recurring B2B revenue without rebuilding infrastructure from scratch. Coinbase’s Echo is an early example of this model.

Issuance advisory firms and major VCs will provide end-to-end services spanning token structure design, regulatory compliance, and post-issuance dispute response. This mirrors the investment banking role that Goldman Sachs and Morgan Stanley play in traditional IPOs. Firms such as a16z and Paradigm are expected to internalize advisory functions directly.

Accredited investor matching businesses will connect global project teams with U.S. investor databases, a task that is currently near-impossible to execute independently. Traditional asset managers and digital asset IR firms will operate as dedicated brokerages, facilitating capital connections efficiently within statutory caps.

These three models will likely settle into two market structures: an integrated full-service model that handles KYC, advisory, and matching under one platform (as seen with CoinList, Republic, and Legion), and a specialized modular model where projects outsource specific functions to dedicated legal, financial SaaS, or IR providers.

In summary: a legal capital-raising channel that removes regulatory risk, and the emergence of a token investment banking ecosystem.

One caveat: quality projects seeking long-term, compliant operations will adopt this infrastructure readily. Whether the majority of the market, still oriented toward speculative projects, will forgo the flexibility of offshore issuance for a stricter U.S. regulatory environment remains an open question.

5. 2026: The Year Market Rules Are Rewritten

2026 marks a decisive shift in the global cryptocurrency market. If the CLARITY Act passes and takes effect in July, the consequences will extend well beyond U.S. borders. Resolution of U.S. regulatory uncertainty opens the door for institutional capital to enter the market through legitimate channels.

The more consequential dynamic is the reaction from other jurisdictions. Governments will not passively watch U.S. capital consolidate dominance over the global crypto ecosystem.

They will monitor in real time which businesses scale under the U.S. framework, then benchmark those results to design tailored domestic regulations, moving quickly to retain domestic capital and competitive positioning.

Formal regulation brings clear tradeoffs on both sides.

Upside (scale and mass adoption): Regulatory clarity clears a path for institutional capital from traditional finance and big tech. Consumer-familiar, compliant products such as activity-based reward models will drive crypto beyond its niche audience toward genuine mass adoption.

Downside (cost and innovation drag): Projects unable to bear compliance costs will be displaced. Businesses that grew in regulatory gray zones will face pressure to exit or restructure. The raw pace of innovation and the creative freedom characteristic of early crypto will slow as the industry moves inside institutional frameworks.

Ultimately, 2026 is the year the ungoverned era ends and institutional order takes its place. Those who track multi-jurisdictional regulatory shifts and establish compliant business infrastructure ahead of others will capture a disproportionate share of the next generation of value creation in crypto.

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.