1. Agent-Era Payment Infrastructure Has Already Begun

Over the past year, global big tech firms, card networks, and exchanges have each announced their own agent payment standards (hereafter, “agent”). Eight standard protocols were released in 2025 alone, with partnership announcements continuing to follow.

Capturing the payment standard carries the greatest weight at moments of structural transition. In the era of offline commerce, Visa and Mastercard locked in the card payment standard and came to dominate the market. Every card transaction since has been routed through their networks.

When commerce shifted online, a new set of players emerged. PayPal built an online payment service on top of email-based remittance, and Stripe followed. The next payments market is agents. With AI now mainstream, no one disputes that the agent era is coming.

When people picture AI agent payments, two scenes typically come to mind: an agent that finds and purchases products on the user’s behalf, and agents that transact directly with one another without human involvement.

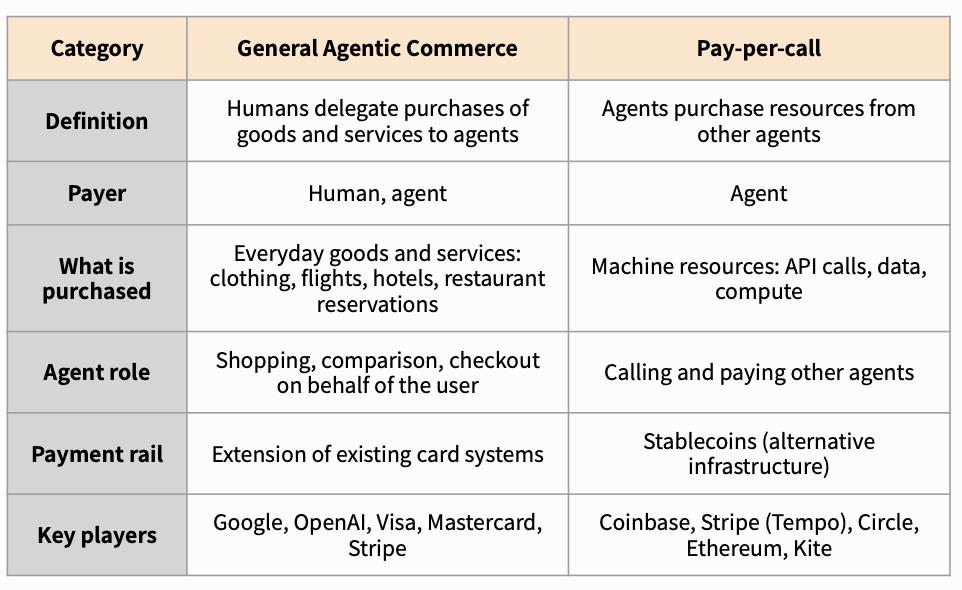

These represent the near and the more distant future, respectively. Agent-executed orders under user instruction fall under General Agentic Commerce, which is already taking shape. Direct agent-to-agent payments fall under Pay-per-call, a more distant future state.

The two categories may appear to stand in opposition, but they are simply players solving different problems. This report examines how each set of players is establishing standards across the two categories of the agent payments industry.

2. General Agentic Commerce

In General Agentic Commerce, humans delegate shopping to agents. Within a given platform, the user registers a card and sets the scope of delegation, after which the agent executes within that platform.

Take an example. The user tells the agent, “Prepare my Tokyo business trip for next week. Budget is 2 million KRW (~$1,400 USD).” That single instruction grants the agent conditional payment authority. Within the budget, the agent selects and sequentially pays for the flight, hotel, airport transfer, currency exchange, and travel insurance using the user’s card.

For this process to work, the agent must first interpret the user’s intent and find the right products, then complete payment securely. The structure breaks into two layers:

Discovery layer: the agent finds products on a platform on behalf of the user

Payment layer: the agent pays within the scope set by the user

Some leading players focus on a single layer, while others aim to capture both.

Alphabet Inc. (GOOG)

Core Technology

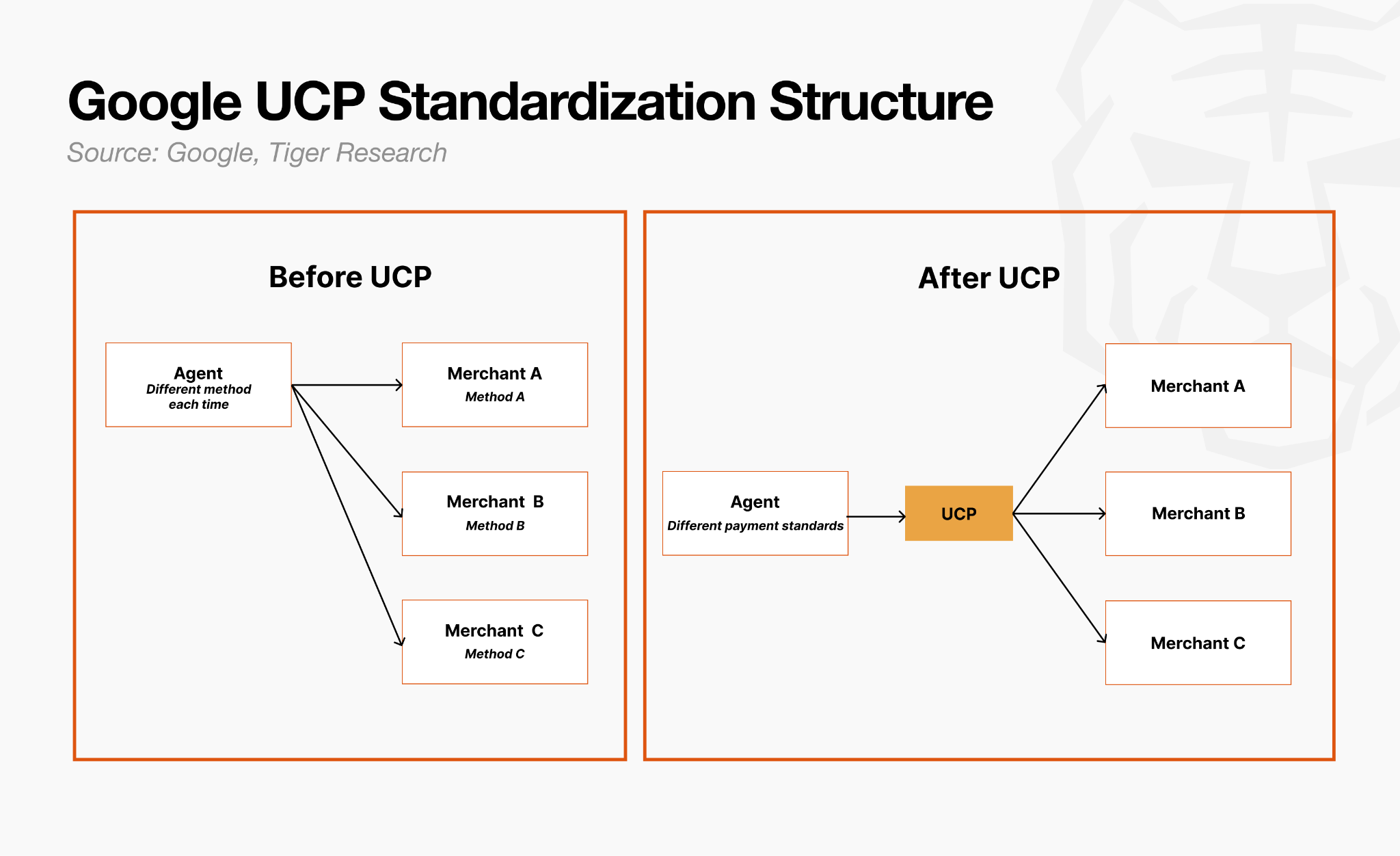

Google is moving to capture both the discovery and payment layers, anchored on two standards: UCP and AP2.

UCP (Universal Commerce Protocol) is the standard governing how agents communicate with merchants.

For an agent to handle shopping on behalf of a user, it must run through countless interactions with different services. The problem is that every service is structured differently. Each time an agent discovers a new service and initiates a transaction, a separate integration has been required. Google aims to eliminate this inefficiency through UCP.

Once a merchant configures itself to the standard, any agent can connect with that merchant in the same way thereafter.

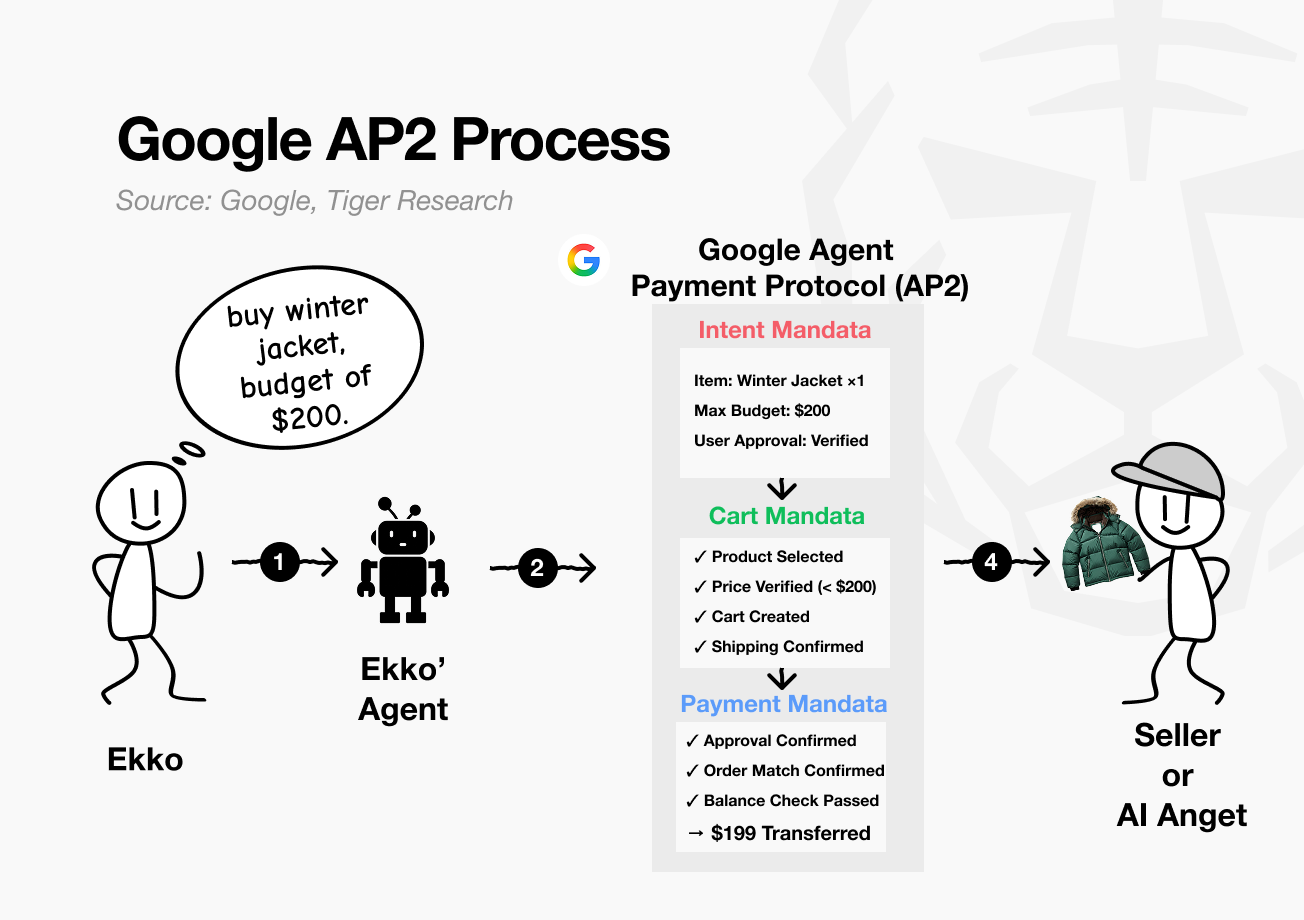

AP2 (Agent Payments Protocol) is the authority standard that guarantees “who authorized what, and up to how much” at the moment of transition from discovery to payment.

When a person presses the payment button directly, the actor and accountability are clear. When an agent pays on the user’s behalf, the scope of authority and locus of responsibility become ambiguous. AP2 records the user’s initial instruction as a tamper-proof digital contract (Mandate). Agents can act only within the user’s instruction, and after the transaction, a traceable record remains of who authorized what and when.

In short, if UCP is the standard for discovery, AP2 is the standard that signs accountability into the transaction.

Core Business

Google’s current revenue rests on two pillars: Advertising and Cloud. As of 2025, advertising revenue stood at $262.7 billion and cloud revenue at $58 billion, accounting for the bulk of total revenue of around $400 billion.

The issue is that the landscape is shifting. As consumers begin to delegate purchases to AI agents instead of typing keywords into a search bar, the existing search advertising model is destabilized. Google’s investment in UCP and AP2 starts here. It is preparing for what comes next.

Google is evolving AI Mode into the next stage of search. What began as a Q&A layer will progressively shift into an agent that executes purchases on the user’s behalf. The moment a merchant joins UCP and lists products, those products enter the agent’s transactable range.

Advertising: ad placement shifts from discovery to recommendation. Agents compare products against user criteria and shortlist; paid merchants surface at the top. Looks like a natural recommendation, but ads now sit at the recommendation stage. Advertisers spend less on stages that don’t convert; Google captures higher ad price per transaction.

Payment: AP2-based Agentic Checkout completes payment with one user approval. Google Pay becomes the payment route, accruing fees per transaction. Agent transactions are faster and more frequent than human ones. Small fees compound at scale.

Cloud: a possibility, not yet a revenue line. Merchants processing agent transactions need AI inference, data storage, and API integration. If that demand flows to Google Cloud, cloud revenue scales with the agent ecosystem.

Outlook

Google’s differentiator is its existing network.

Google led the internet era and already operates a near-complete payment infrastructure, including Google Pay and a vast merchant base. In the AI era as well, the company is at the forefront with Gemini, demonstrating sensitivity to technological change. User touchpoints through Android and Chrome are in place.

If UCP and AP2 take hold, users will conduct purchases end-to-end inside Google’s infrastructure. Merchant onboarding to Google’s infrastructure then follows naturally. Existing systems were built around humans, but UCP and AP2 are designed for agents. Merchants who fail to onboard lose competitive ground against rivals who do.

For merchants to reach buyers, onboarding to UCP and AP2 becomes the path of least resistance.

Google has done this before. In 2008, it open-sourced Android. Manufacturers joined, users grew, and Google’s own infrastructure such as Play Store and Google Pay layered on top. The result: Google became the largest beneficiary of the mobile market without manufacturing a single phone.

Once agent transactions form in earnest, Google is highly likely to walk the same path again. Buyers and merchants both move on its infrastructure, and Google captures revenue at every stage of the transaction.

OpenAI Group PBC

Core Technology

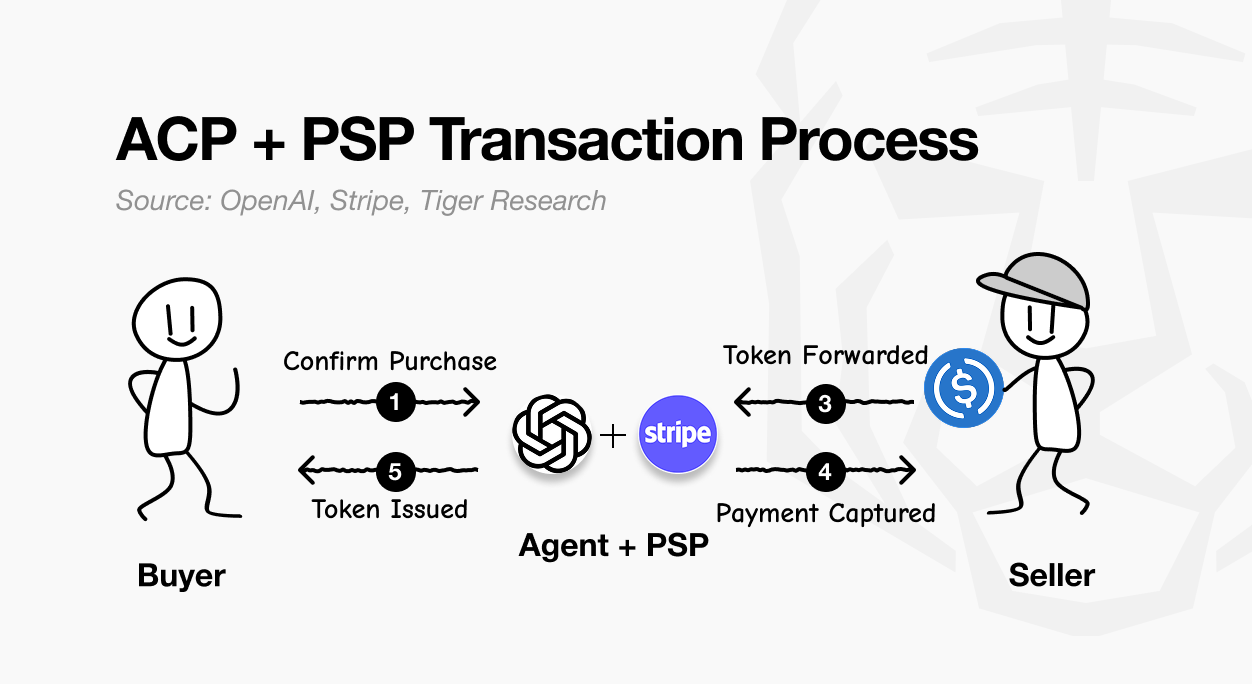

OpenAI co-developed ACP (Agentic Commerce Protocol) with Stripe and released it on September 29, 2025.

ACP is an open-source protocol that enables agents to call a merchant’s payment system and purchase products on the user’s behalf. ACP grants authority through a four-actor structure: 1) Buyer, 2) Seller, 3) Agent, 4) Payment Provider.

ACP’s central question was: “How much payment authority should an agent be given?” Handing the user’s card information to the agent would, in theory, allow the agent to pay at any merchant, in any amount, at any time. But a poorly trained agent could repeatedly purchase unnecessary items, and a hijacked session could be exploited.

ACP solves this through Delegate Payment. The user’s actual card information is never passed to the agent. Instead, the PSP (e.g., Stripe) receives the card information and issues a single-use token, and the agent handles only that token. The token carries four constraints:

Which merchant it can be used at

Up to what amount it can pay

When it expires

Which checkout session it is valid for

As a result, even if the agent malfunctions or is hijacked, the damage cannot extend beyond “this single shopping transaction.”

Core Business

OpenAI’s current revenue comes from three pillars. With approximately $20 billion in annual revenue (ARR basis) for 2025, ChatGPT subscriptions account for roughly 85% of the total. The remainder comes from API usage fees and enterprise contracts. It is a subscription model that grows linearly with user count.

The issue is that the ceiling of this structure is in sight. As long as OpenAI competes with Claude and Gemini on subscriptions, growth is tied to how many more users it can attract. ACP is an attempt to break through that ceiling. Transaction fees on top of subscription fees. Transaction count on top of user count. Growth layered on growth.

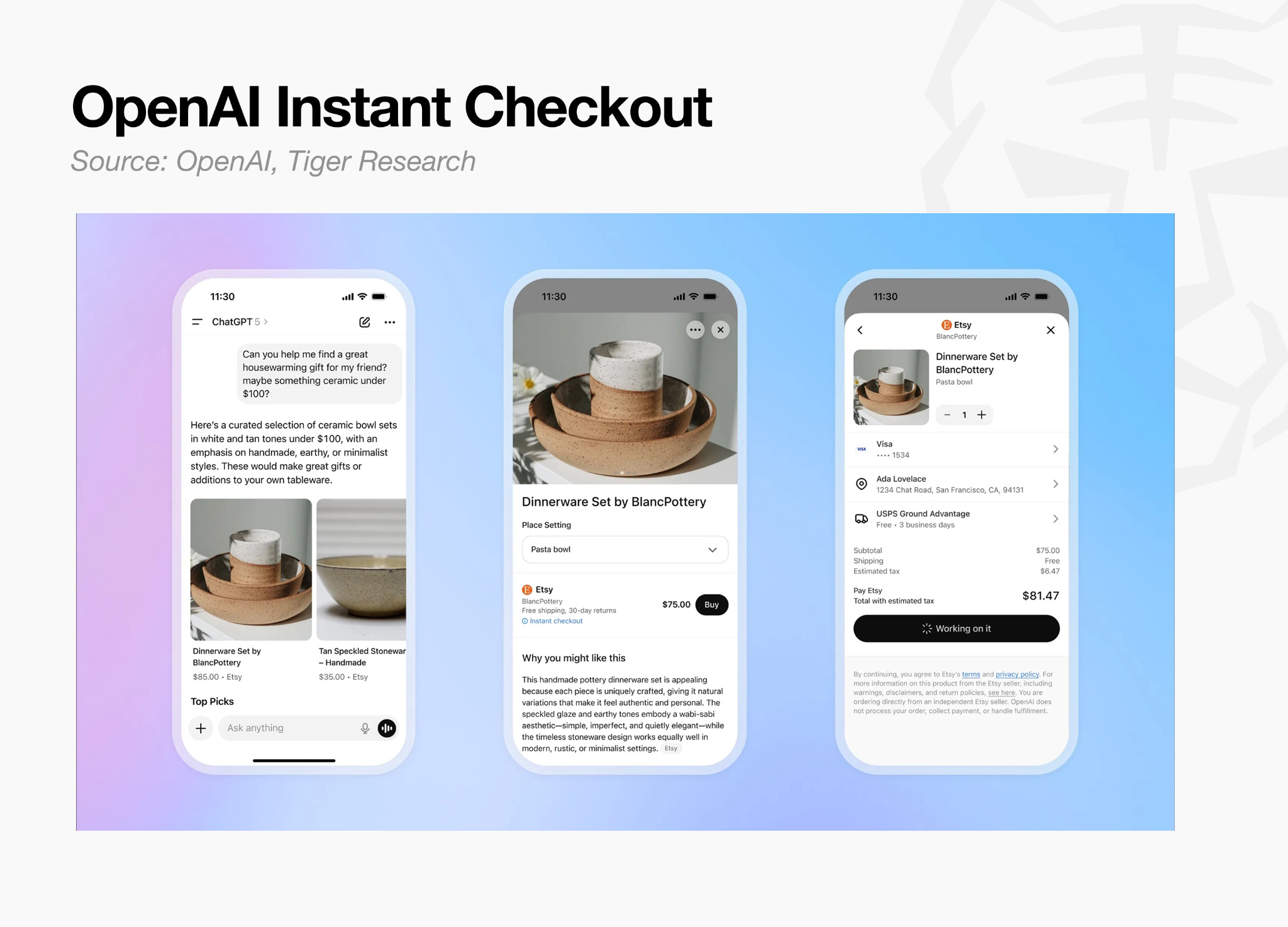

In September 2025, OpenAI launched Instant Checkout, completing payments inside ChatGPT. The structure imposed a 4% transaction fee for Shopify merchants. However, real-time inventory sync, gaps in tax processing infrastructure, and low conversion rates held it back.

Merchants pushed back, citing the difficulty of handling complex variables such as inventory status, tax processing, and price updates directly within ChatGPT. Walmart, in particular, disclosed that conversion through ChatGPT was only one-third of the rate on its own website.

OpenAI ultimately wound down Instant Checkout in March 2026, handing payment back to merchant apps and systems while restricting ChatGPT’s role to product discovery.

This is recalibration, not retreat. The acquisition of personal finance app Hiro Finance is expected to play a key role in this current adjustment. The plan is to upgrade the consumption pattern analysis, financial data management, and inventory, tax, and fraud detection infrastructure that held Instant Checkout back, then re-enter with in-house payments.

Once this ecosystem is in place, OpenAI achieves the structure it originally sought: ChatGPT holds the starting point of every transaction, opening the path to an intermediation fee model.

Outlook

Unlike Google, OpenAI must compete with a single platform: ChatGPT. The strategy is to leave payment, fulfillment, and customer relationships to merchants, while OpenAI captures Product Discovery alone.

OpenAI’s success depends on how well it satisfies both merchants and buyers. On the merchant side, cases like Walmart, where benefits and payment are deeply integrated into ChatGPT, must continue to multiply. On the consumer side, ChatGPT recommendations must convert into actual purchases. If one side falters, the other stalls. If too few merchants come in, the product selection thins; if conversion is low, merchants pull their investment.

OpenAI does not have the luxury of buying time with other assets, as Google does.

Ultimately, whether OpenAI can claim the opening scene of shopping depends on whether ChatGPT can replace the starting point of shopping the same way it replaced search. With Google running the same race through Gemini, this will be OpenAI’s most difficult fight.

Visa Inc. (V)

Core Technology

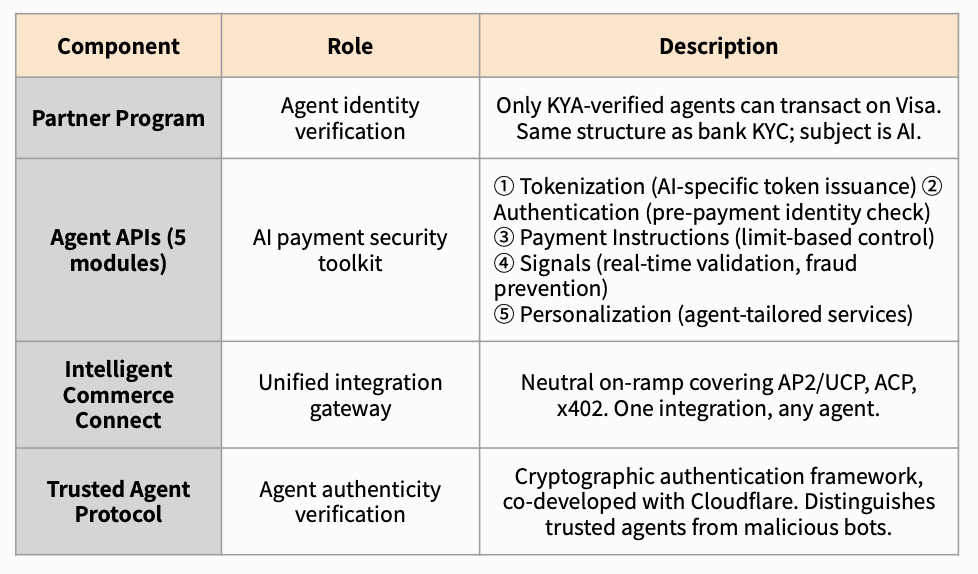

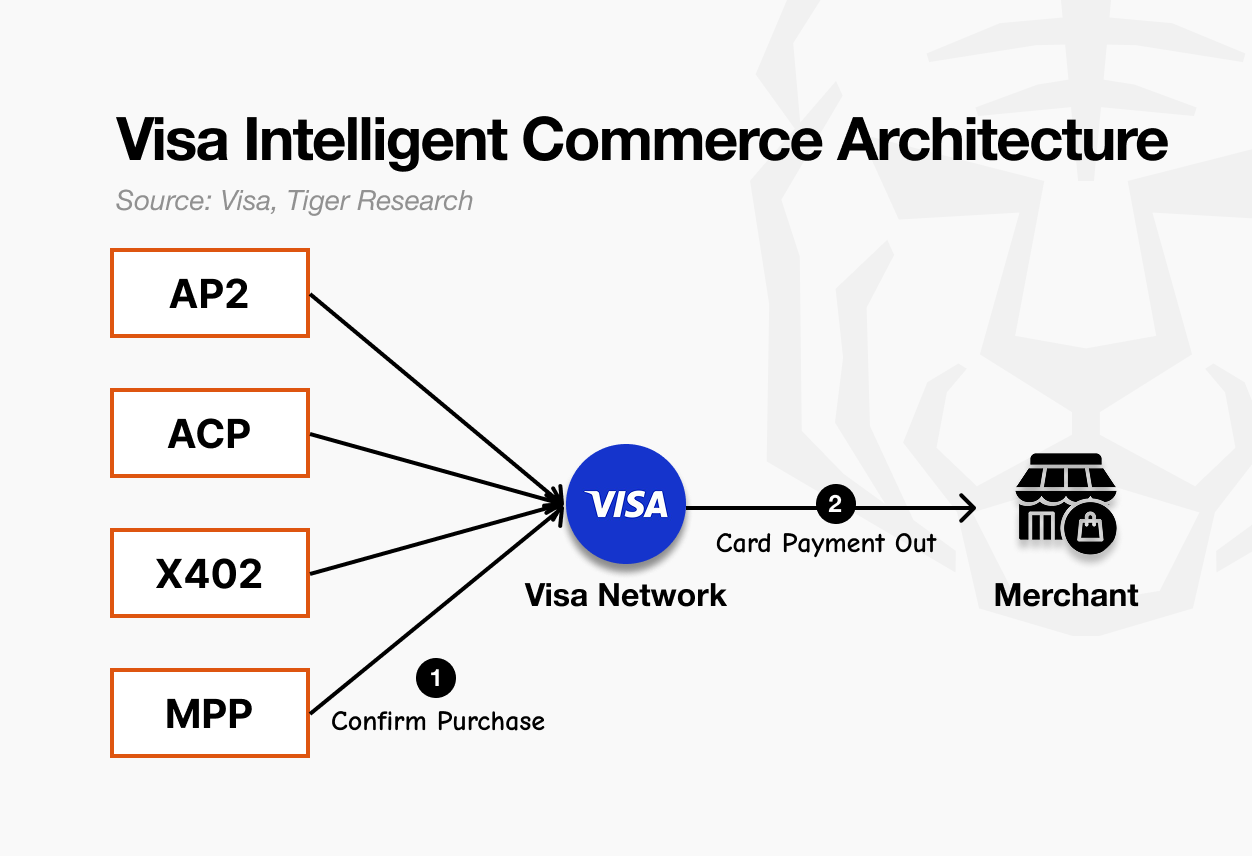

Visa is a company determined to keep its position as “the most widely used payment method,” even in the agent era. To prepare for agent payments, Visa chose a strategy of opening its existing payment network to agents.

In April 2025, Visa unveiled the Visa Intelligent Commerce portfolio. Visa Intelligent Commerce consists of four components that allow agents to pay just as humans do.

What the four components share is that Visa did not enter the protocol race directly.

Agent APIs is Visa’s own technology, activated when a Visa card is used. Intelligent Commerce Connect, however, is a strategy of accepting competing protocols as well.

Core Business

Visa’s current revenue comes from card payment fees. 2025 revenue was approximately $40 billion, with annual transaction volume of $14 trillion. Visa Intelligent Commerce does not generate separate revenue today. It is a strategic foundation for preserving the current revenue structure as the agent commerce era arrives.

The revenue paths remain unchanged.

First, payment fees. Whether an agent presses the payment button on the user’s behalf or a human does it directly, it makes no difference to Visa. As long as payment flows through the Visa network, card fees are generated. This is why Visa designed Intelligent Commerce Connect to accept competing protocols.

No matter which protocol the transaction runs on, fees still come in as long as payment is made with a Visa card.

Second, token infrastructure fees. Whenever an AI-specific token issued by Tokenization, one of the five Agent APIs, is used in a transaction, Visa handles credential conversion and authentication. When PSPs like Stripe and AI platforms use this token service, Visa collects a network usage fee. The token layer built on top of the card becomes a new fee axis in the agent era.

In the end, Visa’s strategy is not to win the protocol race but to charge fees on both winners and losers. On the buyer side, AI platforms such as OpenAI, Anthropic, and Perplexity are lined up as partners. On the seller side, e-commerce platforms like Shopify and PSPs like Stripe are in place. Whichever direction agent transactions grow, Visa sits at both ends.

Outlook

Visa’s outlook in one line: rather than competing with its own protocol, Visa moves toward becoming a payment infrastructure that embraces every protocol.

This choice matters because Visa’s position is fundamentally different from other players. Google, OpenAI, and Coinbase are playing a game in which their own protocol must win. AP2, ACP, or x402 must each become the standard for their respective ecosystems to maximize revenue. The protocol war itself is close to zero-sum.

Visa, by contrast, plays a game in which it does not matter which protocol wins, as long as payment passes through its network. The winner of the protocol war is irrelevant to Visa. It collects fees by attaching to whichever side wins, and continues to collect fees even when the market shifts to a different protocol.

The embrace strategy is not “yielding”; it is in fact the most advantageous position for Visa. This is a choice possible only because Visa already holds 4.8 billion cards and 150 million merchants, and only Visa, with these assets, could make this choice.

There is, however, one variable: stablecoins. If agent-to-agent payments bypass the Visa network entirely and settle directly on a blockchain, Visa loses the very layer from which it collects fees. Visa’s acquisition of Bridge, the launch of stablecoin cards, and its participation as a validator on the stablecoin-only chain Tempo are all responses to this risk.

For the embrace strategy to work, payment must pass through Visa’s infrastructure somewhere. Stablecoins are the only path that can threaten this premise itself.

In the end, Visa’s reason for not aiming to win the protocol war is clear. Holding the existing position of the card network alone is enough to make Visa the largest beneficiary of the agent era. The single point to watch: how quickly stablecoins begin to actually bypass the card network.

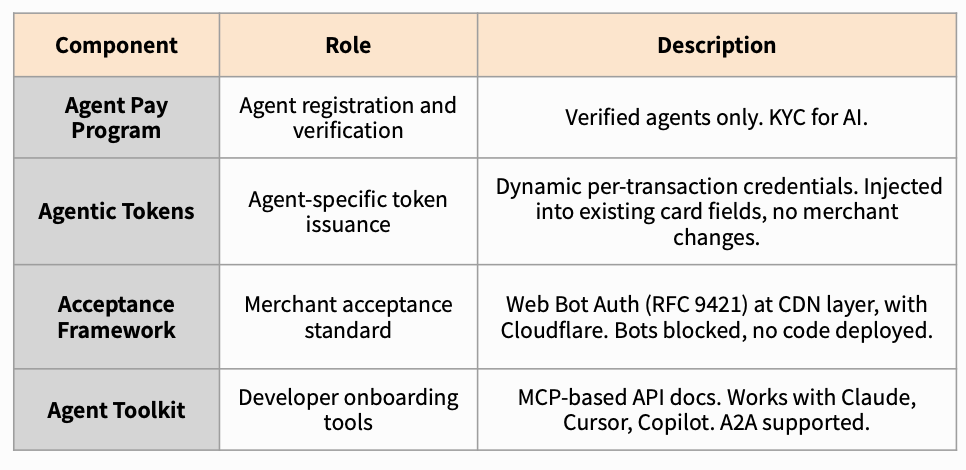

Mastercard Incorporated (MA)

Core Technology

Mastercard plays the same game as Visa. It is a company aiming to keep the card network’s position even in the agent era. Mastercard chose a strategy of opening its existing payment network, operating across more than 210 countries worldwide, to agents, but built the architecture so that merchants could easily onboard onto its system.

In April 2025, Mastercard launched Mastercard Agent Pay, followed by developer tools in September and the Agent Pay Acceptance Framework in October, steadily building out its agent payment system.

What the components share is that Mastercard is not trying to dominate the market with its own protocol. The strategy is to ensure Mastercard intervenes at the moment of payment and authentication, regardless of which direction the market moves. It is the same “payment-layer neutrality” strategy as Visa, but Mastercard concentrates on merchant acceptance.

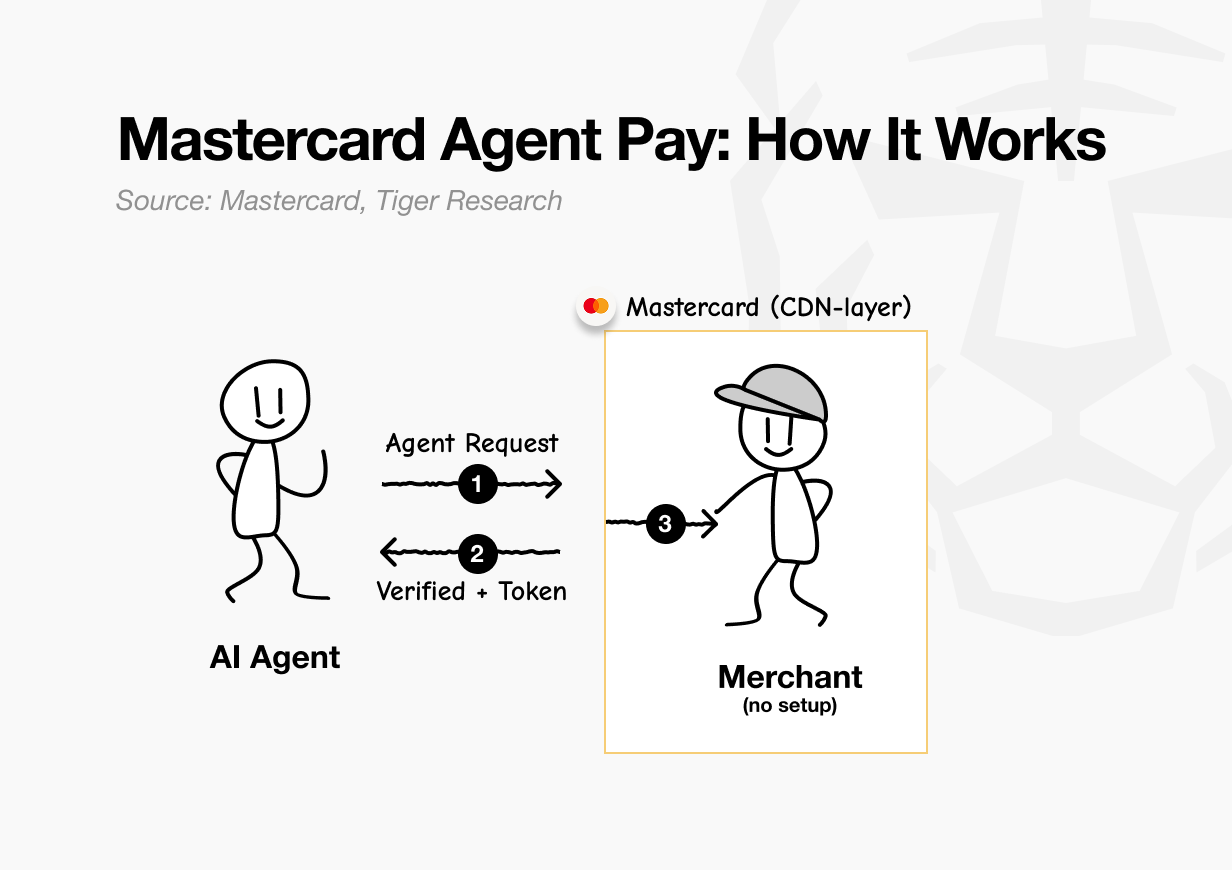

Mastercard’s true battleground is making agent payments work without any action from the merchant. Normally, when a merchant adopts a new payment method, code must be embedded in its website. Mastercard removed this burden.

Through partnership with Cloudflare, Mastercard built a structure that automatically distinguishes “Is this traffic a trusted agent or a malicious bot?” at the front of the merchant’s website, letting only trusted agents through to the merchant. The merchant can accept agent transactions without touching a single line of its own code.

A separate path is also reserved for merchants seeking deeper integration. Those wishing to put their own systems in direct dialogue with agents can connect through major agent protocols such as MCP, A2A, and ACP. The merchant ends up with two choices: do nothing and accept default traffic, or connect a protocol and build a tailored experience. Either path runs through Mastercard.

Core Business

Mastercard’s revenue structure is simple. A fee is generated every time a payment runs through the Mastercard network. As of fiscal year 2025, revenue stood at approximately $32.8 billion with transaction volume of 175.5 billion. Whether an agent or a human pays, the same fee accrues as long as the transaction passes through the Mastercard network.

The issue is that agent payments could bypass the card network entirely. If settlement occurs directly on-chain via stablecoins, there is no place for Mastercard. Agent Pay is the strategy designed to plug that gap.

Mastercard’s chosen approach is to lower the merchant threshold. Adopting a new payment method usually requires a merchant to embed new code in its system. Mastercard removed that burden. Through partnership with Cloudflare, Mastercard built a layer at the front of the merchant site that automatically filters trusted agent traffic.

Merchants accept agent payments without any extra work. The more merchants connected to the network, the more transactions flow through Mastercard.

The revenue path remains unchanged. Every time an agent completes payment through the Mastercard network, a fee is generated. The structure is identical to a person swiping a card. The difference is that agents pay faster and more frequently than humans. As the number of transactions grows, the pace at which fees accumulate accelerates.

For Mastercard, the rise in agent transactions is a natural extension of fee revenue. This is not opening a new business; it is carrying the existing structure forward into the agent era.

Outlook

Mastercard’s outlook in one line: like Visa, it does not pick the winner of the protocol war but instead aims to dominate the way merchants accept agents.

The core of this strategy is enabling merchants to accept agent payments without touching a single line of code. Through partnership with Cloudflare, Mastercard has effectively eliminated the merchant entry barrier.

Visa is moving in the same direction, but Visa is currently dealing with the stablecoin variable at the same time. With the Bridge acquisition and Tempo validator participation, the front line has widened. Mastercard, on the other hand, is still positioned to focus all of its energy on the merchant acceptance layer. Having only one front to defend is, at this point, an advantage.

The question is how long this concentration remains effective. If agent-to-agent payments begin to settle directly on-chain via stablecoins, the volume running through existing payment networks could decline. Visa has already begun to respond to this risk; Mastercard has yet to make a public move.

Stripe, Inc.

Core Technology

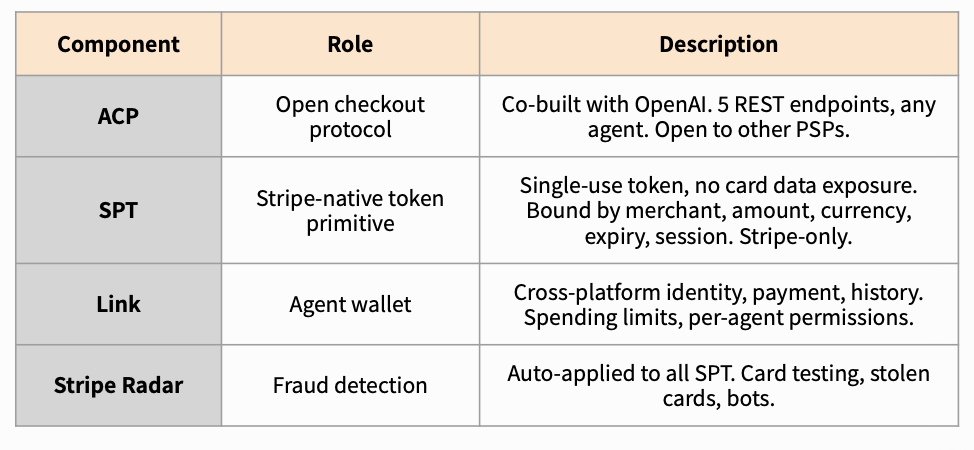

Stripe is the company that, over the past 15 years, became the payment standard for internet commerce through developer-friendly APIs. To hold that same position in the agent era, Stripe chose a strategy of laying new agent-ready payment rails directly on top of its existing infrastructure.

To this end, in September 2025 Stripe co-released ACP as an open standard with OpenAI and, in the same line, announced its own payment primitive, SPT (Shared Payment Token).

Stripe’s agent payment stack is composed of four parts.

What the four components share is that only ACP is an open standard; the rest are all Stripe’s own technology. If ACP is the common language for “how agents and merchants talk to each other,” SPT is Stripe’s proprietary payment token, responsible for how the actual money flows within that conversation.

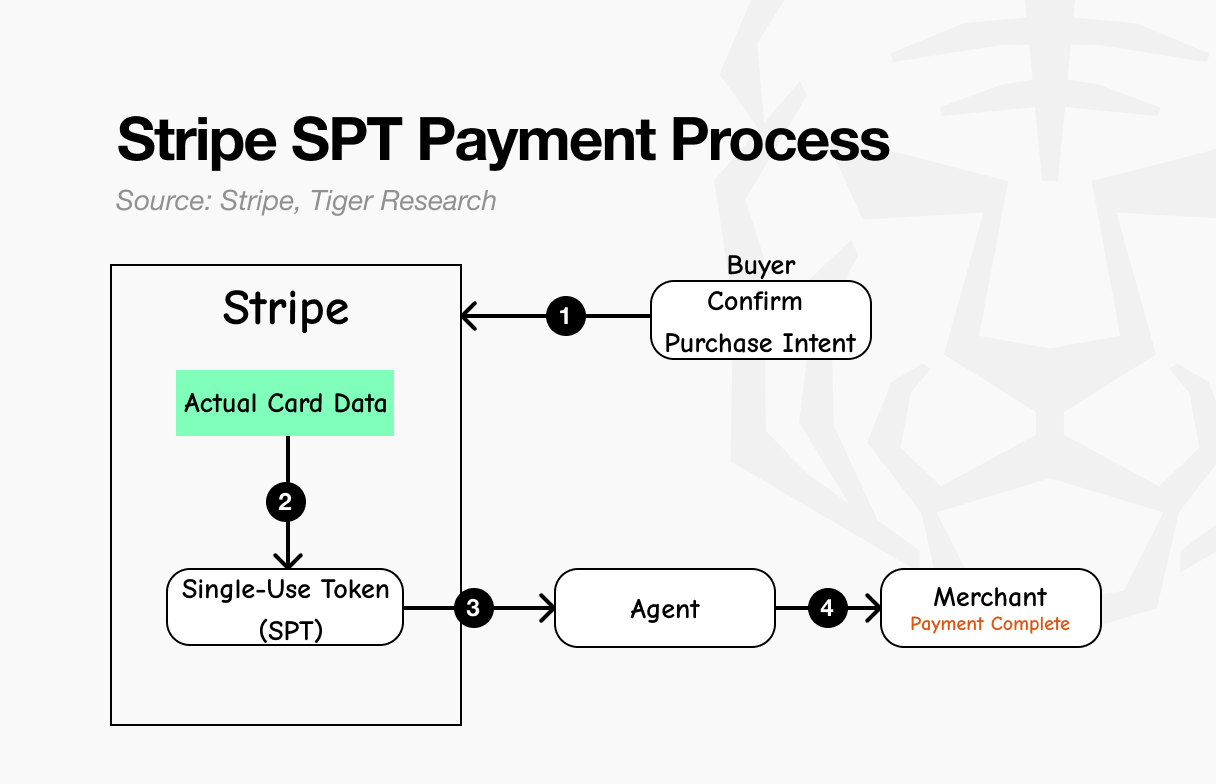

The SPT flow is as follows:

The user says “buy this” in ChatGPT

Stripe issues a single-use payment token (SPT)

The agent passes that token to the merchant

The merchant verifies the token and completes the payment

The card number is never handed directly to the agent. Stripe issues a single-use token (SPT) that can only be used for this transaction, and the agent only passes that token to the merchant, which lowers the risk of card data theft. On top of that, merchants already using Stripe can enable SPT payments with one line of code.

In other words, this is the fastest path for merchants already on Stripe, but merchants on a different PSP need a separate integration.

Core Business

Stripe’s differentiator is that it designed SPT not as a simple payment token but as the hub through which agent payments enter the Stripe ecosystem. The moment a merchant adopts SPT to accept agent payments, the Stripe products attached behind it follow as a bundle. Open one door, and four are connected.

Here is how it works. The moment a merchant adopts SPT to accept agent payments, Stripe’s adjacent services follow as a bundle.

Payment fees: Every agent transaction through SPT carries the same fee structure as before. Agents pay far faster and more frequently than humans. As transaction volume grows, the pace at which per-transaction fees accumulate accelerates. The payment method changes; the fee structure does not.

Visa and Mastercard collect a fee once when payment passes through their network, and that is the end. Stripe uses payment as the entry point to bind merchants to its full financial service stack.

From the merchant’s perspective, plugging in a single agent payment ends up tying the merchant to the entire Stripe ecosystem.

Outlook

Stripe’s outlook in one line: a full-coverage strategy that simultaneously occupies every layer of agent payments.

Stripe has staked positions across every layer of agent payments: the protocol layer (ACP), the payment token layer (SPT), and stablecoins (Tempo). While Visa and Mastercard treat stablecoins as a defensive challenge, Stripe has secured the card-bypass route as an offensive asset.

But the core question is one. Can Stripe move beyond the card network?

Stripe’s revenue structure today still runs on top of the Visa and Mastercard networks. SPT, payment fees, and merchant bundling all operate on the premise of the card network. The structure changes when stablecoins genuinely replace the card network, but no one knows when that point arrives.

It is true that Stripe is now betting in both directions. Yet if Visa and Mastercard run the highway, Stripe is the most successful logistics company on top of it. Being the number-one logistics company is a different game from owning the highway itself.

First, the OpenAI relationship. ACP is co-developed, but ChatGPT instant payment is effectively a Stripe monopoly. If OpenAI builds its own payment rails or aligns with another PSP once enough traffic accumulates, Stripe loses its largest AI channel. The relationship is mutually necessary for now, but no alliance is permanent.

Second, the openness of ACP. Because ACP is an open standard, competing PSPs such as Adyen and Worldpay can produce compatible tokens. Today, Stripe’s market share leads merchants to choose SPT naturally; the moment a competitor releases a token of equivalent quality, the protocol-proposer premium dilutes quickly.

3. Pay-per-call

While Agentic Commerce, examined above, is a market in which humans decide on payment, Pay-per-call is a market in which the agent itself becomes the payer. As long as funds are available in the account, the agent settles autonomously. This is the structure that activates whenever an agent calls another agent’s API, data, or compute.

Take an example. An agent is asked to write a market analysis report.

The user asks the agent to write a market analysis report

The agent queries the OpenAI API and receives a response

To validate the data, it requests information from the Dune and Nansen APIs

The completed report is sent to another agent for review

A single report involves dozens of payments. Unlike Agentic Commerce, however, the amounts settle down to fractions of a cent. In traditional payment systems, fees alone make this structure loss-generating with each transaction. This is why Pay-per-call relies on stablecoins, where fees are minimal.

Pay-per-call currently has three infrastructure standards:

Protocol layer: how agents express payment intent through messages

Settlement layer: which chain settles the payment, and in which asset

Trust layer: who verifies who paid for what, and with what authority

Coinbase Global, Inc. (COIN)

Core Technology

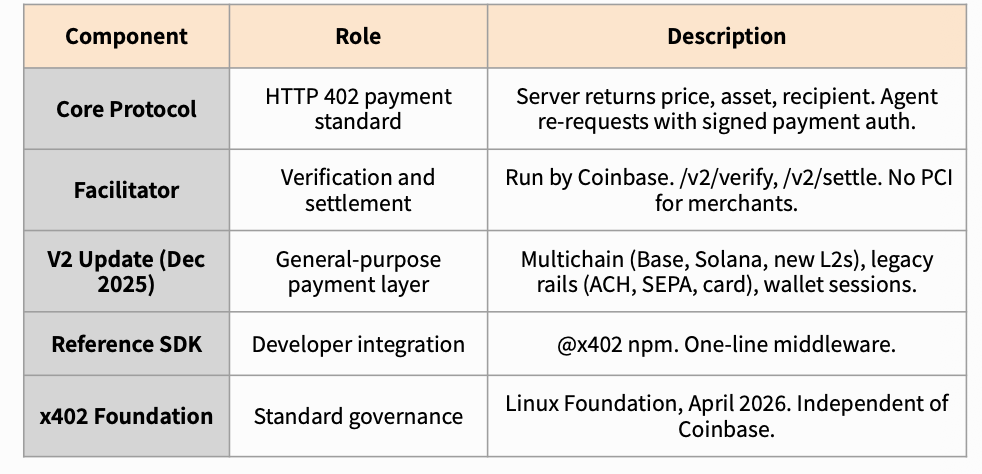

Coinbase is the company that built x402, a standard allowing agents to pay without going through the card network.

In May 2025, Coinbase released the x402 protocol, activating the previously dormant HTTP 402 (Payment Required) status code in practice. In the same year, Coinbase established the x402 Foundation jointly with Cloudflare, expanding x402 into a general-purpose payment layer.

x402 is an open payment protocol composed of five elements.

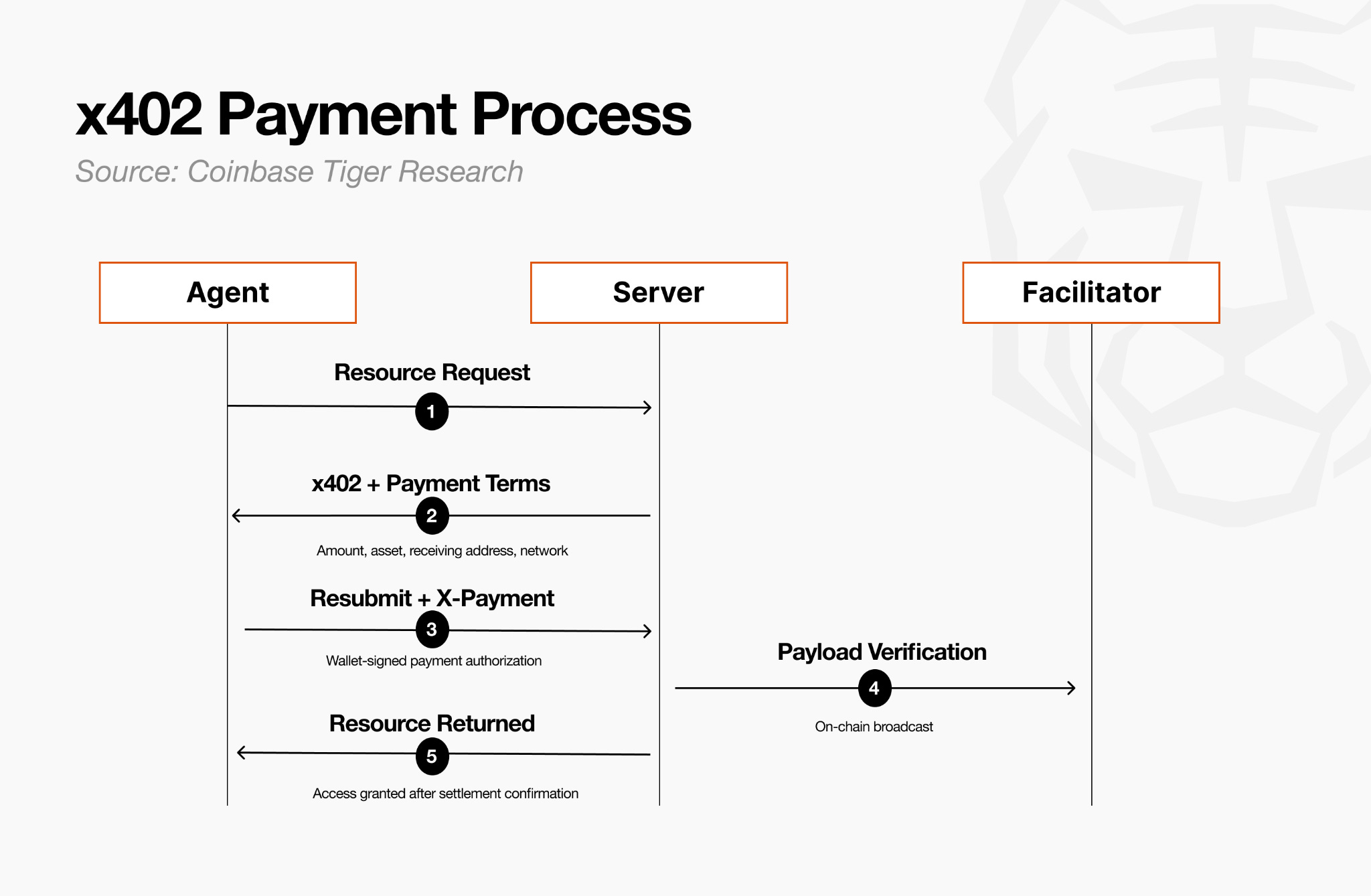

The operating principle of x402 is simple. When an agent calls an API, the server returns an HTTP 402 response containing price, recipient address, asset, and network information. The agent signs the payment with its own wallet, includes it in the header, and re-requests. The server verifies and settles the payment through the Facilitator, then responds with the resource.

Process

The agent requests a resource from the server

The server returns HTTP 402 with payment terms

The agent signs the payment authorization with its own wallet and re-requests, carrying the signature in the X-PAYMENT header

The server passes the payload to the Facilitator (verification and settlement service), which broadcasts it on-chain

After settlement is confirmed, the server returns a 200 response with the resource

The core difference between x402 and existing payment systems is that payment itself functions as authentication. Agents can autonomously discover, pay for, and use new APIs without human intervention.

The V2 update expands x402 from a single-call payment protocol into a general-purpose layer that accommodates multiple authentication, session, and chain types.

The most meaningful change is wallet-based sessions. V1 required payment for every call; V2 introduces session-based payments (Sign-In-With-X) that remain reusable for a set period after a single payment. This change allows workloads that were too slow and too expensive to settle per call, such as LLM calls and multi-call agents, to run on x402 for the first time.

Core Business

Coinbase’s current revenue comes from exchange fees. 2025 annual revenue stood at approximately $7.2 billion, the bulk of it from cryptocurrency trading fees. x402 is unrelated to this revenue structure today. Yet this is precisely why Coinbase open-sourced x402: release the standard for free, then earn revenue on the infrastructure that runs it.

The strategy mirrors Google’s: open-source Android, then capture revenue through Play Store and Google Pay.

The market x402 targets is fundamentally different from Visa, Mastercard, and Stripe. Card payments carry fees of $0.30 plus 2.9% per transaction. Micropayments such as a $0.01 API call, a $0.005 image classification, or $0.50 for one minute of GPU time cannot exist on top of card networks.

The market x402 opens lies in a domain where agents pay other agents, or pay API providers, in units and frequencies where humans cannot press a payment button.

When this distant-future market opens, two revenue streams flow to Coinbase.

Base transaction fees: x402’s default settlement layer is Base, Coinbase’s own Layer 2 chain. Every x402 payment generates a transaction on Base, and Coinbase captures sequencer revenue. As x402 transaction volume grows, Base’s transaction fees and locked assets grow with it. The standard is laid down for free, but the chain on which the standard runs is operated by Coinbase.

CDP infrastructure fees: For every x402 payment, an intermediary (Facilitator) is required to verify “is this payment real?” and actually move the funds. The default Facilitator is operated by Coinbase as part of the Coinbase Developer Platform (CDP). Once developers begin using x402, they naturally pull in adjacent CDP tools: wallet creation, gas sponsoring, and data analytics.

That said, since x402 V2, third-party Facilitators can also be used. The lock-in power of the Facilitator itself is therefore weaker than expected. Coinbase’s real play lies elsewhere. The blockchain optimized for x402 to run cheapest and fastest is Base, built by Coinbase, and even the official whitepaper openly states that x402 works best on Base.

To put it simply: Stripe binds the moment of payment to its system. Coinbase, by contrast, builds the highway through which payments travel and lets travelers on that road naturally stop by Coinbase’s rest areas (CDP tools).

Outlook

Coinbase’s outlook in one line: not a game of beating competitors, but a game of how quickly a market that does not yet exist opens.

This frame matters because x402 does not compete in the same domain as the card network. Credit cards charge $0.30 plus 2.9% per transaction. Micropayments such as a $0.01 API call, $0.005 per image classification, or $0.50 for one minute of GPU cannot exist on top of card networks in the first place.

Even if Visa and Mastercard accept agent payments, that is the domain of agents executing what humans previously did when shopping. The market x402 opens lies one layer below: a domain where agents pay other agents, or pay service providers, in units and frequencies where humans cannot press a payment button.

The issue is that the agent-to-agent transaction market is still small today. For agents to autonomously buy data, buy compute, and buy other agents’ work as part of routine workflow, several conditions must align: LLM inference must become sufficiently cheap, agent frameworks must take hold in production, and data and API providers must support x402.

Whether the market explodes in six months, in two years, or in five, no one knows. Coinbase’s bet succeeds only on a market dependency it does not control. The question is whether Coinbase can hold its position as the company that laid down agent payment infrastructure first, and whether it can endure long enough for the market to open.

Stripe (MPP)

Core Technology

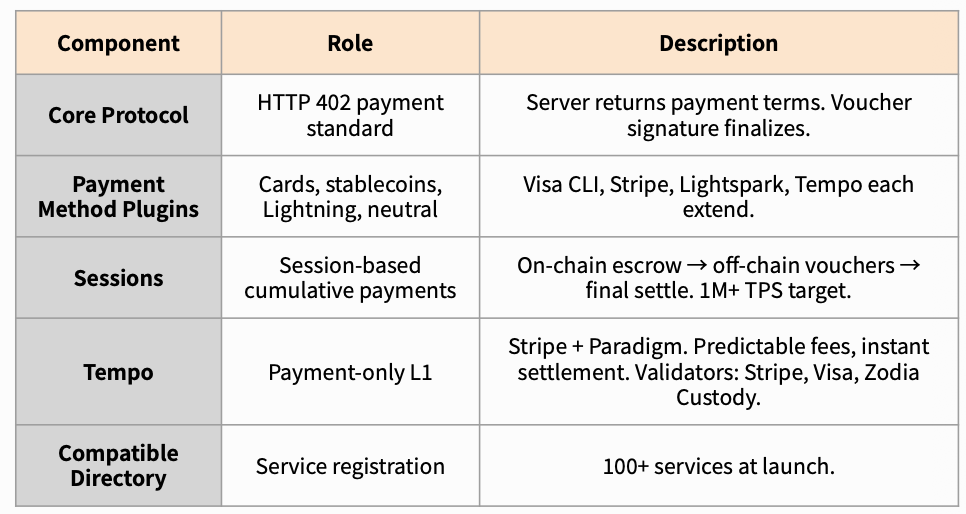

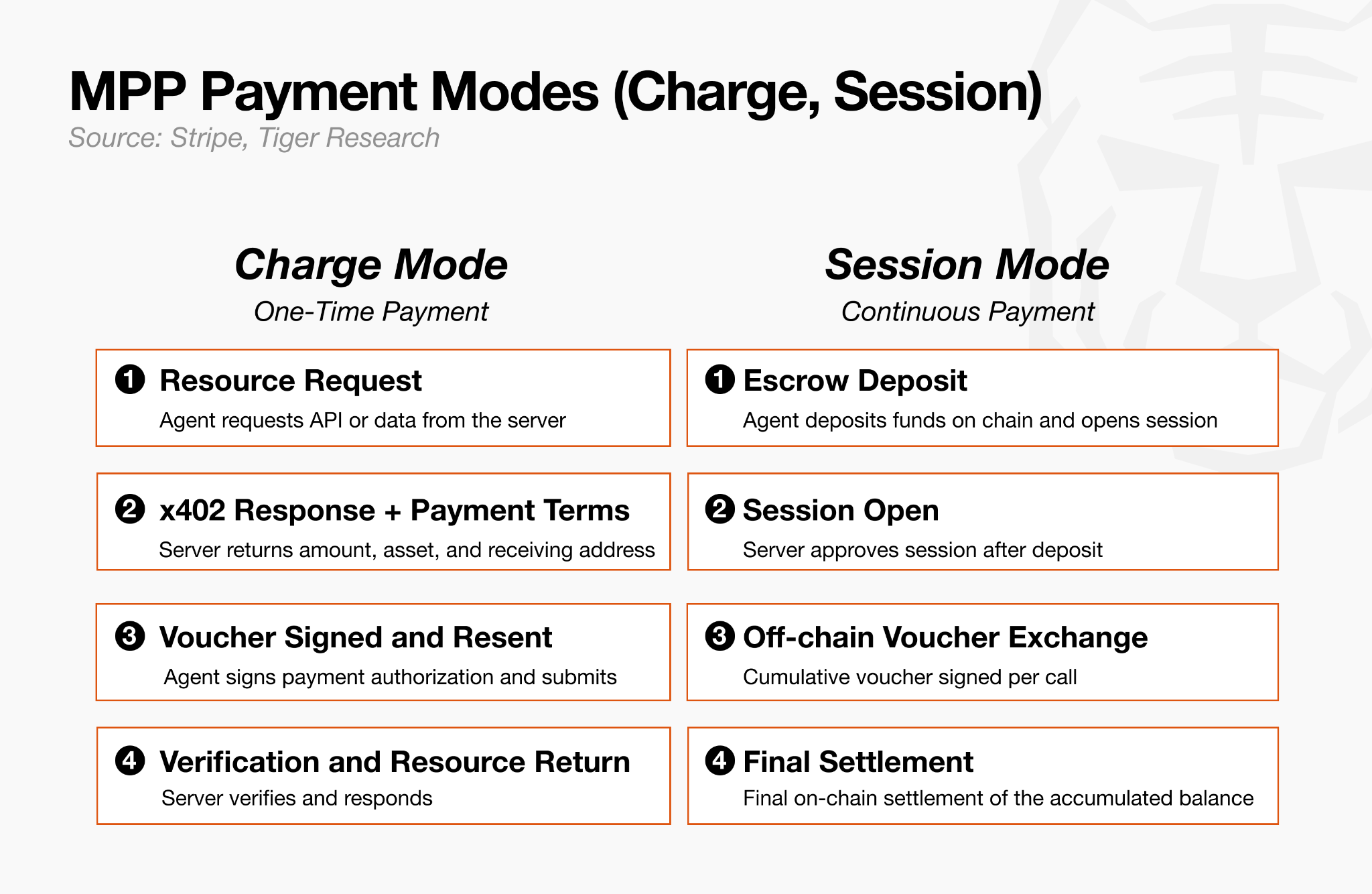

.Stripe is the only payment player to embed its own standard in both Agentic Commerce and Pay-per-call. While ACP and SPT, examined earlier, were card-rail payments through which humans delegate shopping to agents, MPP (Machine Payments Protocol) is a separate protocol designed for the Pay-per-call domain, where agents autonomously pay for other agents’ APIs, data, and compute.

It was released as an open standard on March 18, 2026, in tandem with the mainnet launch of Tempo, jointly developed by Stripe and Paradigm.

Like x402, MPP is an open payment protocol built on top of the HTTP 402 pattern. It differs from x402 on two decisive points.

First, payment-method neutrality. While x402 is structured around stablecoin payments, MPP handles stablecoins and cards or other fiat through the same protocol. Visa extended MPP for card payments, and Stripe supports cards and wallets through its own platform. Different payment methods sit on top of a single protocol like plug-ins.

Second, Sessions support. When an agent opens a session, on-chain escrow is posted once. Vouchers are exchanged off-chain during the session, and a final voucher settles once at the session’s close.

The two modes stand in sharp contrast in the process visualization. A one-time payment (Charge) follows a flow similar to x402, completed in a single on-chain transaction. A continuous payment (Session) records on-chain only twice, at the initial deposit and the final settlement, while the N calls in between are all handled off-chain through vouchers.

This difference is what makes MPP’s throughput target (1M+ transactions per second) possible.

It mirrors gas station payment. One card authorization at the start of fueling, one final charge at the end. Regardless of the fuel volume flowing in between, the transaction count is two. With this structure, MPP targets a scale of 1M+ transactions per second.

Core Business

Stripe sees the agent payment market in two layers. The layer where humans hand shopping to agents is already covered by ACP and SPT. MPP targets the layer below: the domain where agents autonomously pay for other agents’ APIs, data, and compute. It targets the same Pay-per-call market as x402, but its design differs.

While x402 supports stablecoins only, MPP supports cards, stablecoins, and Bitcoin Lightning, building out a diverse set of payment methods. The Tempo initial design partner list reveals the character of this market. Anthropic, OpenAI, Deutsche Bank, and Visa are in. MPP’s own protocol extensions are implemented by Visa (cards), Stripe (cards, wallets), and Lightspark (Lightning).

The reason: AI model calls are what agents will pay for most often. Whether an agent is doing research or writing code, it will continuously invoke OpenAI or Anthropic services. The fact that the companies receiving that money are in from the design phase means the path for transaction volume to accumulate is already laid down.

In this structure, two revenue streams flow to Stripe.

Payment processing fees: When card payments occur on top of MPP, the actual processing is handled by Stripe’s existing system. The protocol stays open as a standard for anyone to use, while the point at which money actually changes hands is pulled into Stripe’s own infrastructure. As agent payments grow, transaction volume passing through Stripe grows with it.

Tempo ecosystem revenue: MPP’s default settlement layer is Tempo. Tempo is a payment-only blockchain built by Stripe with Paradigm, and Stripe participates directly as a validator. As MPP transaction volume grows, Tempo’s transaction fees are distributed to validators, and Stripe holds one of those seats. Open the protocol; secure a validator seat on the chain where the protocol settles, and capture a share of the fees by design.

In the end, Stripe replicated the design from Agentic Commerce in the Pay-per-call domain. ACP and SPT sat on top of card rails; MPP and Tempo sit on top of stablecoin rails. Open the protocol, close the infrastructure. Whichever rail the payment runs on, it ends up passing through Stripe.

Outlook

Stripe’s MPP outlook in one line: the protocol that pulled Visa into a strategy reversal.

Visa was building an independent ecosystem with its own Trusted Agent Protocol and Intelligent Commerce. The approach was, “use our standard.” With the launch of MPP, however, Visa joined as a card-rail extension partner. Cuy Sheffield (Head of Crypto at Visa) commented that Visa “sees MPP as another way of clearly defining how agents and merchants communicate.”

This single sentence signals that Visa shifted from confronting crypto-native standards to embedding card rails within them.

The agent payment market is bifurcating. Regulated human commerce flows on card rails; agent-to-agent transactions (API calls, compute purchases, micropayments) flow on stablecoins. While x402 captured the crypto-native standard for the latter, MPP took the bridge position, integrating both rails into a single protocol. Stripe built a structure in which it operates that bridge.

There are, however, two variables.

First, standard competition with x402. Coinbase’s x402 has already accumulated more than 100 million payments and secured neutral governance through transfer to the Linux Foundation. Stripe also joined the x402 Foundation as a partner, a two-track strategy, but whether the two protocols coexist long-term or converge to one remains uncertain.

Second, Tempo’s adoption pace. MPP’s reference settlement layer is Tempo, but how much agent payment traffic Tempo will actually attract is not yet validated. The trust capital from validators such as Visa and the Standard Chartered subsidiary is significant, but whether developers and service providers will actually choose Tempo is a separate question.

Circle Internet Group, Inc. (CRCL)

Core Technology

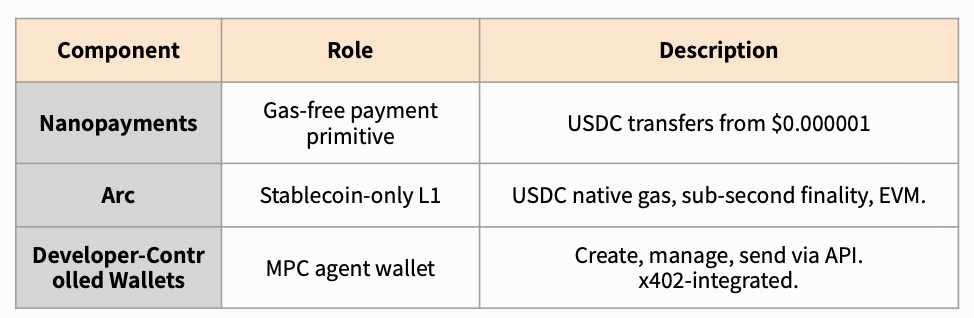

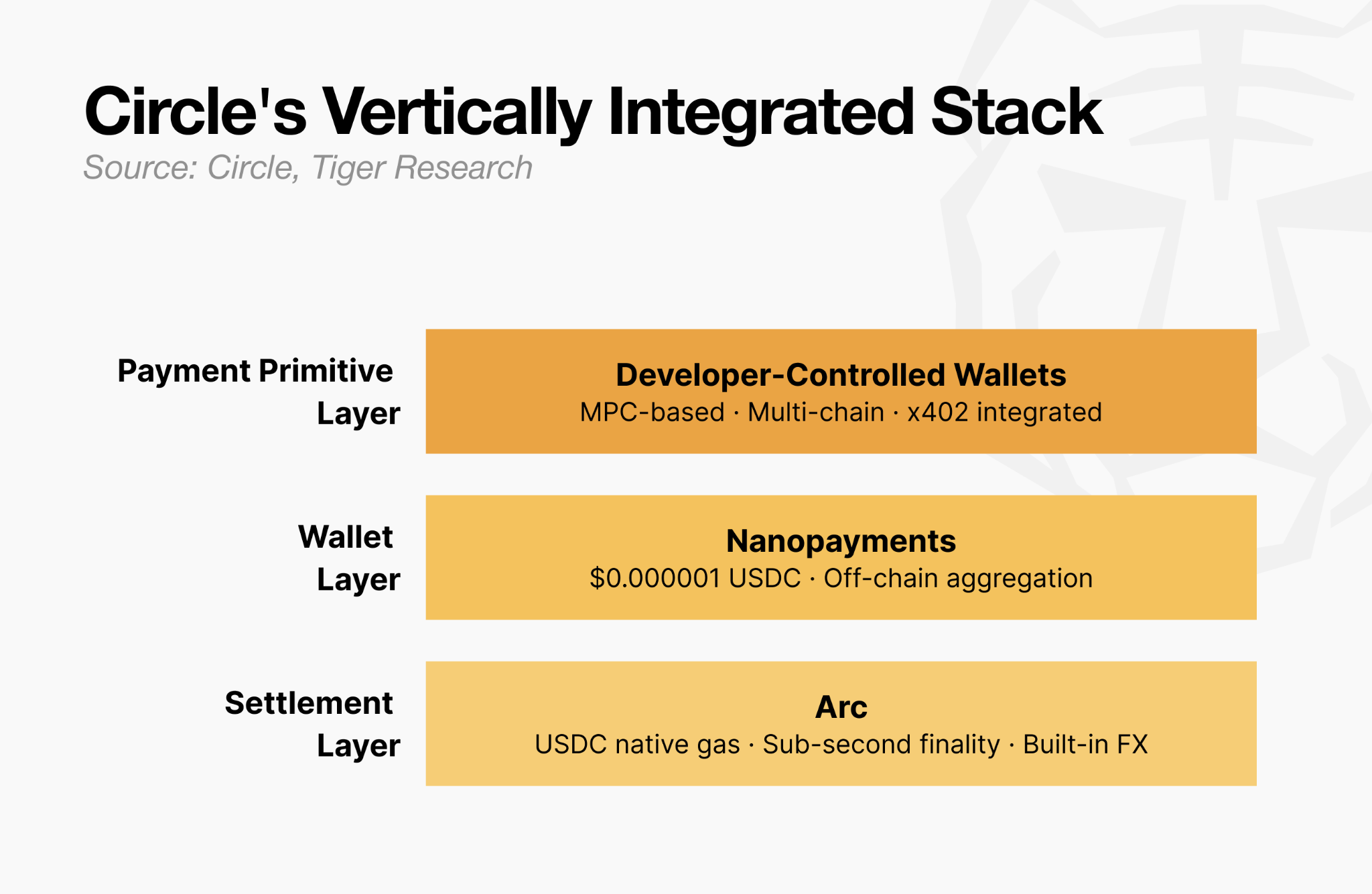

Circle is a company that began with the identity of USDC issuer and has since expanded across stablecoin infrastructure as a whole. In the agent payment era, USDC is no longer simply a payment method. Circle has chosen a full-stack strategy of vertically integrating payment primitives, wallets, and the settlement chain into its own stack.

In September 2025, Circle released Developer-Controlled Wallets and an x402 integration sample. In October 2025, the Arc public testnet went live, followed by the Nanopayments testnet launch in March 2026. Circle’s Pay-per-call stack consists of three components.

The core of Nanopayments is off-chain aggregation and batch settlement. Numerous micropayments are bundled off-chain, then settled on-chain in a single batch, reducing per-transaction gas to effectively zero. Circle absorbs the gas cost at the batch step.

Arc is an L1 designed exclusively for stablecoin finance. The most distinctive design choice is using USDC as native gas. Core specifications include sub-second finality based on the Malachite consensus engine, a built-in FX engine, opt-in privacy, and EVM compatibility.

Developer-Controlled Wallets allow developers to create and manage agent wallets through a single API. As an MPC-based system, it operates without exposing private keys, and handles USDC across multiple chains, including Base, Ethereum, and Arc, as a single unified balance.

When the three technologies are bundled, agents receive a complete payment experience entirely within Circle’s stack: USDC issuance (USDC) → payment rail (Nanopayments) → settlement chain (Arc) → wallet management (Wallets).

OpenMind’s autonomous robot dog, which pays USDC through Nanopayments to charge itself, is the first reference case demonstrating that this stack actually works.

Circle’s revenue structure is simple. 2025 total revenue and reserve income reached $2.7 billion, with more than 95% coming from interest income (Reserve Income) generated on USDC reserves. Wherever USDC is used, reserve interest accrues to Circle. One caveat is worth noting: Circle has agreements with major distribution partners, including Coinbase, that share a fixed portion of this interest. Even so, the broader picture holds: as long as USDC is used as a payment method, Circle’s revenue pool itself grows.

Stripe does not issue the stablecoins running on Tempo, even though it built the chain. The same applies to Coinbase. Whoever wins the chain race, when stablecoin payments grow, Circle’s reserves grow.

This structure compounds as agent payments expand. Each time an agent calls an API, buys data, or purchases compute, USDC circulation grows. As USDC circulation grows, reserves scale with it, and interest income accumulates alongside.

On top of this, Circle is opening a second revenue path through Arc. Once Arc transitions to mainnet, every chain transaction generates gas fees, and the key point is that these fees are paid in USDC. As USDC demand grows, new USDC is issued in proportion, and reserves expand alongside the issuance, lifting interest income with them. While Tempo is structured to use USDC as an external asset, Arc is structured to adopt its own asset as gas, converting chain activity directly into USDC demand.

In the end, Circle’s game operates at a different layer from its competitors. While Stripe and Coinbase try to capture the agent payment flow through chains and protocols, Circle holds the asset that gets used inside that flow.

Outlook

Circle’s outlook in one line: the game of the only full-stack player holding asset issuance rights.

Where Circle decisively differs from competing settlement infrastructure (Tempo, Base) is its monopoly on USDC issuance. Stripe does not issue the stablecoins running on Tempo, even though it built the chain. The USDC running on Tempo is also issued by Circle. Coinbase faces the same situation with Base.

Whichever chain wins the race, when stablecoin payments grow, Circle’s reserves grow. This means a structural advantage at the asset layer.

This advantage carries two variables.

First, USDC market share. The stablecoin market is a two-horse race between USDT and USDC. Tether, PayPal, and bank-issued stablecoins are entering the field. Whether USDC settles in as the default in the agent payment domain, or whether competing stablecoins divide the market, is the first variable.

Second, Arc’s adoption pace. Circle’s move down to the chain layer with Arc is a major bet. But the stablecoin-only chain market is already crowded. Tempo has secured institutional trust capital from Visa and Standard Chartered, and Base has the lead on transaction volume. The question is how much of USDC issuance, Circle’s unique asset, Circle can pull into the Arc ecosystem. The vertical integration only carries weight if USDC usage on Arc grows.

If stablecoin payments become the default in the agent era, Circle is structurally the largest beneficiary. But Circle is also the one that must build that premise itself.

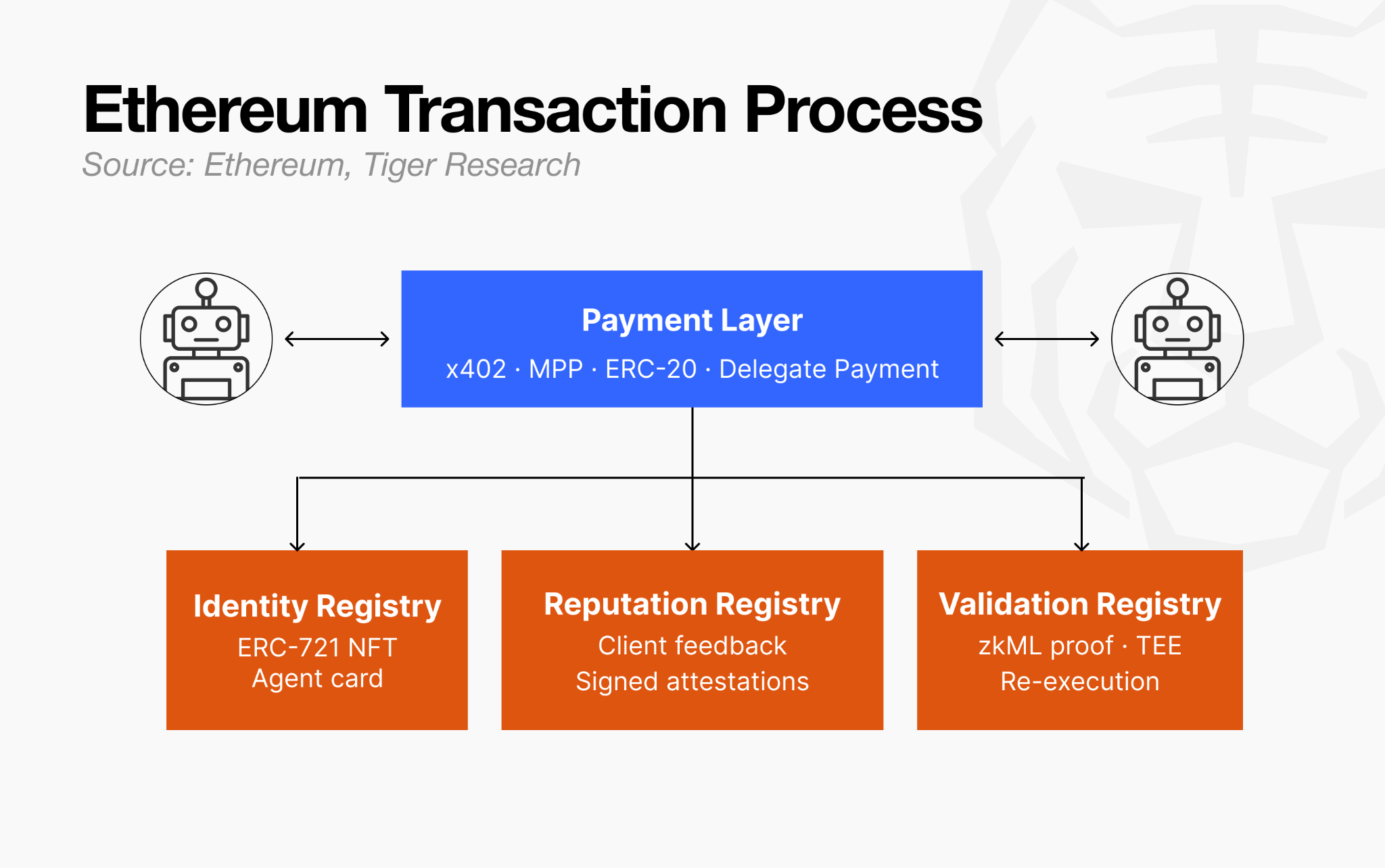

Ethereum Foundation (ETH)

Core Technology

Ethereum has chosen to provide the trust layer for the agent economy as an open standard. While other players process agent payments inside their own fee structures, Ethereum is building a foundation protocol that records who an agent is, what reputation it holds, and whether the result of its work has been verified, in a standardized form on-chain.

The Ethereum Foundation officially submitted ERC-8004 (Trustless Agents) on August 13, 2025, and it was deployed to mainnet on January 29, 2026.

ERC-8004 is designed as a trust extension to the protocol. The list of co-authors signals the character of the standard. Marco De Rossi (MetaMask), Davide Crapis (Ethereum Foundation), Jordan Ellis (Google), and Erik Reppel (Coinbase) participated as co-authors, a lineup that brings AI infrastructure, a crypto exchange, a wallet, and the Foundation to the same table.

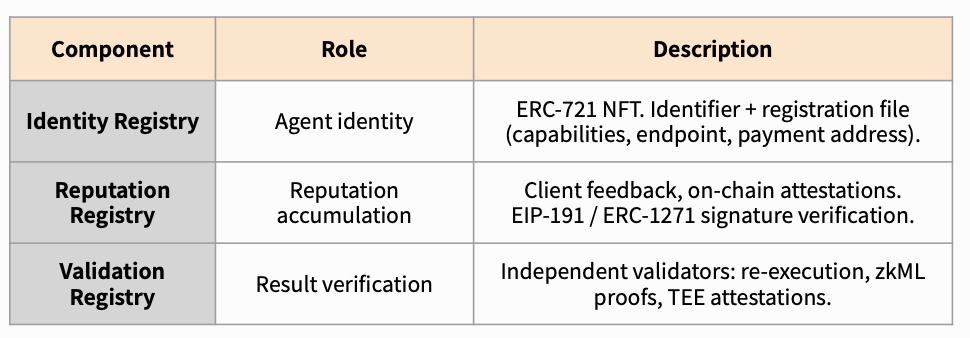

ERC-8004 is composed of three on-chain registries.

When the three registries combine, an agent’s identity → transaction history → verification results all accumulate on-chain. Until now, an agent’s reputation known to Platform A could not be carried over to Platform B. On top of ERC-8004, reputation becomes the agent’s own portable asset.

The trust model is selected in proportion to task risk. For low-risk tasks (e.g., ordering pizza), reputation lookup alone is sufficient. For high-risk tasks (e.g., medical diagnosis), the model requires stake-secured re-execution or even TEE attestation. The same standard applies, but the verification rigor varies depending on the nature of the task, a flexible design.

The important point is that payment itself is not part of ERC-8004. Payment layers such as x402 or ERC-20 transfers attach separately, and payment evidence is appended as feedback to the Reputation Registry. Ethereum, instead of building a payment protocol, provides the common layer of trust and reputation that sits on top of payments.

The flow of an ERC-8004-based agent transaction is as follows:

The agent developer registers the agent with the Identity Registry. An ERC-721 NFT is issued, and the NFT points to a registration file (also known as the agent card) that contains capabilities, endpoint, and payment address

Another agent or user searches for the agent in the Registry. Lookup is possible from any EVM chain

After task execution, result feedback is recorded in the Reputation Registry. Feedback source is verified through EIP-191 or ERC-1271 signature validation

For high-risk tasks, an independent validator in the Validation Registry verifies the result through re-execution, zkML proof, or TEE, and records it on-chain

If a dispute arises, on-chain pointers and hashes cannot be deleted, preserving audit trail integrity

Core Business

ERC-8004 is not a specific company’s revenue structure but an open standard shared by the Ethereum ecosystem as a whole. Instead, the broader the standard’s adoption, the more the entire Ethereum ecosystem benefits. The layer Ethereum operates on is fundamentally different from other payment standard players.

Visa and Mastercard collect fees when payments cross their networks. Stripe and Coinbase open protocols and capture revenue at the infrastructure layer.

Ethereum provides the trust layer that those payment layers must commonly reference. Who an agent is, what reputation it holds, and whether the result of its work has been verified are all recorded on-chain in a standardized form. Whoever wins the payment protocol race, the trust evidence for those transactions runs through ERC-8004.

What the Ethereum ecosystem gains in this structure is one thing. As agents register in the Identity Registry and accumulate reputation, that metadata operates with the highest compatibility in EVM environments. The intent is also stated directly by core players: MetaMask has said that “agent workflow’s home base will be Ethereum and Linea L2.”

The standard originated on Ethereum and runs most naturally on EVM-compatible chains. Non-EVM chains are being extended at the SDK level (MetaMask itself runs a multi-chain SDK), but the fact that the standard’s default environment is EVM does not change.

The broader the standard’s use, the more entrenched the EVM ecosystem’s default-position becomes. In the end, the position the Ethereum Foundation and MetaMask aim for through ERC-8004 is not the game of collecting fees at the payment layer. It is the game of becoming the trust infrastructure that payment layers must commonly reference. The wider the standard spreads, the stronger the entire EVM ecosystem becomes.

Outlook

Ethereum’s outlook in one line: a strategy of dominating the trust layer rather than payment.

The meaning of this choice is clear. Ethereum did not enter the payment protocol race. x402, MPP, and Delegate Payment all deal with the act of payment itself. Ethereum chose to standardize what builds on top of payment: who transacted, and what the outcome was.

In Pay-per-call, the agent-to-agent transaction market, whichever payment protocol wins, the evidence of those transactions is likely to be recorded in the ERC-8004 environment. As long as the standard is widely adopted, whoever wins the payment layer, the Ethereum ecosystem benefits.

There are, however, two variables.

First, the limits of EVM compatibility. ERC-8004 is built on EVM chains. EVM-family chains such as Base, Arc, Tempo, Linea, and BNB Chain can use it directly, but non-EVM camps such as Solana and Bitcoin Lightning require separate adapters. If non-EVM chains build their own identity and reputation standards, the agent economy risks splitting between EVM and non-EVM. The fact that Solana already accounts for 24% of x402 transactions suggests this fragmentation is already happening.

Second, the actual depth of ERC-8004 adoption. The fact that the standard is live on mainnet does not automatically mean agents will actually register in the Identity Registry and accumulate feedback in the Reputation Registry. The question is whether major facilitators and agent platforms move beyond the early prototype level (ChaosChain) and accept ERC-8004 as the default.

Even if the Pay-per-call era arrives, if users gravitate toward wallet-embedded features for the sake of convenience, ERC-8004 may settle into a standard whose practical influence stays limited.

Kite AI (KITE)

Core Technology

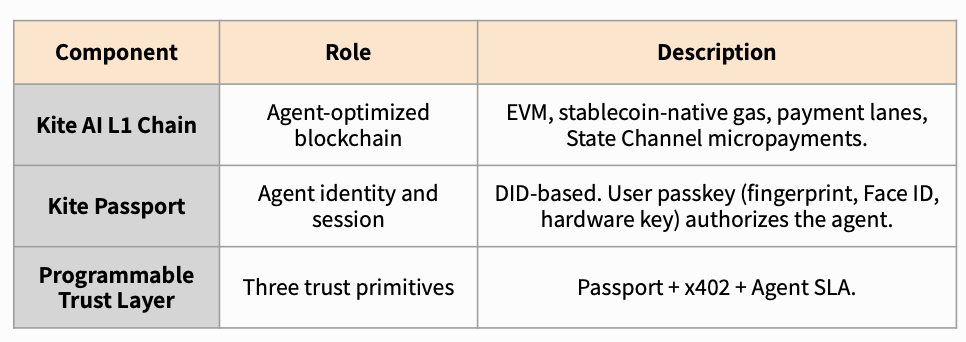

Kite AI is a payment infrastructure designed from the ground up for AI agents. Where Visa, Mastercard, and Stripe transplant existing card networks or PSP infrastructure into agent environments, Kite starts from the opposite direction. It assumes an environment in which agents settle autonomously and bundles chain, identity, session, and reputation into a single stack.

Four elements sit at the core: an EVM-compatible L1 chain (stablecoin-native settlement), Kite Passport (agent identity and delegation management), Programmable Trust Layer (cryptographic spending rules), and an SLA enforcement layer. What structurally distinguishes Kite from other players is that these are not separate products; they operate as one stack.

Protocol compatibility is also in place. Kite supports MCP (Anthropic), A2A and AP2 (Google), x402 (Coinbase), MPP (Stripe and Tempo), and OAuth 2.1. The design is not “choose Kite or your existing stack”; it is “add Kite to your existing stack.”

Kite’s core technology consists of three pieces.

Kite’s core differentiator is its three-layer identity architecture. Rather than applying human key management directly to agents, the design separates authority into three tiers.

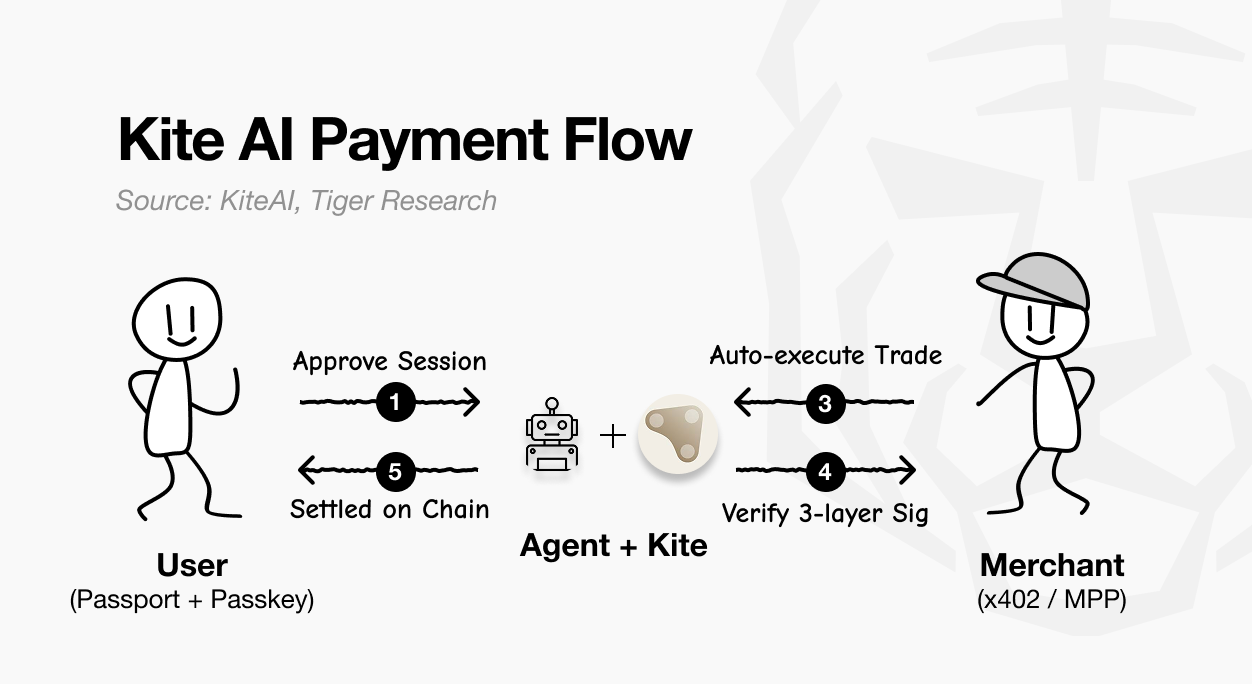

The payment flow has five steps:

User installs Kite Passport, registers passkey (fingerprint, Face ID)

Agent creates Session with budget, duration, permitted actions

User approves with passkey; agent executes autonomously within limits

Each transaction carries a three-layer signature (user root authority, agent delegation token, session signature). All three must pass to finalize

On violation, SLA Oracle submits on-chain attestation; smart contract auto-enforces refunds and penalties

Merchants can participate through two paths: x402 or MPP. x402 returns payment terms via HTTP 402 responses and settles on-chain. MPP, built on Stripe and Tempo, supports both stablecoins and fiat. Either path enables payment from a Kite Passport agent.

Core Business

Kite’s approach starts from a different point than other players. Visa and Mastercard transplant existing card networks into agent environments. Stripe layers an agent layer on top of existing PSP infrastructure. Kite was designed exclusively for agents from the start. It bundles chain, identity, session, and reputation into a single stack and aims to turn the layer where agents exist into infrastructure itself.

The structure here is unique. Fees flowing in as stablecoins are swapped on the open market for Kite tokens and then distributed. The more transactions grow, the more buy-side pressure on the token grows. This is not simple fee revenue; it is a design that converts transaction volume into token value.

Kite’s position in one line: a strategy of being compatible with external payment standards while directly owning the layer on which those standards execute. Kite is also building its own identity and verification standards, including Kite Passport and Agent SLA, but the core value lies in placing the chain through which everything flows under Kite’s own infrastructure.

If standards like Google’s AP2 sit at the upper payment authority layer, Kite aims to claim the lower layer where that authority is actually enforced on-chain. In practice, Kite is designed to be compatible with existing standards such as A2A, MCP, OAuth 2.1, and AP2.

That said, the company is currently at the testnet and early partnership stage. PayPal and Coinbase Ventures backing Kite at the same time signals recognition of the potential, but investment and actual adoption are different questions.

Outlook

Kite’s position is the most ambitious, and at the same time the most uncertain.

The premise of redesigning agent payment infrastructure from scratch is right. Unlike Visa, Mastercard, and Stripe, which operate on top of existing card networks, Kite does not assume the card network. The design, which bundles stablecoin-native settlement, cryptographic identity verification, and auto-enforcing SLAs into a single stack, structurally differentiates Kite.

This means full specialization in Pay-per-call, the agent-to-agent transaction domain.

The challenge is execution. Kite is currently at the testnet and early partnership stage. Ethereum holds standard leadership through ERC-8004, while Stripe, Coinbase, and Google already have existing infrastructure and developer ecosystems in place. Securing share with a proprietary L1 in this environment is a different game.

PayPal and Coinbase Ventures investing at the same time signals that both camps recognize the potential, but investment and adoption are different things. If Pay-per-call adoption actually rises, Kite could build an overwhelming ecosystem. But how long that takes, no one knows.

4. Agentic Commerce first; Pay-per-call follows

Agentic Commerce is ultimately a model that will succeed. The question is not “will this market open?” but “who will capture it?”

The reason is that Agentic Commerce is not an entirely new structure. Within the existing system, users, card issuers, and merchants each need only a single update. This is less about technical superiority and more about how quickly the market onboards.

In practice, the stakeholders have already aligned. Walmart, Etsy, and Shopify, among other e-commerce merchants, have joined as Google and OpenAI partners, and payment networks and enterprise companies have followed.

Pay-per-call is a different story. The possibility that this market will open cannot be denied, but whether demand exists right now is uncertain. The core reason lies in the current API payment structure. API providers such as OpenAI, Anthropic, and AWS already operate on monthly subscription or usage-based postpaid billing.

When an agent calls an API, if the platform auto-links the card and bills monthly, the result is functionally identical to existing SaaS billing structures.

From the corporate finance team’s perspective, there is no incentive to change a structure that is predictable and familiar. This is why the demand that Pay-per-call protocols such as x402 or MPP genuinely require has not yet been validated.

For Pay-per-call to become a meaningful market, conditions must align. Agents must autonomously procure external resources from an unspecified set of providers, without prior contracts, and those transactions must occur at dozens per second, with per-transaction values below $0.001.

Only when speeds and unit prices that the existing subscription structure cannot handle emerge does the proposition “Pay-per-call is better than credit cards” hold.

In the end, this market’s expansion follows a sequence. Agentic Commerce grows first; only after trust and autonomy in agents have accumulated through that process does demand for the Pay-per-call market get validated.

The winners of Agentic Commerce are already competing. The winners of Pay-per-call will be decided at the moment the market opens.

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.