This report, published by Tiger Research, provides a consolidated overview of Web3 developments across major Asian web3 markets in Q2 2025.

TL;DR

Regulation & Government: 1) Hong Kong moves to solidify its role as a digital finance hub with stablecoin legislation set for August. 2) Singapore enforces a strict licensing regime by banning overseas operations of unlicensed firms. 3) Thailand introduces G-Tokens, becoming the first to launch a government-issued digital bond initiative.

Enterprise Activity: 1) In Japan, a wave of Bitcoin treasury strategies among listed firms drives a surge in institutional investment. 2) Chinese companies adopt a pragmatic approach—bypassing domestic restrictions through Hong Kong licenses and accumulating Bitcoin.

Policy Shifts: 1) In South Korea, the emergence of KRW-backed stablecoins as a post-election agenda is offset by continued regulatory fragmentation. 2) Vietnam makes a historic shift from prohibition to full legalization. 3) The Philippines pursues a dual-track strategy, combining strict regulation with a sandbox framework.

1. Asia Web3 Market in Q2: Regulatory Stabilization and Rising Enterprise Investment

While the Web3 market’s center of gravity has clearly shifted toward the U.S., developments in key Asian markets remain critical to track. Asia not only accounts for the world’s largest base of crypto users, but also continues to serve as a core hub for blockchain innovation.

For this reason, Tiger Research has maintained a quarterly review of major Web3 trends across Asia. In Q1 2025, regulators across the region laid foundational groundwork—introducing new legislation, issuing licenses, and launching regulatory sandboxes. Efforts to strengthen cross-border cooperation also began to take shape.

In Q2, this regulatory foundation enabled meaningful business activity and accelerated capital deployment. The policies introduced in Q1 were tested in the market, prompting refinements and more practical implementations.

Institutional and enterprise participation increased significantly. This report analyzes these Q2 developments on a country-by-country basis, and assesses how national policy shifts are shaping the broader global Web3 ecosystem.

2. Key Developments in Major Asian Markets

2.1. South Korea: At the Intersection of Political Transition and Regulatory Realignment

In Q2, cryptocurrency policy emerged as a prominent issue in South Korea ahead of the June presidential election. Candidates actively shared Web3-related pledges, and following the victory of Lee Jae-myung, the market anticipated significant policy shifts.

One of the central topics was the introduction of a KRW-pegged stablecoin. Related stocks, including Kakao Pay, saw a notable uptick, and traditional financial institutions began filing Web3-related trademarks in anticipation of market entry.

However, conflicts emerged during the policy formulation process—most notably between the Bank of Korea and the Financial Services Commission (FSC) over jurisdictional authority. The central bank argued for early involvement in the approval process, positioning stablecoins as part of a broader digital currency ecosystem alongside CBDCs.

In July, the Democratic Party announced a delay in the introduction of its Digital Asset Innovation Act by one to two months. The absence of a clear lead policymaker appears to be a key bottleneck, with inter-agency negotiations remaining fragmented. As a result, while KRW stablecoins have become a focal point, concrete regulatory guidance is still lacking.

That said, incremental institutional progress continued. In June, new guidelines permitted non-profits and exchanges to sell donated crypto assets, enabling immediate liquidation. The rules also required sales to be conducted in a way that minimizes market impact.

Interest in the Korean market remained strong throughout Q2. Global exchanges signaled continued commitment: Crypto.com Korea completed Travel Rule integration with Upbit and Bithumb, and KuCoin mentioned plans to re-enter the market after aligning with regulatory standards.

Offline activity also picked up noticeably. Compared to last year, the number of meet-up events rose sharply, and an increasing number of international projects visited Korea even outside major conference windows. However, the rise of promotion-heavy events—focused more on giveaways than engagement—has drawn fatigue among local builders.

2.2. Japan: Institutional and Corporate Adoption Drives Bitcoin Strategy Expansion

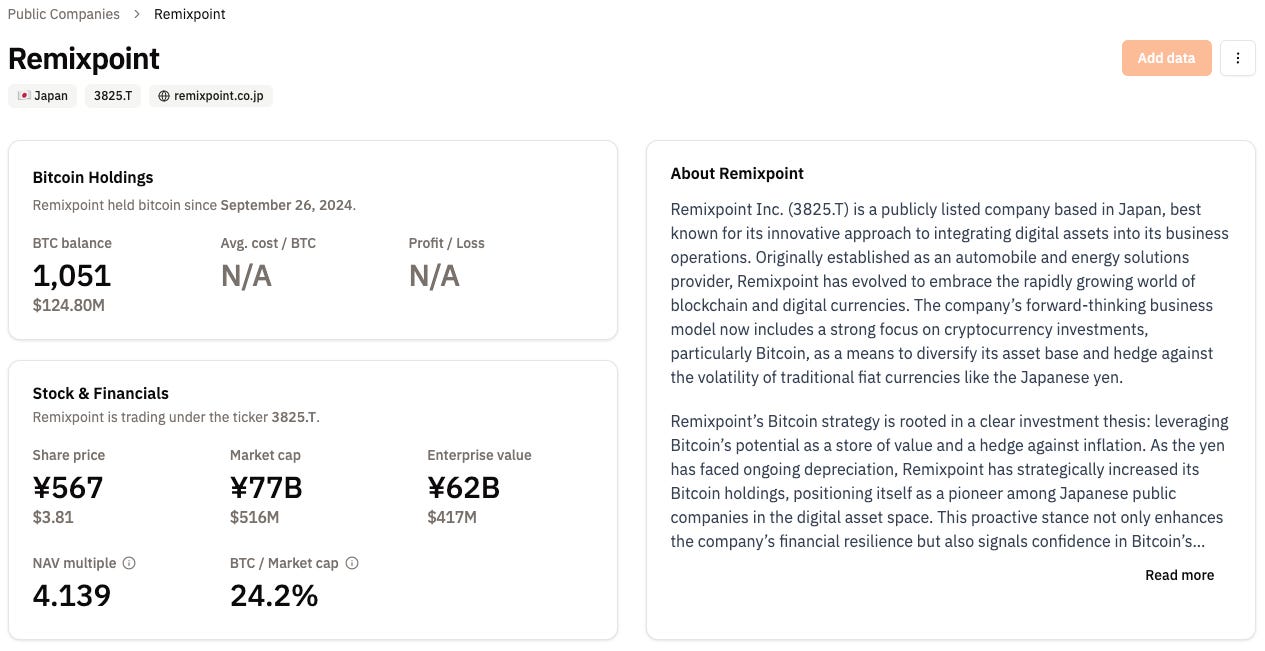

In Q2, Japan saw a wave of Bitcoin adoption among publicly listed companies. The trend was largely catalyzed by MetaPlanet, which achieved approximately a 39x return on its initial Bitcoin purchase made in April 2024. Its performance served as a benchmark, prompting firms such as Remixpoint and others to follow suit with their own BTC allocations.

At the same time, efforts to build out stablecoin and payment infrastructure gained momentum. Sumitomo Mitsui Financial Group began preparing for a stablecoin launch in collaboration with Ava Labs and Fireblocks. Separately, Mercoin—the crypto subsidiary of Mercari—started supporting XRP trading, significantly expanding crypto accessibility on a platform with over 20 million monthly active users.

Alongside private-sector initiatives, regulatory discussions continued to evolve. The Financial Services Agency (FSA) introduced a new classification system, dividing crypto assets into two types: Type 1, which includes tokens used for fundraising or business operations, and Type 2, referring to general-purpose crypto assets. However, most of these regulatory updates remain at the discussion stage, with limited concrete changes to date.

Retail investor participation remains subdued. Japanese retail investors have traditionally favored conservative strategies and remain cautious toward crypto assets. As a result, even with new market entrants, immediate retail capital inflows are unlikely.

This stands in contrast to markets like South Korea, where active retail participation contributes directly to early-stage liquidity for new projects. In Japan, the institution-led investment model offers greater stability, but may limit near-term growth momentum.

2.3. Hong Kong: Regulated Stablecoins and Expansion of Digital Financial Services

In Q2, Hong Kong advanced its stablecoin regulatory framework, reinforcing its position as Asia’s leading digital finance hub. The Hong Kong Monetary Authority (HKMA) announced that new legislation governing stablecoins will take effect on August 1. A licensing regime for stablecoin issuers is expected to follow by year-end.

As a result, the first regulated stablecoins are anticipated to launch in Q4, potentially as early as this summer. Companies that previously participated in HKMA’s regulatory sandbox are expected to be among the first movers, making their progress worth monitoring.

The scope of digital financial services also expanded significantly. The Securities and Futures Commission (SFC) announced plans to permit virtual asset derivatives trading for professional investors. In parallel, licensed exchanges and funds received approval to offer staking services.

These developments reflect a clear regulatory intent to establish a more comprehensive and institution-friendly digital asset ecosystem in Hong Kong.

2.4. Singapore: Regulatory Tightening Between Control and Protection

In Q2, Singapore took a markedly restrictive turn in its crypto regulation. Most notably, the Monetary Authority of Singapore (MAS) implemented a full ban on overseas operations by unlicensed digital asset firms—signaling a firm stance against regulatory arbitrage.

The new rule applies to all Singapore-based entities offering digital asset services to users globally, effectively mandating formal licensing. The environment has shifted: simple business registration is no longer sufficient to operate.

This change places growing pressure on local Web3 firms. Companies now face a binary choice—either build fully compliant, operationally substantive entities or consider relocating to more permissive jurisdictions. While framed as a move to enhance market integrity and consumer protection, the impact is undeniably constraining for early-stage and cross-border projects.

2.5. China: Digital Yuan Internationalization and Corporate Web3 Strategies

In Q2, China advanced the internationalization of the digital yuan, with Shanghai at the center of this effort. The People’s Bank of China announced plans to establish an international operations center in Shanghai to support cross-border adoption of the digital currency.

However, a gap remains between official policy and on-the-ground practices. Despite the nationwide ban on cryptocurrencies, some local governments—such as in Jiangsu Province—have reportedly liquidated confiscated digital assets to offset fiscal shortfalls. This indicates a pragmatic approach that diverges from Beijing’s formal stance.

Chinese enterprises are exhibiting a similar pragmatism. Firms such as logistics group AdanTex have begun accumulating Bitcoin, following the lead of Japanese corporates. Others are leveraging Hong Kong’s licensing regime to bypass mainland restrictions and gain exposure to the global Web3 market—effectively navigating regulatory boundaries to participate in the digital asset economy.

Interest in yuan-pegged stablecoins has also grown, particularly in the latter half of the quarter. Rising concerns over the dominance of USD-based stablecoins and the weakening of the yuan have fueled these discussions.

On June 18, PBOC Governor Pan Gongsheng publicly outlined a vision for a multipolar global currency system, hinting at openness to stablecoin issuance. In July, Shanghai’s State-owned Assets Supervision and Administration Commission (SASAC) initiated discussions around the development of yuan-linked stablecoins.

2.6. Vietnam: Legalization of Crypto and Tightening of Digital Controls

Vietnam enacted a major policy shift in Q2 by officially legalizing cryptocurrency. On June 14, the National Assembly passed the Law on Digital Technology Industry, which recognizes digital assets and outlines incentives for sectors such as AI, semiconductors, and digital infrastructure.

This marks a historic reversal from Vietnam’s previous ban on cryptocurrencies, positioning the country as a potential catalyst for broader adoption across Southeast Asia. Given Vietnam’s formerly restrictive stance, the move signals a significant realignment in regional crypto policy.

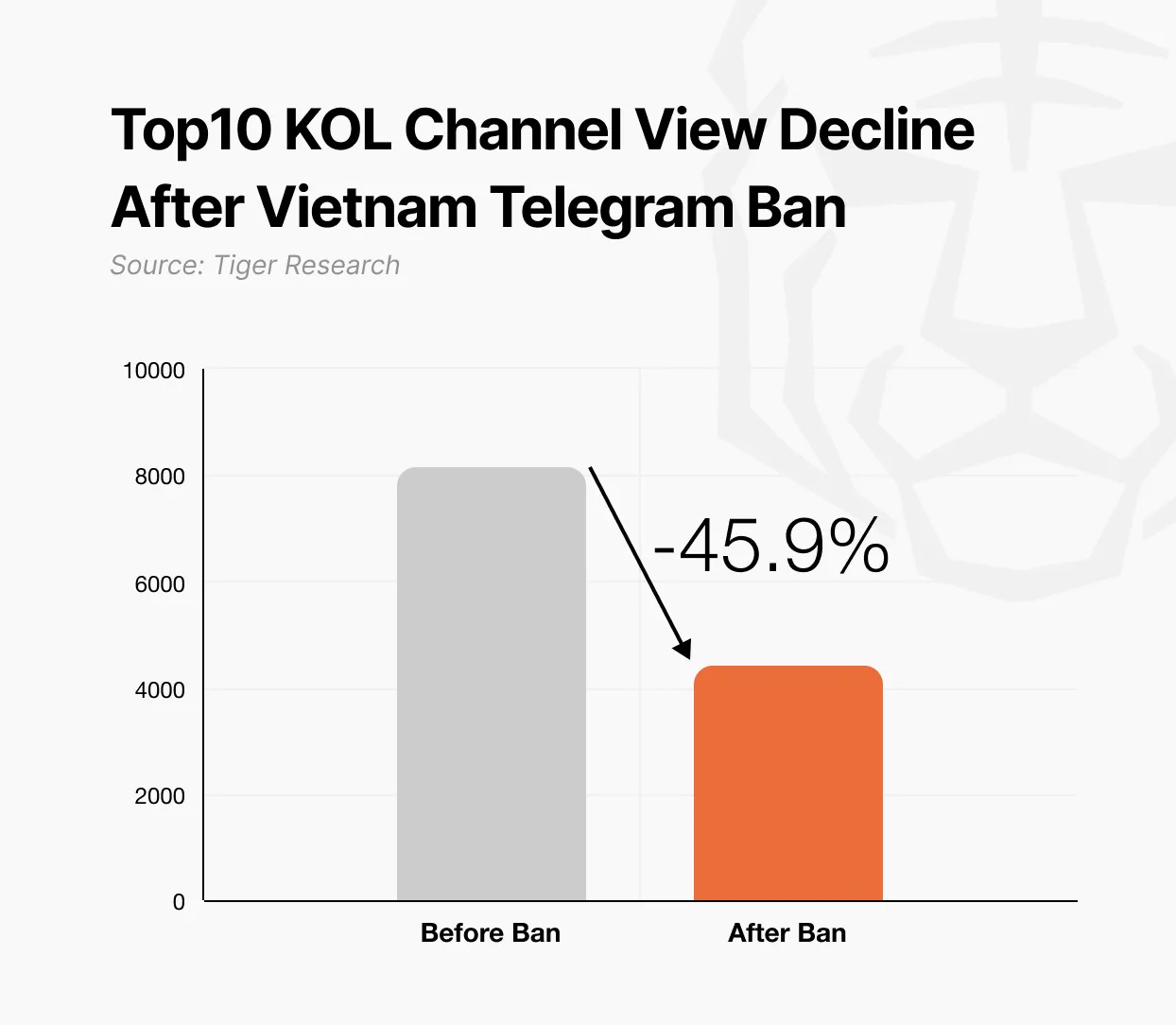

At the same time, the government tightened control over digital platforms. Authorities ordered telecom providers to block access to Telegram, citing its alleged use in scams, drug trafficking, and terrorism. A police report found that 68% of the app’s 9,600 active channels were linked to illegal activities.

This dual approach—legalizing crypto while cracking down on digital misuse—reflects Vietnam’s intent to permit innovation within tightly monitored boundaries. While digital assets are now legally recognized, their use in illicit activities is being met with heightened enforcement.

2.7. Thailand: State-Led Digital Asset Innovation

In Q2, Thailand advanced state-led initiatives in the digital asset sector. The Securities and Exchange Commission (SEC) announced it is reviewing a proposal to allow exchanges to list their own utility tokens—a shift from previous strict listing rules, potentially increasing operational flexibility for platforms.

More notably, the government unveiled plans to issue its own digital bond. On July 25, Thailand will launch “G-Tokens” via an approved ICO portal, with a total issuance size of USD 150 million. These tokens will not be usable for payments or speculative trading.

This initiative represents a rare example of direct government participation in digital asset issuance. Globally, Thailand’s approach stands out as an early model of public-sector-led digital innovation in tokenized finance.

2.8. Philippines: Dual Approach of Strict Oversight and Innovation Sandboxes

In Q2, the Philippines advanced a two-track strategy combining tighter regulation with support for innovation in the crypto sector. The government introduced stricter controls on token listings, with oversight divided between the central bank and the Securities and Exchange Commission (SEC). Requirements for VASP registration and anti-money laundering compliance were significantly expanded.

A particularly notable move was the introduction of influencer regulations. Content creators promoting crypto assets are now required to register with authorities. Violations may result in penalties of up to five years in prison, marking one of the region’s most stringent enforcement regimes.

Alongside these measures, the government also launched a framework to foster innovation. The SEC began accepting applications for “StratBox,” a sandbox program designed to support crypto service providers under a controlled regulatory environment.

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn't harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research's reports, it is mandatory to 1) clearly state 'Tiger Research' as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.