This report was written by Tiger Research, analyzing the impact of DTSP regulatory changes on Singapore's Web3 industry.

TL;DR

Singapore established itself as "Asia's Delaware" by attracting Web3 companies through flexible regulations. Shell companies proliferated and high-profile firms like Terraform Labs and 3AC collapsed. These events exposed regulatory gaps.

MAS will implement the DTSP framework in 2025. All Singapore-based companies providing digital asset services must obtain licenses. Corporate registration alone will not enable digital asset operations.

Singapore maintains support for innovation but tightens regulatory oversight. The government now demands accountability and compliance. Singapore-based Web3 companies must develop operational capabilities or evaluate alternative jurisdictions.

1. Singapore's Changing Regulatory Environment

Global companies have called Singapore "Asia's Delaware" for years. Clear regulations, low corporate taxes, and fast-track incorporation drew businesses worldwide.

This foundation worked equally well for the Web3 industry. Singapore's business-friendly environment naturally made it an appealing destination for Web3 companies too. MAS recognized crypto's growth potential relatively early. MAS actively built regulatory frameworks. It created space for Web3 companies to operate within established systems.

MAS enacted the Payment Services Act (PSA). This brought digital asset services into a clear regulatory system. MAS introduced regulatory sandboxes. These allowed companies to experiment with new business models under specific conditions. These regulatory measures helped reduce early market uncertainty. They established Singapore as Asia's Web3 industry hub.

However, Singapore's policy direction shows signs of change recently. MAS moves away from its flexible approach. MAS now tightens supervisory standards and revamps regulatory frameworks. The numbers show this shift clearly. Over 500 license applications were submitted since 2021. Approval rates stayed below 10%. This suggests MAS significantly raised approval standards. It also shows the authority adopted more selective risk management under limited supervisory capacity.

This report examines how these regulatory shifts are reshaping Singapore's Web3 landscape.

2. DTSP Framework: Why Now, and What Has Changed?

2.1. Background to Regulatory Tightening

Singapore spotted crypto's potential from the industry's early days. It actively attracted companies using flexible regulations and sandboxes. This approach made many Web3 firms see Singapore as an attractive Asian base.

However, the existing system's limitations gradually emerged over time. One key issue was the "shell company" model. This involved companies registering entities in Singapore while conducting actual operations overseas, exploiting gaps in the Payment Services Act (PSA) coverage. The PSA only required licenses for companies serving Singapore users at the time. Some firms avoided this condition. They operated based on Singapore's institutional credibility while avoiding actual oversight.

MAS determined this structure made effective Anti-Money Laundering (AML) and Counter-Terrorism Financing (CFT) enforcement difficult. Companies had entities in Singapore but conducted operations and fund flows entirely overseas. This made supervisory control challenging for authorities. The Financial Action Task Force (FATF) flagged this as an "Offshore VASP" structure and warned that mismatches between registration and operation locations created global regulatory gaps.

The 2022 collapse of Terraform Labs and Three Arrows Capital (3AC) turned these concerns into reality. Both companies registered entities in Singapore but conducted actual operations offshore. MAS could not exercise meaningful oversight or enforcement powers over them. This resulted in billions of dollars in losses. Singapore's regulatory credibility also suffered damage. MAS decided it could no longer tolerate such regulatory gaps.

2.2. Key Changes and Implications of DTSP Regulations

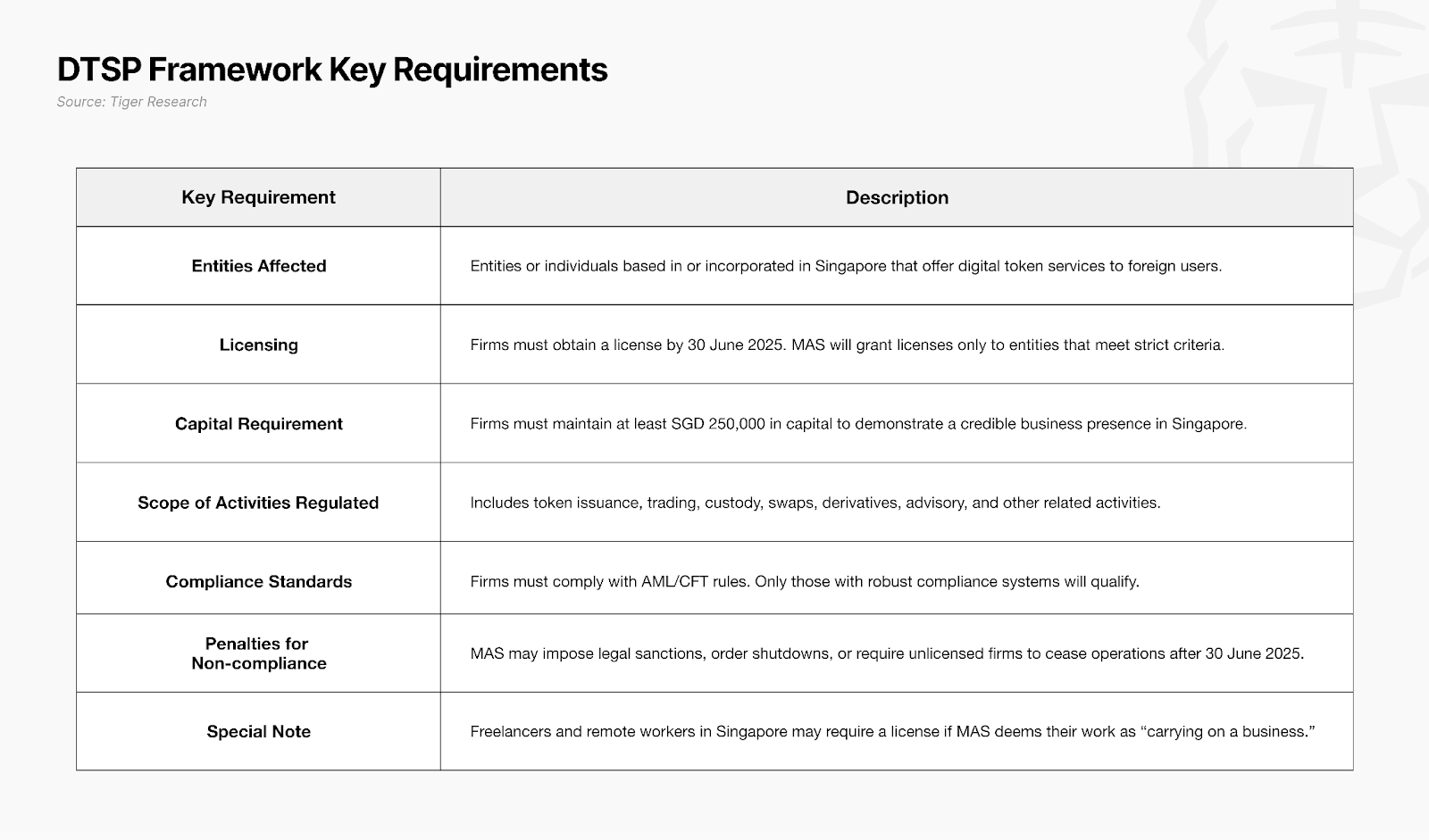

The Monetary Authority of Singapore (MAS) will implement new Digital Token Service Provider (DTSP) regulations from June 30, 2025. These regulations operate under Part 9 of the Financial Services and Markets Act (FSMA 2022). FSMA consolidates MAS's previously scattered supervisory powers and creates comprehensive financial legislation. This addresses new financial environments including digital assets.

These new regulations aim to address the PSA's limitations. The PSA only required licenses for companies serving Singapore users. Some firms exploited this gap. They registered entities in Singapore but operated offshore to circumvent regulations.

The DTSP framework targets this structural avoidance directly. All digital asset companies operating from Singapore or using Singapore as their operational base must obtain licenses. This applies regardless of user location. Even companies serving only overseas customers must comply if they base operations in Singapore.

Under this principle, MAS clarified it will not grant licenses to companies without substantial business foundations. Companies that fail to meet requirements by June 30, 2025, must cease operations immediately. This represents more than temporary enforcement. It signals Singapore's long-term policy shift toward becoming a trust-centered digital finance hub.

3. Redefining Regulatory Scope Under DTSP

The DTSP framework demands clearer regulatory compliance from digital token service operators in Singapore. MAS requires license acquisition for any business deemed Singapore-based. This applies regardless of user location or organizational structure. Various previously unregulated business types now fall under regulatory oversight.

Key examples include companies that establish Singapore entities but operate entirely overseas. It also covers businesses with offshore entities but core functions in Singapore. These functions include development, management, and marketing. Even Singapore residents contributing to projects on a continuous commercial basis may fall under DTSP requirements. This applies regardless of formal organizational affiliation. MAS applies clear criteria: does the activity occur in Singapore? Does it have commercial characteristics?

These changes extend beyond expanded regulatory scope. MAS demands substantial operational capabilities from operators. These include Anti-Money Laundering (AML) and Counter-Terrorism Financing (CFT). Operators must also manage technology risks and maintain internal controls. Operators must now determine whether their Singapore activities fall under regulations. They must assess whether they can sustain business under the regulatory framework.

DTSP implementation shows Singapore's transformation. The jurisdiction no longer serves as a space for leveraging regulatory reputation alone. Singapore now demands responsibility and discipline above certain thresholds. Companies and individuals seeking to continue crypto operations in Singapore must understand their activities clearly. They must recognize regulatory implications under DTSP standards. They must establish appropriate organizational structures where necessary. They must build proper operational systems.

4. Closing Thoughts

Singapore's DTSP regulations show how regulators have shifted their crypto approach. MAS previously maintained flexible policies. This helped new technologies and business models enter markets quickly. However, this regulatory overhaul extends beyond simple tightening. It imposes clear responsibilities on entities using Singapore as their actual business base. The framework shifts from an open experimental space. It now supports only operators who meet regulatory standards.

This change means operators must fundamentally restructure their Singapore operations. Companies unable to meet new regulatory standards may face unavoidable decisions. They may need to adjust operational frameworks or relocate their business bases. Hong Kong, Abu Dhabi, and Dubai each develop crypto regulatory frameworks differently. Some companies may consider these regions as alternative bases.

However, these jurisdictions also require proper licensing for services targeting domestic users or operated from their territory. They apply regulations across multiple areas including capital requirements, anti-money laundering standards, and operational substance rules. Therefore, companies should view relocating as strategic decisions rather than regulatory avoidance. Firms must comprehensively consider regulatory intensity, supervisory approaches, and operational costs.

Singapore's new regulatory framework may create short-term entry barriers. However, it also suggests market restructuring around operators with adequate accountability and transparency. The system's effectiveness depends on whether these structural changes operate sustainably and consistently. How institutions and markets interact going forward will determine whether Singapore earns recognition as a stable and reliable business environment.

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn't harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research's reports, it is mandatory to 1) clearly state 'Tiger Research' as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.