Wall Street is now on-chain, and it already changed while you slept. Giants like UBS and Apollo have tokenized billions in assets that now move 24/7, not just 9-to-5.

This report by DigiFT and Tiger Research breaks down the entire RWA stack: who builds it, who uses it, and how tokenized stocks and bonds are eating legacy finance alive.

Rules are built, institutions placed their bets, and 2025 is when crypto stops being an experiment and starts being infrastructure.

Read the full report below, or at least grab the executive summary if you’re short on time.

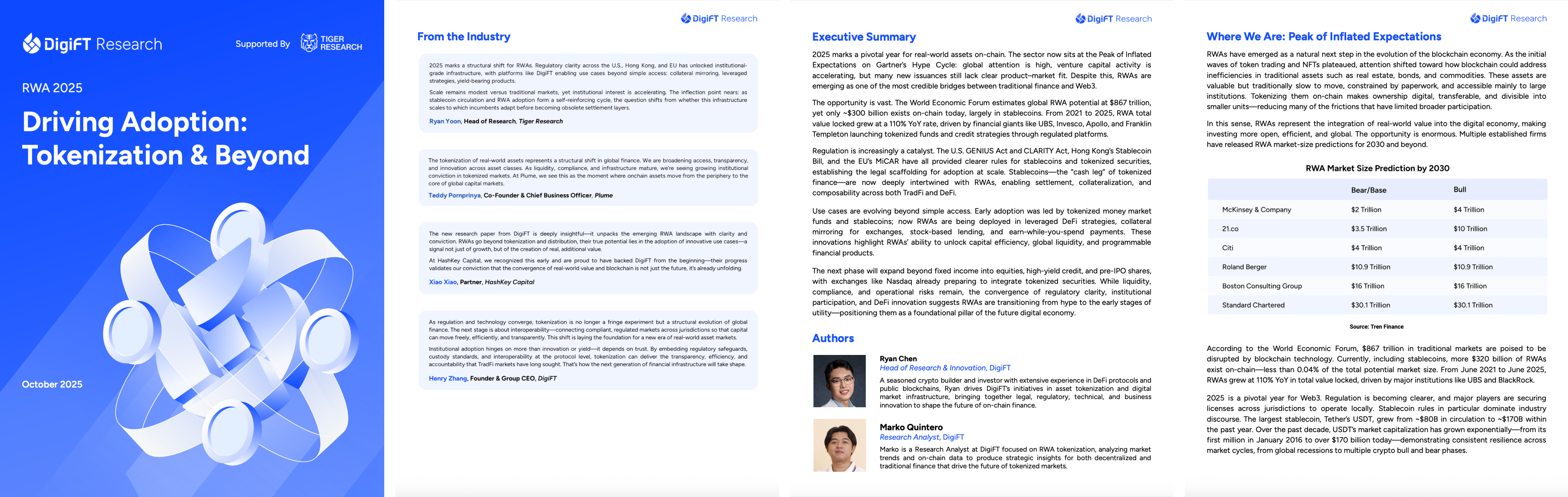

Executive Summary

1. Where We Are: A Market Fueled by Optimism

In 2025, real-world assets (RWAs) have captured global attention, with strong institutional inflows and growing public enthusiasm. Early success stories have raised expectations across the market—some projects are thriving, but others are yet to prove sustainable value. The sector now stands at a pivotal moment between hype and lasting adoption, bridging traditional finance and Web3 more than ever before.

2. How We Got Here: Enabling Access & the Top Developments in the Past Year

Tokenization began as a mission to provide access to traditional assets on-chain. What began as experimentation during a low-rate environment evolved into a regulated movement driven by institutions. The past year saw three key movements in the RWA scene: global institutions like UBS, Invesco, Apollo and more coming on-chain, new and expanding asset classes like tokenized equities and real estate, and the improvements in stablecoin regulations in the US and Hong Kong—these movements helped drive the RWA scene to where we are today.

3. Adoption of On-chain RWA Ecosystem and their Roles across the Ecosystem

The RWA ecosystem has evolved into an interdependent network where each participant drives scalable adoption. RWA ecosystem partners such as tokenization and distribution platforms, defi protocols, curators and asset managers are key players in the space for RWAs to exist and thrive. Infrastructure contributors like L1/L2 blockchains, oracle service providers and interoperability protocols help RWAs grow beyond their base capabilities. Together, these roles form a self-reinforcing loop that drives RWA adoption.

4. Beyond Tokenization: From Accessibilities to Use Cases

RWAs have progressed from mere on-chain representations to programmable financial primitives powering new use cases.

Stock Collateral Lending by xStocks × Kamino

Collateral Mirroring by KuCoin × DigiFT

Earn-While-You-Spend by Amber Premium × DigiFT

Hybrid Lending & Borrowing by Aave

5. From Fixed Income to Equities: Why Trading On-chain Defeats Holding Off-chain

Tokenization has expanded from fixed income to equities and pre-IPO shares. Two issuance models dominate: direct issuance and structured note issuance.

Tokenized equities trade around the clock, providing a decisive advantage over legacy markets. Tokenized equities activate 24/7 liquidity and lets investors manage risk continuously rather than waiting for market hours, ushering in a new era of always-on equity markets where programmable assets outperform traditional holding structures.

6. Regulations Are Driving Adoption

In Singapore, RWA tokens that represent underlying instruments such as debentures, equities, funds, and treasuries are treated under existing securities rules, providing a clear regulatory pathway for licensed players. Hong Kong requires licensing for both securities and virtual-asset activities, while Dubai’s approach under VARA promotes compliant innovation. Across regions, transparency and regulatory clarity are fueling sustainable RWA growth.

Stablecoins continue to anchor the broader RWA economy. Over the past year, new frameworks such as the U,S. GENIUS and CLARITY Acts and Hong Kong’s Stablecoin Bill have been enacted, formally recognizing stablecoins as regulated digital money and linking their growth directly to RWA demand.

7. What’s Next

The coming phase will see RWAs scale from experiments to infrastructure. Hybrid permissioned–permissionless markets, tokenized equity exchanges, and the first on-chain IPOs will anchor a new financial architecture. Asia is set to lead this transition, turning 2025 from a year of expectation into the beginning of utility for the tokenized global economy.

About DigiFT

DigiFT is a next-generation platform for tokenized real-world assets (RWAs), licensed by the Monetary Authority of Singapore (MAS) and the Hong Kong Securities and Futures Commission (SFC). The platform offers end-to-end digital asset services— including tokenization, issuance, distribution, trading, and instant liquidity provision—purpose-built for institutional RWAs.

Trusted by global financial institutions, DigiFT is the on-chain tokenization and distribution partner for leading asset managers, including Invesco, UBS Asset Management, DBS Bank, CMB International, and Wellington Management.

Dive deep into Asia’s Web3 market with Tiger Research. Be among the 18,000+ pioneers who receive exclusive market insights.

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.