Summary

Stablecoin issuance is one of the most profitable businesses in crypto. Yet with USDT and USDC holding over 85% of the market, competing on the same reserve-interest model is not realistic for new entrants. This report analyzes four issuers that have each carved out a distinct position within this structure.

Tether leads with roughly 62% market share. On top of its core reserve-yield model, it is rebuilding trust and diversifying revenue through a Big Four audit and $20B in new business investment.

StraitsX treats payment fees, not reserve interest, as its primary revenue source. Integrations with Alipay+, GrabPay, and Visa demonstrate real-world utility, and monthly transfer volume 2.5x its market cap validates the model. Securing an MAS Major Payment Institution license ahead of competitors turns regulation into a moat.

M0 does not issue stablecoins directly. Instead, it provides shared infrastructure that enables other companies to launch their own. MetaMask and Exodus already operate stablecoins on the platform, and the model strengthens through network effects as issuers and builders accumulate.

KRWQ, operating without a domestic regulatory framework, moved first to capture offshore demand from the KRW NDF market already functioning outside regulation. Once regulation is established, it plans to enter the domestic market leveraging pre-built offshore liquidity, then replicate the model across major Asian NDF currencies.

The stablecoin issuance market is not converging on a single business model. It is diverging, with fundamentally different revenue strategies coexisting depending on each issuer’s scale and positioning.

Stablecoin Issuance Market

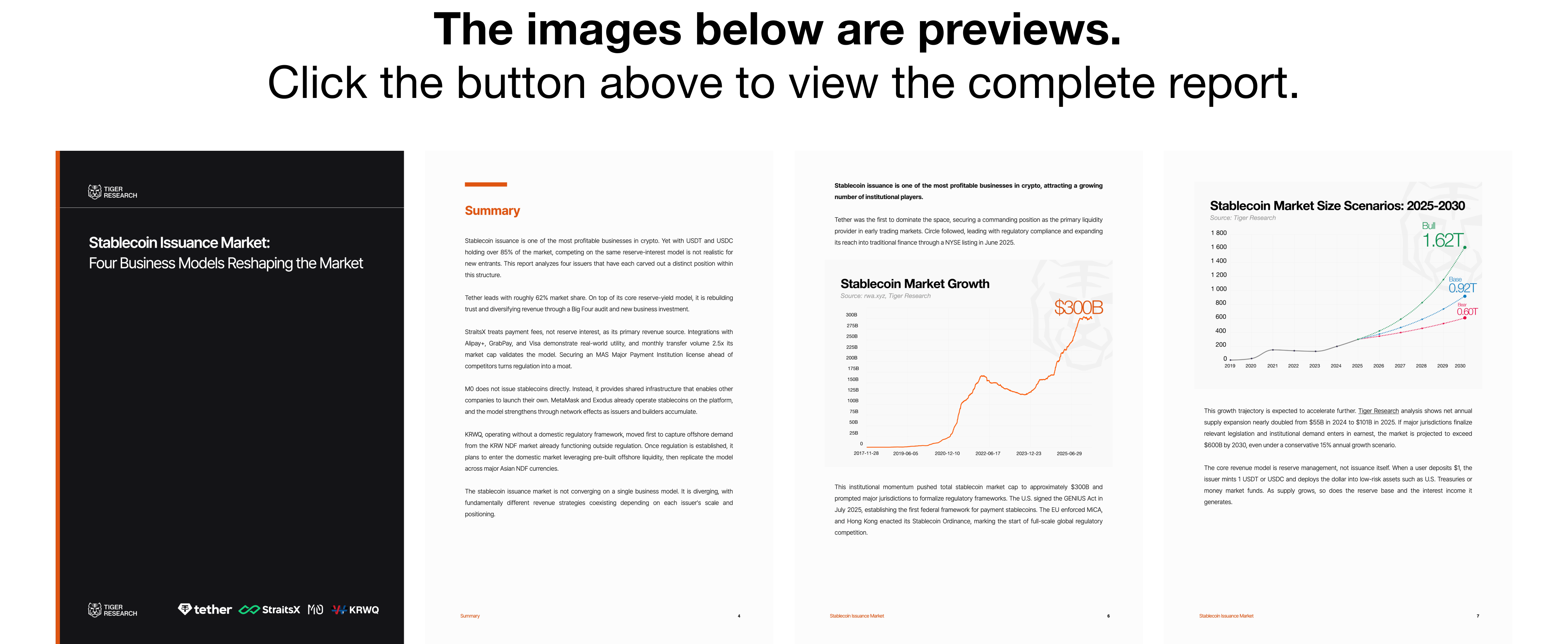

Stablecoin issuance is one of the most profitable businesses in crypto, attracting a growing number of institutional players.

Tether was the first to dominate the space, securing a commanding position as the primary liquidity provider in early trading markets. Circle followed, leading with regulatory compliance and expanding its reach into traditional finance through a NYSE listing in June 2025.

This institutional momentum pushed total stablecoin market cap to approximately $300B and prompted major jurisdictions to formalize regulatory frameworks. The U.S. signed the GENIUS Act in July 2025, establishing the first federal framework for payment stablecoins. The EU enforced MiCA, and Hong Kong enacted its Stablecoin Ordinance, marking the start of full-scale global regulatory competition.

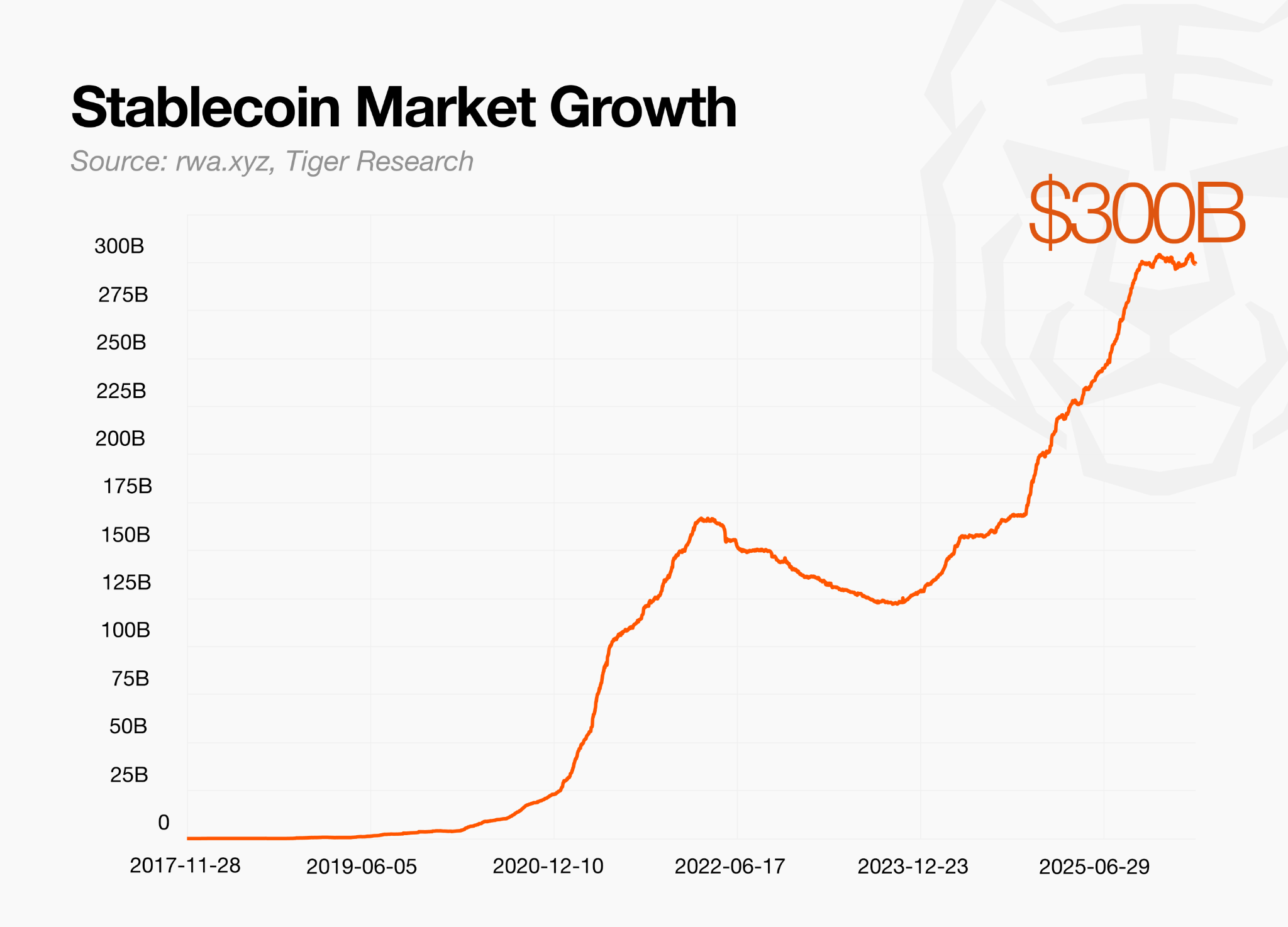

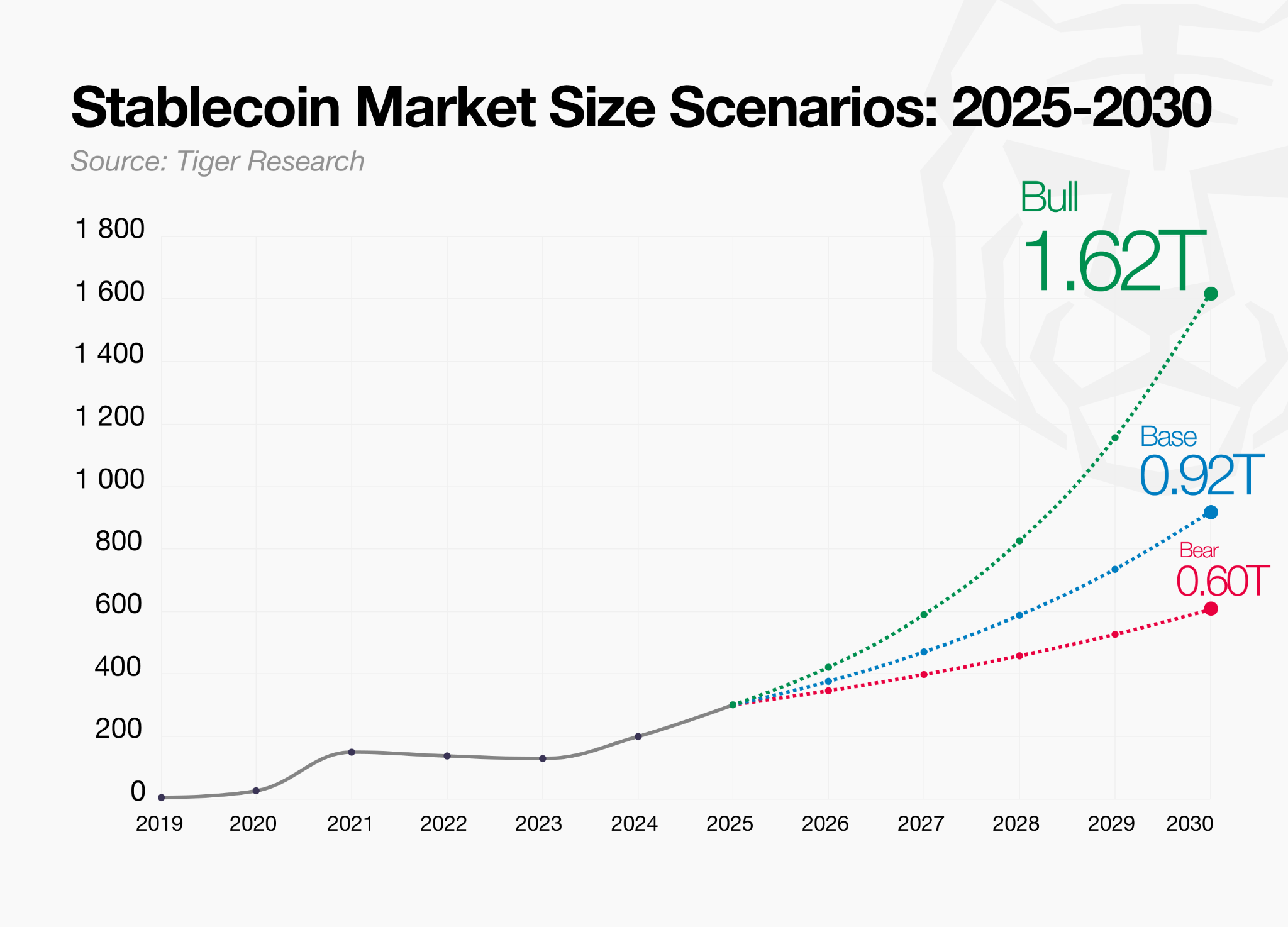

This growth trajectory is expected to accelerate further. Tiger Research analysis shows net annual supply expansion nearly doubled from $55B in 2024 to $101B in 2025. If major jurisdictions finalize relevant legislation and institutional demand enters in earnest, the market is projected to exceed $600B by 2030, even under a conservative 15% annual growth scenario.

The core revenue model is reserve management, not issuance itself. When a user deposits $1, the issuer mints 1 USDT or USDC and deploys the dollar into low-risk assets such as U.S. Treasuries or money market funds. As supply grows, so does the reserve base and the interest income it generates.

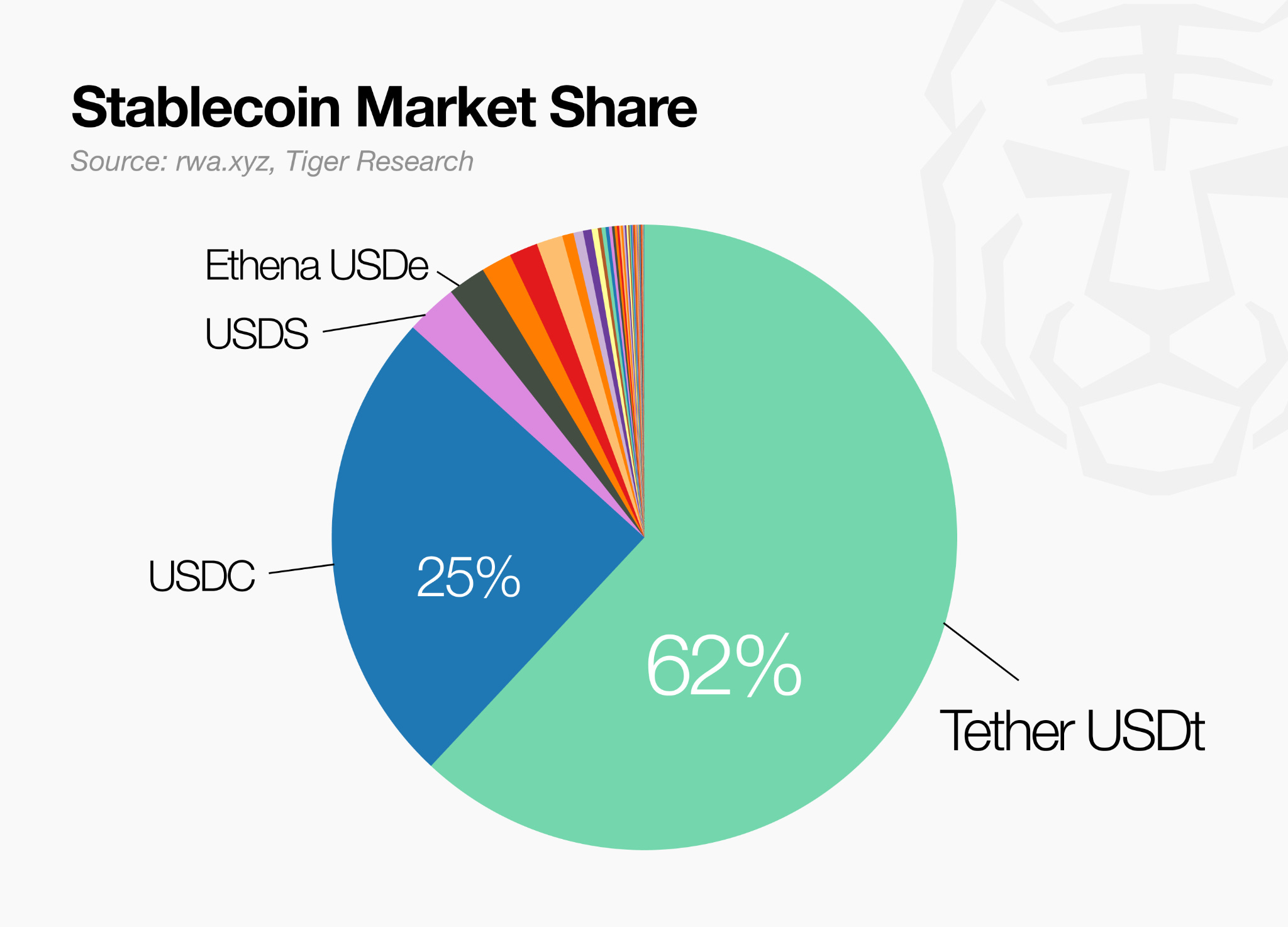

This model is inherently a scale game. Generating meaningful revenue from reserve interest requires tens of billions in circulation. Today, USDT (~62%) and USDC (~25%) together hold over 85% of the market, leaving the remaining 15% divided among dozens of smaller issuers. Competing on reserve interest alone is not viable for latecomers.

New entrants are responding by designing alternative revenue models or redefining the business entirely. Some target payment fees and real-economy integrations as their primary revenue source. Others provide issuance infrastructure rather than issuing directly, earning network fees. Some have chosen to absorb offshore demand first in under-regulated currency zones, with a plan to enter domestic markets once frameworks are in place.

The stablecoin issuance market is not converging on a single model. It is diverging, with fundamentally different revenue strategies coexisting depending on each issuer’s scale and positioning. The sections below examine how these models operate in practice, based on interviews with key players.

Tether: The Market Standard for Stablecoins

Tether is the company that first issued USDT, a dollar-pegged stablecoin, in 2014. It holds approximately 62% of the stablecoin market today and effectively serves as the industry’s pioneer.

Tether’s decade-long hold on market leadership is not simply about being first. What built today’s Tether was a series of deliberate structural shifts: a full overhaul of its reserve composition, moving away from commercial paper toward U.S. Treasuries; the establishment of a quarterly external attestation framework; and a transition to a diversified business model that reinvests stablecoin profits into AI, energy, education, and communications.

Business Model

Tether’s revenue structure spans multiple streams, but reserve management sits at its core.

Each time Tether issues USDT, it receives an equivalent amount in dollars and invests it in safe assets, including U.S. Treasuries, reverse repos, and money market funds. As issuance grows, so does the pool under management, and interest income accumulates accordingly. A portion of reserves is also held in gold and Bitcoin; price appreciation in either asset generates additional mark-to-market gains. Based on publicly available information, reserve management income appears to account for the substantial majority of total profit.

Secondary revenue streams include protocol integration fees and transaction fees. Tether also maintains a separate strategic investment portfolio across AI, energy, and communications, distinct from USDT reserves.

Regulatory Engagement

Since Q1 2025, Tether has held a stablecoin issuer license under El Salvador’s Digital Asset Law, operating under the oversight of the National Commission on Digital Assets (CNAD). However, this structure has been cited as a limitation on transparency. S&P has referenced it as a basis for assigning USDT a low transparency score.

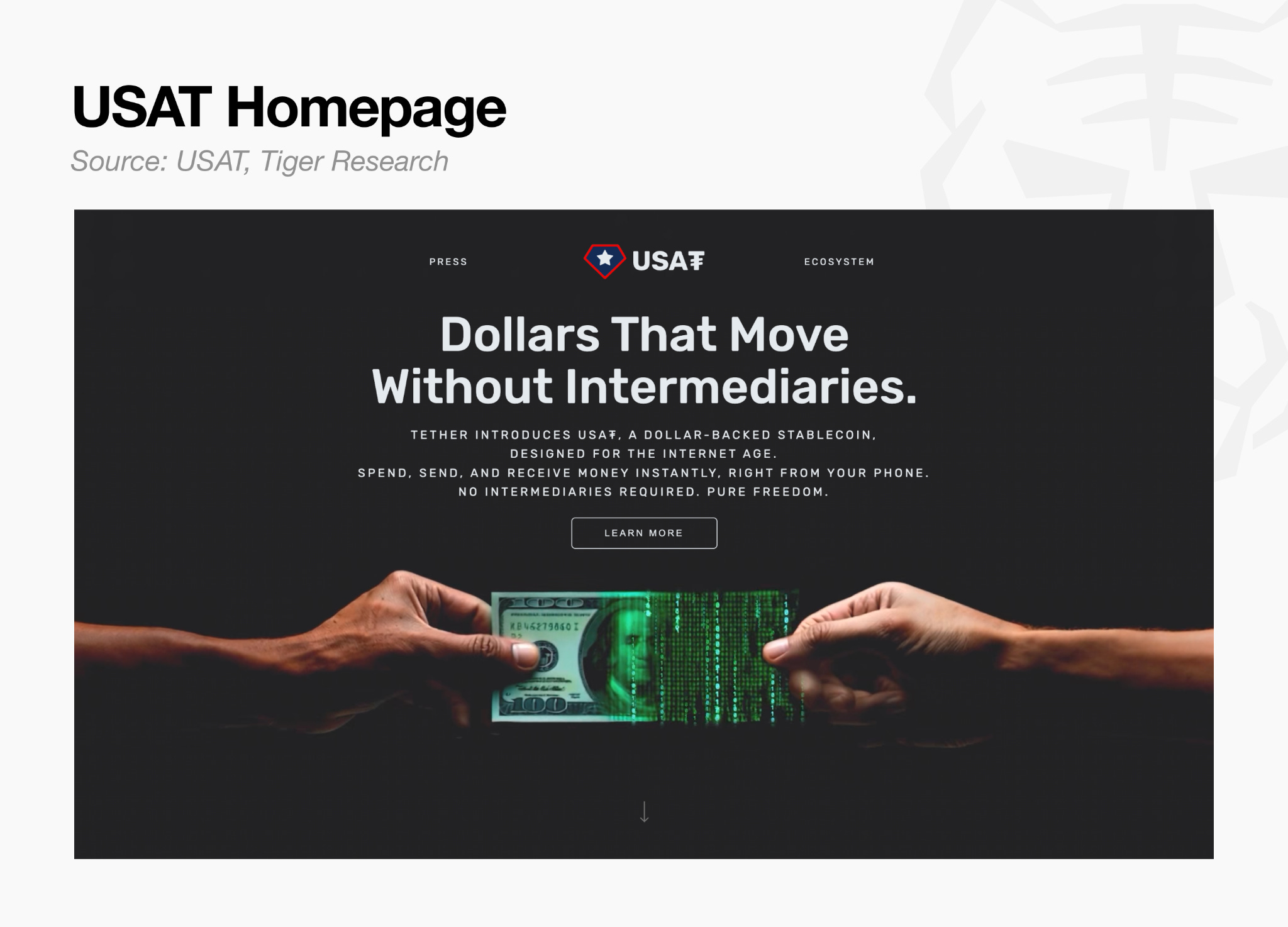

Tether is addressing this by approaching the U.S. market separately. Under the GENIUS Act framework, it launched USAT as a distinct product line tailored to the U.S. regulatory environment, while USDT continues as its global general-purpose offering. The two markets are structurally separated and pursued simultaneously.

Tether is also responding to the transparency debate. While quarterly reserve attestation reports verified by BDO have been the baseline, Tether formally engaged a Big Four accounting firm in March 2026 for a full audit of USDT reserves.

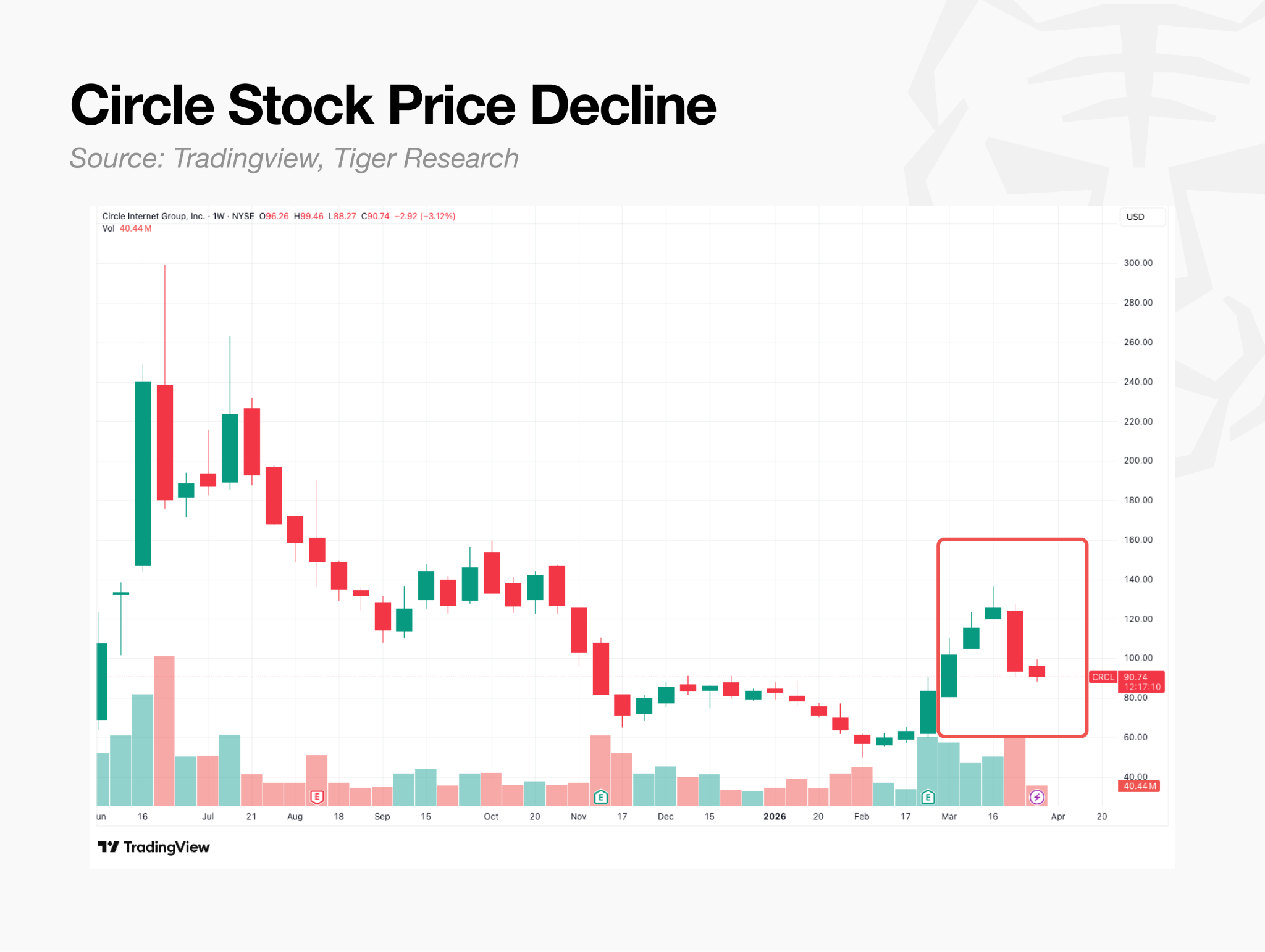

Unlike attestations, which confirm reserve composition at a single point in time, a full audit covers assets, liabilities, and internal control systems at a higher level of scrutiny. Markets took note. As Tether’s regulatory standing improved, Circle’s share price fell approximately 20%, a signal that resolving what had been Tether’s primary competitive weakness is reshaping the competitive landscape.

Growth Strategy

Tether’s growth strategy centers on RWA expansion, Technological innovations, and new business development.

Its flagship RWA product is Tether Gold (XAUT), a token backed 1:1 by physical gold held in Swiss vaults. It accounts for more than half of the total market capitalization of gold-backed stablecoins, with the underlying asset base continuing to expand.

New business expansion is proceeding at the same pace. Tether’s proprietary investment portfolio, diversified across AI, energy, media, and communications, exceeds $20B. Entirely separate from USDT reserves, it functions as a surplus-capital growth engine, reinvesting profits generated from stablecoin issuance into long-term growth drivers.

Key Takeaways

Tether’s case contains structural lessons that any company evaluating the stablecoin business must address.

1. Stablecoin issuance is a scale business. Every dollar of USDT issued is invested in U.S. Treasuries. As issuance grows, Treasury holdings grow, and so does interest income. Understanding this direct link between issuance volume and AUM is the starting point for any business model analysis.

2. Regulatory compliance is a prerequisite, not an option. Even Tether is moving within the regulatory perimeter. Regardless of how unclear the current framework may be, business structures must be designed from the outset with regulatory integration in mind. Stablecoins are, by nature, an industry that operates within regulation.

StraitsX: ASEAN’s Real-Economy Stablecoin Issuer

StraitsX is a Singapore-based stablecoin issuer. Its core offerings are XSGD (SGD-pegged) and XUSD (USD-pegged), with expansion into major ASEAN currencies including the Indonesian rupiah (XIDR).

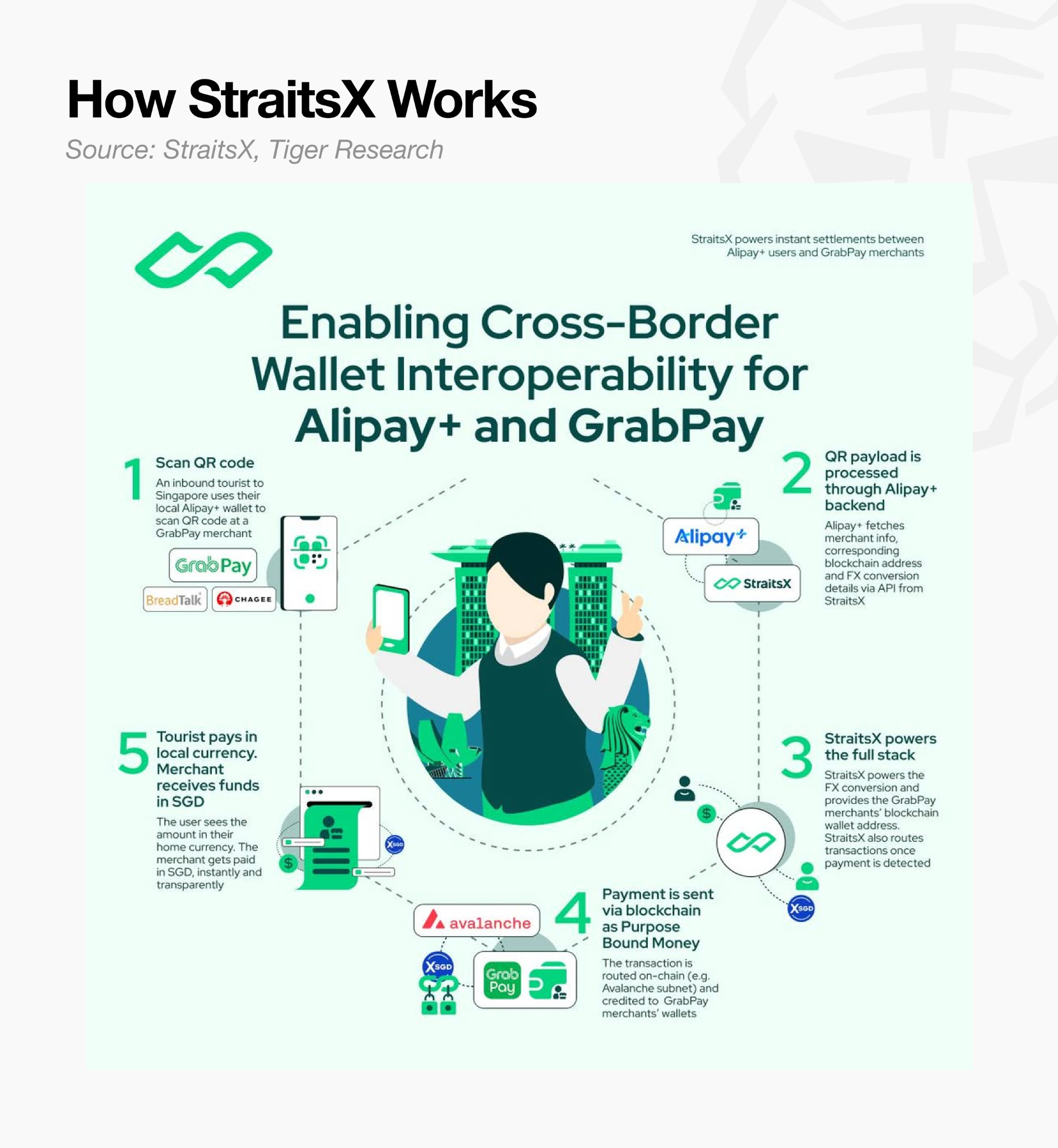

The case for attention goes beyond digital asset issuance: StraitsX is building payment infrastructure directly connected to ASEAN’s real economy. Per on-chain data platform rwa.xyz, XSGD’s monthly transfer volume (~$39.9M) is approximately 2.5x its market cap (~$15.8M).

Compared to dominant global stablecoins such as USDT and USDC, StraitsX’s absolute asset size and turnover remain smaller. But the use case is fundamentally different. Where major stablecoins primarily serve investment trading on crypto exchanges, StraitsX tokens are used in everyday real commerce. The data confirms that issued coins are not sitting idle in investor wallets but circulating continuously in the market.

Ultimately, the reason StraitsX is recognized as a specialized payment infrastructure for the ASEAN region lies not just in on-chain metrics but in the robust B2B payment network integrations behind them.

Business Model

StraitsX’s revenue model is centered on payment fees. Reserve interest income is constrained by external variables such as circulating supply and interest rates, while payment fees are tied to transaction volume and therefore scale with business growth.

Reserve Interest Income: Reserves corresponding to XSGD and XUSD in circulation are held in trust accounts at DBS, Standard Chartered, and CIMB. Per MAS regulations, interest accrues to the company, not token holders. Based on combined circulation of approximately $65M, estimated annual yield is $2.6M–$3.25M.

Payment Processing Fees: Generated each time stablecoins are used for payment or settlement. Key channels include on-ramp/off-ramp (DVA), QR payment networks (Alipay+ and GrabPay integrations), and card issuance (Visa BIN sponsorship). Volume-linked, not rate-linked.

OTC and FX Swap Spreads: FX spreads earned on stablecoin-to-stablecoin swaps, buy/sell transactions, and large OTC trades.

Payment fees in particular are generated through StraitsX’s external network integrations. Major mobile payment platforms such as Alipay+ and GrabPay, as well as global exchanges including Binance and Bybit, have adopted StraitsX’s system for fund settlement, covering use cases.

As a notable data point, StraitsX internal data indicates that Visa card-linked stablecoin payment volume grew 40x over the past year, with 83x growth in cards issued in the same period.

Regulatory Positioning

The crypto industry broadly views strict regulation as a constraint on business expansion. StraitsX takes the opposite approach, using the Monetary Authority of Singapore’s (MAS) regulatory framework as a competitive defense.

The foundation of this strategy is StraitsX’s Major Payment Institution (MPI) license from MAS. Through this license, StraitsX is authorized to operate 6 of the 7 major payment services regulated by MAS. This enables the company to legally conduct cross-border remittance, foreign exchange, merchant payments, and account issuance within a single legal entity, well beyond simple coin issuance. XSGD and XUSD are stablecoins recognized as substantively compliant with the MAS Single-Currency Stablecoin (SCS) regulatory framework.

For institutional capital to enter the blockchain ecosystem at scale, bank-grade KYC and AML systems are a prerequisite. Most crypto firms operating outside the regulatory perimeter cannot meet this standard.

StraitsX is co-developing a next-generation cryptography-based identity verification system with regulators. The strategy is to pre-emptively meet the compliance standards that will be required when institutional funds flow in, positioning StraitsX to capture that capital exclusively.

Growth Strategy

Having established a self-sustaining revenue model, the next objective is entry into new settlement markets.

The primary long-term growth driver is real-world asset (RWA) settlement. Demand is expected to grow for tokenized cash as the settlement leg finalizing on-chain transactions in traditional assets such as equities and bonds. StraitsX plans to capture institutional settlement demand by providing cross-chain interoperability across multiple blockchain environments.

Key Takeaways

The primary long-term growth driver is RWA settlement. As traditional assets such as equities and bonds move on-chain, demand for tokenized cash as a settlement medium will grow alongside them. StraitsX plans to capture institutional settlement demand early by offering cross-chain compatibility across multiple blockchain environments.

1. Velocity matters more than volume. Non-dollar issuers cannot grow through issuance scale alone. Securing real use cases and integrating into B2B settlement networks must come first. The key metric is turnover rate, not market cap.

2. Regulatory compliance is a competitive moat. StraitsX secured MAS licensing preemptively, converting regulatory burden into a structural barrier to entry. Stablecoins operate at the intersection of crypto and traditional finance, making them an inherently regulated industry. How quickly an issuer achieves regulatory alignment, and how closely it engages with regulators, will be a decisive competitive variable.

M0: Shared infrastructure for stablecoin builders and issuers

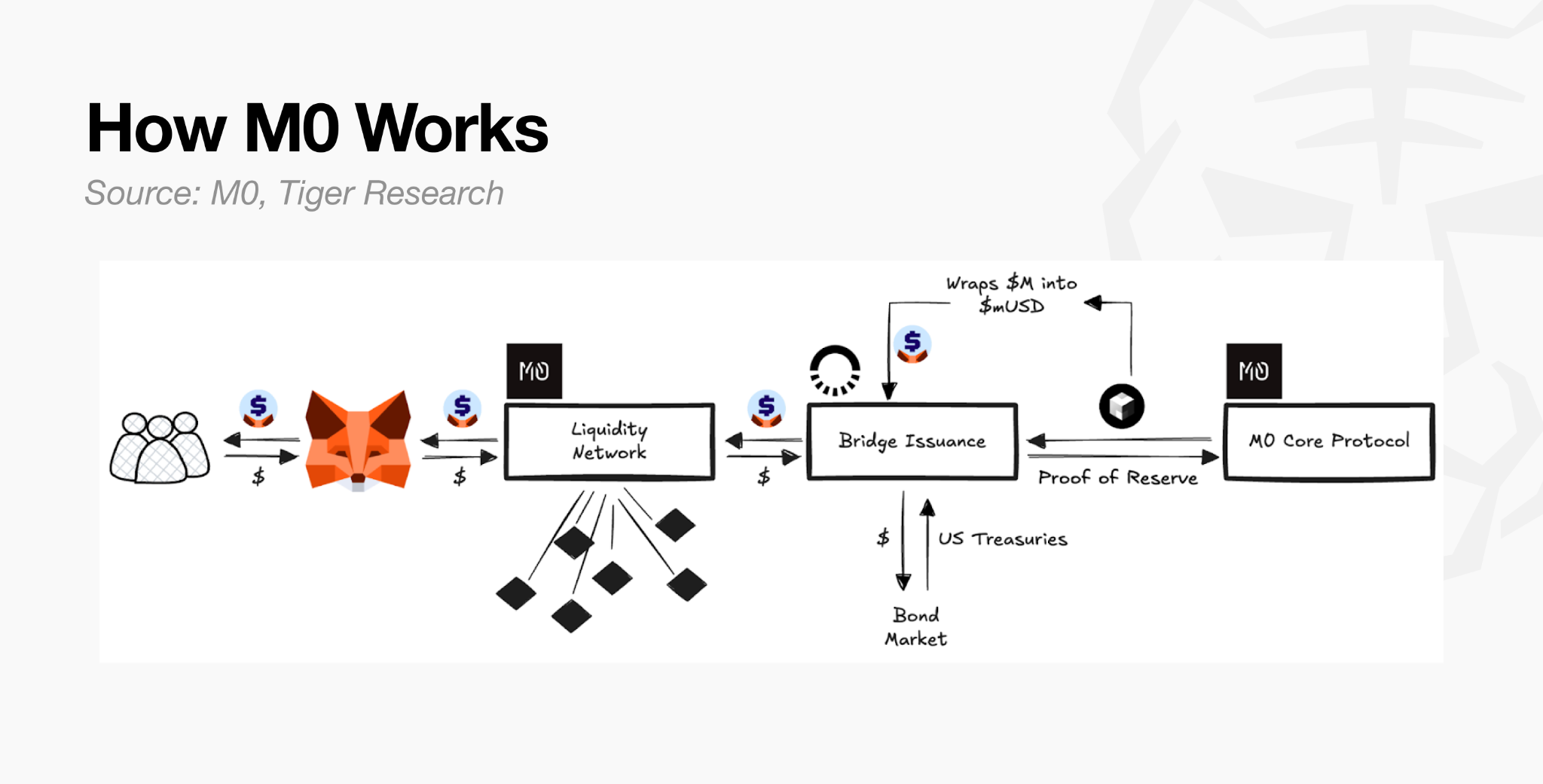

M0 provides shared infrastructure that allows businesses to launch stablecoins and financial institutions to issue them.

Rather than issuing stablecoins directly, M0 provides infrastructure which enables multiple builders to launch their own stablecoins on a common technical foundation.

The structure addresses two core problems.

The stablecoin market is fragmented, with each issuer operating an independent stablecoin issuance stack, making cross-coin compatibility structurally difficult.

Without M0, stablecoin builders face a “cold-start” problem: they must build liquidity, partnerships, and network effects for their own stablecoin from zero on launch day.

M0 resolves both through a shared layer. Every stablecoin on the platform is built on common standards and technology, instantly shares existing liquidity and is redeemable 1:1 with all other stablecoins from the outset.

Current stablecoins built on M0 infrastructure include MetaMask’s mUSD, Exodus XO Cash, KAST’s USDK, Noble’s USDN, Usual’s UsualM - with many more currently in development. Issuers powered by M0 issuance stack include Bridge (a Stripe company), MoonPay and 1Money.

Business Model

Issuer: A regulated institution that holds reserves as collateral to mint stablecoins using the M0 infrastructure, paying the platform a designated rate from a portion of interest earned on reserves.

Builder: An entity that owns a specific use case and uses M0 to launch and control its own stablecoin - capturing the economics, customizing how money behaves directly into its product.

MetaMask’s mUSD illustrates how the two roles work in practice.

MetaMask leveraged M0 technology to design and construct its own stablecoin under the mUSD brand, and applied desired behavior and product layer on top. Bridge holds the regulatory licenses, manages U.S. Treasuries as collateral, and fulfils the platform obligations, ultimately minting and burning mUSD as demanded.

The two roles are fully separated. Bridge doesn’t own the end use case or product. MetaMask never touches the collateral. Yet the stablecoin that reaches the end user carries immediate 1:1 convertibility with every other M0-powered stablecoin on the network, with liquidity shared from day one rather than built from scratch.

The revenue flow begins with Treasury interest on Issuer-held collateral. Issuers collect this interest while separately paying the Minter rate (3.33% as of March 2026) to the platform on outstanding issuance.

M0’s current circulating supply stands at approximately $276M. As more issuers and builders adopt the platform, this figure is expected to grow.

Regulatory Engagement

M0 positions itself as a technology platform and structurally separates compliance obligations among Issuers.

M0’s Stablecoin Core embeds the compliance functions required by issuers at the technology layer, including allow-listing, pausing, and freezing. However, the actual operation of these functions, along with licensing, AML, KYC and any other regulatory obligations, remains the direct responsibility of each Issuer. M0 provides the technical tools; it does not substitute for regulatory responsibility.

For this division of responsibility to function in practice, Issuers s must be compliant with the regulations of each market they operate in.

M0 identifies the United States as the market where stablecoin regulation is moving fastest. The enactment of the GENIUS Act in July 2025 established a federal stablecoin regulatory framework, which has since visibly accelerated enterprise adoption demand. As leading jurisdictions put clear frameworks in place, stablecoin demand expands, and M0’s opportunity to establish its infrastructure as a market standard grows accordingly.

Growth Strategy

M0’s current top priority is the expansion of total M0-powered stablecoins in circulation on the platform. Because spread-based revenue scales with circulation volume, growing the network of builders and issuers is the most critical metric at this stage. In public interviews, CEO Luca Prosperi has stated that network expansion is the top priority for the next two to five years.

The Builder base is already diversifying across wallets, gaming, fintech, and payments, with participants including MetaMask, Exodus, Noble, Usual andKast. With enterprise adoption demand accelerating in the wake of the GENIUS Act, this is the right moment to expand the Issuernetwork. How many Issuers and Builders M0 can bring onto the platform during this window will determine its long-term market position.

Key Takeaways

M0’s case illustrates a competitive shift in the stablecoin market: the contest is moving from “which stablecoin achieves the highest circulation” toward “who controls the Issuer and Builder network and infrastructure standard first.”

1. Fast integration creates network effects. Building on M0’s infrastructure provides automatic compatibility with all stablecoin features across the platform, eliminating the need for repeated, per-stablecoin integration work.

2. Infrastructure value scales with the market. Not every company has the capacity to issue stablecoins independently. The value of shared infrastructure that handles licensing, technology, and liquidity management grows as more issuers join. This is why M0’s structural advantage strengthens alongside market growth.

As long as the stablecoin market does not consolidate around a handful of dominant players, the value of common infrastructure connecting multiple issuers and builders will continue to rise. The key question going forward is whether M0’s shared standard can establish itself as the industry’s foundational infrastructure layer.

KRWQ: Bringing the Korean Won On-Chain

KRWQ is a Korean won (KRW)-pegged stablecoin launched in October 2025 by IQ in partnership with Frax. Notably, South Korea has no domestic regulatory framework for won-denominated stablecoins.

KRWQ’s target market is not domestic but offshore. The won is a currency legally traded only within Korea, yet substantial offshore demand already exists from investors seeking to hedge or speculate on KRW exchange rate movements.

A foreign investor holding Samsung Electronics shares, for example, is fully exposed to KRW fluctuations. A stronger dollar means losses; a weaker dollar means gains. Even investors who want to eliminate this risk cannot directly hedge won exposure from outside Korea. This gave rise to the NDF (Non-Deliverable Forward): a contract settled in dollars for the difference between a contracted rate and the actual rate, with no direct exchange of won. Built on this structure, the KRW NDF market has grown into one of the highest-volume markets in the global NDF landscape.

KRWQ’s strategy is to capture this offshore demand first, then enter the domestic market once Korean regulation is in place. Offshore before onshore, with only the sequence reversed.

Business Model

The existing NDF market is an OTC market structured around bilateral bank negotiations, making pricing opaque and transaction costs high. Korean government restrictions on offshore won trading limit the pool of eligible participants and suppress liquidity. Settlement requires waiting until contract expiry, which creates inherent counterparty risk.

KRWQ aims to address these limitations through perpetual futures. NDFs and perpetual futures are structurally the same product.

No direct exchange of won

Settlement in dollars based on price differential

Used to hedge or take directional positions on KRW exchange rate risk

The only difference is maturity. NDFs have fixed expiry; perpetuals have no maturity, operate on-chain 24 hours a day, and deliver the same function at lower cost. Recently KRWQ has launched an NDF market through EDXM International.

Regulatory Engagement

KRWQ adopts a two-track strategy: build the market offshore first, then enter onshore once domestic regulation is in place.

KRWQ was designed with anticipatory reference to stablecoin legislation currently under deliberation in the Korean National Assembly, with the goal of becoming the first regulatory-compliant KRW stablecoin. The domestic legislative landscape, however, remains complex. Regulatory uncertainty is a near-term barrier to market entry, but for KRWQ it also buys time to build an offshore liquidity lead ahead of competitors.

At the final stage, KRWQ plans to partner with domestic regulated banking institutions to enable direct KRW deposit and withdrawal for issuance and redemption.

Growth Strategy

KRWQ’s growth strategy consists of three phases.

Offshore capture (current): Build KRWQ-based perpetual futures trading infrastructure targeting offshore institutions and DeFi protocols.

Onshore transition: Once domestic legislation is enacted, enter the Korean market using already-established offshore liquidity and infrastructure as a foundation.

Replication across Asian currencies: Beyond KRW, INR (Indian rupee), TWD (Taiwan dollar), and IDR (Indonesian rupiah) are all major Asian NDF currencies. These currencies share the same structural characteristics as the won: capital controls paired with active offshore NDF markets.

Key Takeaways

1. Regulatory absence can be an opportunity, not a waiting period. In Asia’s stablecoin market, regulation is typically treated as a prerequisite for entry, and most players wait indefinitely for legislation to materialize. KRWQ took a different view: market structures already functioning offshore exist regardless of domestic regulation.Offshore liquidity becomes the lever for domestic entry.

2. The KRW NDF market was already operating outside domestic regulatory jurisdiction. KRWQ moved to absorb that demand first. When regulation arrives, it will enter the domestic market equipped with offshore liquidity and infrastructure already in place. The strategy was not to wait, but to start where revenue was already being generated.

Where Do Latecomers Still Have a Chance?

The stablecoin market is heavily concentrated, with USDT and USDC holding over 85% of total supply. Competing on the same reserve-interest model is not a realistic path for new entrants. Yet the cases examined in this report show that there is more than one route into the market.

The core principle for latecomers is to avoid playing the same game as Tether and Circle. Winning a reserve scale competition is not possible, but distinct positions can be secured along different axes: payment networks, issuance infrastructure, and offshore markets. As the stablecoin market expands, so does the variety of competitive forms. The industry is not repeating a single model; it is diverging into a market where different strategies coexist.

That said, the players covered in this report are no longer challengers. They have become leaders in their respective domains. Drawing lessons from their approaches is valuable, but replication alone is not sufficient. The next generation of entrants must define and solve problems beyond the positions these players have already claimed.

Ultimately, the companies that survive in the stablecoin issuance market will not simply be those with differentiated entry strategies. They will be the ones that execute those strategies and solve the next layer of problems as they scale. The market has moved past the question of who finds a new model, and into the question of who actually makes it work.

Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.