Crypto is in a downturn, yet the tokenized stock market keeps growing. It splits into fully collateralized spot and perpetual futures, with perps drawing the most attention and a range of strategies emerging.

Key Takeaways

While equities set record highs, crypto saw both market cap and volume fall. As the two diverged, the tokenized stock market grew by building perpetual futures open interest.

The market splits into fully collateralized spot and perpetual futures. Perps draw attention because they trade stocks unavailable on home exchanges, 24 hours a day, with leverage on top.

When the regular session is closed, the price perps set becomes a leading indicator of the next day’s spot open, predicting not just direction but also the size of the move.

Two retail openings, a delta neutral trade that collects the spot to perp premium as funding, and cross-exchange arbitrage on price gaps.

The same structure extends to businesses such as market makers, regional oracles, tokenized issuance, and basis hedge funds. Small in scale, but as institutions enter, opportunity exists on both the investment and business sides.

1.Equity Markets Now Pulling In Crypto Liquidity

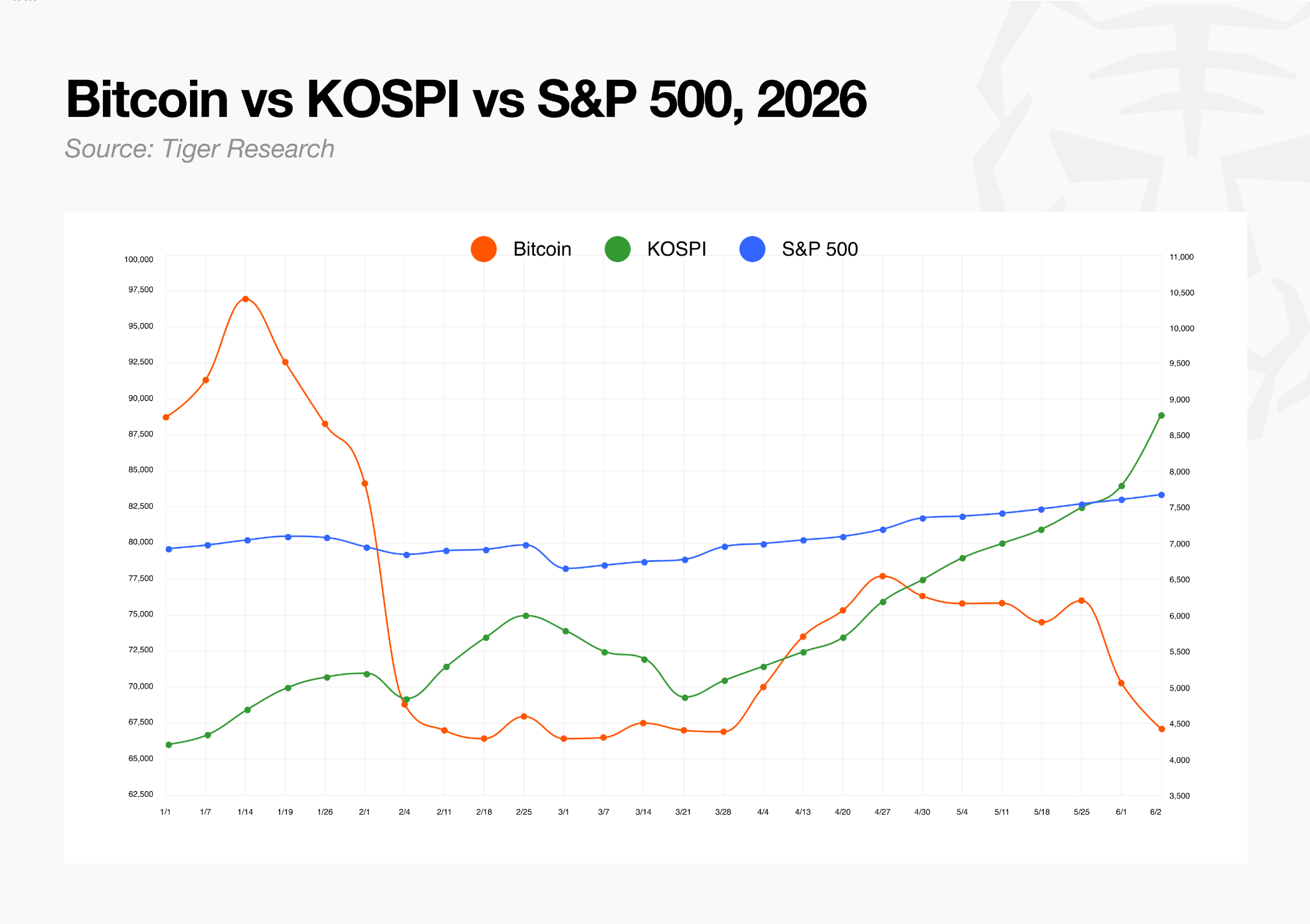

In Q1 2026, total crypto market cap fell 20.4% and centralized exchange spot volume dropped 39.1%. Bitcoin has been declining since its October 2025 record high.

Equities went the other way. The S&P 500 cleared its annual target, and the KOSPI rode a semiconductor rally to double this year. As total crypto market cap fell sharply, most national equity markets set record highs. The two paths have never split this clearly.

2. Collateral Splits the Market, Capital Flows to Perps

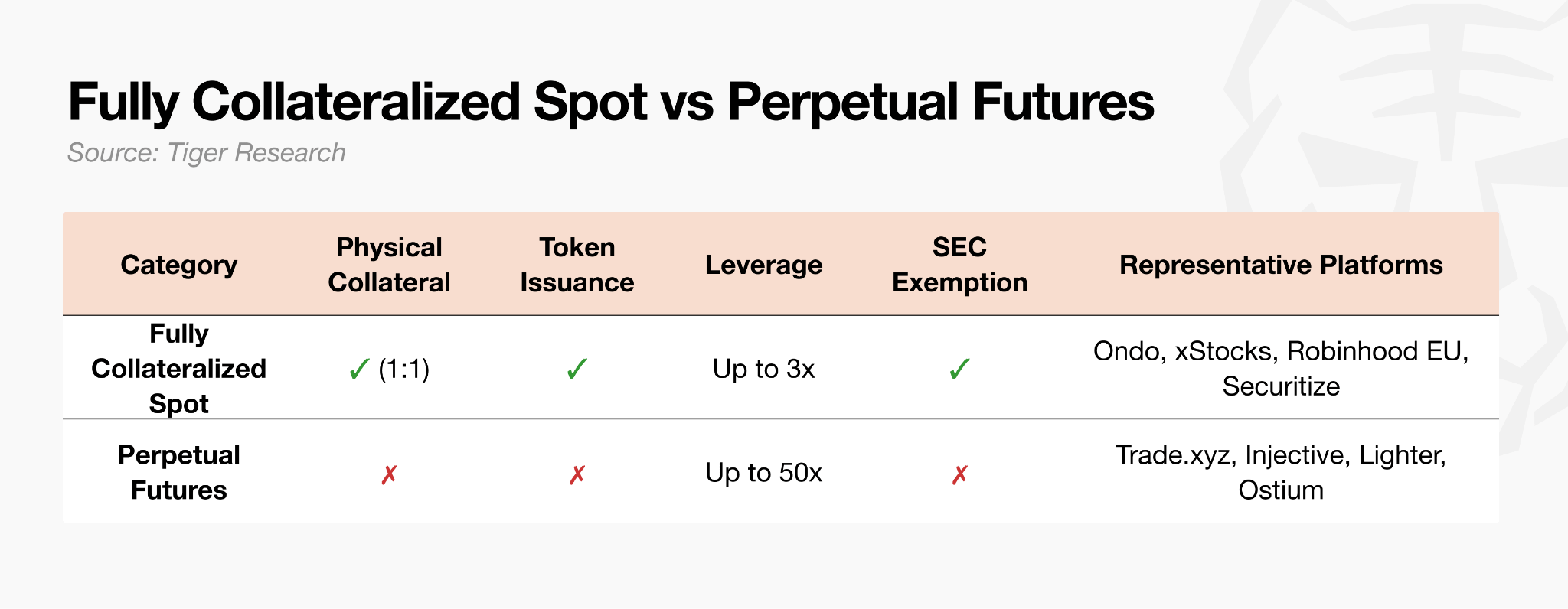

The tokenized stock market splits in two by collateral structure.

Fully collateralized spot deposits real shares 1 to 1, then issues a token. The investor holds the share itself or a legal claim on it. Issuance details differ by platform, but an underlying asset always exists.

Perpetual futures work differently. No real shares are held. The trader posts margin and opens a contract that tracks the price, so there is no claimable underlying. Margin is mostly stablecoins, and a growing number of platforms now accept other assets such as ETH.

Perps draw attention because they keep spot’s advantage, 24-hour access to stocks unavailable on home exchanges, and add far greater leverage. Some fully collateralized spot products on Kraken xStocks offer up to 3x margin, while perps reach up to 20x depending on the product. With no underlying to custody and price tracked only through an oracle feed, listings are fast and the range of tradable tickers is wide.

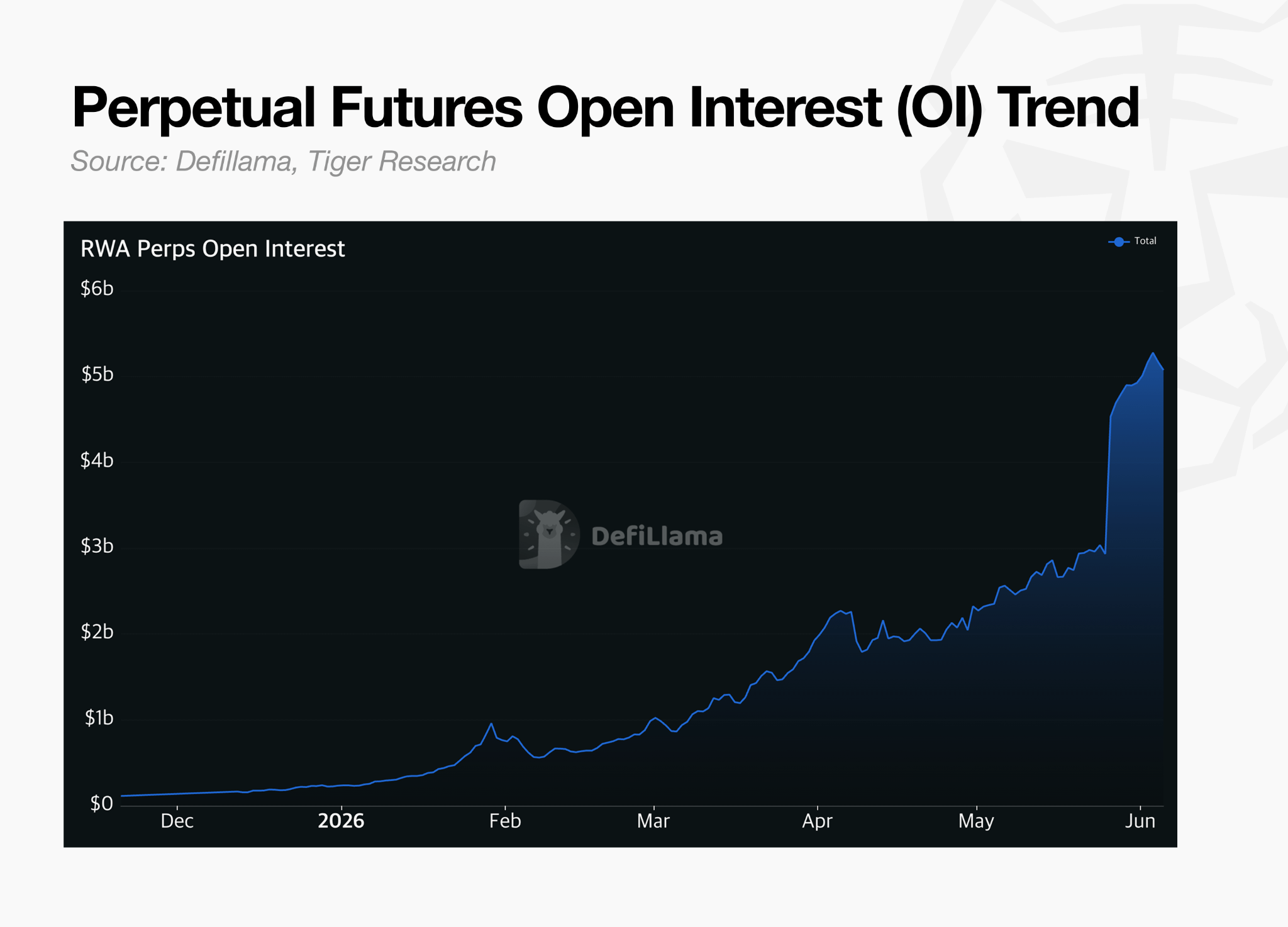

Against traditional markets it is still small. US equity markets turn over about 1.1 trillion dollars a day. Stock perp open interest, the total of contracts currently live, sits at 2.25 billion dollars. The metrics differ, so a direct comparison is hard, but the market is clearly early stage.

The direction is clear. OI rises each quarter, and regulators are starting to treat it as a market. The SEC has cited perps as an innovative financial product, and the CFTC is publicly reviewing US institutionalization. It began outside regulation, but is moving inside the system faster.

3. The 24-Hour Market vs the Real Market

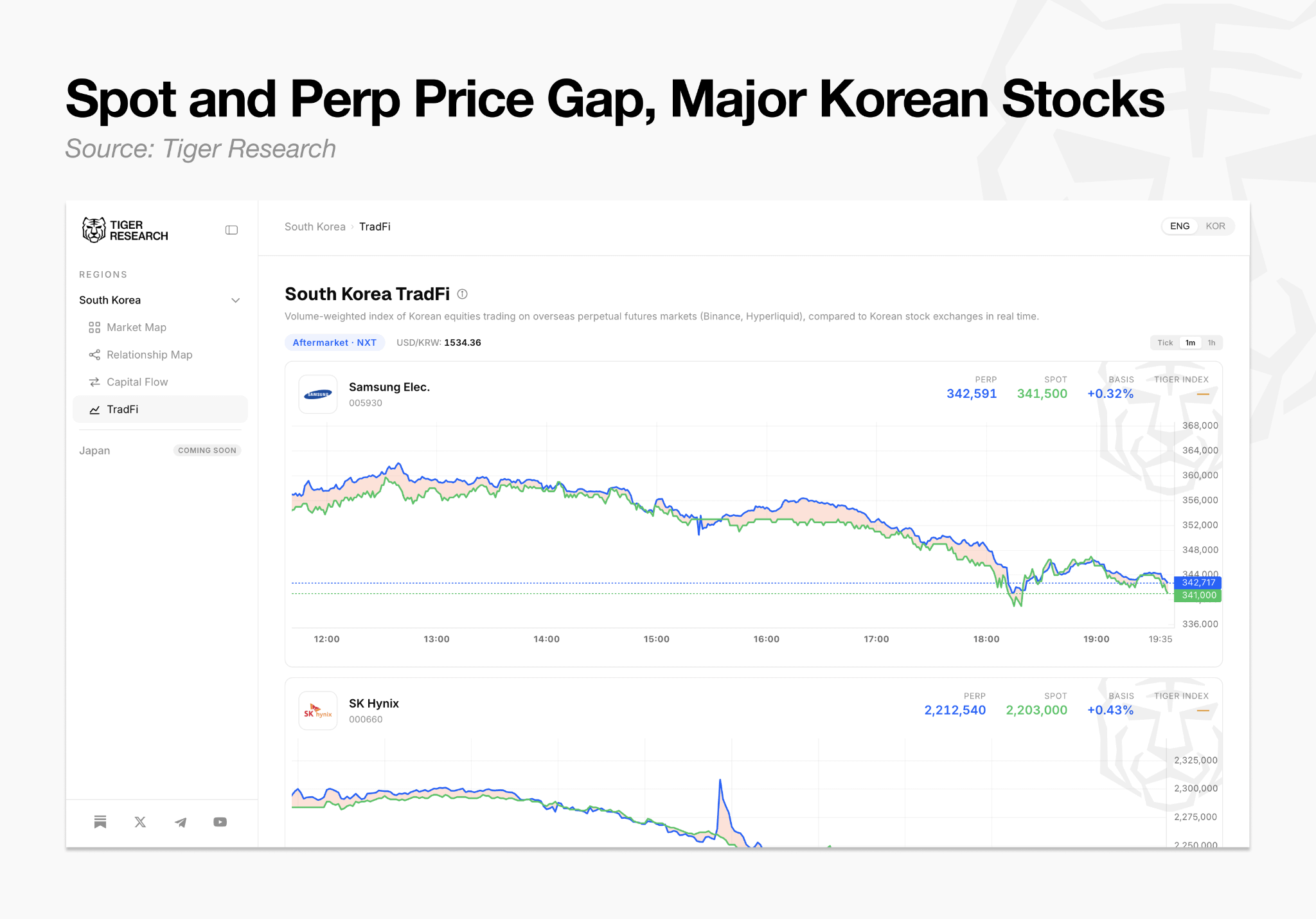

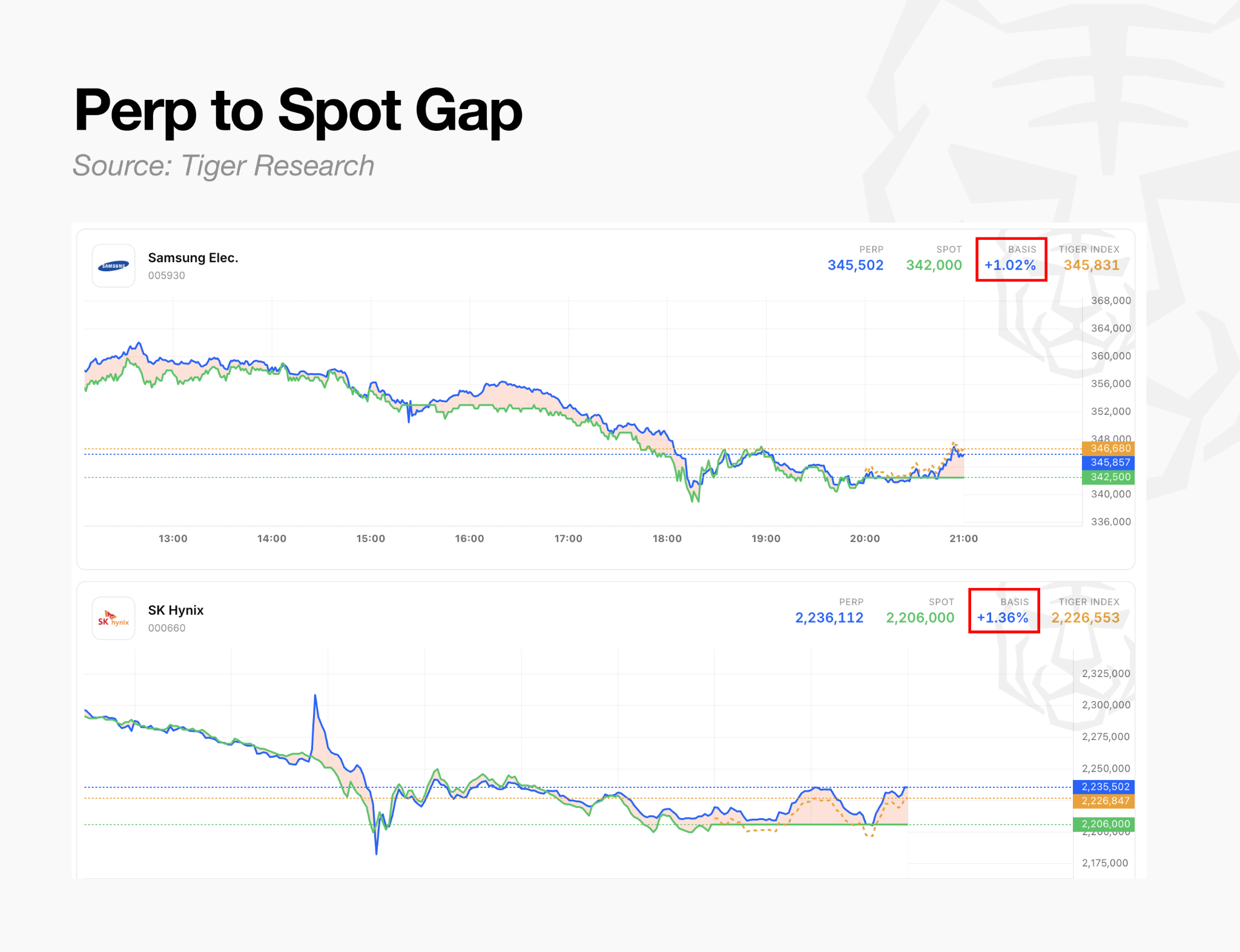

Tiger Research tracks this shift, offering a tool that compares Korean stock prices on overseas perpetual markets against KRX spot in real time. It aggregates prices from the perp exchanges that support Samsung Electronics, SK Hynix, and Hyundai Motor using a volume-weighted average, set side by side with each name’s domestic spot price.

The data so far shows three patterns.

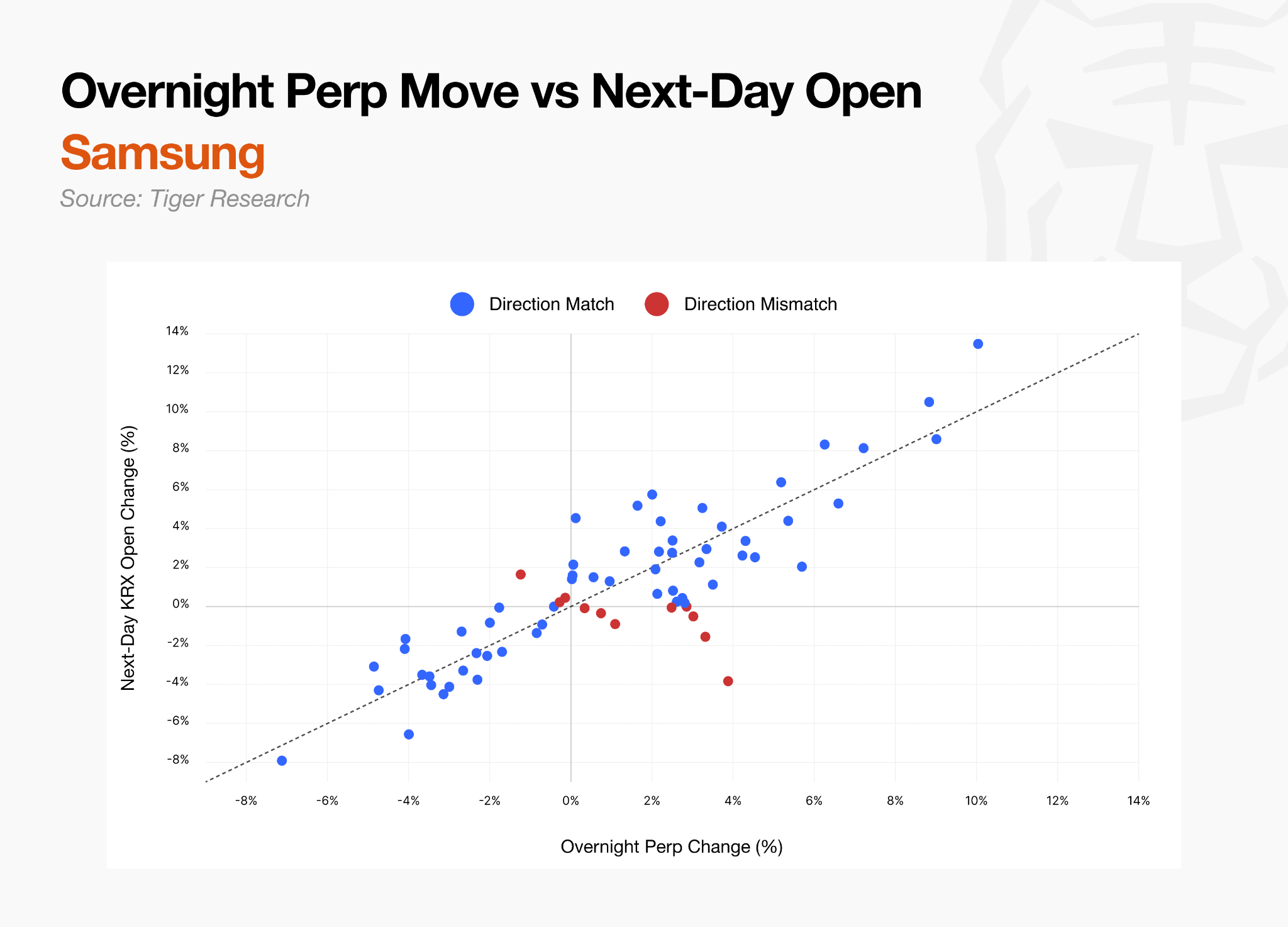

3.1. Overnight Perp Moves Predict the Next Open

Korea’s market stops at night. US markets move, Nvidia reports, FX swings, but Korea sees no trading until the next morning. Perps trade through it.

This raises a question. With spot closed, what price do perps reference?

The answer is that they do not follow one. While the session is open, perps pull spot prices from institutional data. When it closes, perp participants’ own trades set the price directly. Rather than copying a closed spot market, they discover a new price that reflects overnight news and macro variables.

The data bears this out. On days perps rose after the close, the next session opened higher 82% of the time for Samsung Electronics and 95% for SK Hynix. When perps fell, the next session opened lower 96% for Samsung Electronics and 78% for SK Hynix. Directional match runs around 85% for both, with correlation of 0.85 to 0.89.

Magnitude tracks too. A 3% overnight gain in perps led to an open roughly 3% higher. The regression coefficient of perp change against the actual opening gap is 0.93 for Samsung Electronics and 1.00 for SK Hynix, all but signaling how far the move will run.

Weekends are sharper. From Friday close to Monday open, the perp-implied direction matched the actual Monday open 93% of the time for Samsung Electronics and 87% for SK Hynix, because perps absorb two days of global variables first.

Reading the overnight perp price gives an early read on where the morning open will land.

3.2. Delta Neutral Trade on the Spot-Perp Premium

Perps have no expiry. To keep the price from drifting too far from its reference, longs and shorts exchange a fee at set intervals, called the funding rate.

For example, when a perp trades above its reference, the gaining longs pay the losing shorts. The larger the premium, the larger the payment. When one side gains more than the reference, it is charged accordingly. As traders move to avoid that cost, the price converges back to the reference.

In the data, Korean stock perps traded above spot, with an intraday average premium of 0.15% for Samsung Electronics and 0.23% for SK Hynix. Selling the perp means collecting that premium as funding each cycle.

The strategy follows. Buy KRX spot intraday and sell an equal amount of the perp at the same time. If the stock rises, spot gains and the perp loses. If it falls, the reverse. The two offset, so the outcome is near zero whichever way the stock moves. In return, funding comes in from the short perp. The position earns from the premium alone, with no bet on direction. Removing directional risk this way is the delta neutral trade.

The premium does not last. The perp to spot gap closed halfway in about 40 minutes on average. It suits high-volatility phases where premiums widen, and it requires constant monitoring.

3.3. Arbitrage on Cross-Exchange Price Gaps

At the same moment, for the same name, perp prices differ across exchanges. In June 2026 data, Binance’s Samsung Electronics perp traded 0.93% higher on average than Hyperliquid’s. SK Hynix showed a 1.03% gap, widening to as much as 2.3%.

Perp positions cannot move between exchanges. Instead, a trader opens opposite positions on both at once. Short on the higher-priced exchange, long on the lower, and the directional P&L offsets. As the two prices converge, the original gap remains as profit. On the higher side, the short also collects funding, adding return.

Later-entrant exchanges tend to hold higher prices because less arbitrage capital flows in. These gaps recur in the early phase as more exchanges launch. They widen further at night and on weekends, when spot is closed and each exchange discovers price on its own.

4. Market Shifts and Emerging Opportunities

One catch in this market is fragmentation, which is both a risk and an opportunity. As the same name scatters across Korea’s existing exchanges and Hyperliquid, Binance, and Lighter, liquidity splits. With price spread across venues, it is harder to agree on which is real, and differing prices create room for confusion and manipulation. Stack leverage on thin liquidity and liquidations can cascade. An opportunity, and a risk.

The openings above were for retail. The same structure also opens business opportunities.

Market makers: the same name trades 0.15% to 0.75% apart across exchanges, and the gap widens at night. In an early market with little arbitrage capital, spreads stay wide. With thin liquidity and several exchanges managing fragmented liquidity, market making demand should keep growing.

Regional oracles: perps discover price while spot is closed, and accuracy hinges on the oracle. A specialized oracle that feeds accurate prices for Asian-timezone assets such as Korea, Japan, and Taiwan is still an open space.

Tokenized issuance: listed Korean names today are limited to Samsung Electronics, SK Hynix, and Hyundai Motor. The market needs an intermediary to list and manage KOSPI 200 names and major Asian companies.

Basis hedge funds: perps convert the premium over spot into funding cash every hour. A dedicated fund collecting basis and funding gaps across exchanges turns capital faster than a conventional basis trade, though the market is still too small to absorb it.

The perp market is small against traditional markets, but it matters. It discovers price first, stays open 24 hours, and is institutionalizing fast. Opportunity remains on both the investment and business sides.

🐯 More from Tiger Research

Read more reports related to this research.Can Tokenized Pre-IPO Stocks Break Barriers in the Private Equity Market?

Tokenized Stock Market Map: How Tokenized Stock is Reshaping Global Finance

Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.