What if bridged assets could be put to work? Meet Katana, a chain that never sleeps. It maximizes capital efficiency by reinvesting 100% of on-chain, off-chain yield, and trading fees back into DeFi.

Key Takeaways

Most Layer 2s lock bridge assets without using them. Katana deploys these assets into Ethereum lending protocols to generate yield, then redistributes earnings as DeFi protocol incentives.

Holding assets in storage generates no return. Users must deploy capital into Katana DeFi protocols to earn additional rewards.

As of Q3 2025, over 95% of Katana’s TVL was actively deployed in DeFi protocols. This contrasts with most chains, where utilization rates range from 50% to 70%.

Katana reinvests 100% of net sequencer fee revenue into liquidity provision, maintaining stable trading conditions even during market volatility.

1. Why Capital Is Sitting Idle

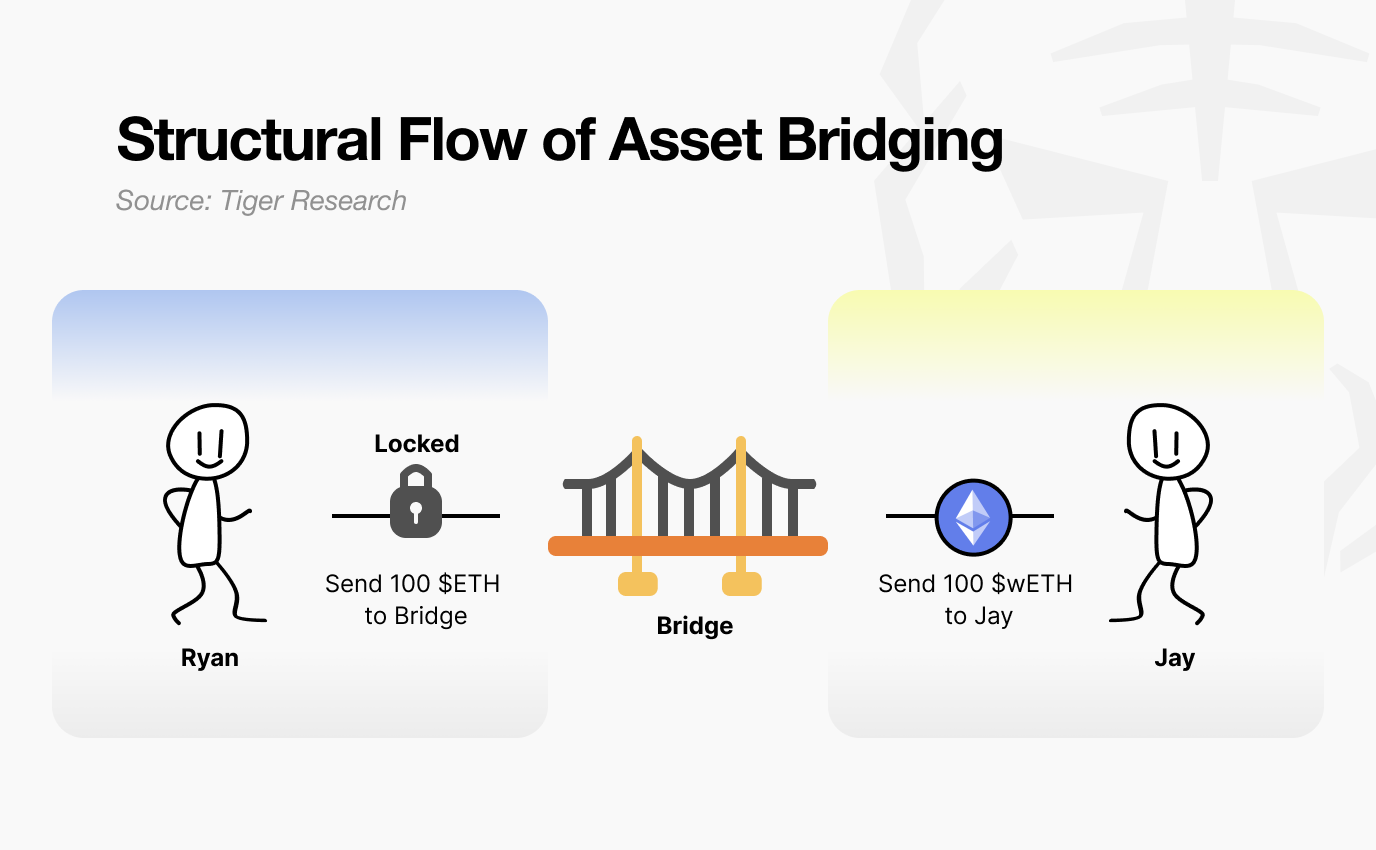

What happens to your money when you bridge from Ethereum to a Layer 2?

Most people assume their assets are simply transferred. In reality, the process is closer to freezing. When you deposit assets into a bridge contract, the contract holds them in escrow. The Layer 2 mints an equivalent amount of tokens. You can transact freely on Layer 2, but your original assets on mainnet remain locked and idle.

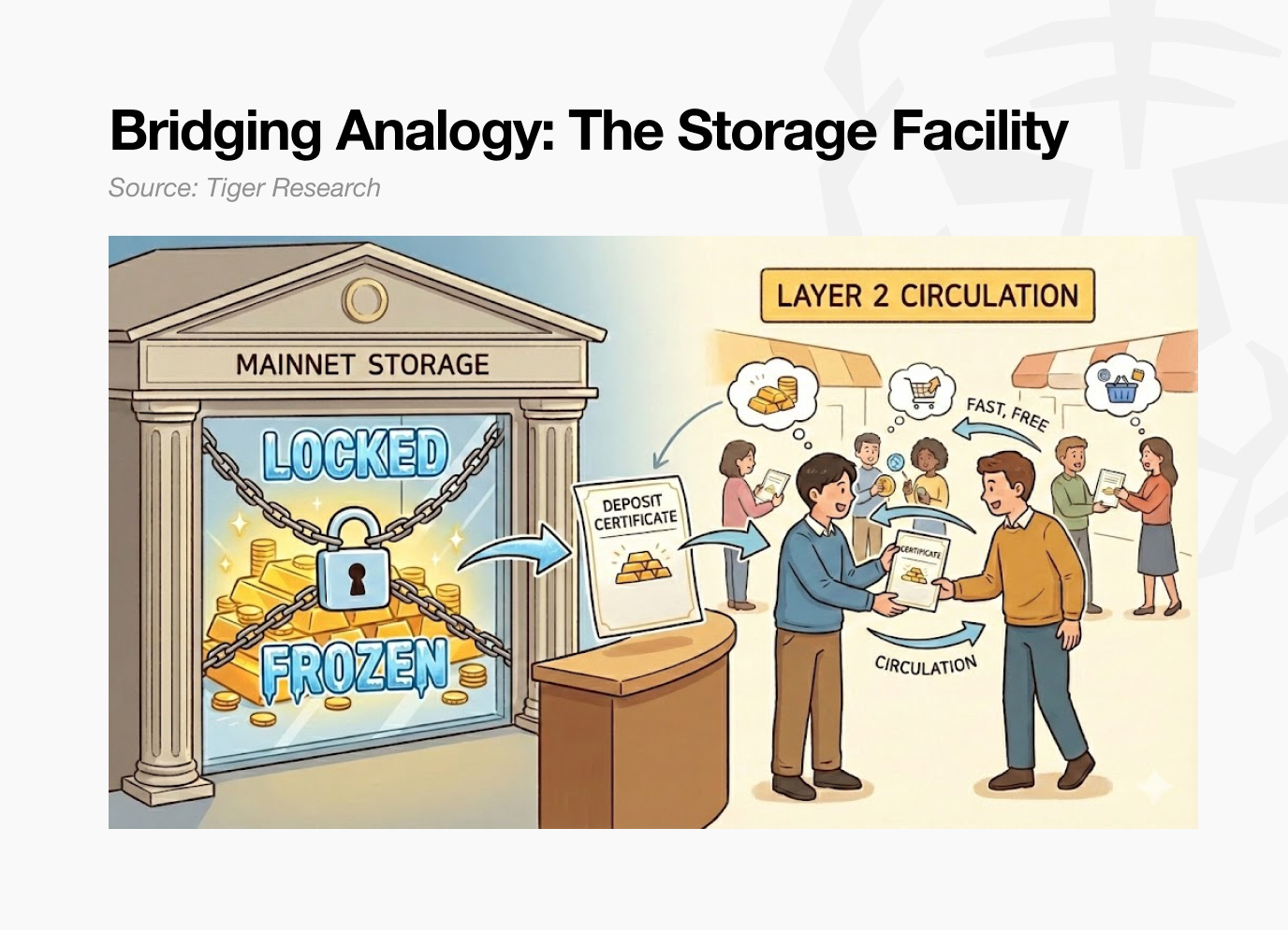

Consider a simple analogy. You deposit items at a storage facility and receive a claim ticket. The ticket can be transferred to others. But the items themselves stay in storage until you retrieve them.

This describes how most Layer 2 bridges work. Assets held in Ethereum escrow contracts generate no yield. They wait passively until users withdraw them back to mainnet.

What if bridge deposits on mainnet could earn DeFi yield while you still access fast, low-cost transactions on Layer 2?

Katana answers this question directly. Capital entering the bridge does not sit idle. It is put to work.

2. How Katana Puts Capital to Work

Katana activates capital through three mechanisms:

Bridge assets are deployed into Ethereum lending markets to generate yield.

Trading fee revenue is reinvested into liquidity pools.

Native stablecoin AUSD captures U.S. Treasury yields.

External capital works. Chain-generated capital works. These three mechanisms combine to eliminate idle assets on Katana.

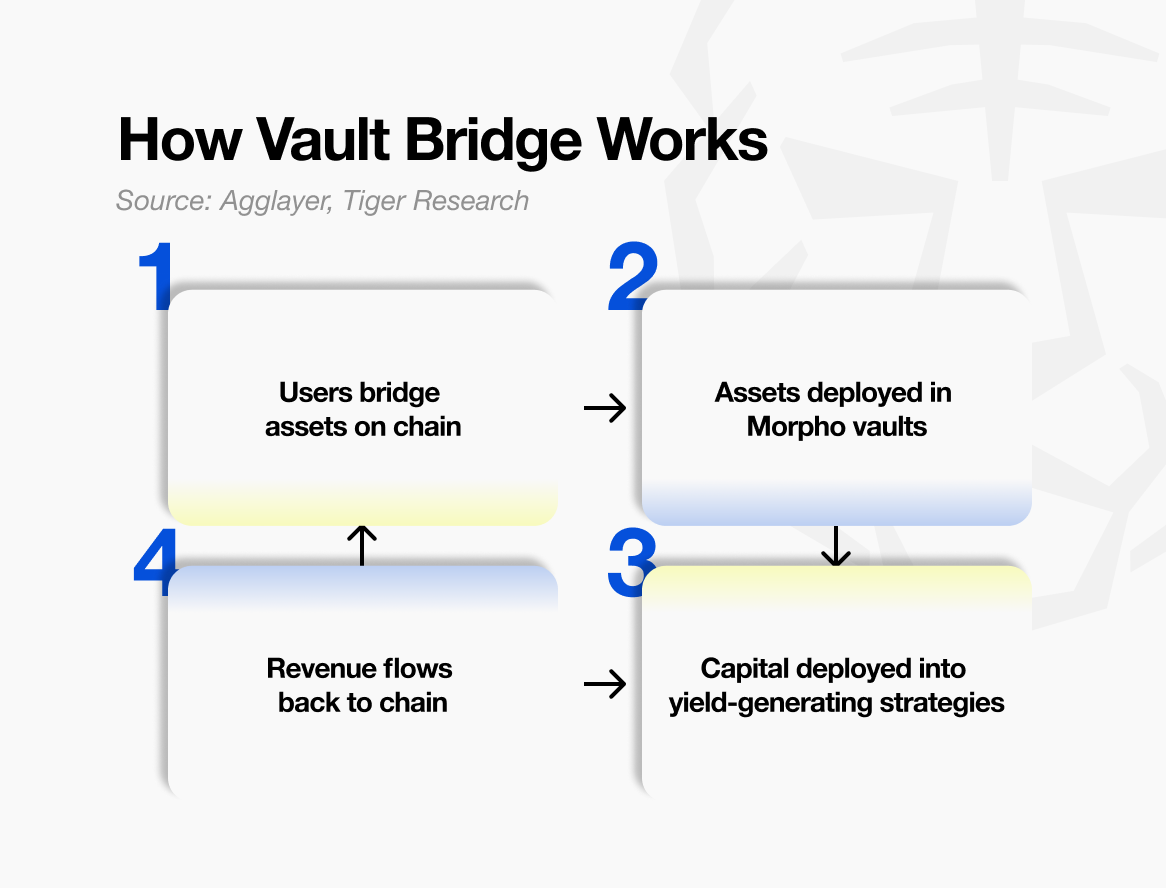

2.1. Vault Bridge

The first mechanism is Vault Bridge. When users send assets to Katana, the original assets remaining on Ethereum mainnet are deployed into lending markets to generate interest.

When you bridge USDC from Ethereum to Katana, those assets are not simply locked. On Ethereum mainnet, they are deployed into curated vault strategies on Morpho, a major lending protocol. The yield generated does not go directly to individual users. Instead, it is collected at the network level and redistributed as rewards to core DeFi markets on Katana.

On Katana, the user receives a corresponding vbToken, such as vbUSDC. This token can be freely used across Katana’s DeFi ecosystem.

One common misunderstanding should be addressed. vbTokens should not be compared to staking derivatives like stETH from Lido. stETH appreciates over time as staking rewards accrue.

vbTokens work differently. Holding vbUSDC in your wallet does not increase the quantity or price. The yield Vault Bridge generates on Ethereum does not flow to individual vbToken holders. It flows to Katana’s DeFi pools. Revenue is distributed periodically to the network, strengthening incentives for Sushi liquidity pools and Morpho lending markets.

Users benefit only when they actively deploy vbTokens. Supplying vbTokens to Sushi liquidity pools or to lending strategies such as those offered by Yearn allows users to earn base yield plus additional rewards sourced from Vault Bridge. Simply holding vbTokens provides no return.

Katana rewards asset utilization rather than passive ownership. Capital that moves is rewarded. Capital that remains idle is not.

2.2. Chain-Owned Liquidity (CoL)

The second mechanism is Chain-Owned Liquidity (CoL). Katana collects 100% of net sequencer fee revenue (transaction processing fees minus Ethereum settlement costs).

The foundation uses this revenue to become a direct liquidity provider. It supplies assets to Sushi trading pools and Morpho lending markets. The chain itself owns and manages this liquidity.

This creates a reinforcing cycle. As users transact on Katana, sequencer fees accumulate. Those fees are converted into chain-owned liquidity, which deepens pools. Slippage declines, lending rates stabilize, and user experience improves. Improved conditions attract more users, which generates additional fees. The cycle continues.

In theory, this structure is especially effective during market downturns. External liquidity is mobile and often exits quickly under stress. Chain-owned liquidity, by contrast, is designed to remain in place, allowing pools to persist and absorb shocks more effectively.

In practical terms, this sets Katana apart from most DeFi systems that rely on incentivizing external capital through token emissions. By maintaining liquidity it owns directly, the network aims for more stable and sustainable operation.

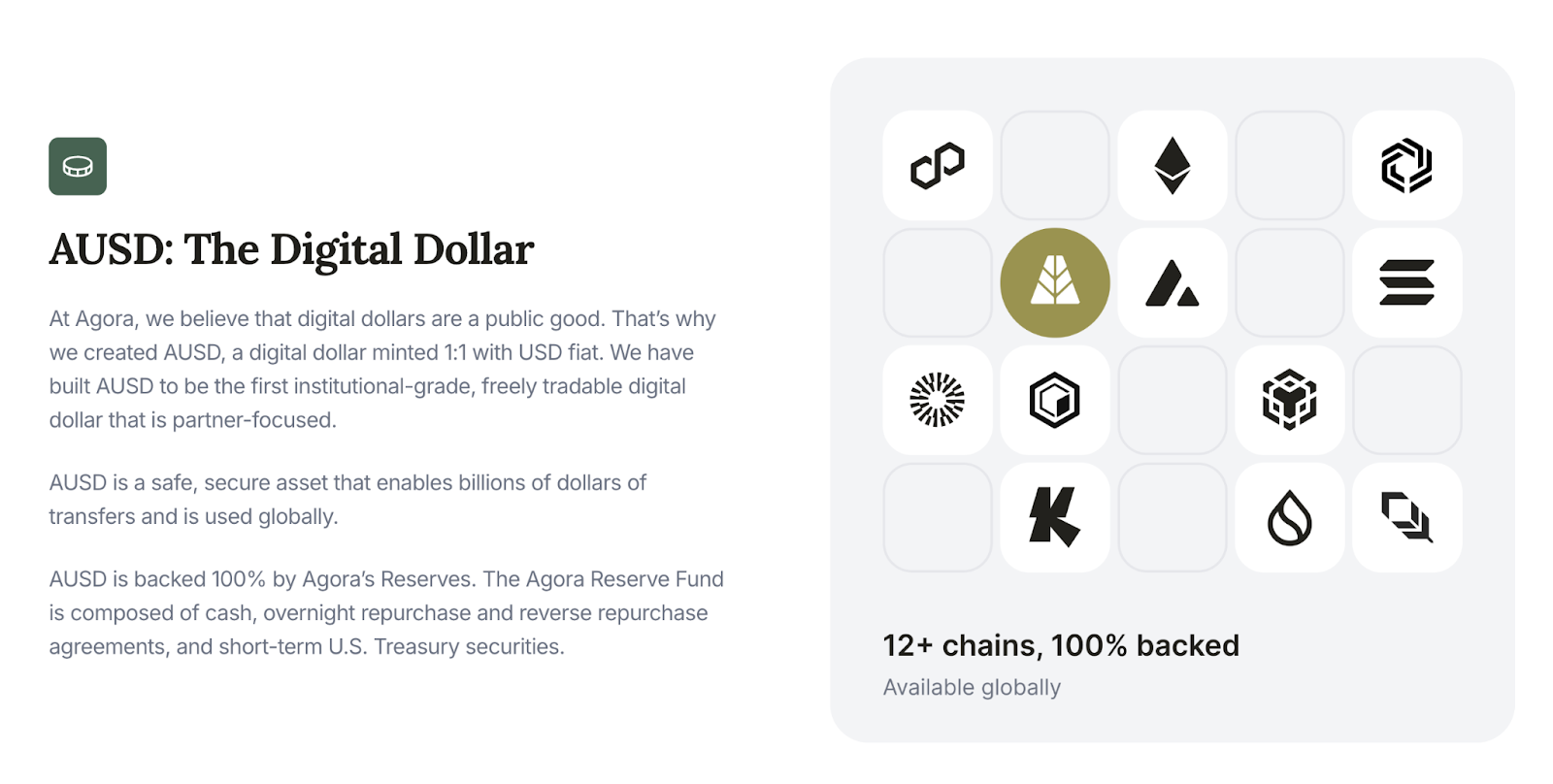

2.3. AUSD Treasury Yield

The third mechanism is AUSD, Katana’s native stablecoin. AUSD is backed by U.S. Treasuries, and the off-chain yield from these Treasury holdings flows into the Katana ecosystem.

AUSD is issued by Agora. The collateral backing AUSD is invested in physical U.S. Treasuries. Interest earned from these Treasuries accrues off-chain. This yield is periodically channeled to the Katana network, where it strengthens incentives for AUSD-denominated pools.

If Vault Bridge brings on-chain yield, AUSD brings off-chain yield. The two revenue sources differ in nature. Vault Bridge yield fluctuates with Ethereum DeFi market conditions. AUSD yield is tied to U.S. Treasury rates and remains relatively stable.

This diversifies Katana’s revenue structure. When on-chain markets are volatile, off-chain yield provides a buffer. When on-chain yields are low, Treasury returns support overall returns. The structure spans both crypto markets and traditional finance.

3. Locking Capital Versus Putting It to Work

As discussed earlier, there is a reason most existing bridges simply lock assets. Security. When assets do not move, system design remains simple and attack surfaces are limited. Most Layer 2 networks adopt this approach. It is safe, but capital remains idle.

Katana takes the opposite position. Activating idle assets introduces additional risk, and Katana acknowledges this tradeoff directly. Rather than avoiding it, the network works with established risk management specialists in DeFi. These include firms such as Gauntlet and Steakhouse Financial.

Gauntlet and Steakhouse Financial are established risk management firms in the DeFi sector, with experience setting parameters for major lending protocols and advising leading DeFi projects. Their role is comparable to that of professional asset managers in traditional finance. They assess which protocols capital should be allocated to, determine appropriate position sizes, and monitor risk exposure on an ongoing basis.

No financial system offers 100% safety, so concerns about residual risk are valid.

However, Katana works with top-tier risk curators and maintains conservative vault structures. An internal Risk Committee oversees operations. Additional safeguards include liquidity buffers provided by Cork Protocol and other protective mechanisms.

4. The DeFi Heaven Katana Creates

Current DeFi markets suffer from fragmented liquidity. Pools trading the same assets exist separately across chains and protocols. This reduces execution efficiency, increases slippage, and lowers capital utilization. Some users exploit these inefficiencies through arbitrage. Most users simply pay higher costs.

Katana solves this problem at the system level.

Vault Bridge and chain-owned liquidity concentrate liquidity in core protocols. As a result, trade execution improves, slippage declines, and lending rates stabilize. Most importantly, yield from idle assets on Ethereum mainnet is added to base returns, raising overall yield.

Katana’s incentive structure can also significantly lower effective borrowing costs at certain points, or even create negative interest rates depending on market conditions and reward programs. This happens because Vault Bridge, CoL, and AUSD yields are reinvested into core markets. However, these are incentive-driven outcomes that vary with market conditions.

As a result, as of Q3 2025, over 95% of Katana’s TVL was actively deployed in DeFi protocols. This contrasts with most chains, where utilization rates range from 50% to 70%. Ultimately, what Katana creates is a chain where capital does not sleep, a system that rewards actual usage.

Katana never sleep.

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report was partially funded by Katana. It was independently produced by our researchers using credible sources. The findings, recommendations, and opinions are based on information available at publication time and may change without notice. We disclaim liability for any losses from using this report or its contents and do not warrant its accuracy or completeness. The information may differ from others’ views. This report is for informational purposes only and is not legal, business, investment, or tax advice. References to securities or digital assets are for illustration only, not investment advice or offers. This material is not intended for investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo following brand guideline. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.