The AI industry continues its upward trajectory with no sign of cooling. The blockchain AI sector tells a different story. Why has it failed to attract comparable attention?

Key Takeaways

Amid the AI boom, the blockchain industry needs to be evaluated from a demand-side perspective: what problems does it solve that incumbent systems cannot, and what distinct capabilities does it bring to bear?

Decentralized computing and storage carry legitimate rationales around data sovereignty and cost competitiveness. The barrier is that neither has yet demonstrated a technical advantage compelling enough to justify the switching risk for buyers already committed to existing cloud infrastructure.

Model verification and privacy technology do not address problems that enterprises feel urgently enough to act on voluntarily. Demand in this category is more likely to follow regulatory mandates than to precede them. The EU AI Act illustrates the pattern: standards come first, and market adoption follows.

In the agent framework category, the constraint is not technological. Mainstream enterprises remain focused on internal workflow automation, while blockchain projects are already building the infrastructure layer that comes after. Demand needs time to reach the technology.

Agent payments is the one area where blockchain and traditional finance stand on equal footing. Neither has solved the problem yet, making this the only category in which both sides are confronting the same challenge at the same moment.

The blockchain AI sector as a whole is not struggling because the combination is incoherent. It is struggling because of a mismatch: each of the four categories faces its own distinct reason why demand has not yet materialized, and only agent payments is currently in a position to compete.

1. Blockchain Projects Left Behind in the AI Boom

The AI industry is experiencing an unprecedented concentration of capital and infrastructure investment. Large language model ecosystems led by major technology companies have become a standard feature of both daily life and industrial operations. Within this rapid expansion, the crypto industry has also been evolving quickly, seeking points of technical connection with AI.

Early efforts centered on supplementing or replicating segments of the traditional AI value chain: decentralized GPU supply, data ownership recovery, and cryptographic verification. More recently, the focus has shifted toward filling gaps that centralized architectures struggle to address, including autonomous on-chain activity by AI agents and real-time machine-to-machine settlement.

Describing this space generically as “AI plus blockchain” obscures more than it reveals. A rigorous demand-side analysis is needed: which problems does each sub-sector target, and does the blockchain-native approach offer a genuinely differentiated solution?

2. What Each Category Does

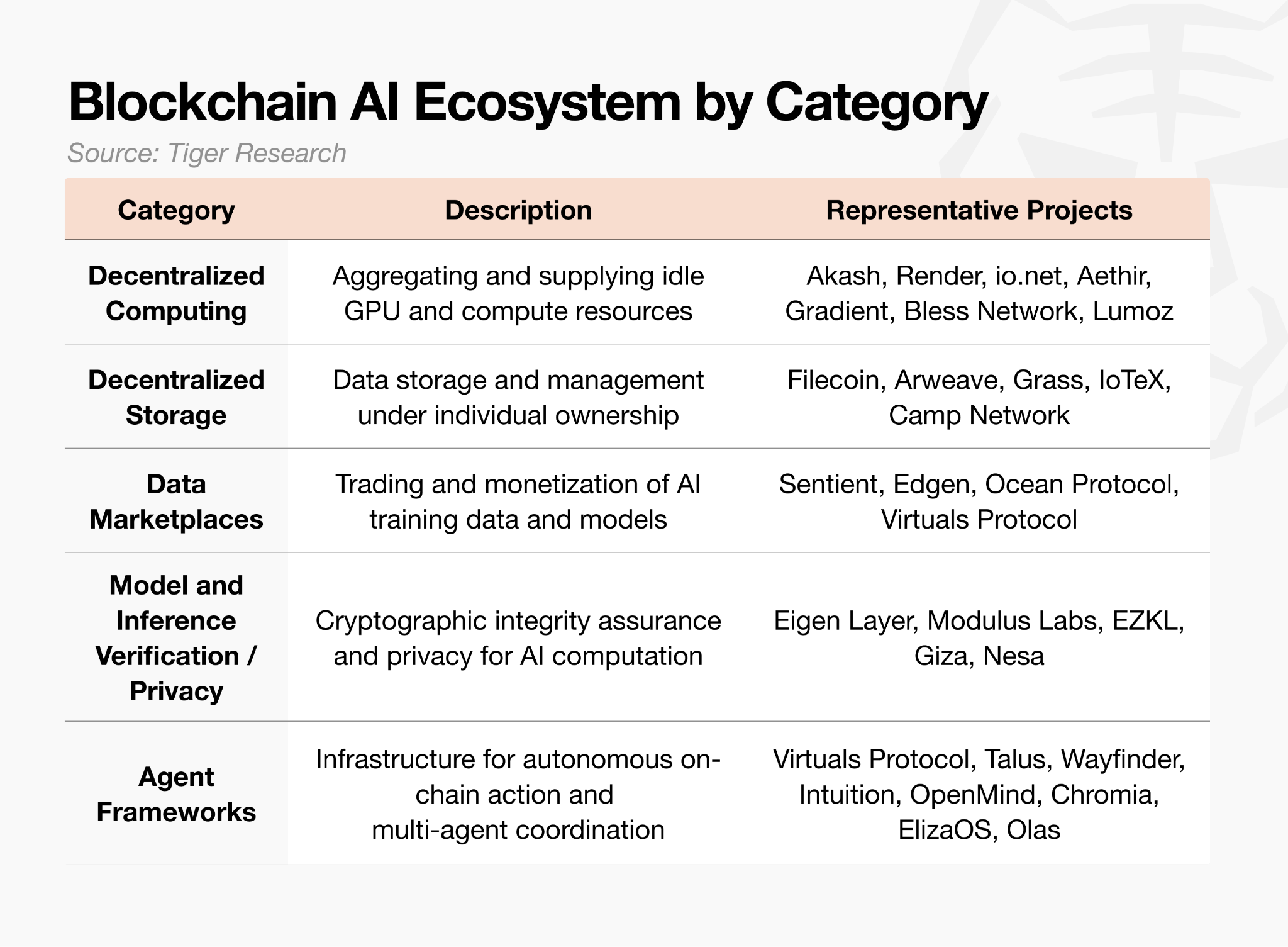

2.1. Decentralized Computing

The cloud market today is structurally dependent on a small number of major technology companies that control compute resources. High-performance GPUs are both difficult to procure and prohibitively expensive, creating a steep entry barrier for AI startups and research teams that cannot access large-scale infrastructure.

Centralized systems concentrate resources toward the largest buyers, and there is no neutral channel for redistributing the substantial volume of idle GPU capacity that exists across the market.

Decentralized computing addresses this concentration and inefficiency through two approaches. Under a shared-economy model, projects aggregate idle GPU resources held by individuals and small data centers into a unified network, creating a more flexible supply chain outside the incumbent technology monopoly.

Under a distributed computing model, users can access and lease compute resources globally without dependence on any single provider’s infrastructure, raising utilization of dormant hardware and lowering the entry threshold for high-performance compute.

2.2. Decentralized Storage

Current data storage architecture is almost entirely dependent on centralized cloud infrastructure operated by companies such as Google and Meta. When users upload data to these platforms, ownership effectively transfers to the platform, entrenching monopoly control over AI training data. Centralized infrastructure also introduces operational risk: policy changes, service disruptions, or platform failures can cut off data access or result in data loss.

Decentralized storage addresses these structural problems through two approaches. A shared-economy model, exemplified by Filecoin and Arweave, pools idle storage space across individual participants into a network capable of substituting for incumbent centralized cloud.

A permanent storage model replicates data across distributed nodes, ensuring persistence regardless of the operational status of any individual server and reducing dependence on any single platform.

2.3. Data Marketplaces

AI developers require training data, but the current data distribution market operates as a closed system in which large platforms such as Hugging Face and cloud vendors capture the economics and control pricing. Data creators receive little compensation, and the mechanisms for rewarding data collection and contribution lack transparency.

On-chain marketplaces eliminate intermediaries through smart contracts and establish transparent transaction terms. In a direct-trading model such as Ocean Protocol, data owners and AI developers transact directly through smart contracts, with compensation distributed transparently. In a contribution-reward model such as Grass, individuals connect idle bandwidth to AI data collection and receive compensation proportionate to the value of their contribution.

2.4. Model and Inference Verification / Privacy

Conventional AI systems operate as black boxes, providing no external means to verify that a model ran correctly or that sensitive user data was handled securely.

Zero-knowledge machine learning (ZKML) introduces a cryptographic verification layer into AI inference, enabling both privacy protection and auditability. In this architecture, models run off-chain in the conventional manner, but the computation generates a cryptographic proof that the process was executed correctly according to defined rules.

This proof is recorded on-chain rather than the underlying data. To illustrate: in an automated medical insurance reimbursement service, a hospital would submit only a proof that the AI model ran correctly, rather than sharing the full medical record. The insurer can verify the legitimacy of the claim without accessing the original data.

2.5. AI Agent Frameworks

As AI agents become the primary locus of traffic and value creation, they are evolving from tools into autonomous economic actors. The existing financial system was designed around human consumption patterns and is structurally incompatible with a machine-centric payment environment.

The agent economy requires microtransactions, high-frequency settlement, and cross-border payments executed at millisecond speeds, and incumbent financial infrastructure cannot accommodate this.

On-chain agent infrastructure addresses this through two mechanisms. An autonomous execution and control mechanism assigns unique wallets and identities to AI agents, enabling them to sign transactions directly, with configurable spending limits and safeguards to prevent unintended behavior.

A protocol-based settlement mechanism uses stablecoin payment protocols such as x402 to settle microtransactions and high-frequency payments in real time, bypassing currency conversion and approval workflows.

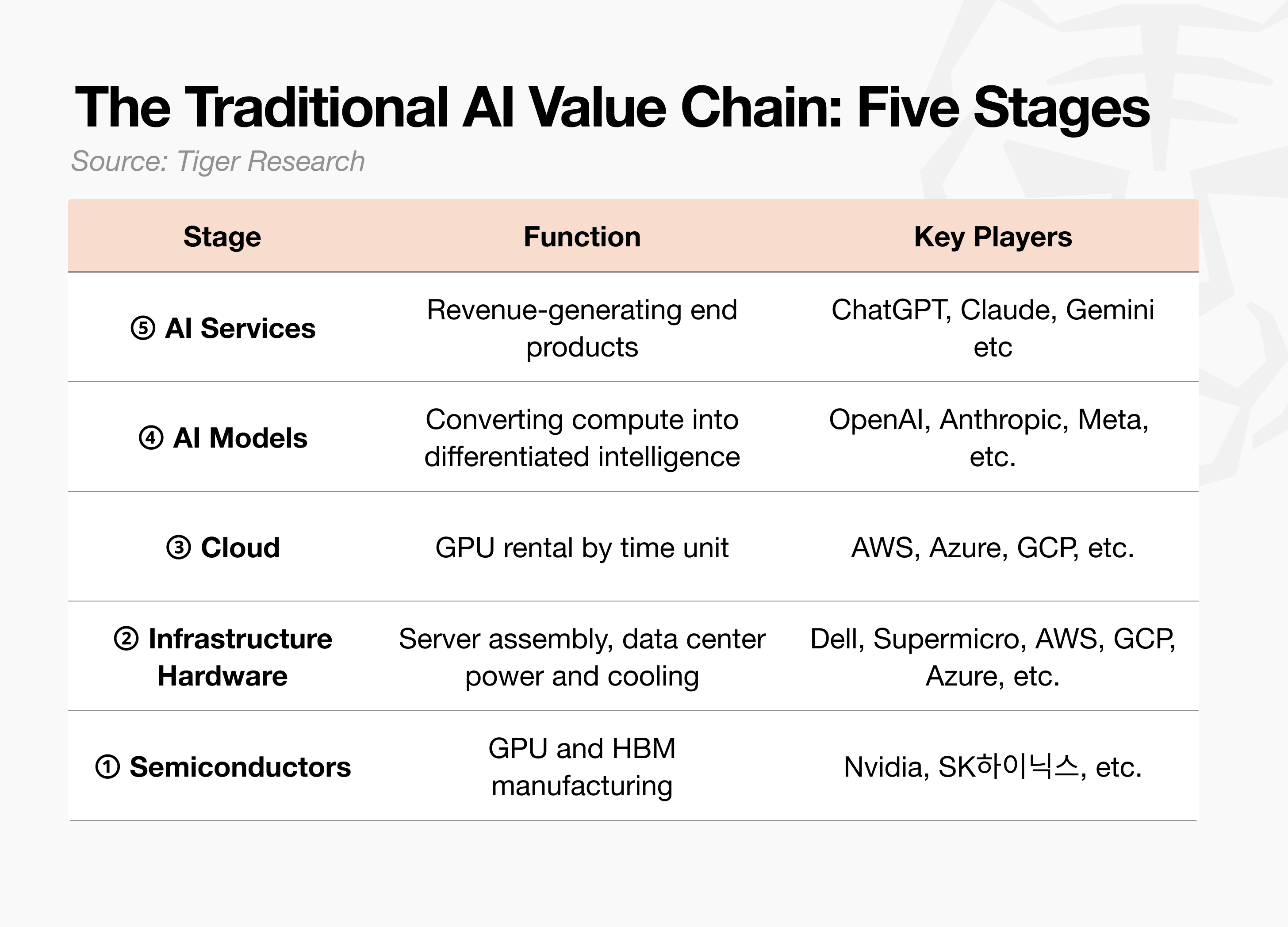

3. Where Blockchain AI Diverges from the AI Value Chain

The AI value chain has formed around the sequential removal of bottlenecks. As AI demand grows, memory shortages emerge, and power and data transmission capacity come under strain. Companies that solve these problems quickly, such as HBM manufacturers and power infrastructure providers, attract enormous capital and substantial market appreciation. The market assigns clear value to solutions that remove barriers to growth.

Blockchain AI projects have identified real problems, yet they have not captured anything like the same level of market interest. If these problems were as urgent as claimed, they would already have driven measurable shifts in the market.

The reason blockchain AI projects cannot attract mainstream capital despite advancing legitimate goals such as reducing GPU concentration and restoring data sovereignty is a pronounced gap between the priorities of the technology suppliers and those of the buyers who control capital allocation.

The AI industry moves on a competitive timeline, and buyers, primarily large technology companies and enterprise clients, invest at scale in whatever resolves their immediate operational bottlenecks most quickly. They do not spend time evaluating unproven infrastructure. Their priorities are computational performance, infrastructure reliability, and demonstrable return on investment.

To illustrate: when data transmission speeds became a bottleneck during model training, substantial capital moved into fiber optic infrastructure as a replacement for copper. When memory bandwidth emerged as the primary constraint, buyers identified it as the critical problem, and SK Hynix and Samsung Electronics gained global prominence by solving it with high-bandwidth memory. The pattern is consistent: capital follows whoever removes the constraint that is actively limiting progress.

The underlying problem for blockchain AI is one of framing. Buyers with large capital budgets are focused exclusively on near-term performance gains and cost reduction. Blockchain AI, by contrast, has concentrated on problems that buyers regard as secondary or future-state concerns.

The technical ambitions of the supply side do not align with the immediate operational requirements of the demand side.

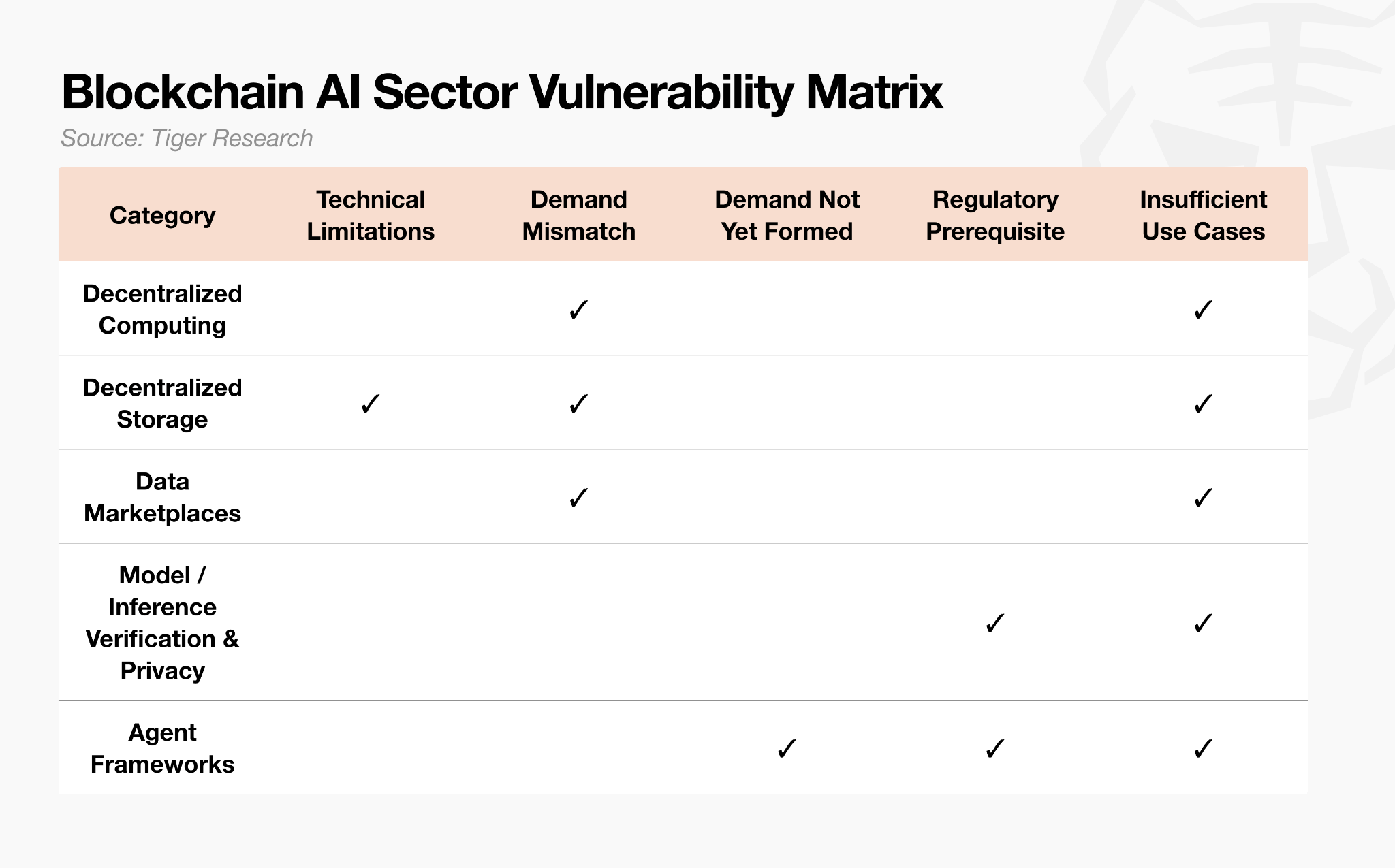

3.1. Technical Limitations

Several projects have used benchmarks to demonstrate the potential and design philosophy of decentralized infrastructure. The more fundamental problem is that this work has not yet produced a technical leap decisive enough to displace entrenched incumbents in the mainstream market.

For a new technology to take share from centralized cloud providers such as AWS or GCP, which already command massive capital and infrastructure, it must deliver a performance advantage so substantial that the gap with incumbents becomes irrelevant.

When Apple transitioned from Intel to M1 chips, absorbing the significant risk of breaking software compatibility, the move was justified by a threefold improvement in power efficiency, a gap large enough to make the transition worthwhile.

Blockchain AI has not yet offered enterprise buyers, who require petabyte-scale data synchronization and ultra-low latency as baseline conditions, a sufficiently clear case to accept the switching risk.

3.2. Demand Mismatch

In decentralized computing, some projects have introduced service level agreements as a risk mitigation mechanism, yet enterprise buyers remain unpersuaded. The reason is structural rather than contractual. Major cloud providers supply controlled, dedicated data centers. Blockchain networks rely on fragmented, anonymous node participation.

If a node drops out and interrupts a model training run worth hundreds of millions of won, no combination of token refunds or financial compensation can recover the opportunity cost and time lost. For enterprise buyers operating on competitive timelines, system stability is not a negotiable parameter.

Even with hedging mechanisms in place, the residual uncertainty is not a risk most buyers have any incentive to absorb.

3.3. Demand Not Yet Formed

Blockchain agent frameworks are designed for sophisticated ecosystems in which multiple AI agents collaborate autonomously, but there is a maturity gap between that vision and the current state of the mainstream market.

Enterprise adoption of AI agents is accelerating, led by companies such as Microsoft and Salesforce, but the current focus is firmly on workflow automation operating within controlled internal networks. The infrastructure that blockchain projects are building addresses the stage that follows: independent AI agents operating autonomously across external networks beyond any organization’s perimeter. Most enterprises today are still focused on establishing the stability and return on investment of the AI systems they have already deployed. Multi-agent collaboration across external networks is not yet a priority on enterprise infrastructure roadmaps.

The limited demand at this stage reflects timing rather than technical failure. This is better understood as a long-range infrastructure investment in anticipation of the agent economy, rather than a near-term revenue opportunity.

3.4. Regulatory Prerequisite

Zero-knowledge proofs and privacy-preserving technology represent core solutions for establishing AI trustworthiness, but practical enterprise demand for privacy infrastructure has been limited in the early stages of AI adoption. Voluntary adoption by enterprises is unlikely to drive meaningful uptake; the more probable path is that regulatory standards create the demand that the technology is then positioned to meet.

The growing specificity of global regulatory frameworks, including the EU AI Act, is a favorable development in this respect. As legal requirements around data provenance and security become concrete, blockchain’s advanced verification capabilities stand to become a compliance requirement rather than an optional feature in enterprise deployments.

Regulatory development in this space is better understood as a catalyst for market formation than as a constraint. Clear regulatory standards reduce market uncertainty, and in doing so, create a stable path through which blockchain AI can establish mainstream demand within an institutional framework.

3.5. Insufficient Use Cases

These structural factors combine to produce a more fundamental problem: the absence of a defining success case that demonstrates value at scale. The traditional AI industry built its current position through the adoption flywheel that ChatGPT initiated, using a concrete, widely visible product to attract the capital and talent necessary to sustain further growth.

Blockchain AI projects have not yet produced comparable evidence of product-market fit at scale. Beyond early community enthusiasm, none has demonstrated adoption at the level of enterprise operations or consumer daily life in a way that commands serious attention from mainstream capital. The absence of a compelling reference case remains the most significant barrier to attracting the conservative institutional investment that would accelerate broader adoption.

4. Does the Combination Have Value?

Blockchain AI has not yet found stable footing in the mainstream AI value chain, independent of market expectations. Does that mean the combination is without merit?

It does not.

The fundamental reason blockchain AI projects are currently overlooked is not that the combination is internally contradictory. It is that a mismatch exists in each sub-category between what incumbent industry requires and what the technology is oriented toward delivering.

The priorities of the traditional AI industry are clear: near-term performance, cost optimization, and rigorous infrastructure reliability. Many current blockchain AI proposals, by contrast, are centered on data ownership, computational transparency, and decentralization.

These are not problems that established industry participants treat as immediate bottlenecks, and pursuing them often requires accepting performance overhead that is too costly relative to the benefit.

Before the AI boom, power infrastructure companies were broadly classified as mature, slow-growth businesses. The data-center-driven surge in power demand changed that, and they have since attracted significant market attention. The current indifference to blockchain AI may reflect a similar lag, the period just before a new paradigm creates the conditions that reveal the value of the infrastructure being built ahead of it.

What matters during this transitional period is how the sector responds to what the market actually requires.

The path forward divides into two directions: adapting actively to the standards of the established AI value chain and closing the near-term performance gaps, or holding to present capabilities while continuing to build the infrastructure that a future generation of AI deployment will need.

The outcome will depend on which of those choices proves more aligned with where demand goes next.

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.