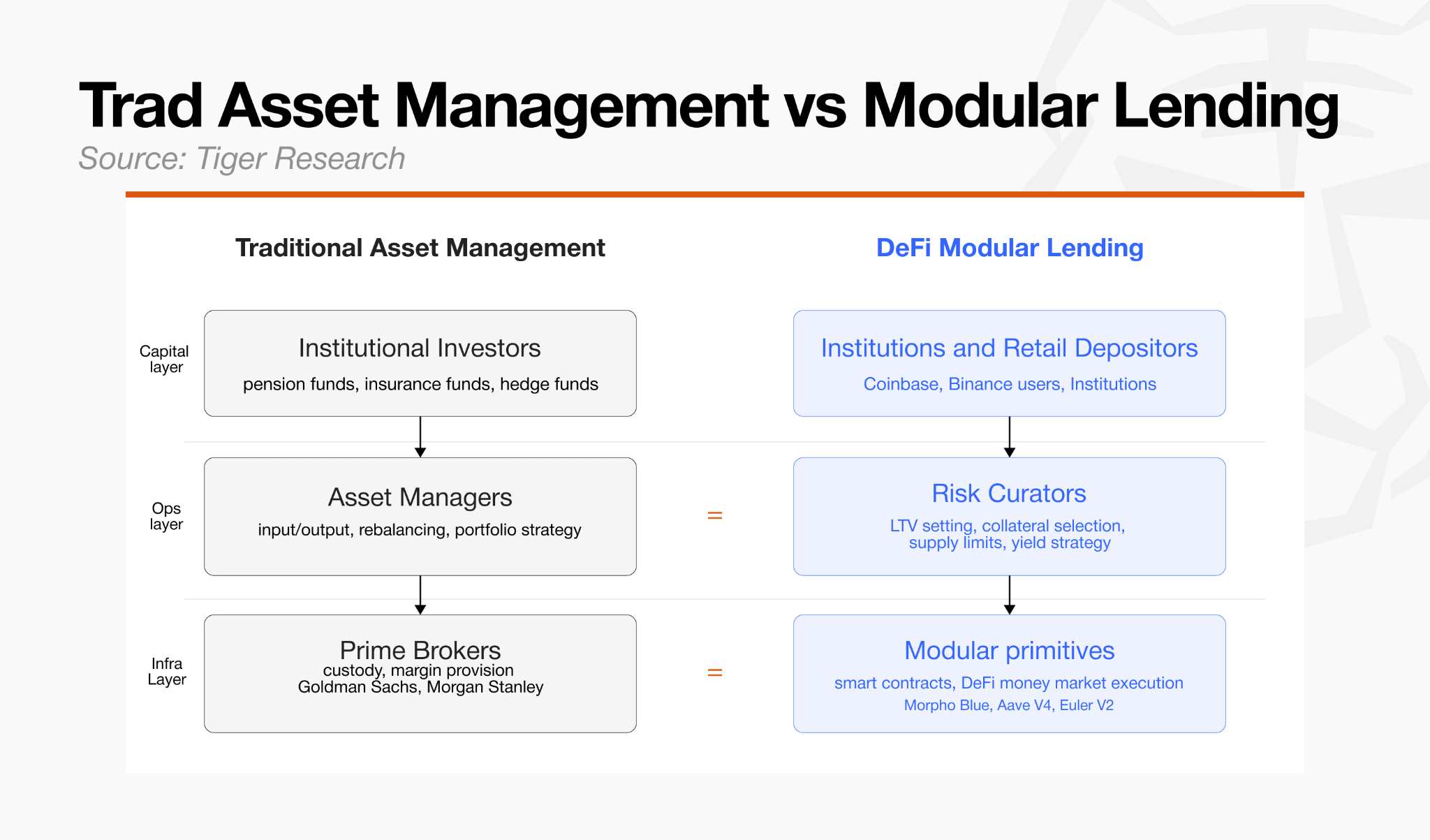

As institutional investors enter the onchain lending market, DeFi is moving away from single shared-pool architecture toward structures that isolate risk and specialize the operational layer.

Key Takeaways

The Lehman crisis and the Kelp DAO incident both exposed the same structural flaw: a single shared-pool architecture amplifies the failure of one asset into a system-wide crisis.

TradFi responded by separating each functional layer of the financial stack.

The DeFi ecosystem is converging on the same answer, a modular architecture built around risk isolation.

The shift has accelerated as RWA assets begin flowing onchain.

In a modular architecture, the capability of the operational layer, the layer that actually manages the products, becomes the critical differentiating factor.

1. The Lesson of the Lehman Crisis

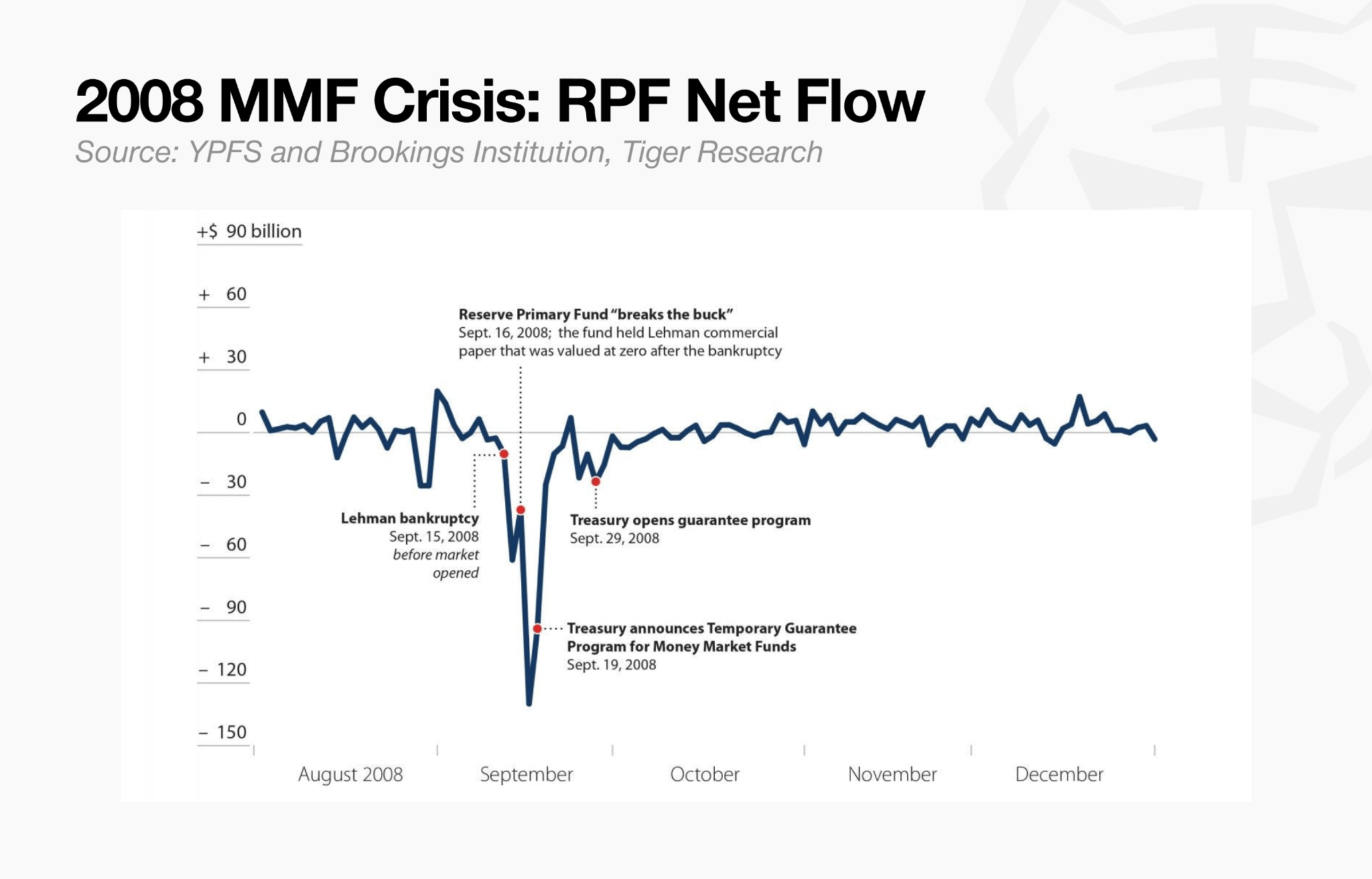

In September 2008, the collapse of Lehman Brothers triggered a crisis without precedent, Reserve Primary Fund (RPF), the world’s third-largest money market fund, suspended all redemptions within a single day.

At the time, RPF’s exposure to Lehman Brothers debt amounted to just 1.2% of assets under management. When Lehman’s bankruptcy rendered that 1.2% unrecoverable, the fund’s total asset value fell from 100 cents on the dollar to 98.8 cents. That was enough to break the MMF industry’s foundational principle of maintaining a fixed one-dollar net asset value per share. The fund’s per-share value fell below one dollar to $0.97.

Once principal loss became visible, panic spread almost immediately. The fear that waiting would mean further losses drove a bank run of historic scale, with $40 billion in redemption requests arriving within two days. Unable to absorb the pressure, the fund froze and halted all withdrawals.

The Lehman episode forced a comprehensive restructuring of traditional capital markets. In the MMF sector, risk-tiered liquidity buffers and redemption restriction guidelines were overhauled. In the hedge fund sector, the industry absorbed the lessons of Lehman’s rehypothecation risk, where a single prime broker had concentrated custody over client assets.

The result was a structural shift away from concentrating assets and credit with a single intermediary. Separating execution infrastructure from risk management, and distributing exposure across multiple prime brokers, became the global standard for risk isolation. Built on that institutional safeguard of separating infrastructure from risk to contain contagion, the asset management industry was able to rebuild operational trust and resume its growth.

2. How Traditional Capital Markets Solved This Problem

In 2014, the U.S. Securities and Exchange Commission restructured the MMF framework. Funds were segmented by the nature of their capital, with different standards applied to each category. The purpose was to prevent a bank run or failure in one segment from spreading to other fund types or to the system as a whole, with each category carrying its own dedicated buffer.

The core philosophy behind traditional finance’s approach to risk control is separation. Authority is divided so that risk does not concentrate in a single point, and independent verification is inserted at each stage of the capital flow.

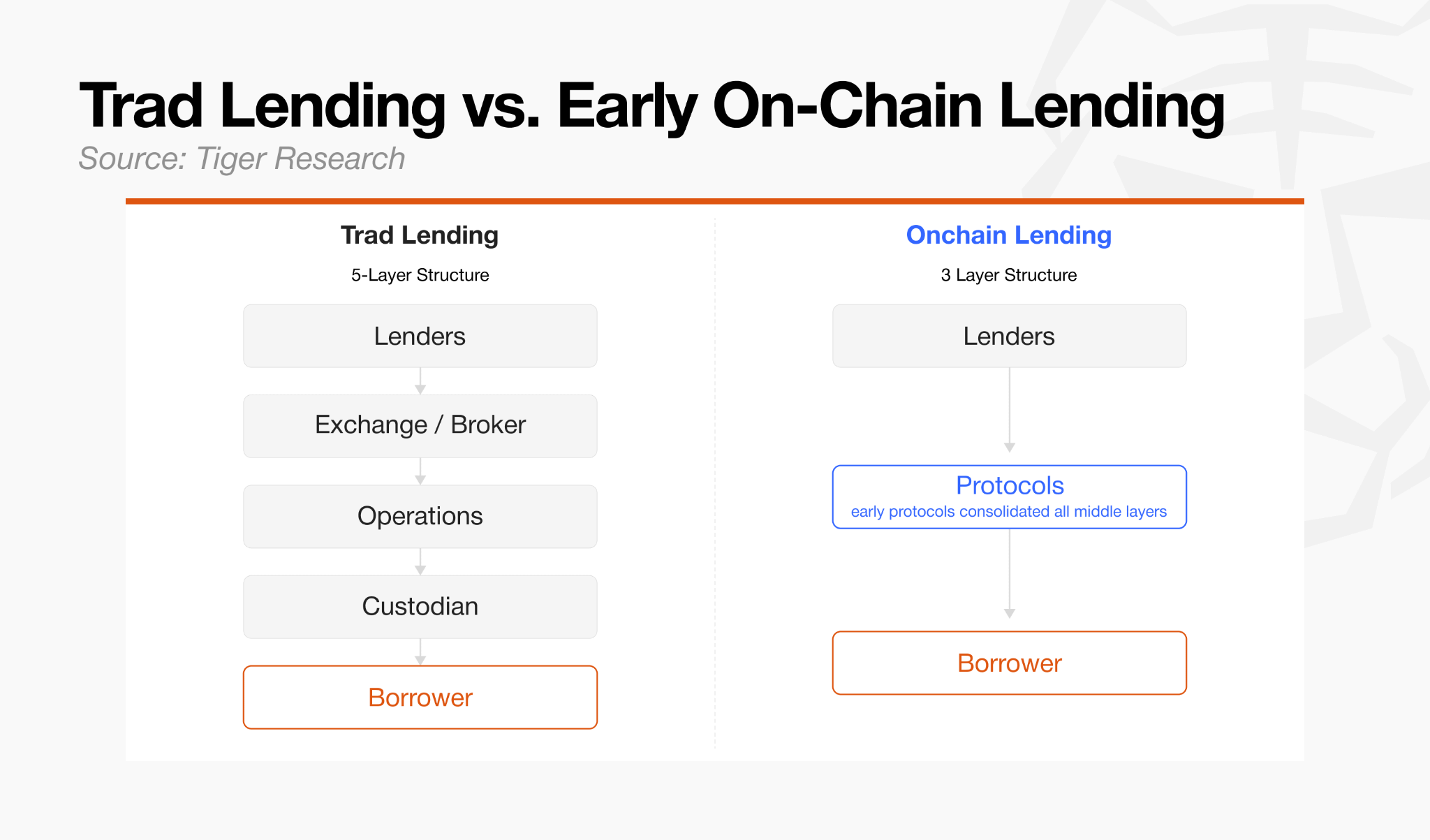

Prime brokerage in capital markets is the clearest illustration of this principle. Investment authority sits with the hedge fund; risk oversight sits with the broker. The two functions are deliberately kept apart. In traditional lending markets, the same logic took hold: credit assessment, underwriting, collateral management, and custody each became the domain of distinct, independent actors.

When asset management and lending began migrating to DeFi, however, the layered intermediary structure that traditional finance had built was compressed into a single layer. Early DeFi protocols focused on eliminating the intermediaries that the separated structure required, encoding the relevant mechanisms directly into smart contracts and automating what had previously been handled by multiple parties.

3. From Shared Pools to Modular Architecture

Early DeFi’s approach of compressing all lending mechanics into a single smart contract reduced intermediary costs, but concentrated every category of risk within a single protocol. Because credit assessment, underwriting, and collateral management operated inside one codebase rather than as separate functions, the failure of a single asset or a liquidation breakdown could directly paralyze liquidity across the entire system.

This potential for contagion forced protocol governance bodies to set risk parameters conservatively. Assets with shorter track records or higher volatility, anything beyond Bitcoin and Ethereum, were structurally excluded from collateral eligibility. The compression of functions into a single contract produced the opposite of capital efficiency: limited asset diversity and constrained market access.

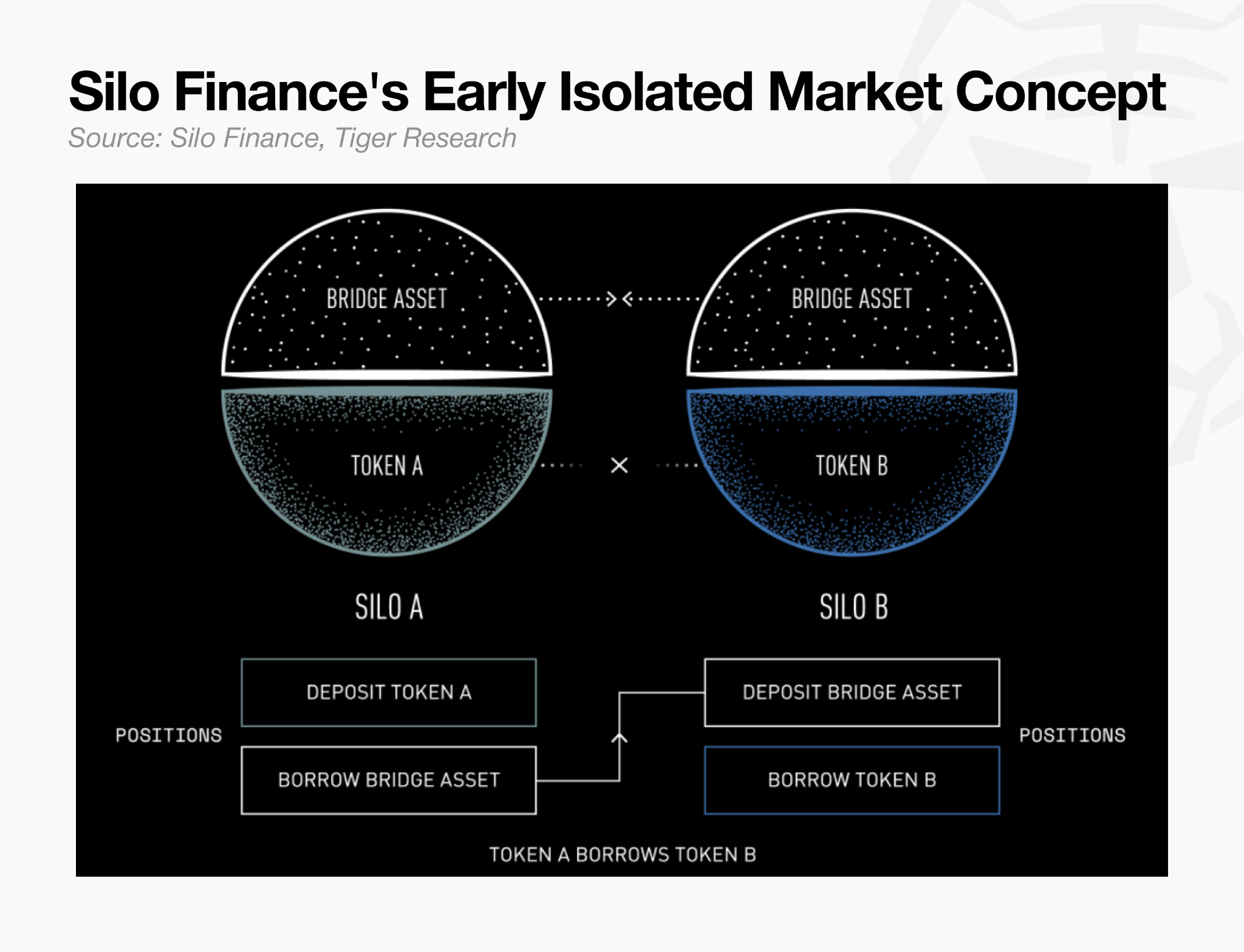

Silo Finance addressed the risk concentration problem of the unified pool by introducing isolated lending pools for each asset. By containing price manipulation or sharp value declines within a single collateral pool and preventing that risk from spreading to others, Silo demonstrated that governance approval thresholds could be lowered and new lending markets opened more rapidly. The architecture showed that a single large pool could be broken apart and risk isolated at the market level, and it pointed toward the layered modular structures that followed.

The modular system that Silo pioneered became a foundational standard for onchain lending as RWA assets, including tokenized Treasuries and private credit, began flowing onchain in volume. Each category of RWA differs fundamentally across trading hours, oracle reliability, regulatory requirements such as KYC and AML, and liquidation procedures. Managing assets this varied under a single unified parameter set, as the early shared-pool model required, is not viable.

The influx of RWA created a demand that went beyond simply isolating assets from one another. It required transplanting the kind of sophisticated risk control frameworks found in traditional finance onto the onchain environment. As assets diversified, the risks emerging onchain grew more complex. Containing those risks required a structural separation between an immutable infrastructure layer handling liquidation and settlement, and an operational layer with real-time authority to adjust and take responsibility for risk parameters.

Early DeFi began by compressing the middle layers of finance into a single codebase. As RWA assets flowed in and the lending market matured, the path taken was different: liquidation and settlement efficiency was delegated to the blockchain, while risk oversight authority was separated into an independent layer. In absorbing greater asset complexity, onchain lending arrived at an architecture that resembles the structures traditional finance had already built, prime brokerage and independent credit assessment, where investment and risk surveillance are kept apart. That modular architecture has become the new standard for onchain lending markets.

4. Institutional-Grade Risk Isolation and Convergence

Although modular architecture emerged from within the DeFi ecosystem itself, it converged precisely with the risk control standards that institutional participants required.

Morpho’s decision to prioritize complete risk isolation at the base infrastructure layer, at some cost to capital efficiency, generated institutional demand. That demand became the inflection point that drew other major lending protocols, those that had started with shared-pool structures, toward the same direction.

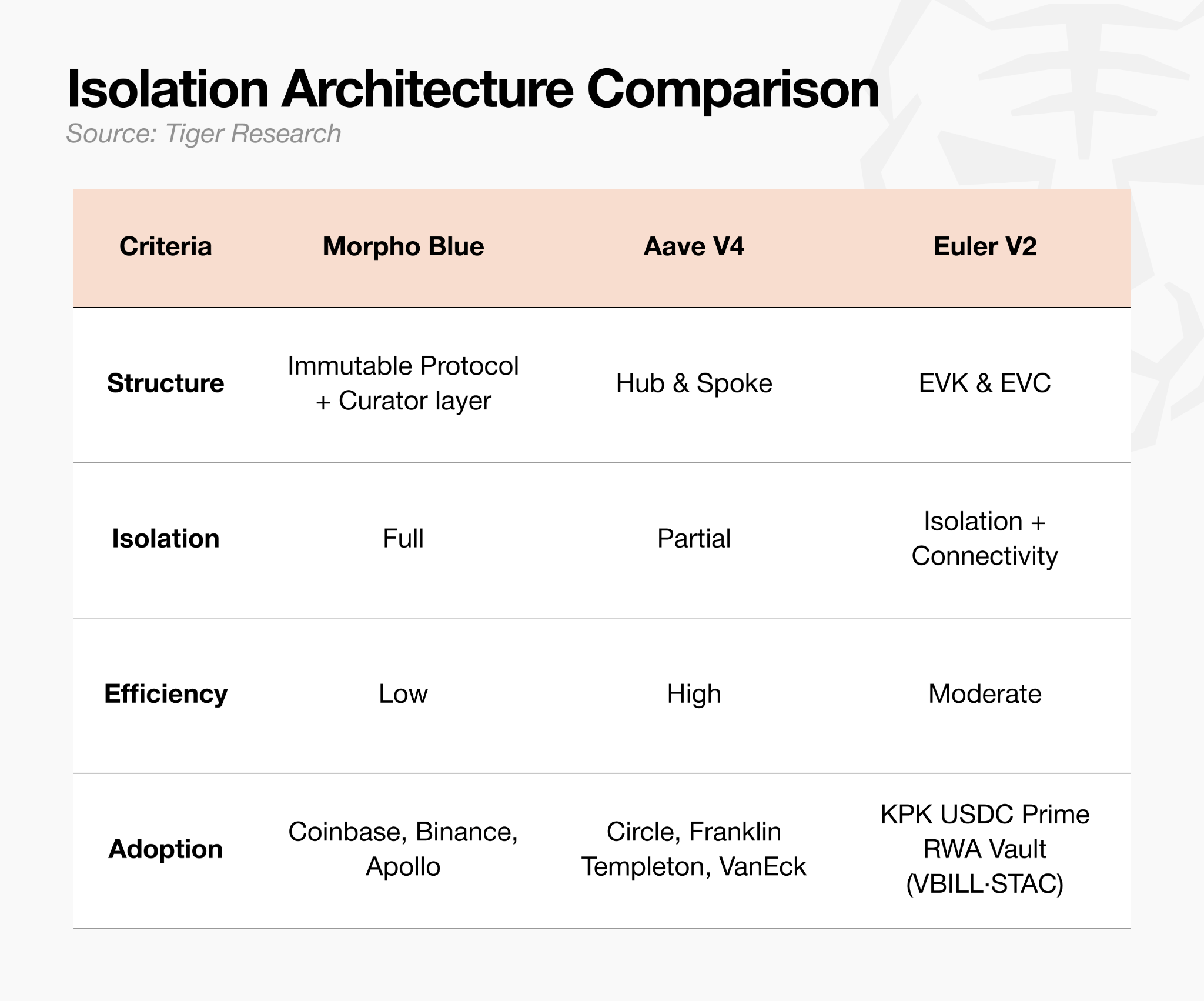

4.1. Morpho Blue: Prime Brokerage

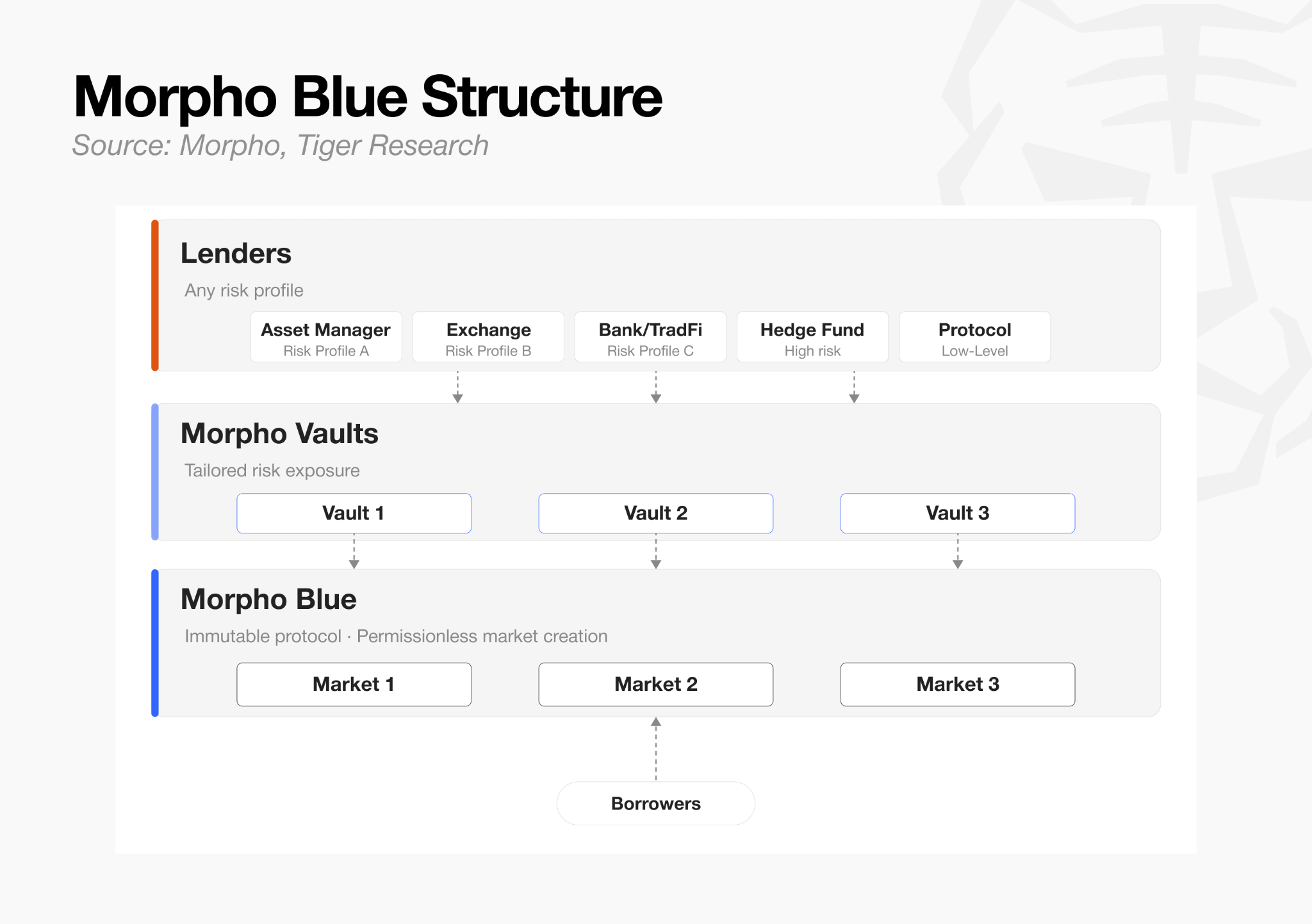

Morpho began as an intermediary layer that optimized interest rates on top of first-generation DeFi lending protocols such as Aave and Compound. In that form, it could not exist independently. In 2023, Morpho published the Morpho Blue whitepaper, and in early 2024 it launched Morpho Blue and Morpho Vaults, effectively declaring independence.

The transition moved away from a structure in which governance made all risk decisions across all markets, and separated market creation and risk judgment from the protocol itself. That separation became the structural foundation allowing institutional participants to select and control risk according to their own compliance standards.

Structure

Morpho Blue: An immutable protocol. Five parameters are fixed at market creation: collateral asset, borrow asset, liquidation loan-to-value ratio (LLTV), price feed, and interest rate model. Anyone can create a market without permission. The protocol itself is responsible only for executing the code as written.

Morpho Vaults: A risk management layer in which independent curators select eligible markets, set supply limits, and allocate capital. Each vault carries a distinct risk profile.

Lenders: Depositors with varying risk appetites, including DAOs, protocols, individuals, and hedge funds, select the vault that matches their profile and supply capital.

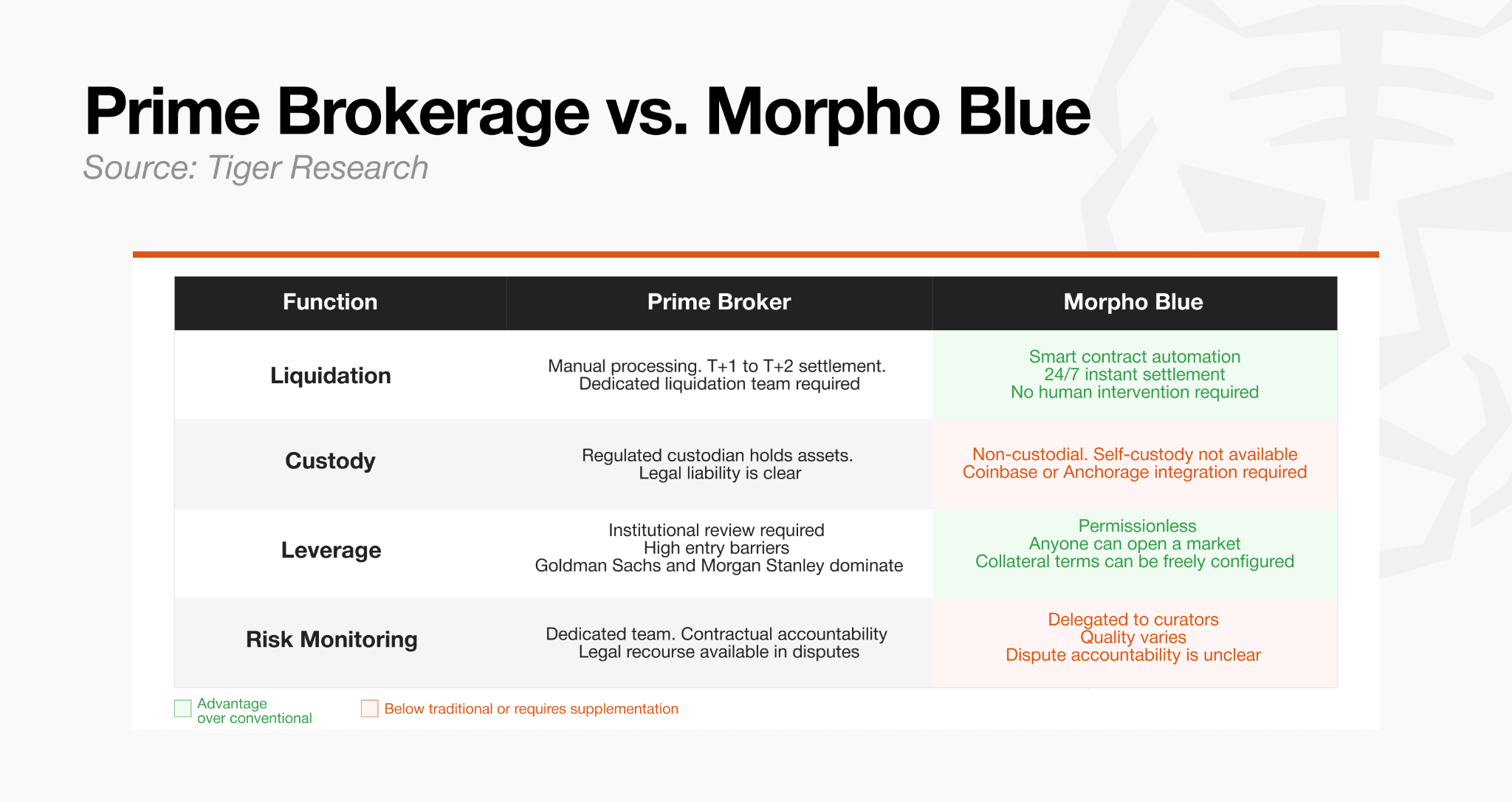

Traditional prime brokers are expected to perform four functions: liquidation, custody, leverage provision, and risk monitoring. Morpho has automated liquidation and leverage provision at the protocol level through smart contracts. Its non-custodial structure, however, means it cannot provide the custody environment that institutions require for regulatory compliance. Integration with external custodians such as Coinbase or Anchorage is therefore necessary.

Risk monitoring similarly depends not on the protocol but on each curator’s ability to select assets and manage exposure. This creates a persistent risk: curator quality is uneven. The xUSD and Stream Finance incident in 2025 illustrated the vulnerability directly. Several Morpho vaults held xUSD exposure and incurred bad debt. In the aftermath, the market began scrutinizing curators’ asset selection capabilities and real-time risk management more rigorously, and institutional capital concentrated around top-tier curators with demonstrated track records, including Steakhouse, Gauntlet, and Sentora.

Traditional prime brokerage bundled liquidation, custody, leverage, and collateral management into a single institutional counterpart. Morpho replaced that model with a division of labor, distributing each function across specialized actors within the ecosystem rather than concentrating it in one institution.

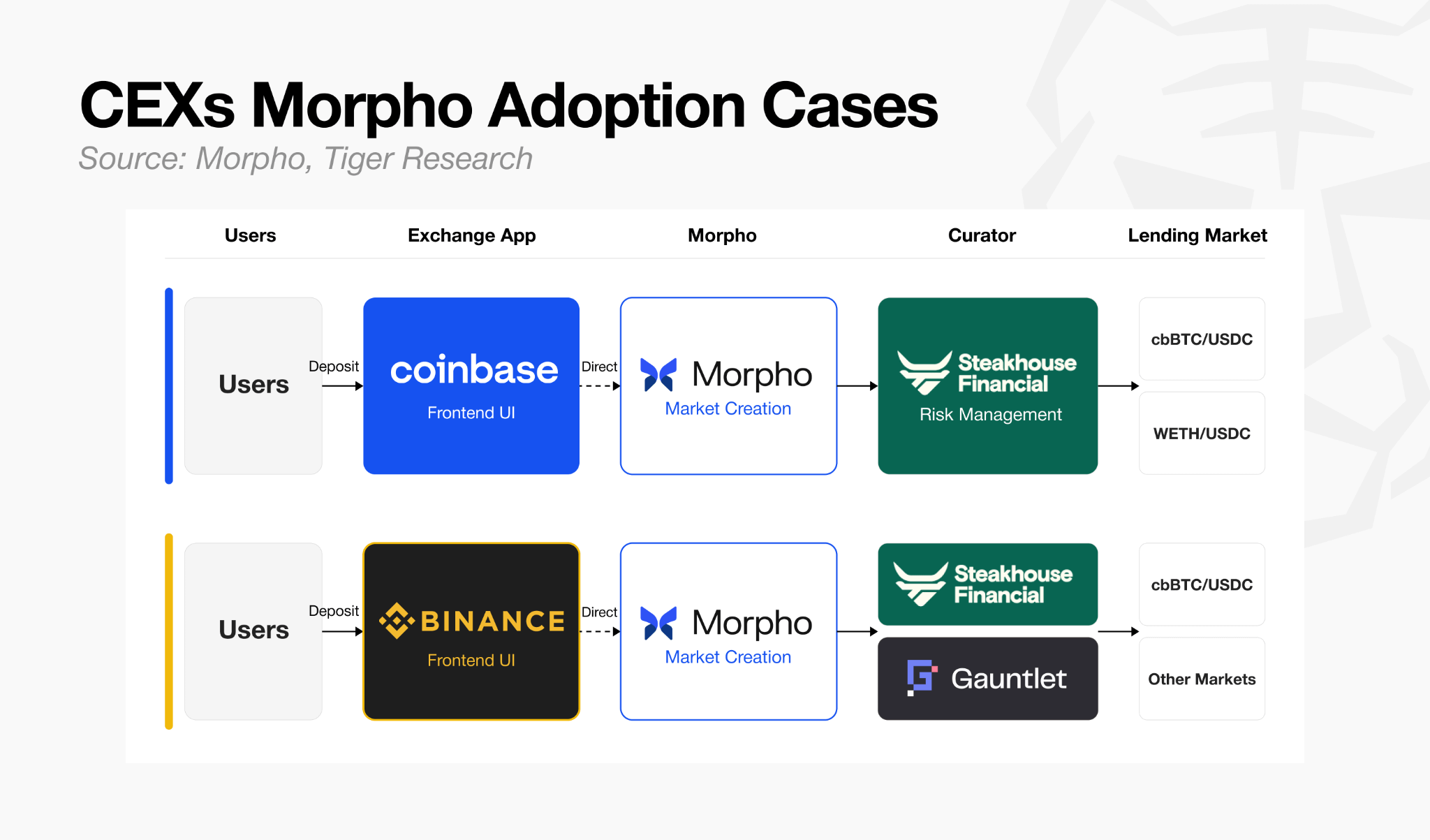

Institutional adoption is now happening at scale, and it began with centralized exchanges.

Coinbase: USDC lending service built on top of Morpho Blue, with Steakhouse Financial as curator.

Binance: Adopted the same structure, with Steakhouse Financial and Gauntlet as curators.

A user pressing the “Borrow” button inside the Coinbase or Binance app receives a loan. The world’s two largest exchanges by volume have chosen the same infrastructure. Adoption has extended to traditional financial institutions as well.

SG-FORGE: Deploys MiCA-compliant stablecoin EURCV and USDCV on Morpho.

Apollo: Brings private credit fund ACRED onchain and uses it as collateral on Morpho.

Bitwise: Curates risk directly on top of Morpho Vaults.

If tokenization opened access to assets, Morpho opened the path to putting those assets to work as productive capital. The trajectory Morpho has set is beginning to present a direction of evolution that lending protocols with very different starting points find difficult to ignore.

4.2. Aave V4: Universal Bank

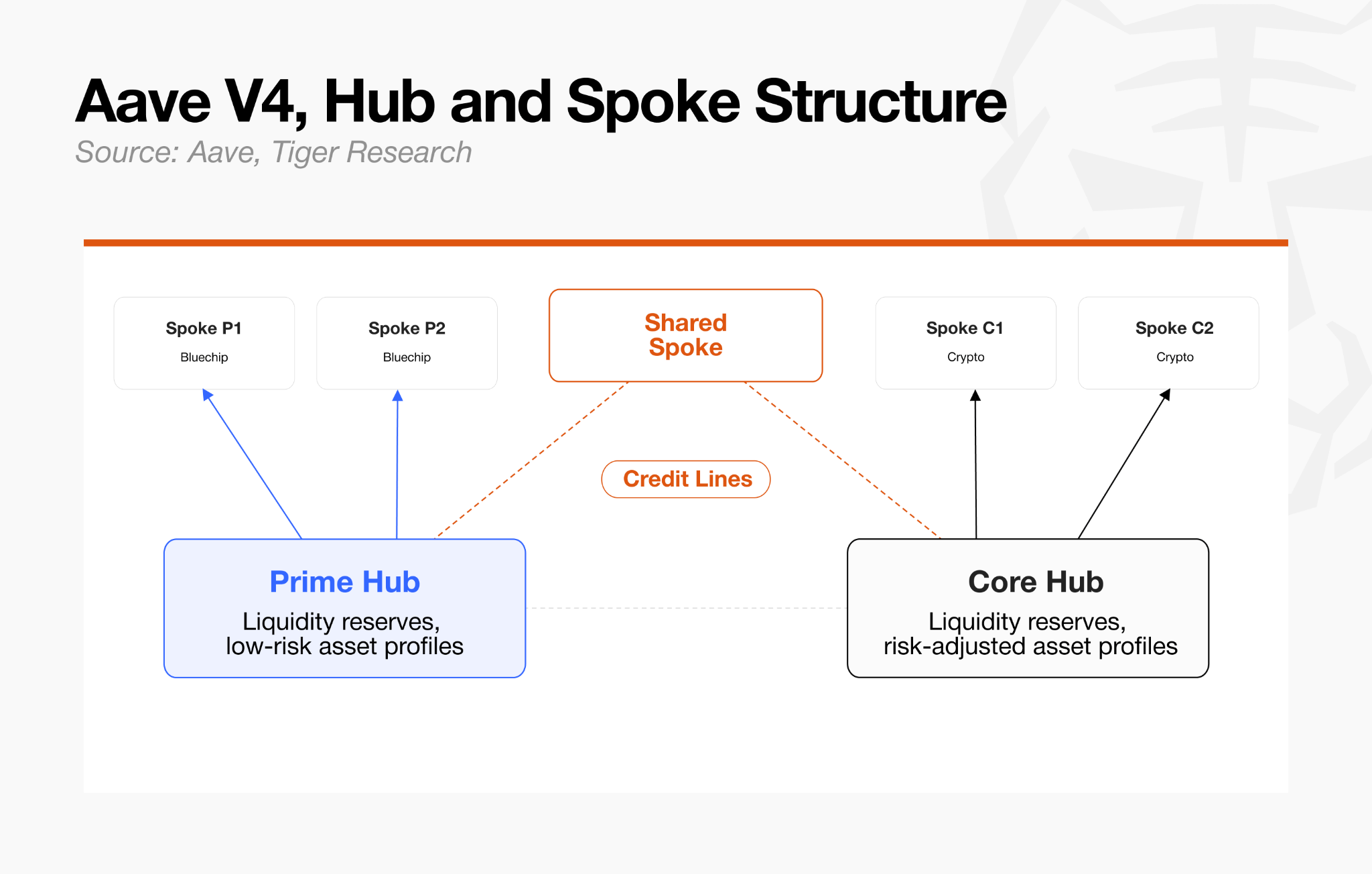

Aave began as ETHLend, a peer-to-peer loan matching model, before evolving through shared-pool architecture across V1, V2, and V3. In March 2026, it activated V4, a modular architecture, on Ethereum mainnet. Where Morpho chose to structurally separate infrastructure from operations, Aave V4 chose a hybrid model that maintains liquidity efficiency while controlling risk.

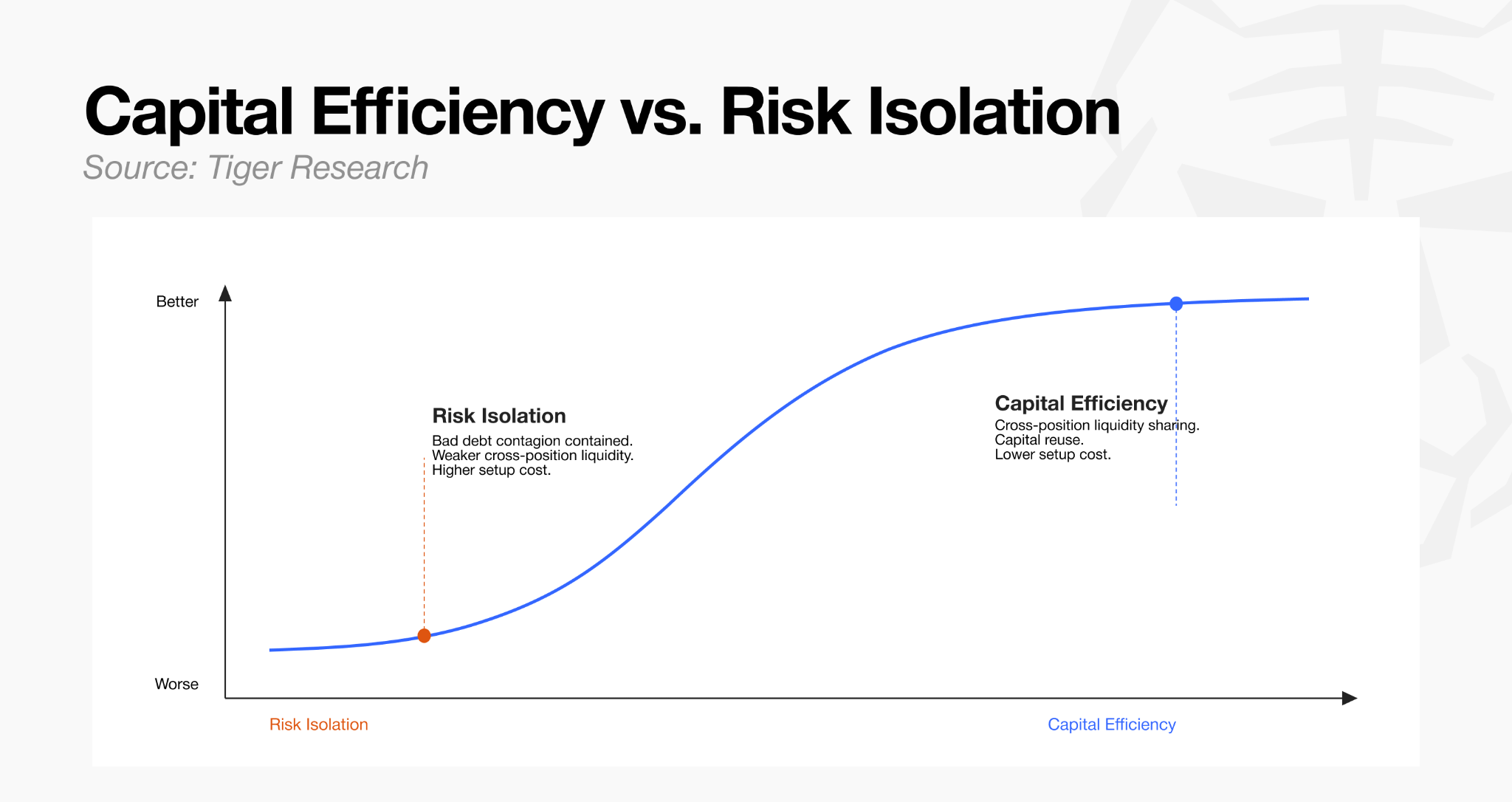

Aave recognized that risk isolation and capital efficiency exist in tension. Moving toward isolation contains bad debt contagion but weakens liquidity network effects and reduces capital efficiency. V4 was designed to resolve that tradeoff structurally.

Structure

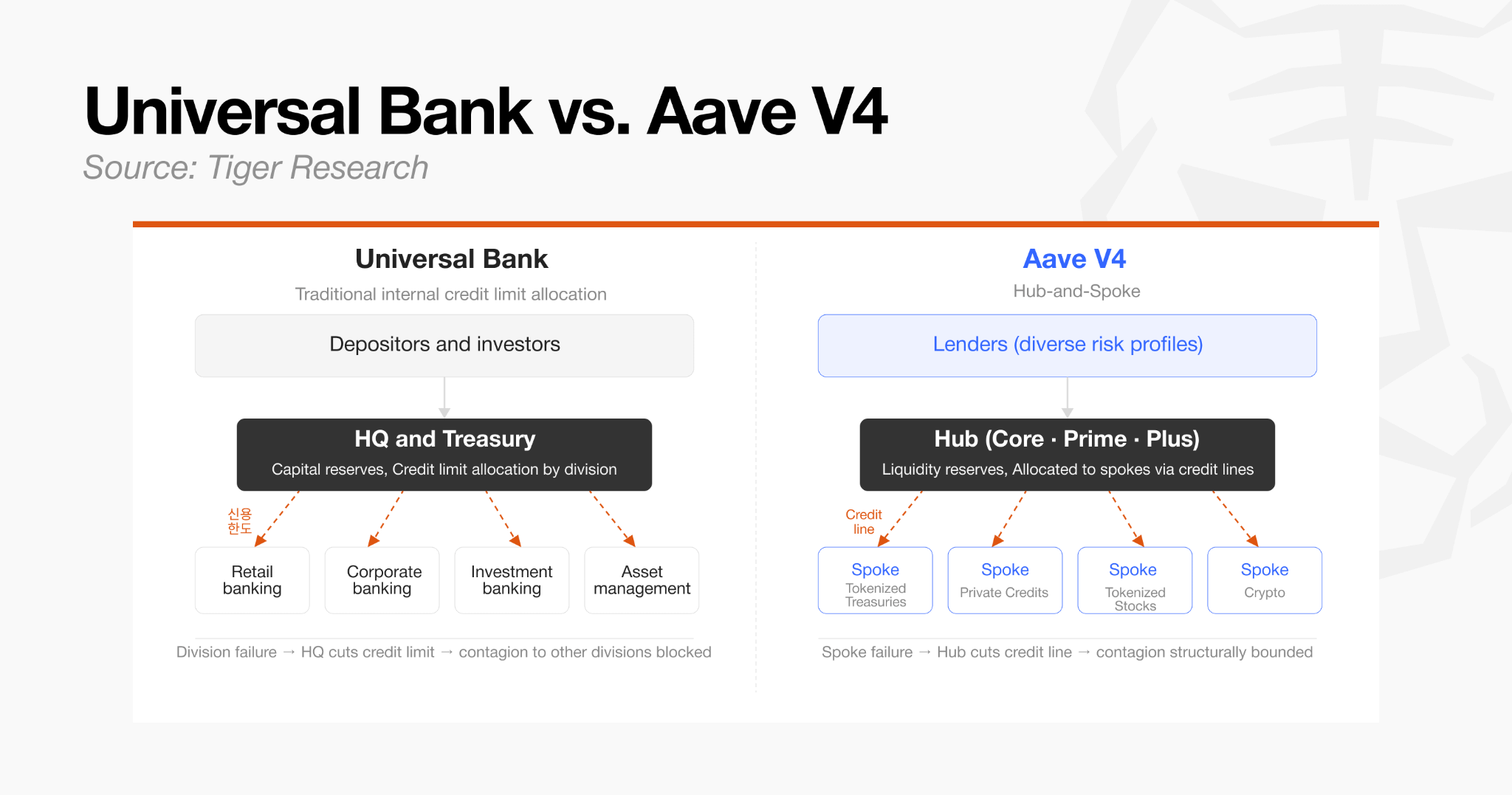

Hub: The central layer that consolidates liquidity and accounting. It assigns credit lines and debit lines to each spoke, capping how much liquidity any given market can draw. The basic risk firewall is formed by these per-spoke limits and local parameters.

Spoke: An individual borrowing market with independent parameters for each asset. When a problem arises in a specific spoke or asset, governance and risk managers can limit exposure by adjusting that spoke’s credit line limit, restricting new borrowing, or activating emergency controls. Because maximum exposure is fixed at the credit line ceiling, the structural spread of contagion is bounded by design.

In traditional finance, this structure resembles a universal bank’s internal credit limit allocation system. The head office assigns credit limits to each division, and when one division runs into trouble, the head office adjusts those limits to contain the spread. The hub plays the role of the head office, and each spoke operates independently like a business division. Unlike Morpho’s full isolation model, where capital is strictly locked within each asset pair, the hub-and-spoke structure allows unused liquidity in one spoke to be redistributed flexibly to more productive spokes through the hub’s credit lines. The result is higher capital efficiency.

This structure becomes a significant advantage in the RWA market. Nascent RWA markets can struggle to attract initial liquidity, but in Aave V4, the existing liquidity hub can serve as a seeding mechanism for new spoke markets. By structuring tokenized assets as independent spokes and setting credit line limits at the hub, new asset classes can be brought to market at lower bootstrapping cost using the liquidity base of safer assets, while initial exposure remains capped within the credit line.

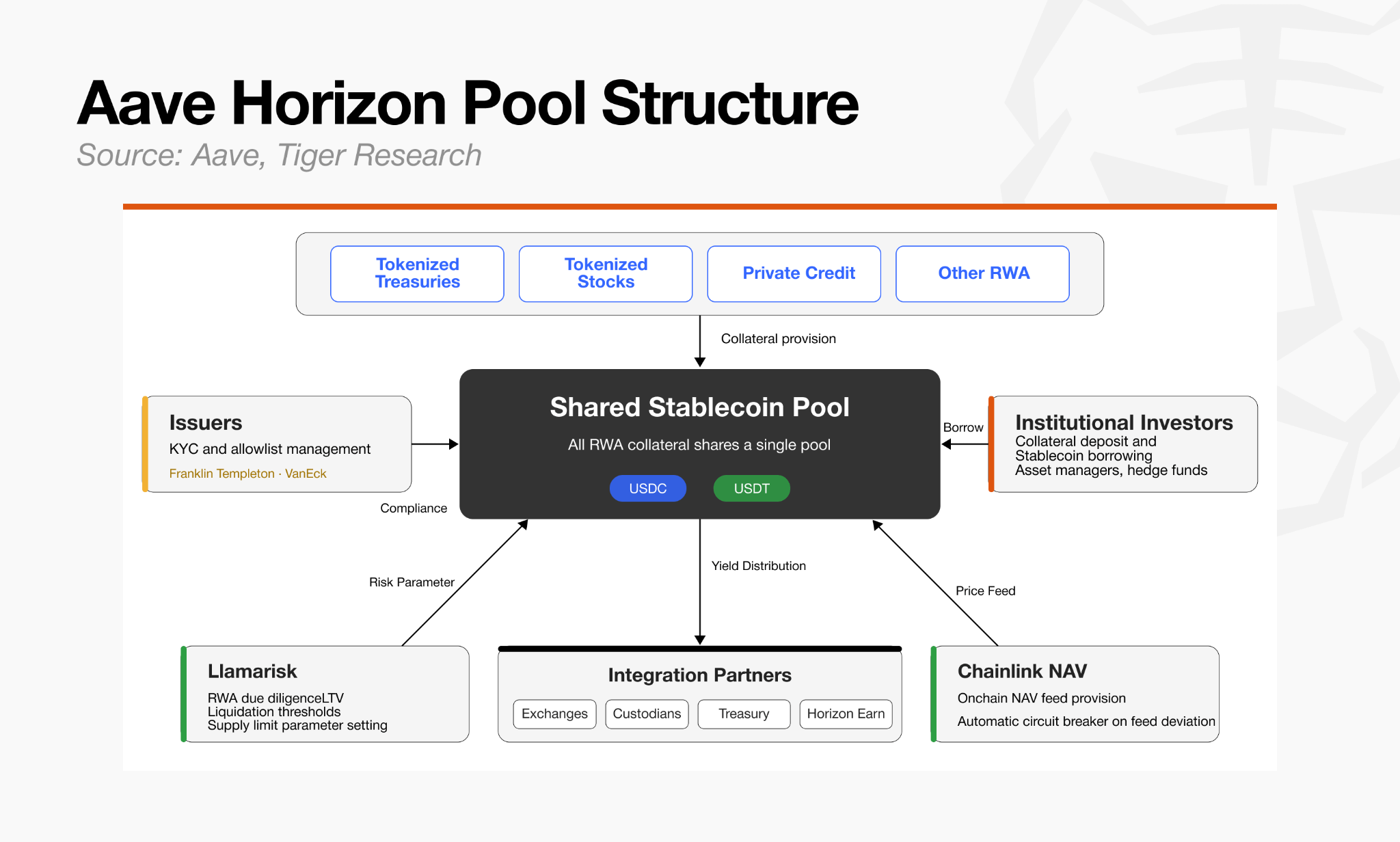

Institutional adoption is organized around Horizon. Horizon launched as a separate RWA lending instance built on Aave v3.3, but its design philosophy aligns with V4’s direction of unified liquidity and risk separation. As it becomes more deeply integrated with V4’s credit line structure, Horizon is likely to consolidate further into Aave’s institutional RWA layer.

Horizon is designed to allow regulated tokenized Treasuries, money market funds, and institutional funds to serve as collateral for stablecoin borrowing, with scope to expand into asset classes such as tokenized stocks and ETFs.

Because approved institutional assets within Horizon are connected to the same institutional liquidity layer, any newly added RWA can immediately draw on existing stablecoin liquidity.

The division of roles within that liquidity layer is as follows:

Issuers: Investor onboarding and KYC/AML allowlist management.

Risk manager (LlamaRisk): RWA due diligence and risk framework and parameter proposals.

Oracle (Chainlink): Onchain price feed provision.

Protocol (Aave): Smart contract execution.

In traditional Aave markets, adding a new asset requires DAO governance deliberation and a vote, which slows the process. Horizon separates these responsibilities: issuers handle per-asset compliance, LlamaRisk handles risk due diligence, and Chainlink handles price verification. This structure allows institutional asset onboarding and risk adjustments to move faster than routing every decision through general DAO governance.

Where Morpho minimized governance involvement and externalized market creation and risk management, choosing speed and optionality, Aave chose a different path: controlled governance delegation and shared liquidity, preserving capital efficiency.

Both approaches are coherent solutions for transplanting traditional finance’s philosophy of risk distribution onto the onchain environment, but which side the RWA market ultimately converges toward remains to be seen.

4.3.Euler V2: Multi Strategy Hedgefund

In March 2023, Euler suffered a $197 million exploit. The attack exploited a flaw in the smart contract code, and because multiple asset markets were connected within a single protocol accounting and liquidation structure, the damage spread across multiple assets.

After roughly three weeks of negotiation, most of the stolen assets were recovered. Euler nonetheless chose to rebuild the architecture rather than simply repair it, and subsequently repositioned itself as flexible institutional lending infrastructure.

Euler’s entry into the RWA and institutional credit market was driven by a gap in traditional finance’s asset tokenization efforts. Banks were issuing tokenized bonds, funds, and Treasuries, but those assets lacked the onchain infrastructure needed to be used for lending or credit provision.

Rather than drawing institutional demand into volatile long-tail crypto asset markets, Euler began positioning itself as a credit layer for institutional finance, one that gives those assets liquidity onchain.

Structure

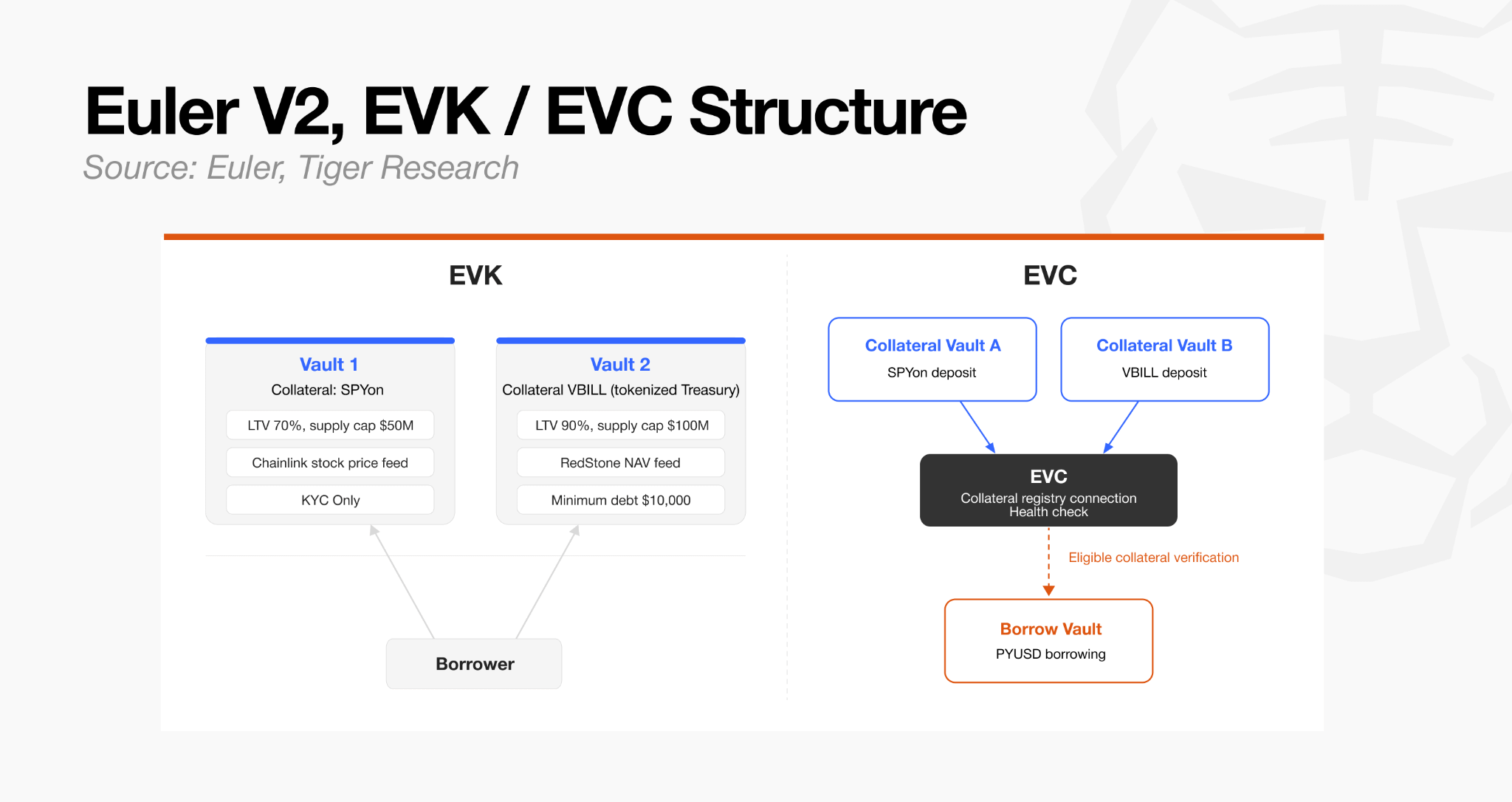

EVK (Euler Vault Kit): A kit for creating ERC-4626-based credit vaults with borrowing functionality. Each vault holds independent parameters for a specific asset and risk configuration, and connects to other vaults through the EVC to form lending markets.

EVC (Ethereum Vault Connector): The core immutable primitive that connects collateral and debt relationships distributed across multiple vaults, managing them within a single account. In traditional finance terms, it is analogous to consolidating multiple dispersed asset accounts into a single margin account that provides cross-collateral.

Where the EVK enables independent design at the asset level, the EVC connects assets that would otherwise be fragmented into a unified account and position management framework.

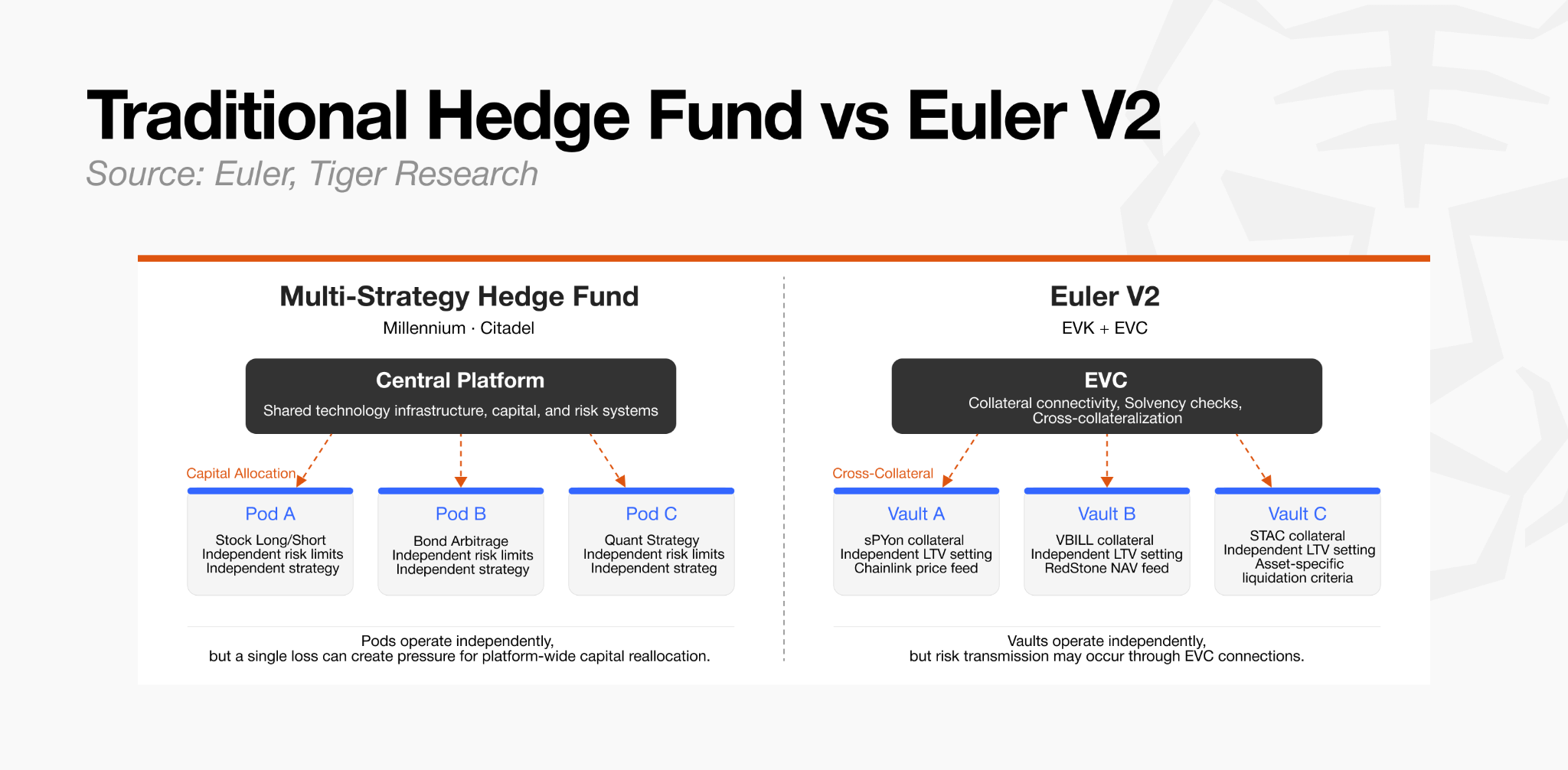

In traditional finance terms, Euler shares certain characteristics with the pod structure of a multi-strategy hedge fund. Independent pods each operate with their own strategies and risk limits, while sharing technology infrastructure and capital management systems.

The key difference is that Euler is not a single firm’s internal organization but an open infrastructure where multiple independent actors can create and connect vaults.

By analogy, where Morpho resembles a prime brokerage division-of-labor model and Aave resembles a universal bank shared-liquidity model, Euler resembles a multi-strategy hedge fund’s connected modular structure. The same flexibility and capital efficiency that the architecture enables also creates the possibility of indirect risk transmission from one asset to other positions within the connected vault ecosystem. Curator risk management capability therefore remains a central challenge for the Euler V2 ecosystem.

Euler’s institutional adoption is developing in a direction that accommodates asset-specific characteristics and regulatory requirements. The first front is tokenized stocks. Equity assets trade in a 24/5 environment and require price feeds capable of reflecting corporate events such as dividends and stock splits. Under a single shared-risk structure, building an isolated market meeting those conditions was not feasible. The EVK, which enables independent design at the asset level, made it possible.

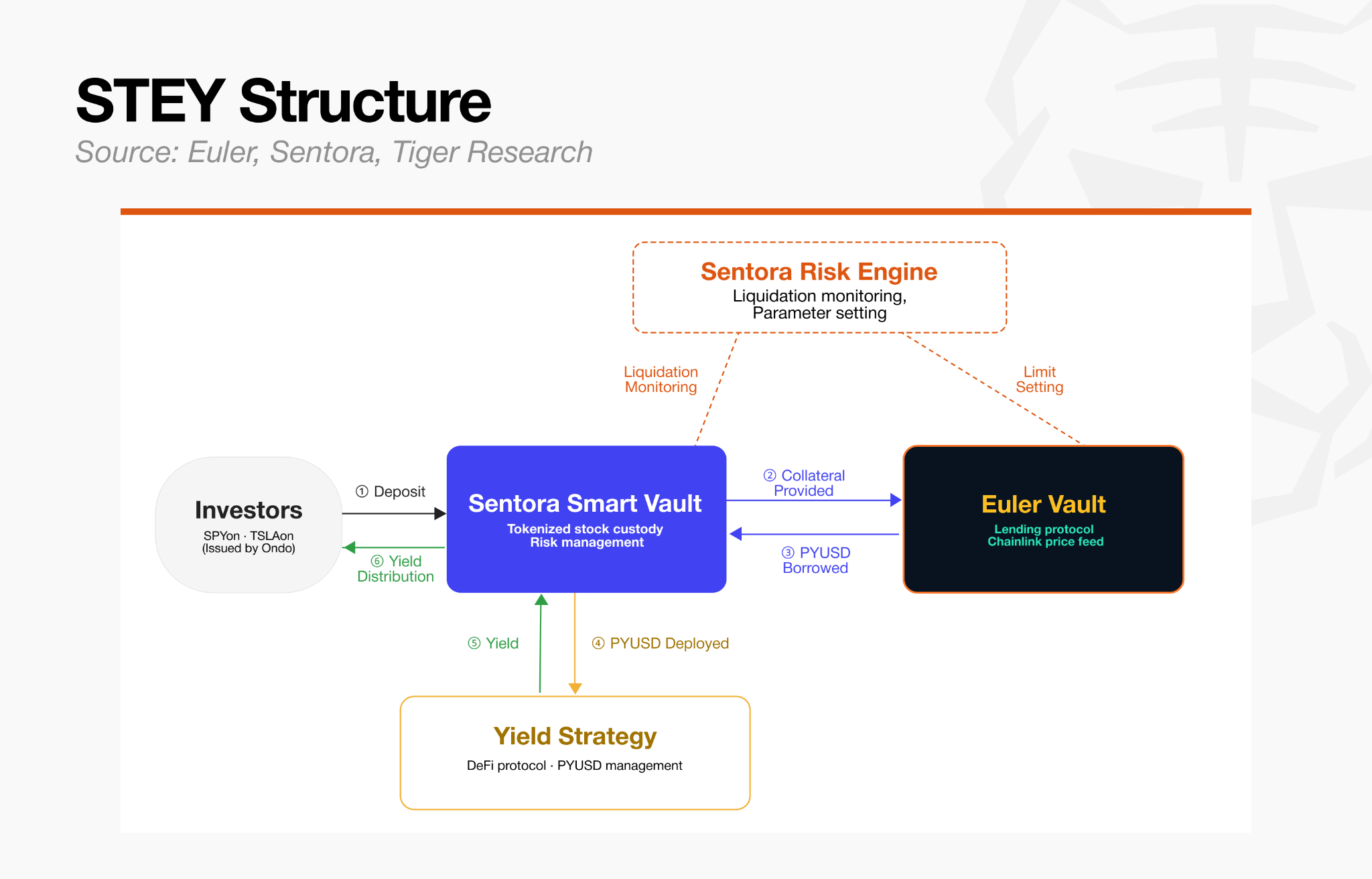

In partnership with Ondo Finance, Euler launched STEY, a lending market accepting SPYon (S&P 500), QQQon (Nasdaq-100), and TSLAon (Tesla) as collateral.

STEY Market Structure

Collateral: Ondo tokenized stocks (SPYon, QQQon, TSLAon)

Borrow asset: PYUSD (PayPal stablecoin)

Price feed: Chainlink real-time equity price feeds

Risk management: Curated by Sentora

Just as traditional finance uses Lombard loans to unlock liquidity from stock holdings, the STEY market replicates that mechanism onchain. Investors can maintain price exposure to tokenized stocks while redeploying borrowed stablecoins into onchain yield strategies, maximizing capital efficiency.

The second front is the combination of tokenized Treasuries and CLOs (collateralized loan obligations). Euler launched the KPK USDC Prime RWA Vault to demonstrate this structural flexibility.

KPK USDC Prime RWA Vault Structure

Collateral: VBILL (VanEck tokenized Treasury), STAC (Securitize AAA-rated CLO)

Borrow asset: USDC

Price feed: RedStone daily NAV feeds

Risk management: Curated by Sentora

CLOs require periodic NAV pricing through oracles and asset-specific liquidation standards. Tokenized Treasuries require strict compliance controls. Without modular infrastructure that allows independent hooks and parameters to be custom-designed at the vault level, onboarding either asset class as onchain lending collateral would have been extremely difficult.

The possibility of indirect risk transmission from overlapping exposure to the same assets, oracles, and collateral nonetheless remains, and Euler V2 faces the ongoing challenge of calibrating the balance between flexibility and control.

All three protocols are addressing the barriers to institutional entry from different starting points and with different methodologies.

Morpho: Fully externalizes market creation and risk management to maximize speed and optionality, with the quality of the curator layer as the critical variable to validate.

Aave: Combines controlled governance delegation with V4’s hub-and-spoke architecture, pursuing a hybrid approach that preserves capital efficiency without compromising stability.

Euler: Uses the EVK and EVC to secure both per-asset independence and cross-collateral flexibility simultaneously, seeking the optimal risk balance within a multi-strategy structure.

Their approaches differ, but all three are converging on the same structural direction: separating the base execution infrastructure from the risk judgment layer, and designing asset-specific risk parameters for each collateral type.

5. Conclusion

In traditional capital markets, prime brokerage took decades to establish itself as the core infrastructure supporting hedge funds across trading, custody, settlement, leverage, and risk management. The collapse of Lehman Brothers in 2008 and the Reserve Primary Fund bank run each exposed distinct categories of systemic risk, and the market became more attentive to custody, collateral, liquidity management, and role separation in the aftermath.

The DeFi ecosystem arrived at a structurally similar set of conclusions in far less time. The reason it could move so quickly is that code moves faster than regulation.

After early shared-risk structures encountered governance bottlenecks and experienced unexpected exposure and bad debt contagion, Morpho, Aave, and Euler each implemented risk isolation and operational separation onchain in a fraction of the time. The DeFi market has learned through repeated cycles of actual capital loss and architectural rebuilding, compressing into years a process that took traditional finance decades.

The history of traditional finance shows that the maturation of infrastructure such as prime brokerage was one of the conditions that enabled the hedge fund industry to grow. After 2008, total hedge fund AUM approached $2 trillion as infrastructure stabilized and institutional capital began flowing in. Between 2015 and 2025 alone, the industry grew from $1.4 trillion to $4.5 trillion. As infrastructure matured, genuine competition in strategy and risk management began at the operational layer above it, and managers who demonstrated superior capability attracted the market’s capital.

The onchain lending market is entering a similar inflection point. With Morpho, Aave V4, and Euler V2 all converging on risk isolation and operational separation, the central question is now the competition that will unfold at the operational layer above that infrastructure.

Total AUM across onchain curation vaults currently stands at approximately $7.4 billion. Given how substantially the hedge fund industry grew after its infrastructure was established, the onchain credit market today resembles the early stages of a much larger expansion.

In traditional finance, Goldman Sachs and Morgan Stanley held near-duopoly control over prime brokerage infrastructure, and hedge funds had to accept their terms to gain access. Onchain infrastructure operates differently. Opening a market on Morpho or Euler requires no institution’s permission.

With the infrastructure monopoly broken, competition at the onchain operational layer is likely to unfold more openly and more rapidly than it did in traditional finance. In the traditional market, platforms such as Bridgewater, Millennium, and Citadel, along with alternative asset managers such as Blackstone and Apollo, attracted large pools of capital through a combination of operational capability and infrastructure access.

Onchain, any actor with the capacity to assess collateral, design risk parameters, navigate institutional regulatory requirements, and build a track record now has the opportunity to capture a position in the emerging credit market, on an infrastructure that is far more accessible than what traditional finance has ever offered.

🐯 More from Tiger Research

Read more reports related to this research.Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.