This report was written by Tiger Research, analyzing the rapid growth of the digital asset custody industry, examining three distinct business models, and exploring regulatory approaches across Singapore, Hong Kong, Japan, and Korea.

TL;DR

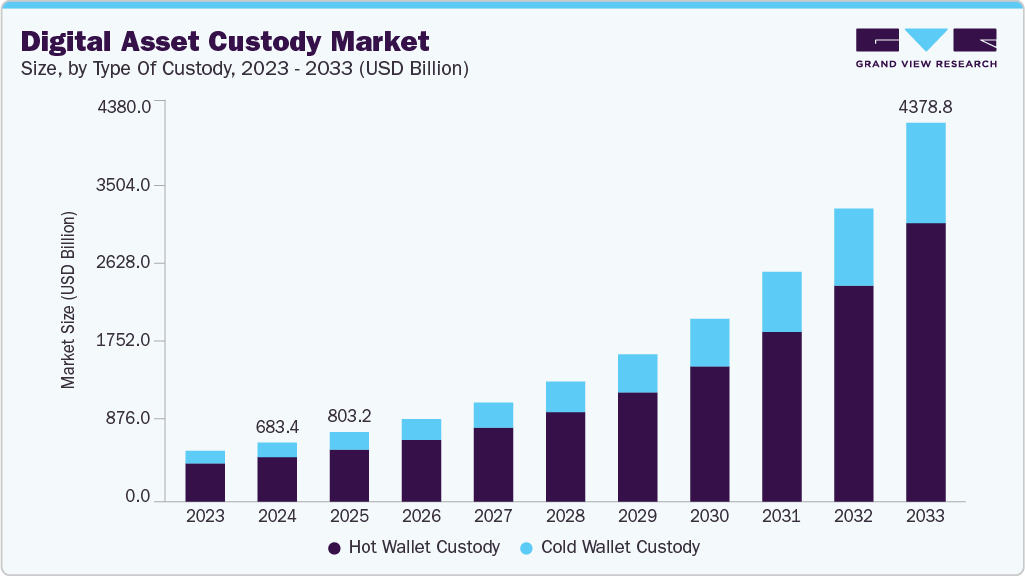

The global custody market expanded more than 50%, from USD 447.9 billion in 2022 to USD 683 billion in 2024, evolving from a basic safekeeping function into a core infrastructure for institutional participation.

Custody providers can be broadly categorized into three models: traditional custodians focus on regulatory trust and compliance, hybrid models pursue service diversification, and technology providers compete through security and API-based infrastructure. Across jurisdictions, Singapore, Hong Kong, Japan, and South Korea have each developed distinct local custody frameworks.

The future of custody depends not only on the growth of assets under custody but also on how providers layer financial services atop custody infrastructure. A deep understanding of regulation and local adaptation will remain the decisive factors for global expansion and the success of new entrants.

1. Why the Custody Market Matters Now

The custody industry has expanded rapidly since entering the regulated financial system. Initially, custody services played a limited role, primarily holding digital assets for exchanges. However, as institutional demand has increased, the client base has diversified and broadened. The rise of digital asset ETFs and digital asset treasury (DAT) firms has further fueled institutional participation, driving up the total volume of assets under custody.

This trend is reflected in market data: the global custody market grew from approximately USD 447.9 billion in 2022 to USD 683 billion in 2024—an increase of more than 50% in just two years. Growth is accelerating, with multiple reports projecting an average annual expansion of 17–25% for digital-asset-focused custody. Given the current wave of institutional capital inflows and expanding regulatory infrastructure, actual growth could surpass these forecasts.

As the volume of assets requiring custody increases, so does the demand for secure, reliable service providers. This report examines how the custody market has evolved and explores how different jurisdictions are structuring and regulating their custody frameworks.

2. The Custody Industry Born from Crisis

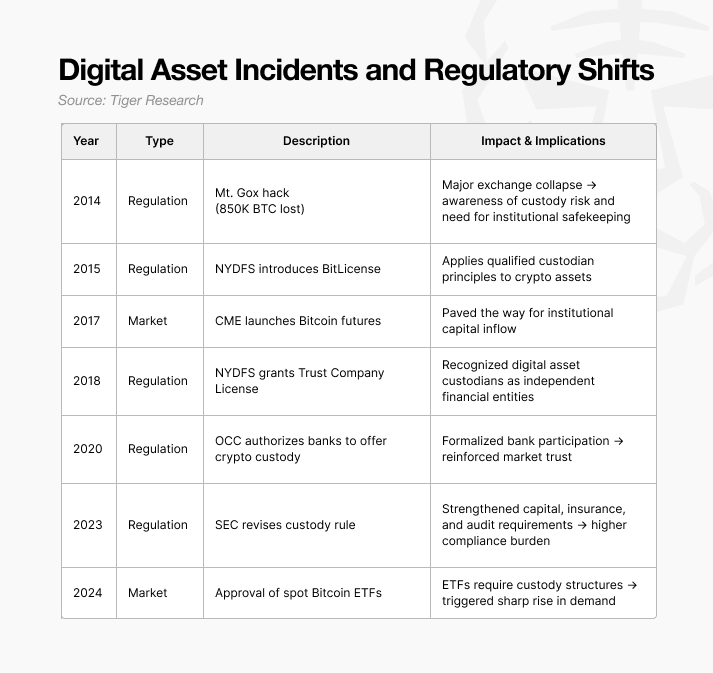

The custody industry emerged from a crisis. The turning point was the 2014 Mt. Gox incident in Japan, where approximately 850,000 bitcoins were stolen, causing massive losses for users. The event underscored a critical lesson for the entire industry: without institutional mechanisms to safeguard digital assets, it is impossible to operate a sustainable business in the market.

This realization drove regulatory progress. In the aftermath of Mt. Gox, frameworks governing digital asset custody steadily evolved. The United States, in particular, established custody guidelines comparable to those applied in traditional finance. These regulatory developments laid the groundwork for a clearer and more robust structure, enabling the custody industry to grow under defined standards.

3. Types of Custody Services

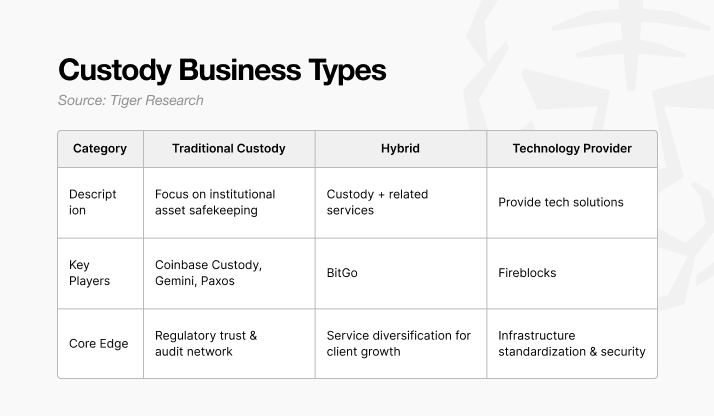

While most custody providers are built around core asset safekeeping functions, their market positioning and competitiveness vary significantly depending on their strategic focus. Broadly, custody businesses can be categorized into three models:

Traditional Custody Model: Focused solely on asset safekeeping, similar to conventional financial custodians.

Hybrid Model: Expands beyond custody to offer value-added services such as staking, settlement, or reporting.

Technology Provider Model: Offers custody infrastructure as a SaaS-based solution, enabling institutions to operate their own custody systems.

Each model targets different client segments and needs, competing based on their operational strengths and service depth.

3.1. Traditional Custody

Traditional custody providers focus primarily on asset safekeeping. Their core value lies in trust built through proven operational records, positioning them as reliable custodians for institutional investors. The leading example is Coinbase Custody.

Coinbase’s strength is clearly reflected in the U.S. spot ETF market. As of 2025, it serves as custodian for 9 out of 11 SEC-approved Bitcoin spot ETFs and 8 out of 9 Ethereum ETFs. This dominant market share has established Coinbase Custody as the most trusted institutional custodian in the sector.

The company’s credibility stems from its early regulatory alignment. In 2018, Coinbase Custody received a Limited Purpose Trust Charter from the New York Department of Financial Services (NYDFS). In 2025, it was also recognized by the U.S. Securities and Exchange Commission (SEC) as a Qualified Custodian under asset custody regulations. This status gives it the same legal authority to hold client assets as banks and broker-dealers.

While many competitors are only now obtaining similar licenses, Coinbase has accumulated years of operational experience under regulatory oversight. This track record has become a decisive factor in attracting institutional clients. In custody services, technological sophistication is important, but verified operational history remains the key measure of trust.

Ultimately, the core advantage of the traditional custody model is proven performance. Even technologically advanced newcomers struggle to surpass incumbents whose regulatory history and operational record underpin their credibility.

3.2. Hybrid

Hybrid custody models build on basic safekeeping services but extend into integrated offerings that combine custody, trading, and asset management. In essence, they provide institutional clients with a one-stop solution that spans from storage to utilization. The leading example is BitGo.

BitGo’s service portfolio goes well beyond custody. It includes staking, over-the-counter (OTC) trading, lending, and real-world asset (RWA) tokenization. Through institutional-grade wallets and APIs, BitGo integrates custody with treasury management systems, while its staking services are directly linked to custodial accounts. Its OTC operations are licensed by Germany’s Federal Financial Supervisory Authority (BaFin).

Leveraging service diversification, BitGo achieved rapid global expansion. By entering flexible regulatory environments such as Hong Kong, Singapore, and Abu Dhabi early, it established a strong local presence and quickly built its institutional client base.

The hybrid model’s core strength lies in diversification built on custody. Rather than limiting itself to storage, it delivers interconnected services spanning trading, asset management, and tokenization. While traditional custodians grow through regulatory trust, hybrid models gain momentum through service expansion.

3.3. Technology Providers

Basically, the technology provider model does not directly hold digital assets. Instead, they offer SaaS infrastructure that enables banks, exchanges, and fintech firms to manage their own custody systems. The leading player in this segment is Fireblocks.

Fireblocks’ technological capabilities have made it the preferred partner for building secure digital asset infrastructure. Major clients such as BNY Mellon, Galaxy Digital, and Crypto.com highlight its market credibility. As of 2025, over USD 200 billion in assets are managed on its platform across more than 1,800 institutions. This accumulated experience and technical reliability have positioned Fireblocks as the go-to provider for institutional custody solutions.

In 2024, Fireblocks obtained a Limited Purpose Trust Charter from the NYDFS, granting it the legal authority to hold assets directly. However, the company remains primarily focused on technology provision. The license functions more as a trust-building mechanism for institutional clients than a shift in business direction. While Fireblocks has evolved into an infrastructure firm capable of direct custody, it uses this status strategically to reinforce its leadership as a technology-first provider.

4. Local Strategies under Varying National Custody Regulations

Financial regulations differ significantly across jurisdictions, and custody services must adapt to these local frameworks. As regulatory standards vary by country, demand for locally compliant service providers continues to grow. Even in markets that are less developed than the U.S.—where ETFs and digital asset trusts (DATs) are already well established—specialized local custody solutions have emerged to align with national regulatory environments.

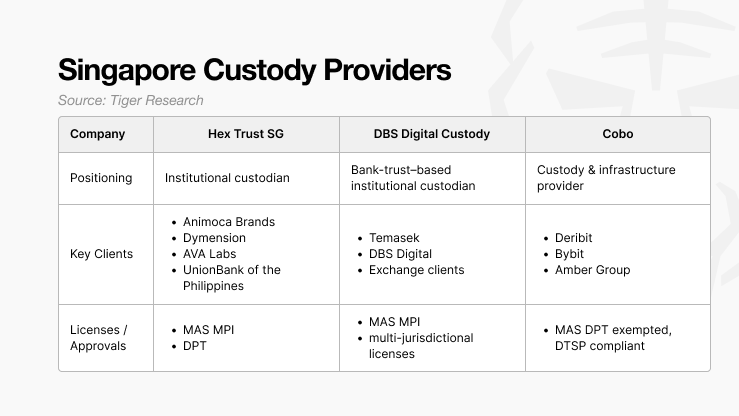

4.1. Singapore

As of June 30, Singapore expanded the scope of the Financial Services and Markets Act (FSMA) to include custody within the definition of digital asset services. Under this revision, even custody firms serving only overseas clients must obtain approval from the Monetary Authority of Singapore (MAS) if they operate locally. MAS has stated that licensing standards for custody will be applied strictly, implying that participation will largely be limited to banks and institutional-grade entities.

4.2. Hong Kong

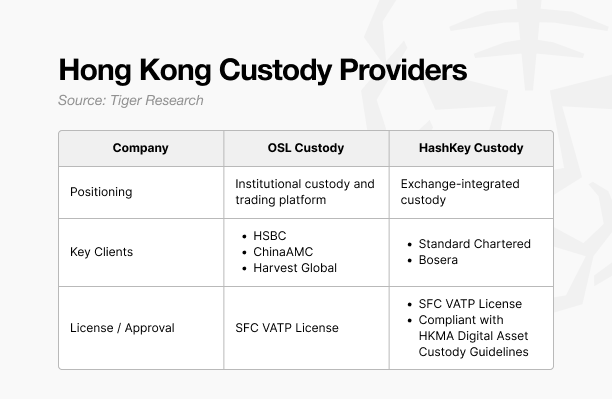

In 2023, Hong Kong’s Securities and Futures Commission (SFC) introduced the Virtual Asset Trading Platform (VATP) regime, integrating trading and custody under a single regulatory framework. This structure goes beyond a simple registration system by requiring dual authorization for both exchange and custody functions.

OSL offers integrated custody, OTC, and tokenization services alongside its exchange operations. It currently provides custody for three of the four approved spot digital asset ETFs in Hong Kong. HashKey, in partnership with Standard Chartered, offers institutional clients fiat on- and off-ramp services and enhances settlement efficiency between digital and fiat assets through its proprietary infrastructure.

Hong Kong’s regulatory direction is clear: it emphasizes a “regulation plus banking collaboration” model. Whereas Singapore’s custody ecosystem evolved through partnerships between local firms and global service providers, Hong Kong’s approach centers on cooperation between traditional financial institutions and local custodians to attract institutional capital.

4.3. Japan

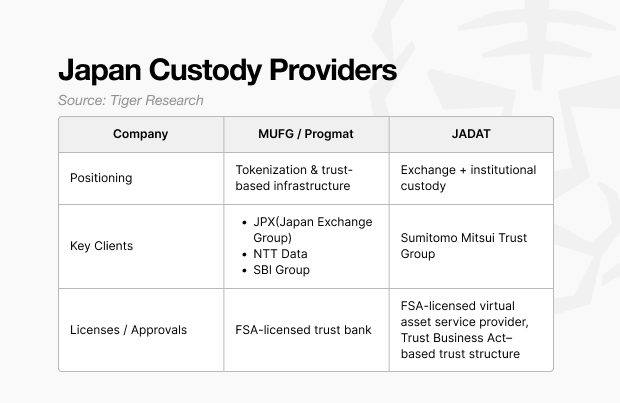

Japan’s Financial Services Agency (FSA) enforces a strict custody framework prioritizing client asset protection. Custodians must store at least 95% of client assets in offline cold wallets. The remaining portion, held in hot wallets, must be fully collateralized with equivalent amounts of fiat currency or bonds. External audits are also mandatory.

Due to these high regulatory requirements, Japan’s custody market is dominated by traditional financial groups rather than Web3-native firms. Only institutions with sufficient capital and robust infrastructure can meet the FSA’s standards.

MUFG/Progmat focuses on tokenization and trust-based infrastructure, leveraging its status as an FSA-licensed trust bank. JADAT operates a hybrid model that combines exchange and institutional custody functions. It holds both a virtual asset exchange license and a trust business license under the Trust Business Act, enabling it to provide integrated trading and custody services.

Japan illustrates how stringent regulation amplifies the influence of traditional finance. High collateral thresholds and mandatory audits have made banks and trust companies the dominant custodians in the market.

4.4. South Korea

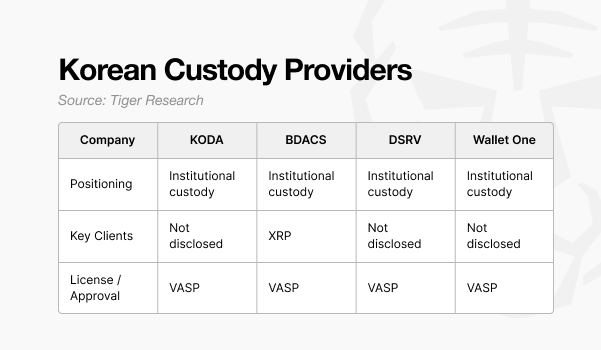

South Korea’s custody industry operates under the Act on Reporting and Use of Certain Financial Transaction Information (the “Specific Financial Information Act” or “VASP framework”), which governs virtual asset service providers. The Korean market is characterized by two parallel trends: financial-institution-led partnerships and technology-driven specialization. Models range from joint ventures like KODA, led by traditional financial institutions, to startups differentiating through security and infrastructure innovation.

Recently, in preparation for Phase 2 of the Financial Services Commission’s (FSC) roadmap for corporate digital asset trading, exchanges have begun actively competing to attract corporate clients. Institutional demand is expected to grow once the corporate trading market officially opens.

A near-term inflection point for Korea’s custody industry will be the participation of roughly 3,500 qualified professional investors. If institutions begin entering the market in visible numbers, the sector could expand toward security tokens (STOs) and real-world asset (RWA) tokenization. Regulatory integration may thus serve not only compliance purposes but also as a catalyst for new market formation.

5. The Custody Industry Is Only Beginning

The custody industry is still in its early stages. Its competitive strategies can largely be divided into two approaches.

The first is early market entry, as seen with Coinbase Custody, which established dominance by building institutional trust and a strong client base ahead of competitors.

The second is service diversification, exemplified by BitGo, which has differentiated itself through offerings such as staking, real-world asset (RWA) tokenization, and lending.

As the digital asset market transitions from retail-driven activity to institutional participation, custody providers are focusing on developing bank-grade infrastructure and audit frameworks that meet institutional standards. At the same time, technology infrastructure providers that enable new entrants to build compliant custody systems are gaining attention.

Successful market entry, however, depends on a deep understanding of local regulatory frameworks and ecosystem dynamics.

In the United States, obtaining regulatory approval is essential to building institutional credibility, though new entrants must compete against the strong position of Coinbase Custody.

In Hong Kong and Singapore, success relies on collaboration models with banks under clear regulatory oversight.

In Japan, strict client asset protection rules make partnerships with large domestic financial institutions a prerequisite for entry.

In South Korea, diverse players exist, but institutional participation is still developing, leaving room for growth once regulatory clarity improves.

Ultimately, firms seeking to enter the custody market must prioritize precision over speed. Sustainable growth depends on accurately analyzing local regulations and designing robust partnership structures with financial institutions. Even latecomers can find meaningful opportunities—if they align their business models with regulatory requirements and build credible local partnerships.

🐯 More from Tiger Research

Read more reports related to this research.BTCFi #3: Breaking Down the Asset & Custodian Layer of BTCFi

The Game Is Changing for Vietnam’s Centralized Exchange Licenses

Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn’t harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research’s reports, it is mandatory to 1) clearly state ‘Tiger Research’ as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.