Summary

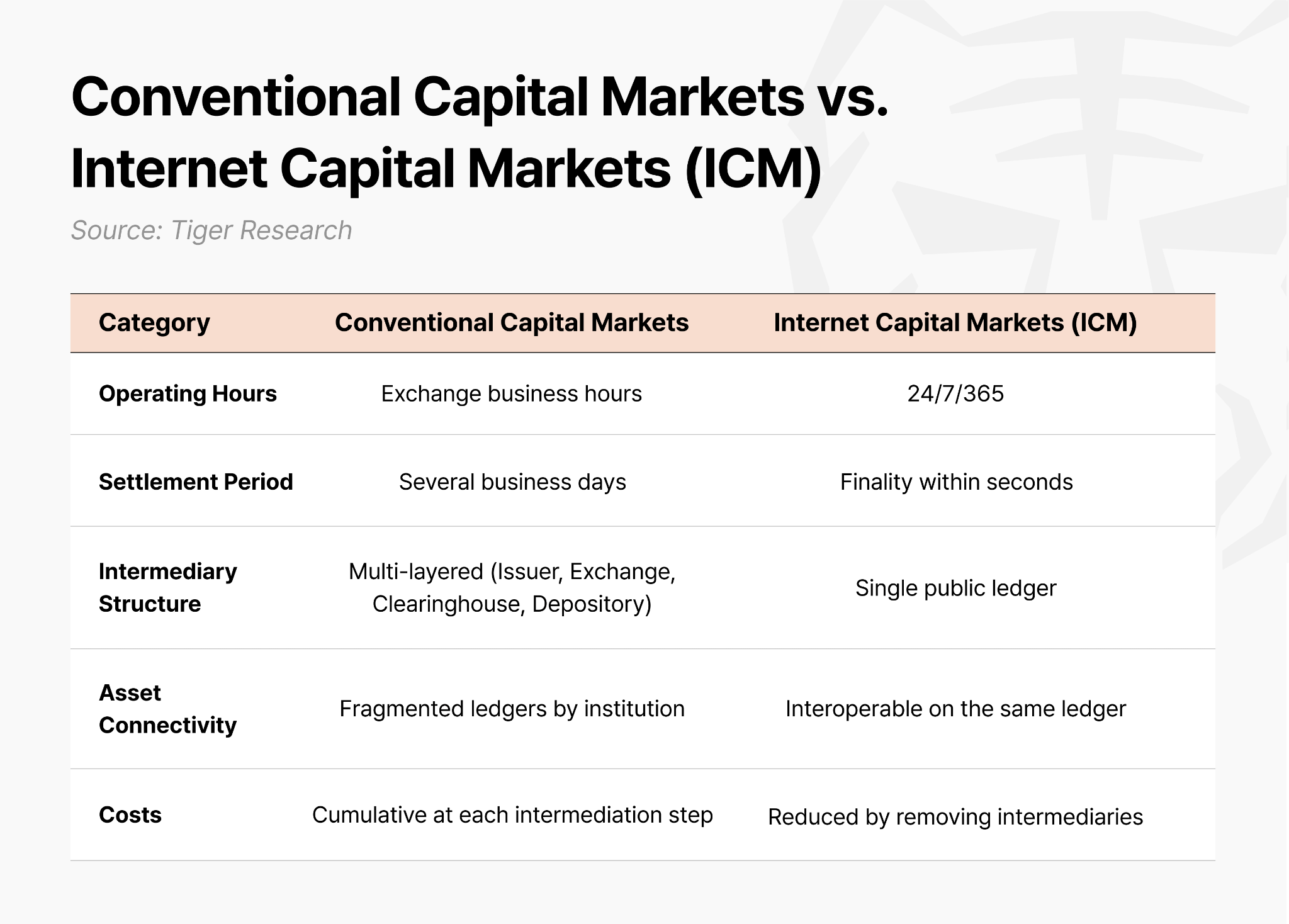

Crypto has crossed from experimentation into industry. The form that industry is taking is the Internet Capital Markets, or ICM: a structure in which asset issuance, trading, and settlement all complete on a single public blockchain.

Capital markets today still run on infrastructure designed before the internet. Even a simple stock transaction passes through clearinghouses and depositories, and settlement takes at least a day. The ICM removes that lag entirely, because assets move across a single ledger rather than through a chain of institutional records. It is the next stage of capital market architecture.

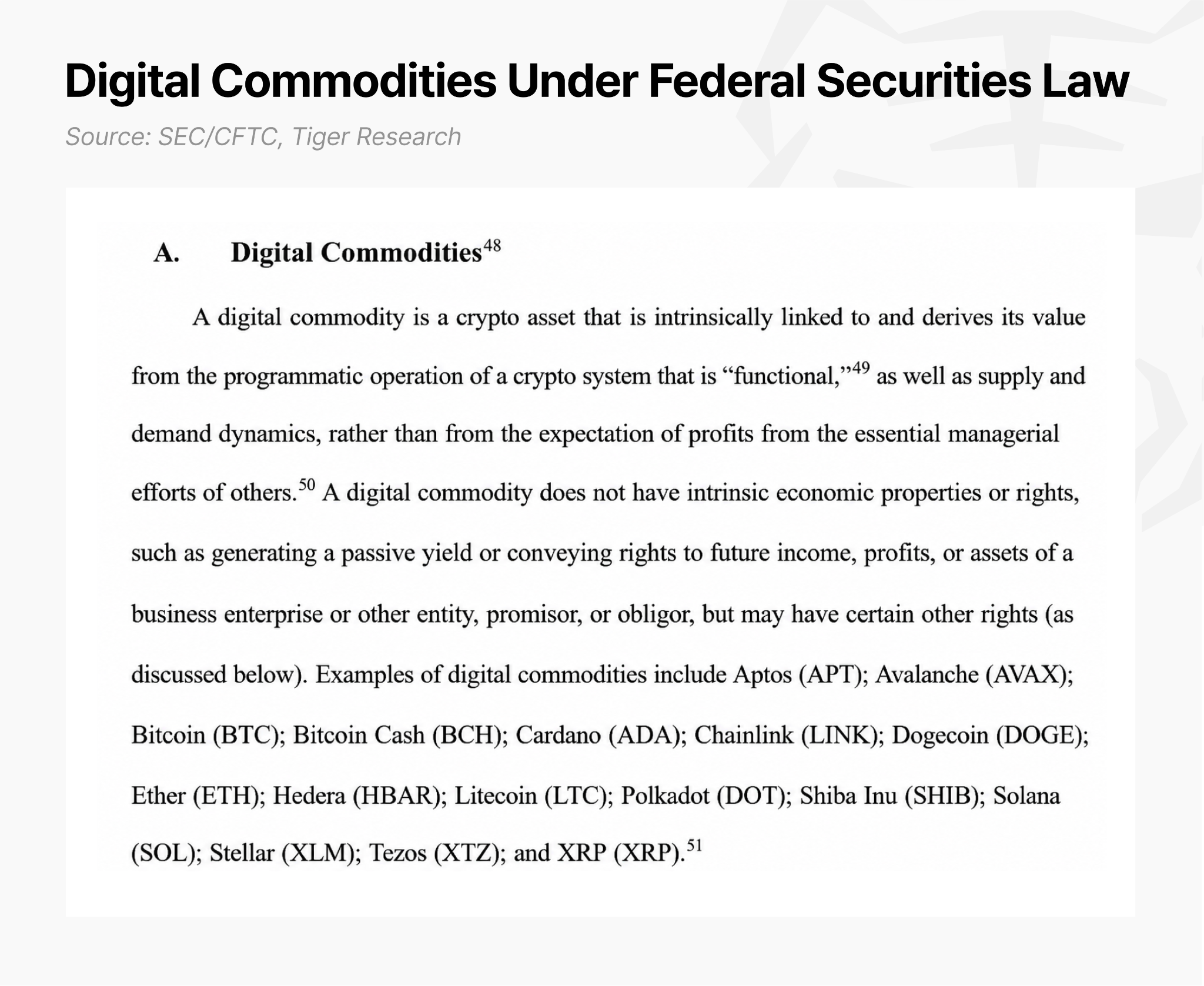

The United States is moving fastest to set the standard. Congress defined the legal status of stablecoins through the GENIUS Act, and in March 2026 the SEC and CFTC classified 16 assets, including Solana (SOL), as digital commodities, clearing much of the regulatory uncertainty that had been holding capital back. The pattern repeats: the jurisdiction that sets the standard sets the terms of the market, and that pattern is now playing out in the ICM.

Solana is the network where that shift is taking concrete form. It is accumulating both institutional case studies and regulatory design simultaneously. Major financial institutions, including J.P. Morgan, State Street, and Citi, have built cases on Solana. The Solana Policy Institute, established in Washington, DC, did not wait for rules to be finalized; it submitted the Project Open pilot framework directly to the SEC, building precedent rather than waiting for it.

As the standard consolidates in the United States, the window for Asian institutions narrows. The first-mover phase, in which every piece of infrastructure had to be designed from scratch, has already passed. The practical path now is to adopt proven infrastructure and regulatory references, reducing trial and error. For institutions whose home regulators are moving slowly, jurisdictions such as Singapore and the UAE, where frameworks are already in place, offer a route to engage with Solana’s validated model first.

The question of whether and on what timeline to engage remains a policy and risk judgment for each institution and its regulator. Among public chains, Solana has accumulated a significant number of institutional pilots and live transactions. This report does not benchmark it against private or permissioned ledgers.

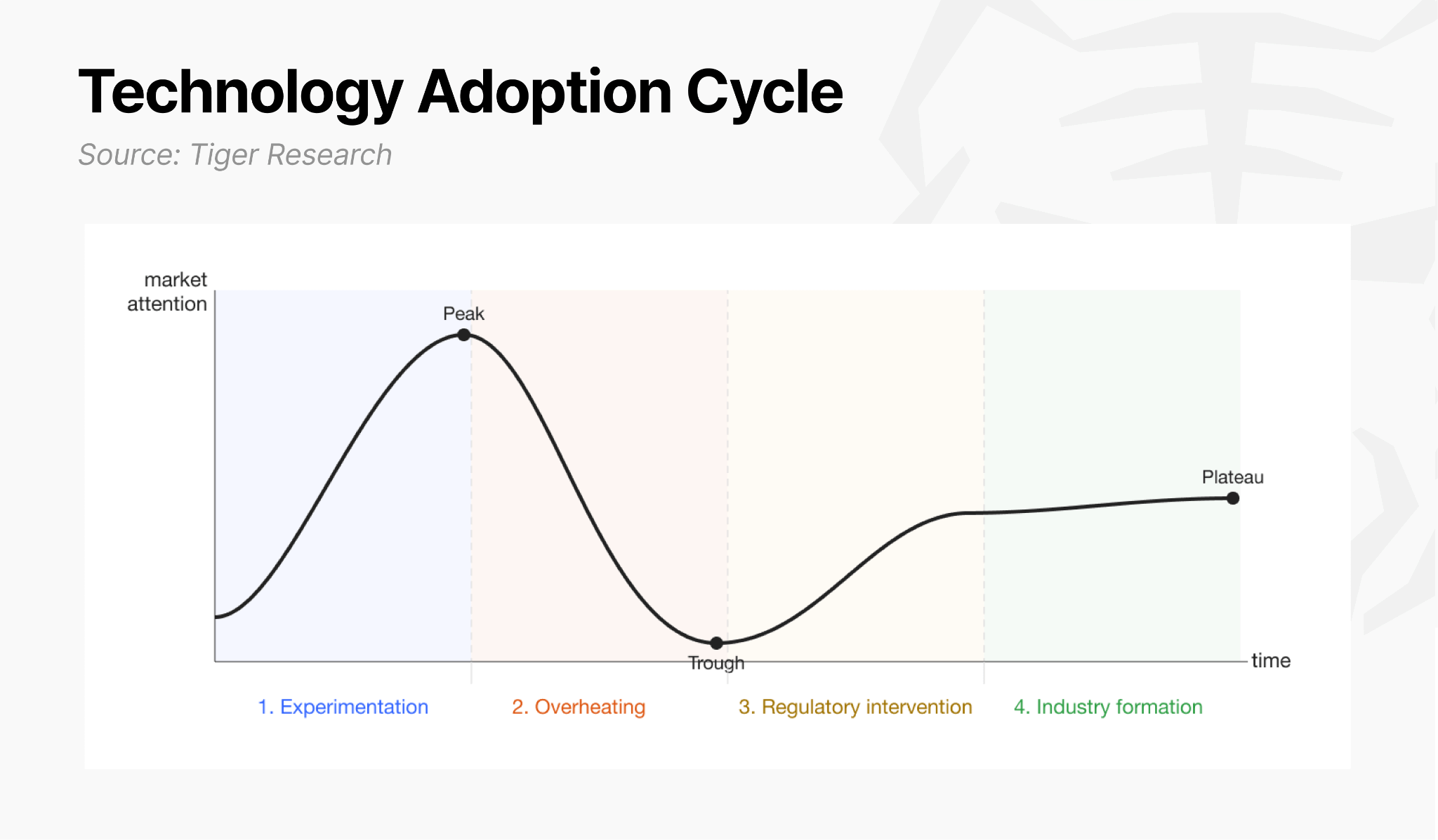

1. Crypto: From Experiment to Industry

New technologies generally move through a consistent set of stages as they pass from experiment to industry, as the internet, fintech, and AI each illustrate.

Experimentation: a small group of developers and early users validate the technology in a regulatory vacuum.

Overheating: as the potential becomes widely known, capital floods in and cycles of mania and collapse repeat.

Regulatory intervention: once the market reaches scale, authorities step in to set institutional boundaries.

Industry formation: as regulatory risk and practical utility are confirmed, the technology combines with existing industries to form an industry of its own.

The internet, the most prominent of these technologies, passed through experimentation in the 1990s and the overheating of the dot-com bubble, then settled into today’s industry as regulation and standards took shape after the bubble burst. Fintech moved from the experiments and investment frenzy of early startups into mainstream finance as governments built electronic-banking and simple-payment regimes. AI has passed the peak of expectations around generative models and now sits in the intervention stage, where governments are drafting regulatory frameworks. Each follows the same path from experiment to industry, differing only in pace and form.

Crypto today sits between the third and fourth stages. After Bitcoin appeared, a small group of developers tested its use for payment and settlement (experimentation). Investors rushed in and out each time the potential became visible, as in the 2017 ICO boom and the 2021 DeFi wave (overheating). The 2022 collapse of FTX was both the peak and the turning point. Through repeated collapses, speculative demand was filtered out and real use cases were proven, and once the market reached systemic scale, US regulators turned toward formalization rather than neglect or crackdown (regulatory intervention).

Because crypto seeks to replace the core financial functions of settlement, payment, and issuance directly, it met friction with conventional financial institutions and took longer to be absorbed. Only now has crypto reached the stage between regulatory intervention and industry formation.

On the regulatory side, there has been notable progress in recent years. The US Congress passed the GENIUS Act, which defined the legal status of stablecoins, and in March 2026 the SEC and CFTC confirmed 16 assets, including SOL, as digital commodities. Much of the regulatory uncertainty that had blocked capital has lifted. Core measures that would govern the overall market structure, including the CLARITY Act, remain under discussion.

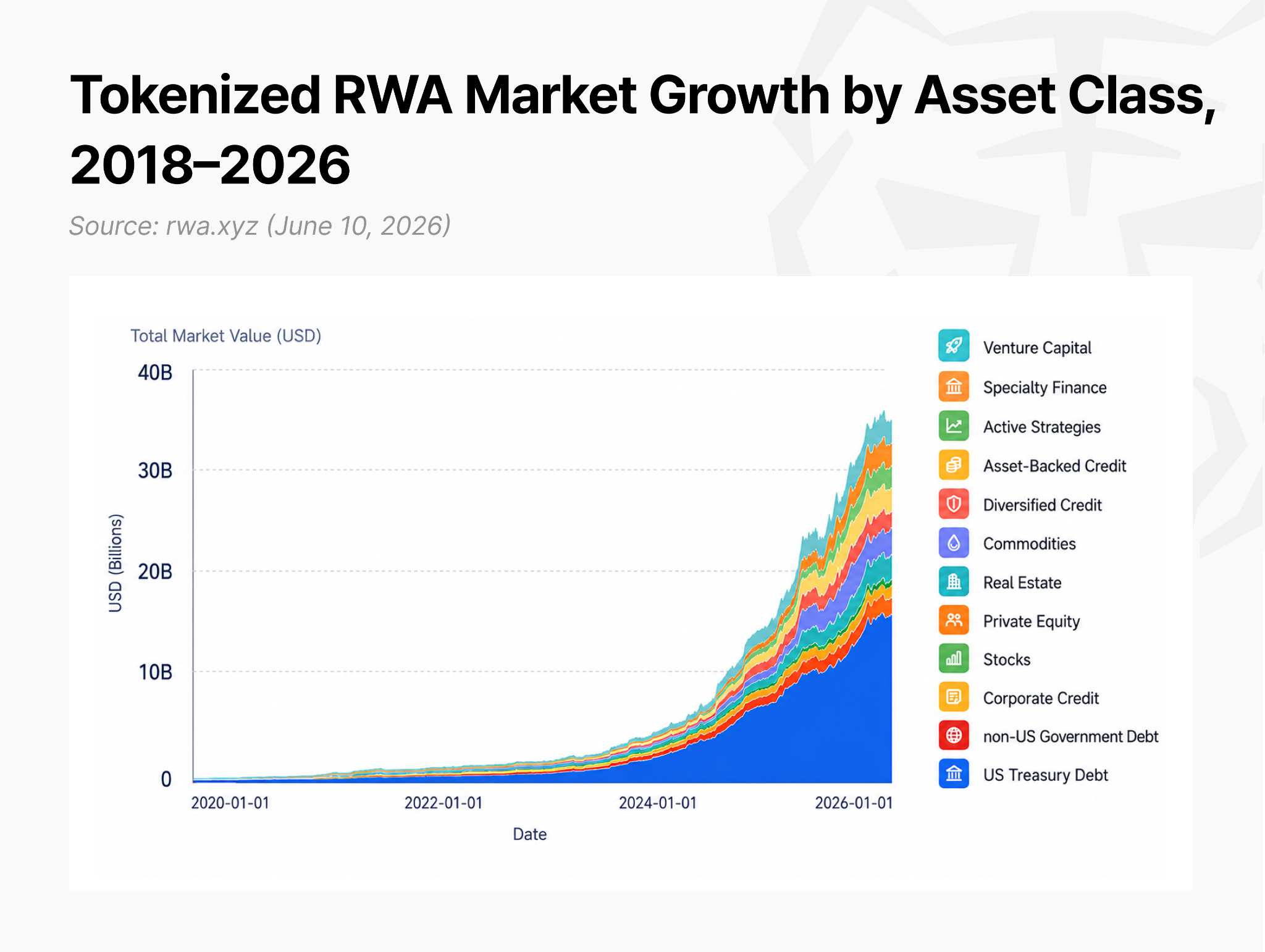

As the industry-formation stage begins, institutional adoption within the crypto landscape continues to increase. Asset managers are putting funds on-chain, and banks are settling funds on-chain. The tokenized real-world asset (RWA) market grew about 257% in 15 months, from $5.4 billion in early 2025 to $19.3 billion at the end of March 2026, and including stablecoins, on-chain assets reach roughly $300 billion (rwa.xyz, as of June 10, 2026).

This is not yet large enough to call a full-scale industry, but industry formation is beginning alongside the buildout of regulation.

2. The Future of the Crypto Industry: Internet Capital Markets (ICM)

The future toward which crypto is heading, now that it has entered the industry stage, is the reconstruction of the capital market itself. This future can be defined as Internet Capital Markets (ICM). It is a capital market in which the issuance, trading, and settlement of assets all take place on a single public blockchain.

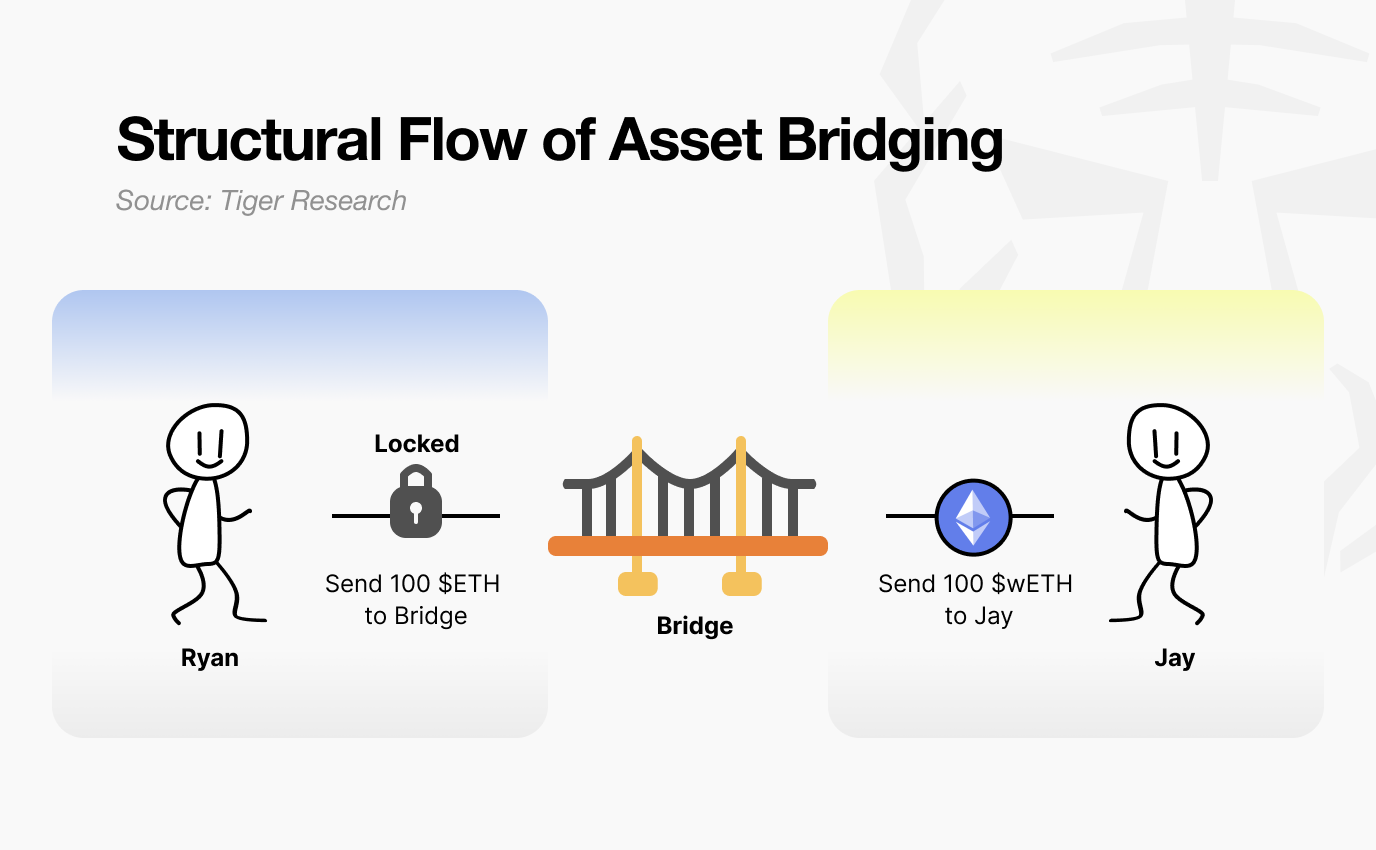

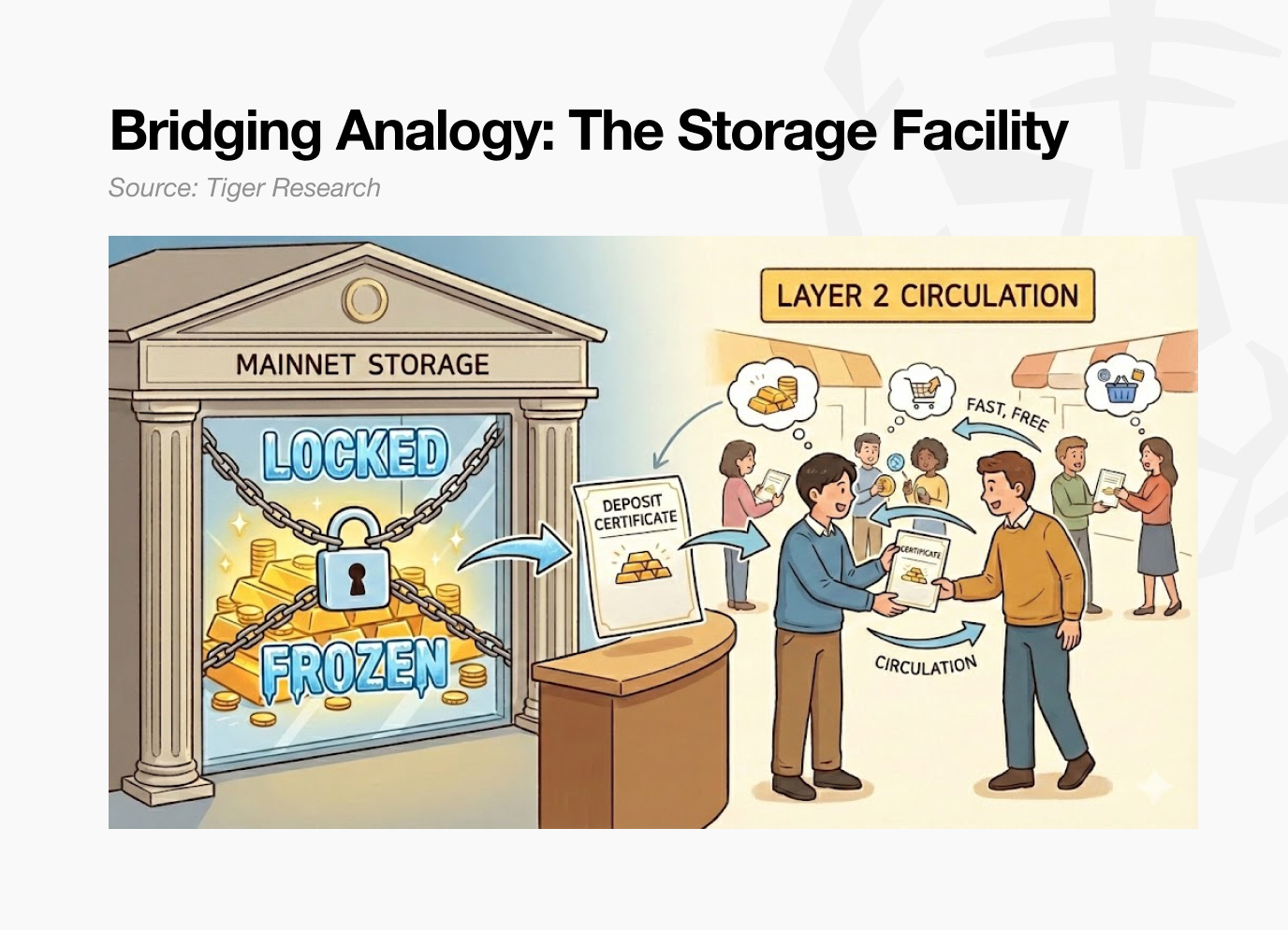

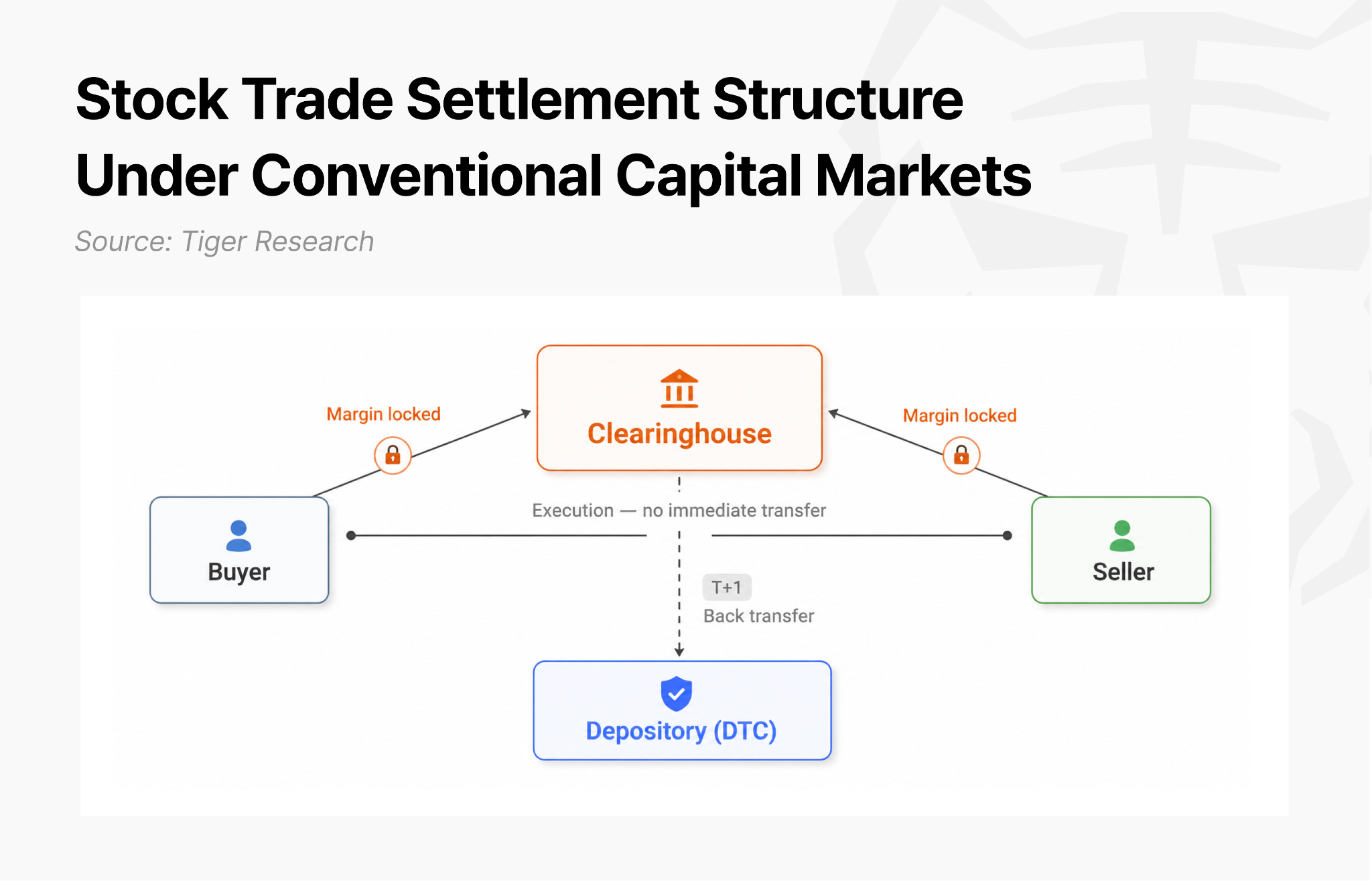

Today’s capital market runs on a structure designed before the internet. Buying and selling a single share is a clear example. At the moment of execution, the asset and the cash do not change hands immediately. A clearinghouse stands between buyer and seller and absorbs the risk that one side fails to perform before settlement. In return, the clearinghouse requires margin from both sides, and that money is locked until settlement completes. In the US, the book transfer at the depository is only finalized on the business day after execution.

Because brokers, exchanges, clearinghouses, depositories, and custodians each keep their own separate ledgers, they must check those ledgers against one another every business day to reconcile them, and any discrepancy delays settlement. For cross-border trades, currency conversion and the depositories of each country are added, so settlement can stretch to T+3 or longer. This structure was designed for an era when counterparties could not be trusted, and that design is now itself a cost.

In Internet Capital Markets, code takes over the role the clearinghouse played. The buyer’s payment and the seller’s asset are placed into a smart contract at the same time, and the two transfers execute as a single transaction. If either side’s condition is not met, the entire transaction is canceled. A case where only the buyer’s payment leaves or only the asset transfers cannot occur technically. Because counterparty performance risk is removed at the level of code, no clearinghouse is needed to require margin. Because all participants share the same ledger in real time, there is no reconciliation between institutions. Execution and settlement complete together within seconds.

The actors driving this change are expanding from crypto startups to conventional financial institutions. The very institutions that earned revenue from the layered intermediation structure are now taking part. This movement reflects a pattern in which, at each tipping point, institutions that followed late paid higher costs or lost their leading position.

The shift to electronic trading in the 1990s is a clear example. Large institutions built on floor trading initially resisted electronic platforms such as Island ECN and Instinet, and only after these became the standard did they follow late, through acquisition and absorption. The fintech shift followed the same pattern. Only after digital banking had taken their customers did conventional banks launch their own apps or acquire fintech firms. Each time they faced the same choice, to design the new infrastructure and redefine their role, or to accept a structure designed by others. Infrastructure replacement that has passed the tipping point is hard to reverse, and institutions are moving because they know that cost.

This change is happening fastest in the US. As the center of global capital markets, the US has shown through history that whoever sets the standard in financial infrastructure designs the market.

After the dollar became the reserve currency under the 1944 Bretton Woods system, trade and financial transactions worldwide were priced and settled in dollars. CHIPS, designed by US private banks, processes more than $2.2 trillion in domestic and international payments each business day, and the NYSE and Nasdaq serve as the reference venues where global companies raise capital (The Clearing House, June 2026). The SEC’s disclosure standards became the reference for capital-market regimes in other countries. Whoever set the standard defined the terms of the market, and the rest had to follow their rules.

The US is working to create the same pattern in Internet Capital Markets, and that movement has already begun. It established regulatory standards first, and on top of them institutions have begun building cases. More than 99% of stablecoins worldwide are dollar-denominated, and the base unit of on-chain transactions is also the dollar (rwa.xyz, June 10, 2026).

In the RWA market, US Treasuries came on-chain earliest and in the greatest volume, and large global financial institutions began their on-chain practice earlier in the US. The range of assets eligible for tokenization, the settlement standards, and investor-protection requirements are all being decided first in the US.

Asia is aware of this change as well. Financial authorities in Singapore, Hong Kong, and Japan are building out digital-asset regulatory frameworks, and large institutions in the region have begun to consider adopting on-chain infrastructure. The US is clearly ahead, however, in the pace of regulatory clarity and the density of institutional practice references.

This is why Asian institutions are increasingly visiting the US in person. An institution that does not take part in the process of forming the standard ends up having to accept the finished standard. The change has become a question not of whether to act but of how quickly.

3. Internet Capital Markets in Practice: Solana

The network that shows a concrete implementation of US Internet Capital Markets is Solana. Within a single ecosystem, the building of institutional practice references and the design of the regulatory framework are proceeding at the same time.

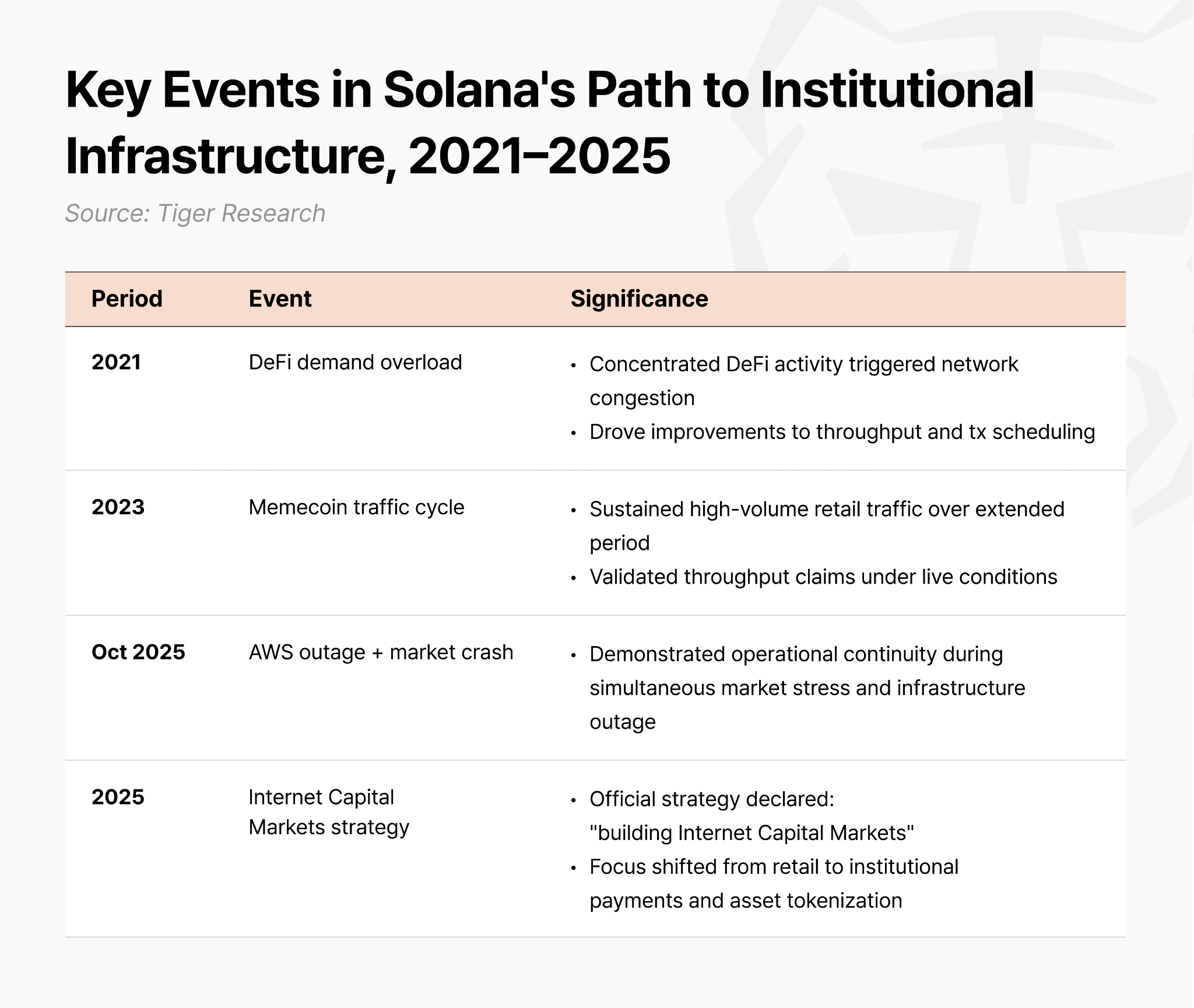

Solana built its technical foundation in the retail market. It treated the network overload caused by concentrated DeFi demand in 2021 as an occasion to improve performance, and it proved its throughput and stability by handling the heavy traffic of the 2023 memecoin cycle.

In October 2025, when a market crash coincided with an AWS outage, fees on other chains rose to as much as $100 per transaction while Solana operated without interruption at $0.0013 per transaction. The infrastructure stability that institutional finance requires was secured first through stress tests in the retail environment.

In 2025, Solana declared “building Internet Capital Markets” as its official strategy and shifted its focus to institutional payments and asset tokenization. The Token-2022 standard introduced for this purpose embeds seizure, freezing, allowlist management, and confidential-balance functions as code in the token itself. An issuer can implement compliance requirements inside the token without going through an external system. It resolves finance’s essential requirements for eligibility to hold and trade assets at the protocol layer.

On this infrastructure, US financial institutions carried out working transactions. Seven large institutions, J.P. Morgan, State Street, Citi, Franklin Templeton, Visa, PayPal, and Western Union, have initiated PoC or have executed working transactions on Solana. This includes three of the eight US global systemically important banks (G-SIBs).

At the same time, Solana made its participation in regulatory design concrete. The Solana Policy Institute (SPI), founded in Washington, DC, in spring 2025, recruited the former CEO of the DeFi Education Fund and the former CEO of the Blockchain Association and is carrying out policy work.

Notably, instead of waiting for legislation to pass and reacting afterward, SPI chose to submit a pilot framework called Project Open directly to the US Securities and Exchange Commission (SEC). The strategy is to propose a regulatory precedent first and thereby advance both business diversification and the setting of regulation at once.

Solana is thus pursuing technical stability, the building of working cases by large institutions, and the setting of regulatory standards at the same time within a single ecosystem. This is why Solana is identified as core infrastructure when reading the current structure and the future regulatory direction of US Internet Capital Markets.

4. Institutions on Solana: Sector Case Analysis

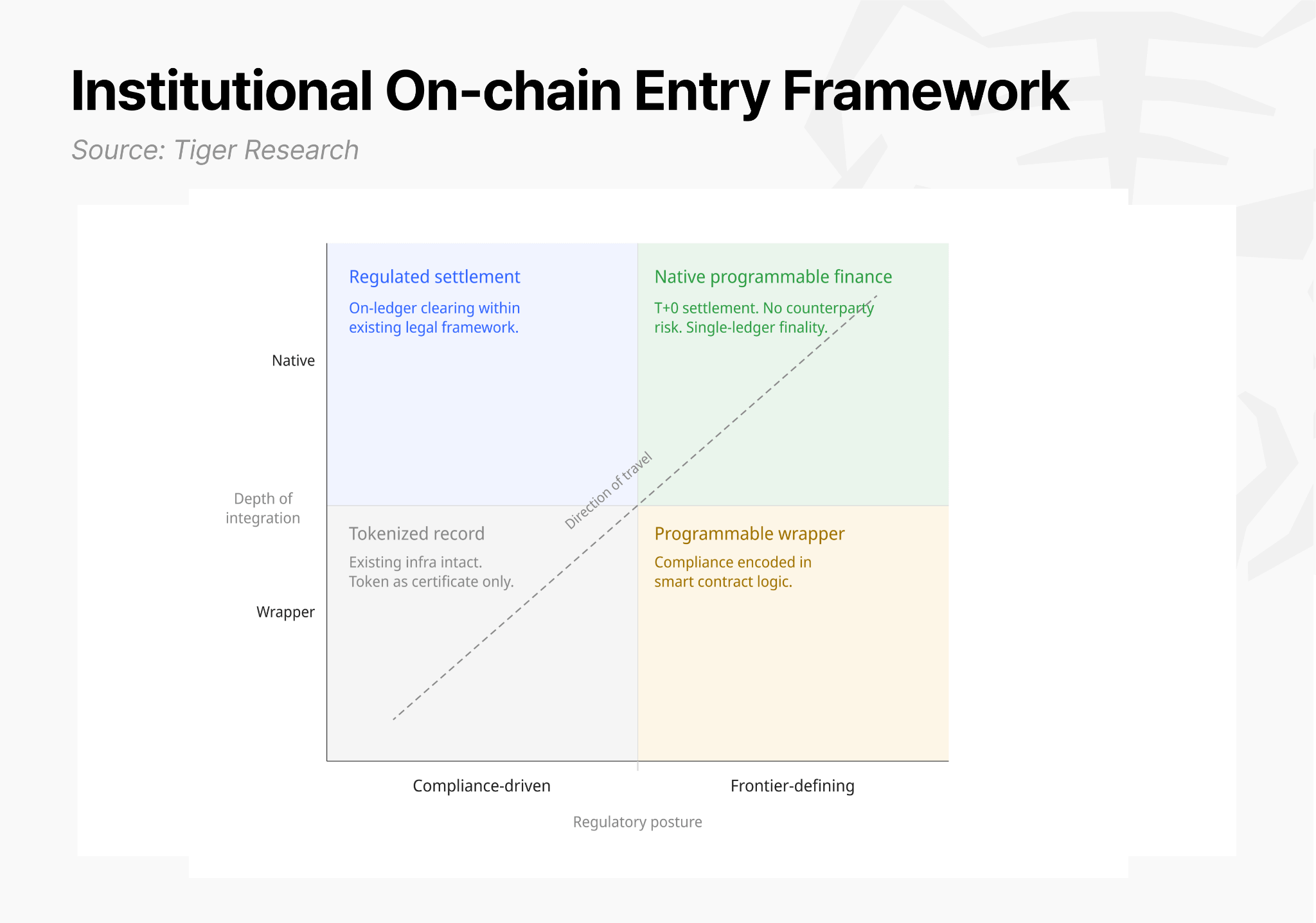

Institutional engagement with Solana-based Internet Capital Markets is developing across multiple fronts, though not all participants share the same objective. Entry strategies vary considerably depending on each institution’s strategic priorities and operating constraints. Making sense of this layered activity requires an analytical framework built around two core axes.

First axis: Regulatory posture

Compliance-Driven: Institutions in this category work within established regulatory frameworks, accepting existing legal guidelines to achieve capital efficiency quickly. J.P. Morgan’s same-day settlement of commercial paper is representative.

Frontier-Defining: Institutions in this category operate in areas where clear rules do not yet exist, encoding compliance requirements directly into smart contracts through programmable compliance and establishing new precedent in the process. Orca’s permissioned pool illustrates this approach.

Second axis: Depth of value chain integration

Wrapper: The entry-level stage, in which existing financial infrastructure remains in place and the token functions as a simple certificate of record.

Native: The advanced stage, in which issuance, clearing, and settlement all complete on a single ledger. Intermediary structures are replaced by smart contracts, enabling T+0 settlement and eliminating counterparty performance risk.

Together, these two axes form a matrix that provides a clear reference point for assessing where institutions stand in their on-chain positioning. This report maps that framework across four functional areas of the capital markets to examine which cost structures and constraints of conventional infrastructure each institution has addressed, and what strategic conclusions follow from those choices.

The four sectors are: 1) banking and capital markets, 2) payments and stablecoins, 3) real-world asset tokenization (RWA), and 4) infrastructure buildout.

4.1 Banking and Capital Markets

The banking and capital markets sector covers bond issuance, trade finance, and treasury management. It is the set of processes by which institutions raise funds, send and receive trade payments, and put idle capital to work. It is a core revenue source for conventional financial institutions and the area where the cost savings from the shift to Internet Capital Markets appear earliest and most directly.

All three areas in this sector share the same critical problem. There is a time gap between the moment a trade is executed and the moment the funds actually move, that is, settlement.

Bond issuance: completing an issuance requires the arranger, clearinghouse, depository, and custodian each to record their own ledgers separately and then cross-check them afterward, a complex manual process.

Trade finance: processing a single bill of exchange consumes days to weeks before funds are disbursed, as the issuer, bank, guarantor, and payee verify the ledger in sequence.

Treasury management: large idle funds held by an institution stay locked in the system, unable to convert into yield-bearing assets outside standard business hours, which is why liquidity freezes at night and on weekends.

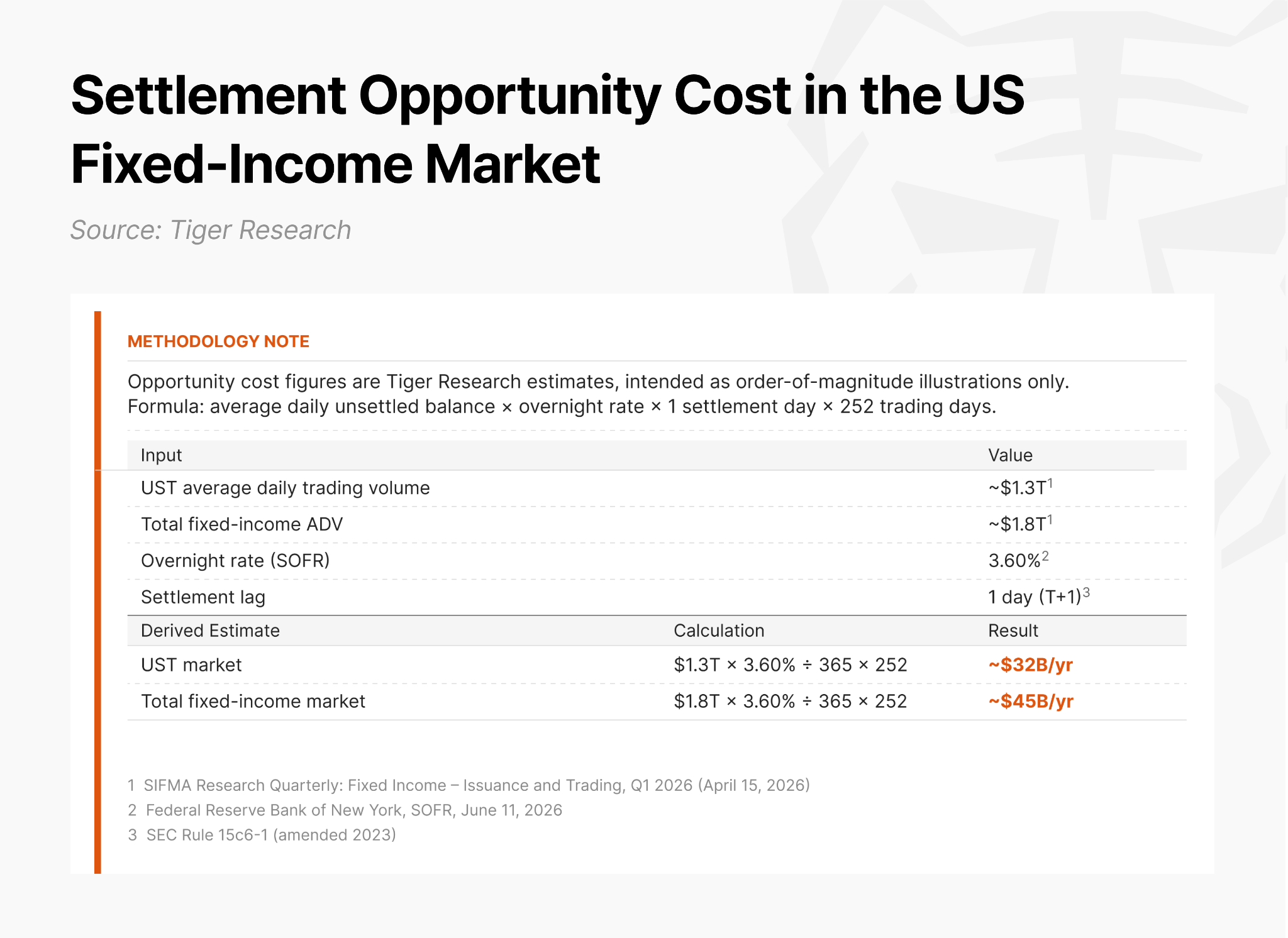

In a high-rate environment, this settlement delay creates a large opportunity cost by tying up funds across the capital market. During a one-day settlement gap (T+1), substantial funds sit idle in the infrastructure and cannot move.

By our analysis, the cost of capital left idle because of this delay reaches approximately $32 billion a year in the US Treasury market alone, and widening the view to the entire US fixed-income market, the annual opportunity cost exceeds $45 billion. In effect, the speed limits of the existing financial system impose large hidden costs on market participants.

On Internet Capital Markets infrastructure, this chronic time gap disappears. This is due to atomic settlement, known as delivery versus payment (DvP), in which the asset transfer and the payment are bundled into one transaction and processed in real time. Because if one side of the trade is not performed the other side does not execute either, the clearinghouse that absorbed performance risk in the middle is no longer needed, and the reconciliation process that each institution ran separately disappears. As a result, execution and clearing complete within seconds (T+0).

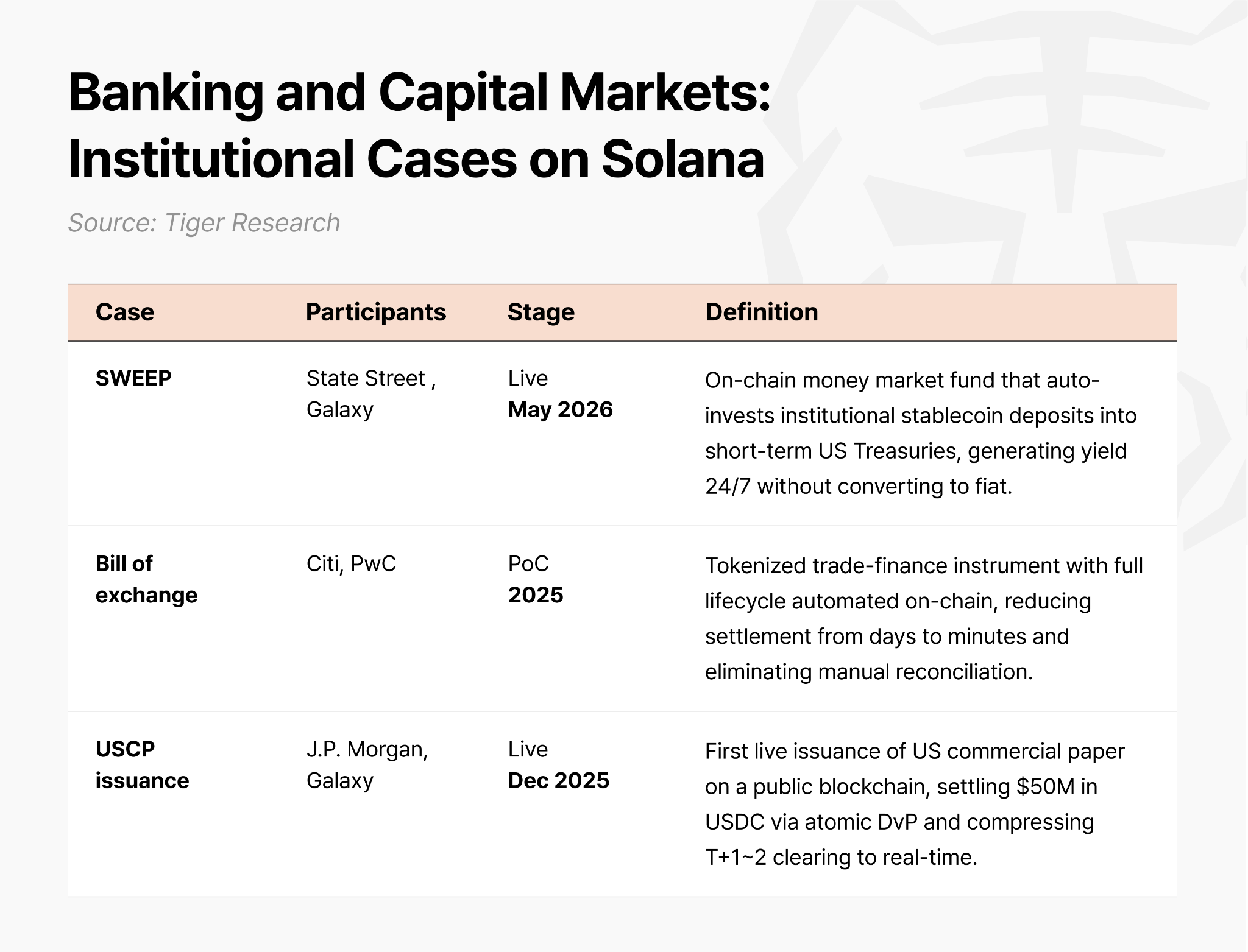

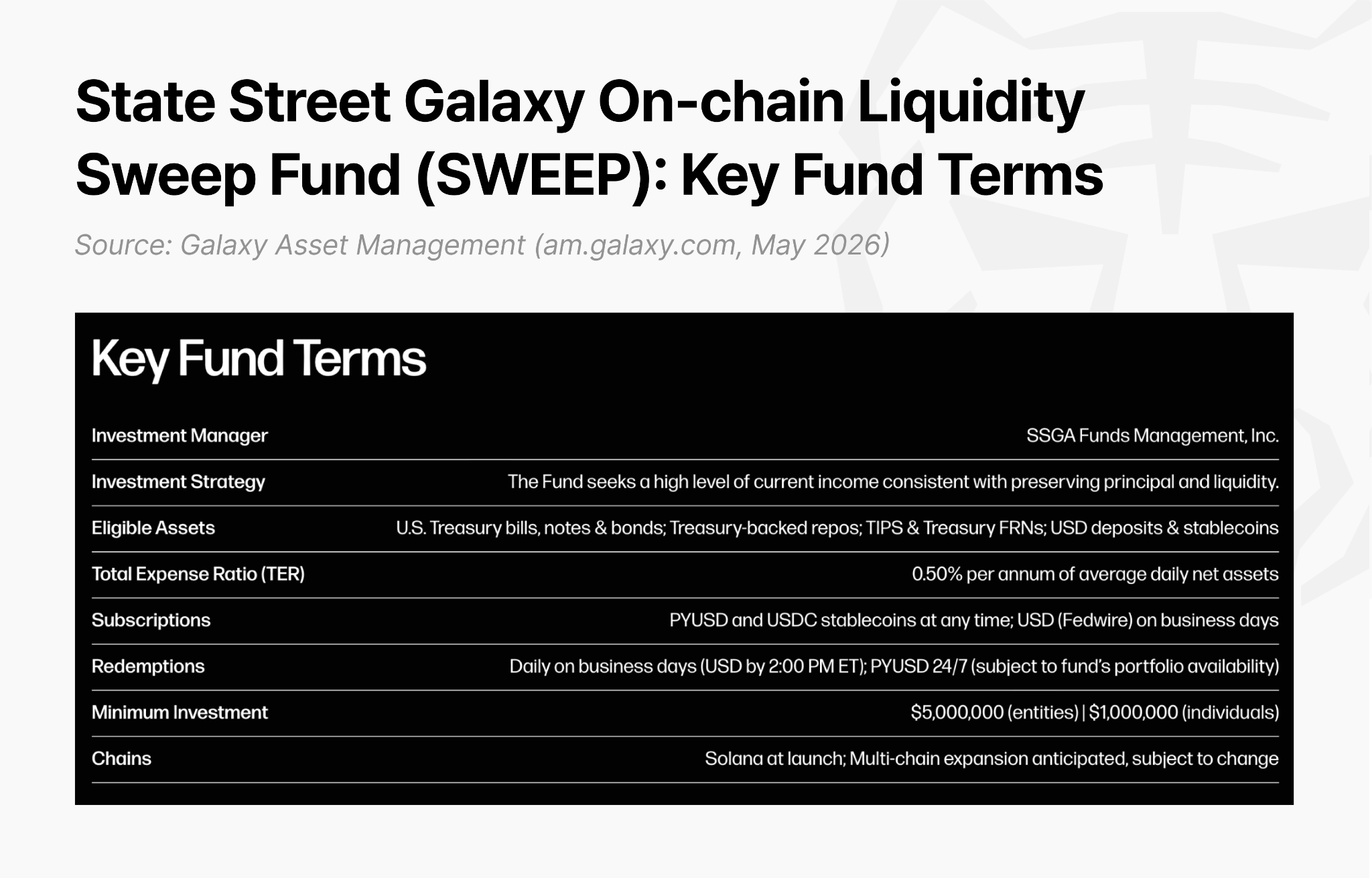

State Street x Galaxy: On-Chain Treasury Management (SWEEP)

Launched on Solana on May 5, 2026, the State Street Galaxy On-chain Liquidity Sweep Fund (SWEEP) is an on-chain fund for institutional investors that takes in stablecoins (PYUSD, USDC) or fiat currency and invests in safe assets such as short-term US Treasuries to generate yield. Leading institutions from conventional finance and the Web3 ecosystem established a structure of separated custody and operation based on their respective expertise, raising reliability. The specific division of roles is as follows.

State Street: handles custody of conventional assets such as short-term US Treasuries and fund administration, bringing established asset-management capability to the on-chain environment.

Galaxy Digital: as a financial firm specializing in digital assets, leads the fund’s issuance and the structuring of on-chain liquidity.

Anchorage Digital: as a regulated digital-asset custodian, is responsible for the secure, separated custody of on-chain assets, namely stablecoins and the issued tokens.

As its name shows, the fund draws on the sweep account concept from conventional finance. A sweep account is a financial service that automatically invests a company’s or institution’s funds in short-term bonds or MMFs to earn yield once the funds are deposited. SWEEP implements this delegated treasury function as an on-chain fund on the blockchain, supporting institutions’ advanced treasury management.

It is a new opportunity in particular for Web3 foundations that hold large amounts of stablecoins. Under existing infrastructure, using conventional financial services required converting stablecoins into dollars first before subscribing, which incurred friction costs in the form of conversion and transfer fees and unnecessary time delay.

In a future macro environment where the global stablecoin supply is expected to expand further, SWEEP enables direct deposits into and withdrawals from a Treasury-yield asset from an institution’s wallet, with issuer-controlled eligibility enforced on-chain.

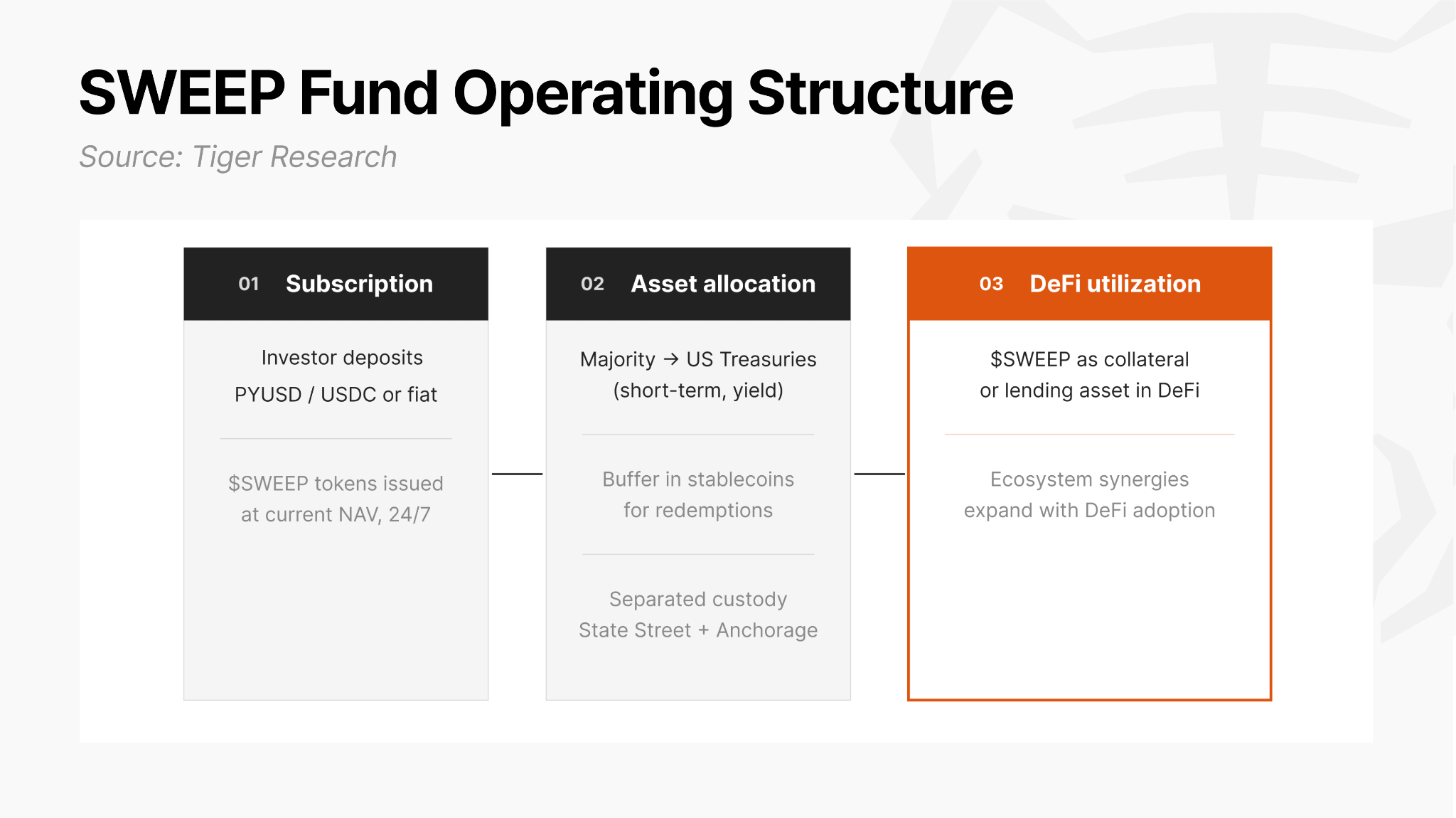

Treasury management is of course possible through Treasury-tokenization products such as BlackRock’s BUIDL or Franklin Templeton’s BENJI, but simply investing in a single asset and automated treasury management, in which the system manages the funds on its own, differ clearly in capital efficiency. SWEEP operates in three stages.

Stage 1, subscriptions: around the clock, when an investor deposits stablecoins (PYUSD, USDC) from an on-chain wallet or transfers dollars, SWEEP tokens are issued in proportion to the value at that moment.

Stage 2, asset allocation: most of the deposits are invested in safe assets such as short-term US Treasuries to produce steady yield. At the same time, a set portion is held as a liquidity buffer in stablecoins so the fund can meet redemption requests at any time, with State Street holding the conventional assets and Anchorage Digital holding the on-chain assets in separated custody.

Stage 3, DeFi utilization: the issued SWEEP tokens are used as collateral or lending assets in external DeFi protocols to mobilize capital further. The specific uses and synergies here will diversify with how the connected DeFi ecosystem expands.

As an example, Ondo Finance’s flagship fund OUSG made an anchor investment of approximately $200 million in SWEEP at launch, representing around 26% of its TVL at the time (State Street IR, December 2025). This commitment reflects confidence in the asset’s reliability as an on-chain cash management product, and as that utility becomes more firmly established, synergies within the ecosystem are likely to broaden.

The key point is that, on Solana, this is not merely a proof of concept (PoC) but a commercial-proof stage in which real, large-scale capital is moving. Asian institutions, many of which remain at the pilot stage, can treat this as a live-operation reference point for the next-generation infrastructure they are building.

For such a proven system to operate, however, the regulatory groundwork must come first. In the end, what matters is not a technology race but the pace at which regulation is formalized. In Asia, the timing of an equivalent product depends on when each jurisdiction establishes the legal basis for locally regulated stablecoins and on-chain Treasury management.

Citi x PwC: Tokenizing Trade Finance (Bill of Exchange)

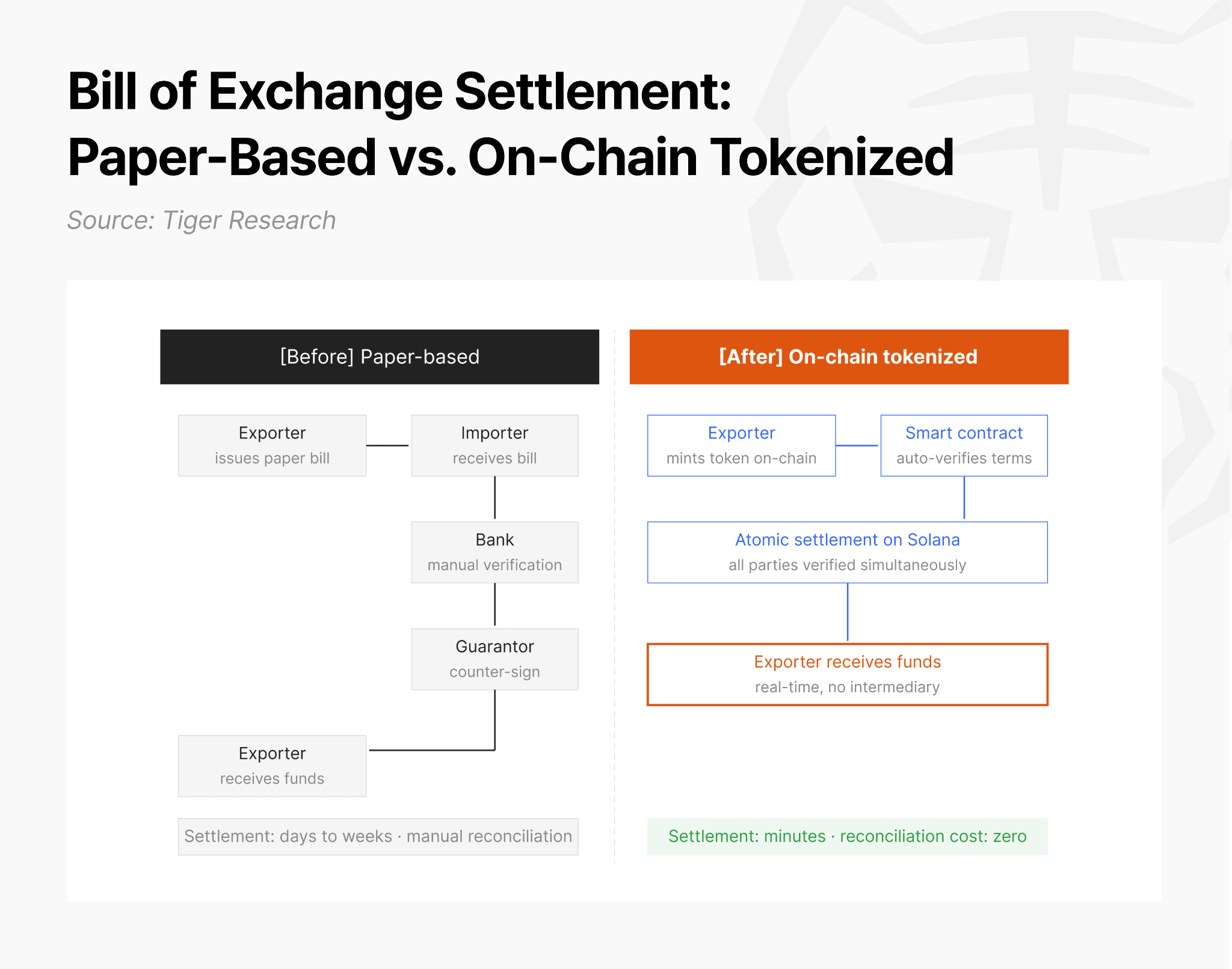

Existing trade finance has kept a low-efficiency structure in which funds take days to weeks to be disbursed, passing through extensive paper documentation and multiple layers of intermediaries. The time delay and intermediary fees in this process have been a main drag on companies’ asset productivity and a major obstacle to gaining visibility into the cash flow that disbursement depends on.

The bill of exchange, central to international trade, is a security through which an exporter demands payment from an importer and a key credit-settlement instrument. In effect, after shipping goods, the exporter issues a document to the importer specifying a payment deadline. Because the exporter can present this document to a bank and borrow against it before maturity, it serves as one of the most important means of securing trade financing. Reducing the time it takes to process this bill of exchange is therefore central to corporate cash-flow management.

Under the current paper-based system, however, a physical time gap arises at every step as the bill moves back and forth and the bank verifies it before paying out, so funds inevitably get tied up. If this bill of exchange could be verified and circulated instantly on a digital ledger, a company could secure the cash it needs in real time without waiting.

To resolve this structural capital friction and test the possibility of supplying real-time liquidity across the supply chain, Citi worked with PwC and Solana to complete an internal proof of concept (PoC) that converts a conventional bill of exchange into a tokenized digital asset. The roles of the participating institutions are as follows.

Citi: led the project and designed and ran the full on-chain lifecycle of the bill of exchange (issuance, financing, circulation, and settlement) in a simulation environment.

PwC: as a collaborating partner, supported the project’s simulation process throughout.

In the simulation environment built on this collaboration, the full lifecycle of the bill of exchange is automated through smart contracts on Solana rails. By streamlining the complex conventional process on-chain, settlement time that previously took days was reduced to minutes, and the cost of manual reconciliation was recorded at zero, according to the participants.

The case is significant for demonstrating that the bill-of-exchange settlement cycle, the oldest bottleneck in trade finance, can be shortened to minutes and the manual reconciliation process removed. It is a key indicator of how far tokenizing off-chain assets can raise the liquidity of corporate treasury assets and the efficiency of treasury management.

Because this project is at the stage of an internal PoC in a simulation environment, the move to actual commercial operation will likely take time.

The structure carries strong implications for Asian finance, where global trade hubs are concentrated. For regional institutions preparing to adopt next-generation supply-chain finance and trade capital markets, the technical results of this PoC and its ledger-integration mechanism will serve as a concrete reference for how to build on-chain infrastructure.

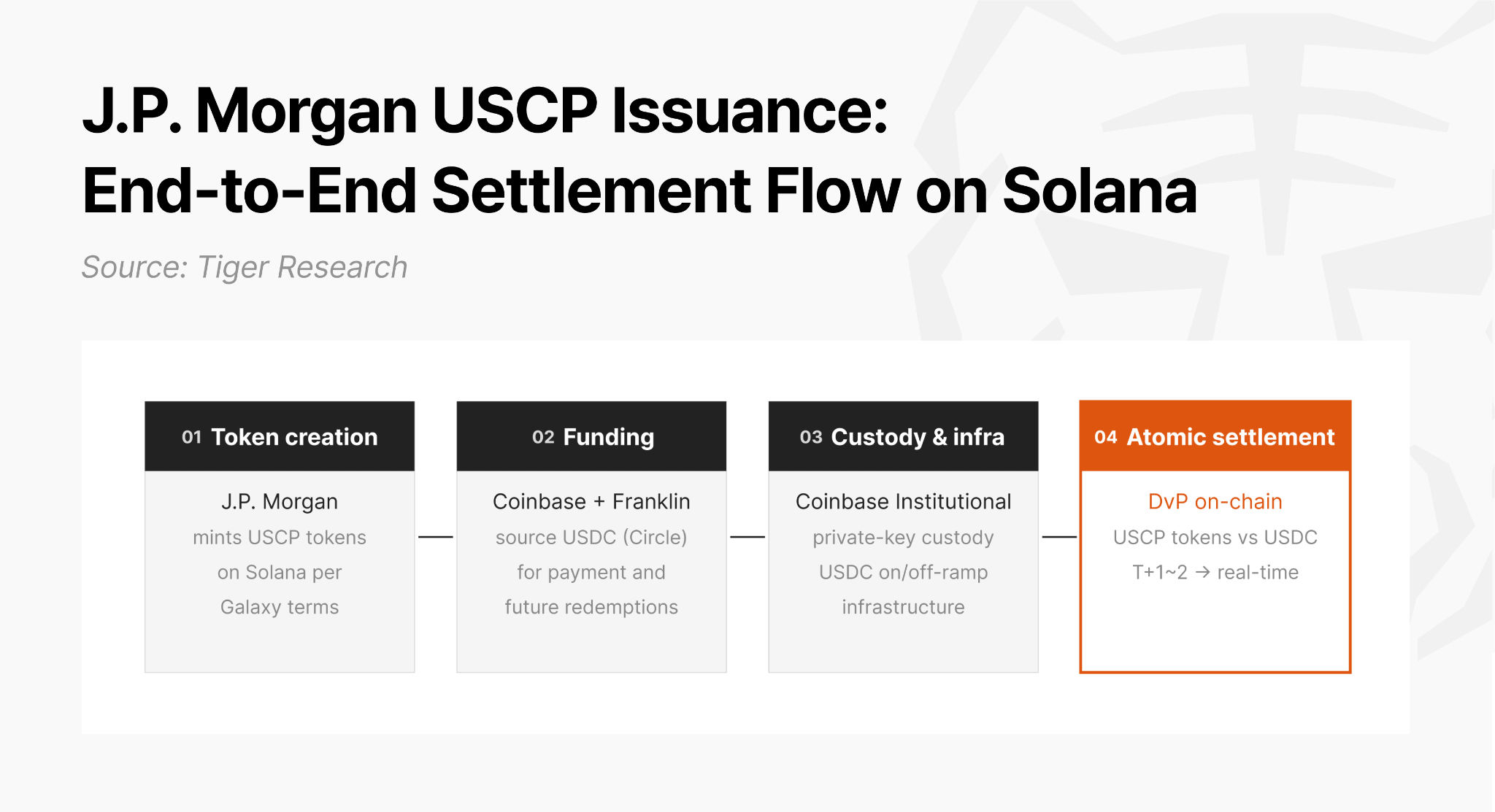

J.P. Morgan x Galaxy: Issuing Commercial Paper (USCP)

US commercial paper (USCP) is the most widely used instrument for companies raising short-term operating funds. The existing issuance and trading and liquidity infrastructure carried a structural inefficiency. Because they had to pass through multiple intermediaries such as clearinghouses and custodians, the funds arriving and the books matching, that is, settlement and reconciliation, normally took one to two days (T+1 to T+2).

To resolve this friction, in December 2025 J.P. Morgan arranged a $50 million issuance of US commercial paper on the Solana public blockchain. This was not a simple simulation (PoC) but among the first live debt-security transactions on a public blockchain, completed by combining real institutional capital with stablecoin (USDC) settlement. The division of roles among participants was clear, as follows.

J.P. Morgan (arranger): as arranger, created the USCP tokens directly on the Solana blockchain and oversaw the atomic settlement of the primary issuance.

Galaxy (issuer and structuring agent): the parent, Galaxy Digital Holdings LP, served as the actual issuer of the paper, while its investment-banking affiliate, Galaxy Digital Partners LLC, acted as structuring agent, keeping the two roles clearly separated.

Coinbase and Franklin Templeton (buyers and infrastructure support): Coinbase and Franklin Templeton stepped in as lead investors and buyers. Coinbase in particular provided private-key custody and wallet services for the newly issued USCP tokens and handled the USDC on/off-ramp infrastructure.

By combining this stablecoin payment network with on-chain atomic settlement (DvP), J.P. Morgan was able to turn a corporate funding cycle that took days on the existing financial network into an immediate, real-time settlement system.

Stage 1, token creation: following the terms designed by the structuring agent (Galaxy Digital Partners LLC), the arranger J.P. Morgan created the on-chain USCP tokens directly on the Solana blockchain.

Stage 2, funding: the lead investor Coinbase and the buyer Franklin Templeton sourced the stablecoin (USDC) issued by Circle to pay for the paper and prepare settlement. Future redemption payments are also made in USDC.

Stage 3, custody and infrastructure: Coinbase Institutional provided private-key custody and wallet services for the newly issued USCP tokens and handled the USDC on/off-ramp infrastructure essential to live settlement.

Stage 4, on-chain atomic settlement: under J.P. Morgan’s arrangement, the delivery of the USCP tokens and the payment of USDC were processed as atomic settlement (DvP). The clearing process that normally took T+1 to T+2 through multiple intermediaries completed instantly on-chain.

Unlike Citi’s trade-finance PoC discussed earlier, this case carries practical weight because it was a live transaction that completed the entire process, from issuance to redemption, in a real market with real institutional capital. Together with the earlier on-chain treasury-management case (SWEEP), the completion of this live transaction shows directly that bond issuance, a core function of conventional capital markets, has entered commercial operation through on-chain atomic settlement (DvP) without passing through the complex existing clearing system. Because it goes beyond merely tokenizing an asset and connects the raising and settlement of real capital into one flow, this case is a representative example of Internet Capital Markets and will be a key benchmark for Asian financial institutions preparing the next step.

4.2 Payments and Stablecoins

The payments and stablecoins sector is defined as the financial-infrastructure area that covers cross-border remittance, business-to-business settlement, and consumer payments. It refers to the set of processes by which individuals send money abroad, companies and institutions pay overseas counterparties, and consumers buy goods.

This sector is a major revenue source for conventional financial infrastructure and also the area where structural inefficiencies such as speed delays and intermediary fees accumulate most widely in the daily life of individuals and companies. The introduction of blockchain and stablecoins centers on reducing this multilayered intermediation and building a real-time settlement system.

Cross-border remittance bottleneck: the adoption of Swift GPI (Global Payment Innovation), the global standard network that improved the processing speed and tracking visibility of overseas transfers, has cut transfers between large banks to within a few hours, but transfers that route through small and midsize institutions or settle in exotic currencies still have to pass through a multilayered correspondent-bank network. The intermediary fees that arise here, in the range of $30 to $100 per transaction, and the intermittent delays from AML/CFT compliance review are a practical bottleneck that undermines the predictability of cross-border fund movement.

Fragmented liquidity in corporate settlement: to manage settlement-timing differences across currencies and foreign-exchange (FX) volatility, global companies must keep local-currency funds distributed at all times in the deposit accounts (nostro accounts) of correspondent banks in each country. This is not a shortcoming of payment technology but a structural limit of the established banking system, and in a high-rate macro environment it lowers capital efficiency by leaving large amounts of capital idle and earning no interest.

Limits of payment availability: retail payment networks (Visa, Mastercard) appear to run in real time 24/7, but that is limited to the front-end authorization step. The final clearing and settlement, where actual funds move between financial institutions, are processed only under the established banks’ business-day (nine-to-five) schedule, so during the two-to-three-day gap on weekend or holiday payments, merchants and financial firms bear the liquidity shortfall and credit risk entirely.

In a high-rate macro environment, these structural time gaps in the conventional financial network deepen liquidity isolation and opportunity cost. Solana-based on-chain infrastructure, by contrast, combines a single distributed ledger with stablecoins to achieve real-time settlement without intermediaries, minimizing capital friction. The concrete commercial cases that established finance and big-tech firms have built on these rails are as follows.

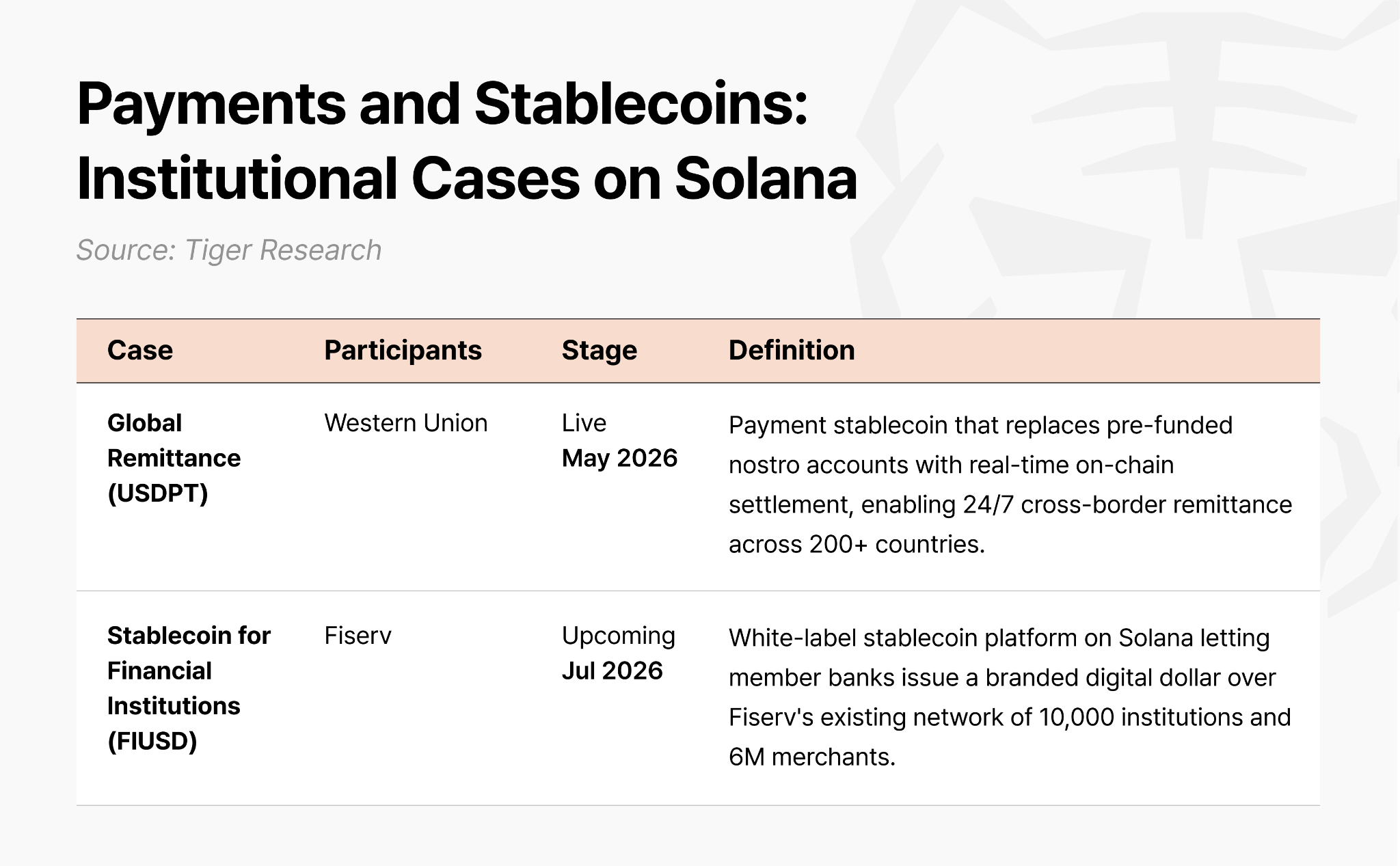

Western Union: Global Remittance (USDPT)

On May 4, 2026, the global remittance company Western Union launched USDPT (US Dollar Payment Token), a payment stablecoin pegged to the US dollar. It is a proof case that aims to solve, on Solana public-blockchain rails, the chronic settlement gap of the existing correspondent-banking system and the problem of deposits frozen to guard against FX risk. The existing correspondent-banking system works as a multilayered structure in which an international transfer starts at the originating bank, passes through one or two correspondent banks, and then reaches the receiving bank.

The problem is that each intermediary bank processes only within its own system and business hours, so settlement normally takes one to two business days. On weekends and holidays, all processing stops. To respond immediately to real-time payout requests in each base country, the company therefore has to lock up dollars in local bank accounts in advance, sized to forecast demand.

These pre-funded nostro account balances sit locked, earning nothing, until a transfer occurs. For a company like Western Union, which over 175 years has processed about $150 billion in remittances a year across more than 200 countries, this cost of stuck liquidity has been structurally hard to resolve.

Western Union: oversees the project and integrates its own agent-network clearing system with the digital-asset network infrastructure.

Anchorage Digital Bank N.A.: as a custodian and issuer chartered by the US Office of the Comptroller of the Currency (OCC), handles OCC-chartered, 1:1 USD-backed issuance of USDPT, with KYC/eligibility enforced on-chain.

Crossmint: as the infrastructure partner, supplies the technical infrastructure for issuing and distributing USDPT through an enterprise minting API and distributed-custody rails.

Western Union’s adoption of USDPT fundamentally redesigns the settlement process to break through these bottlenecks. Adopting the Solana public blockchain and USDPT shifts the settlement paradigm from a structure that stockpiles funds in advance to one that supplies them in real time when needed.

Stage 1, real-time demand detection: when an agent’s cash inventory in a particular country, for example an emerging market where transfer demand spikes on weekends, falls below a threshold, a real-time alert is generated in the head-office treasury operations system.

Stage 2, high-speed on-chain settlement: the US head-office treasury team immediately sends USDPT issued through Anchorage Digital to that local agent’s institutional on-chain wallet. Regardless of weekend, night, or holiday, this reaches final settlement quickly on the Solana network on the basis of a 0.4-second block time.

Stage 3, freedom from business-hour dependence: even on a weekend when banks are closed, the local agent receives the dollar value (USDPT) sent by the head office on-chain in real time and reflects it on its own books.

With this mechanism in place, Western Union can recover its pre-funded buffer, which runs to hundreds of millions of dollars, down to a minimal level, at a scale fitting its operations.

Western Union is also pursuing expansion as a next step. It is building a Digital Asset Network (DAN) that connects the crypto ecosystem with its offline agent network so that USDPT can be cashed out into local fiat instantly, and it plans to launch a B2C service, Stable by Western Union, that lets ordinary consumers pay with stablecoins at physical merchants, rolling it out to more than 40 countries within 2026 to connect even the frontline retail touchpoint onto a single rail.

The case shows that the Solana public blockchain can function beyond a simple asset-trading network as core payment infrastructure for mainstream finance.

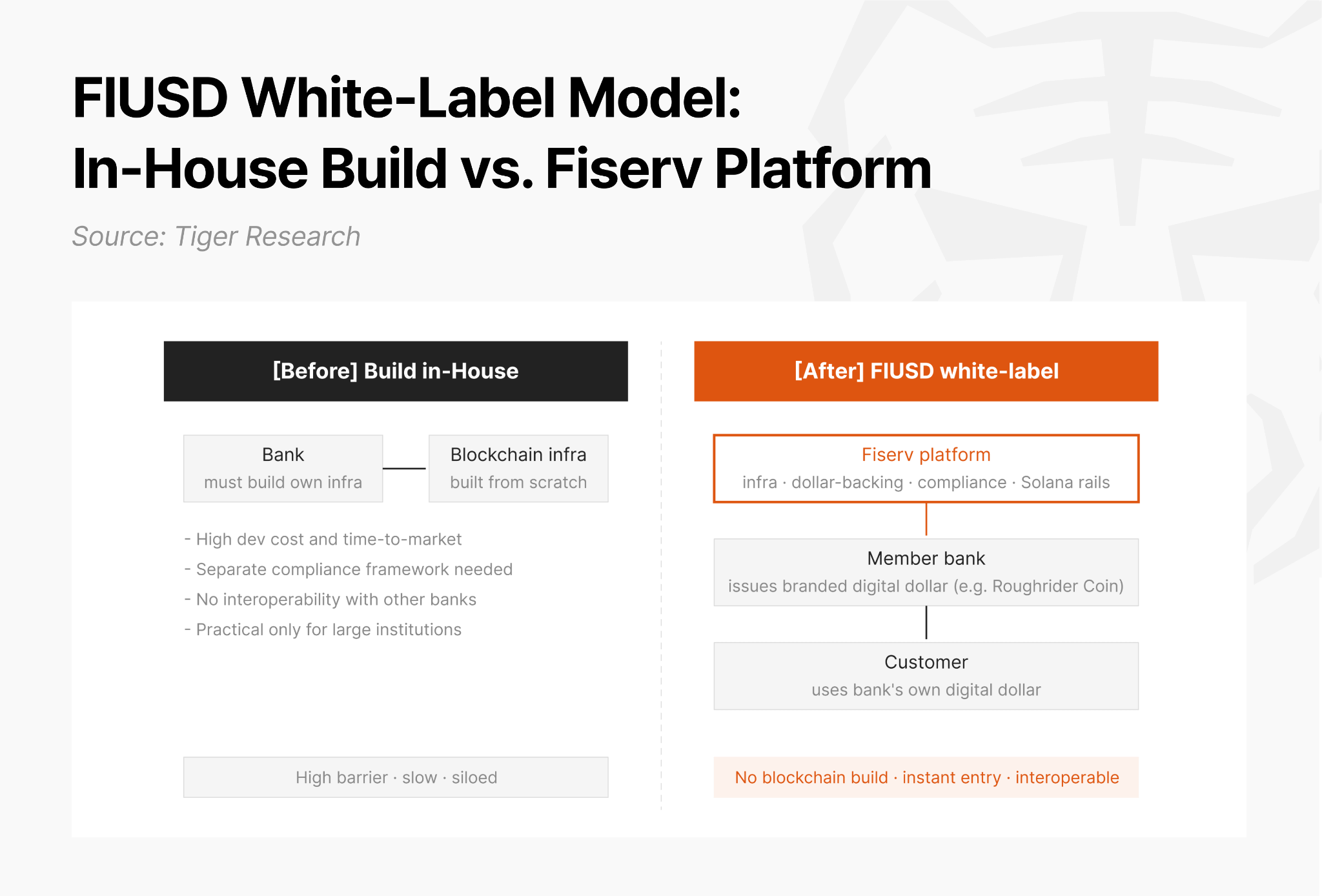

Fiserv: A Stablecoin for Financial Institutions (FIUSD)

On June 23, 2025, the global financial-technology company Fiserv announced plans to launch FIUSD, a white-label stablecoin for financial institutions that member institutions can build into their own payment and remittance services, along with a digital-asset platform.

Under a white-label structure, Fiserv supplies the technical infrastructure and dollar-backing system, and each financial institution issues and offers the stablecoin under its own brand. A bank can offer its own digital dollar to customers without building separate blockchain infrastructure.

The platform runs on Solana, with a formal launch scheduled for July 2026. The roles of the participating institutions are as follows.

Fiserv: leads the platform and provides the infrastructure, running it through its own global payment network and banking solutions.

Paxos: supports enterprise-scale technical infrastructure and handles the issuance and management of FIUSD under Paxos’s regulated framework.

Circle: provides stablecoin technical infrastructure and supports interoperability with other major stablecoin ecosystems.

There is already an adoption case. The Bank of North Dakota, the only state-owned bank in the US, announced it will launch “Roughrider Coin” on the FIUSD platform. It works as follows.

Core processing and orchestration: Fiserv’s new digital-asset platform uses its own Finxact core-processing platform as the base ledger and connects to cloud-native orchestration, payment, and banking platforms, forming an interoperable end-to-end fiat and digital ecosystem.

Network scale: Fiserv’s multisided network spans about 10,000 financial-institution clients and 6 million merchants and processes 90 billion transactions a year. Fiserv plans to offer FIUSD to its member financial-institution clients at no extra cost by using existing technology.

Risk and capital efficiency: member institutions use Fiserv’s existing customer-facing banking platform and receive compliance support through built-in functions such as fraud monitoring, risk management, and settlement control. Fiserv is also exploring the use of deposit tokens, which keep the benefits of a stablecoin while offering banks a more capital-friendly structure.

This is a structure that Asian financial institutions can readily learn from. In many regions, regulation currently makes issuing stablecoins difficult or entry impractical for now. This structure, in which an infrastructure provider supplies a white-label platform on Solana and a financial institution issues a digital dollar under its own brand, can be transplanted immediately once the regulatory environment is in place.

For Korea specifically, the white-label model maps onto the ongoing debate over whether banks or non-banks may issue stablecoins; it becomes viable once the FSC sets that boundary and establishes won-denomination rules.

4.3 Real-World Asset Tokenization (RWA)

The real-world asset tokenization sector covers Treasuries, private credit, money market funds (MMFs), listed stocks, and unlisted securities/commodities. It is the set of processes that converts financial assets traded in conventional markets into tokens on a blockchain for issuance, circulation, and settlement. Where the previous two sectors dealt with the speed at which funds move, this sector deals with how the asset itself exists.

The structural problem in this sector arises from infrastructure that is fragmented by asset type. For the same investor to access Treasuries, private credit, listed stocks, and unlisted securities/commodities, each asset class requires going through a separate intermediary, account, and settlement system.

Limited access: private credit and private equity have run mainly for institutions and ultra-high-net-worth individuals because of high minimum investments and long lockups, which structurally blocks entry by ordinary investors.

No secondary market: for illiquid assets, there is effectively no secondary market to trade in after issuance. Investors are tied to the asset until maturity, and price discovery barely functions.

Disconnected settlement: because settlement cycles and infrastructure differ by asset class, real-time portfolio-level fund management is impossible. To invest the proceeds from selling Treasuries into private credit, an investor has to pass through two separate settlement systems in sequence.

Tokenization resolves this fragmentation on a single ledger. Once an asset exists as a token, issuance, circulation, and settlement are all handled on the same on-chain infrastructure. A private credit fund interest, for example, becomes a token that can circulate around the clock, and an MMF income right becomes an asset transferable between wallets. When an investor rebalances a portfolio across different asset classes, what is required is not opening a separate account but a single on-chain transaction.

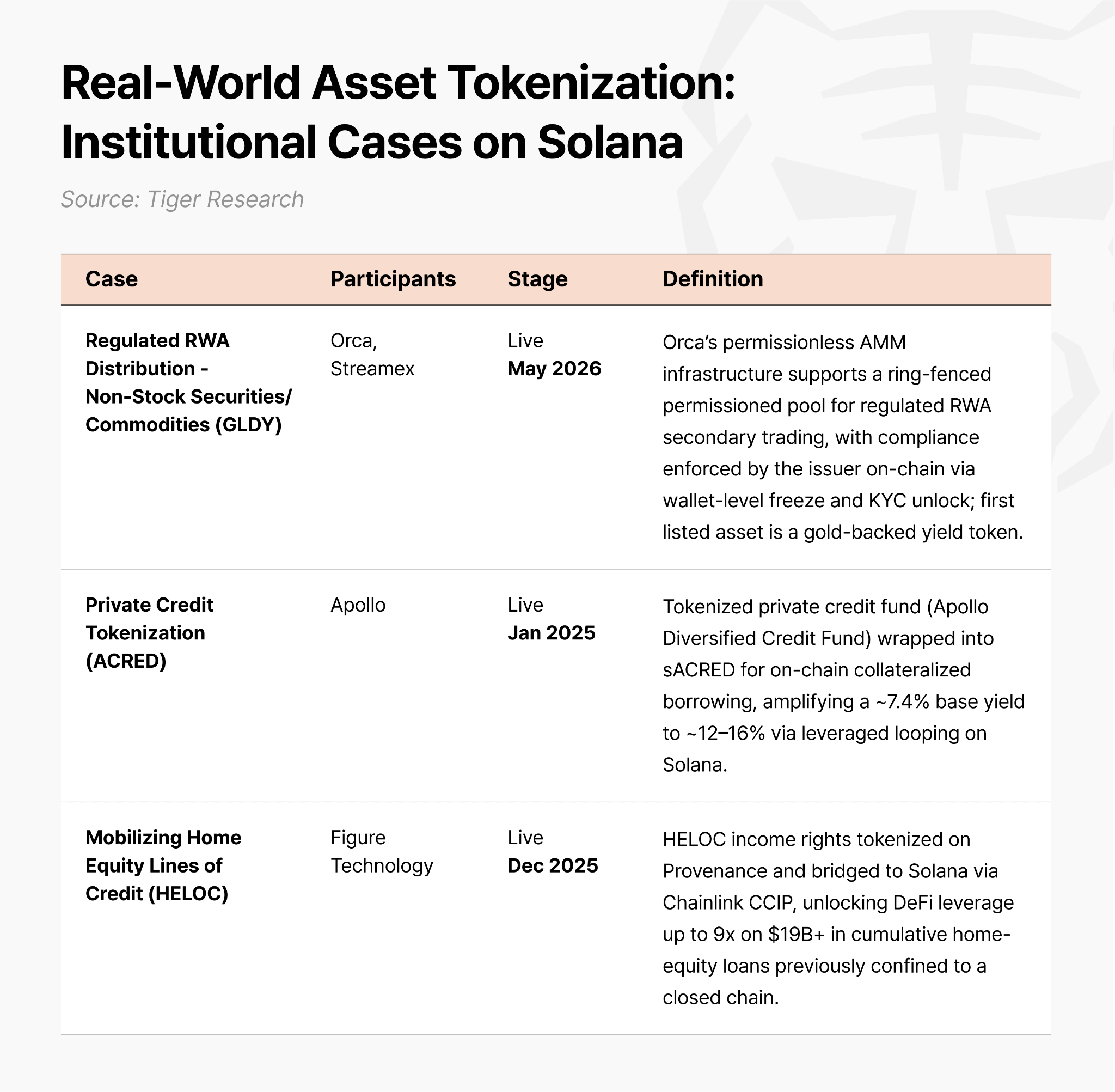

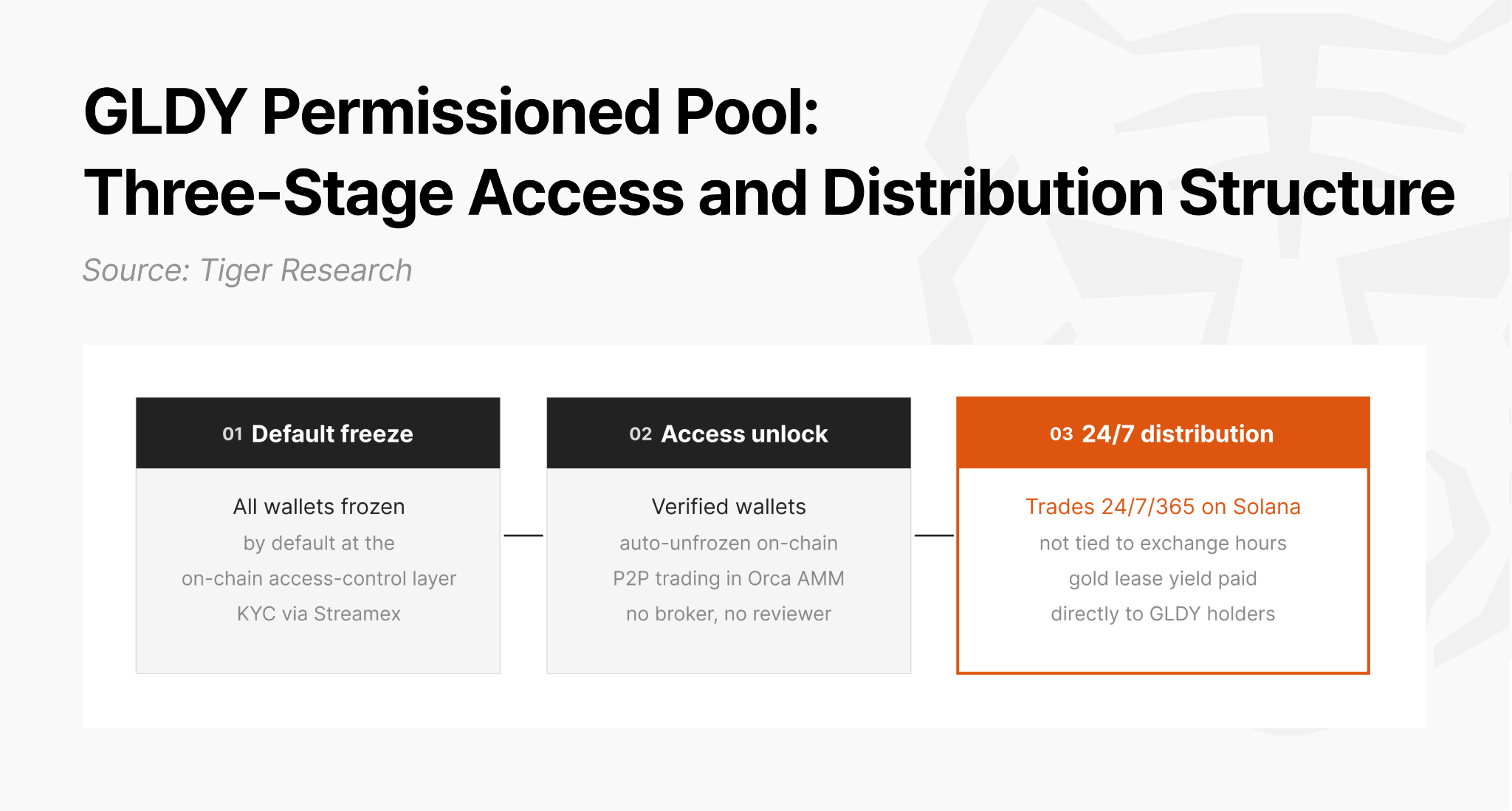

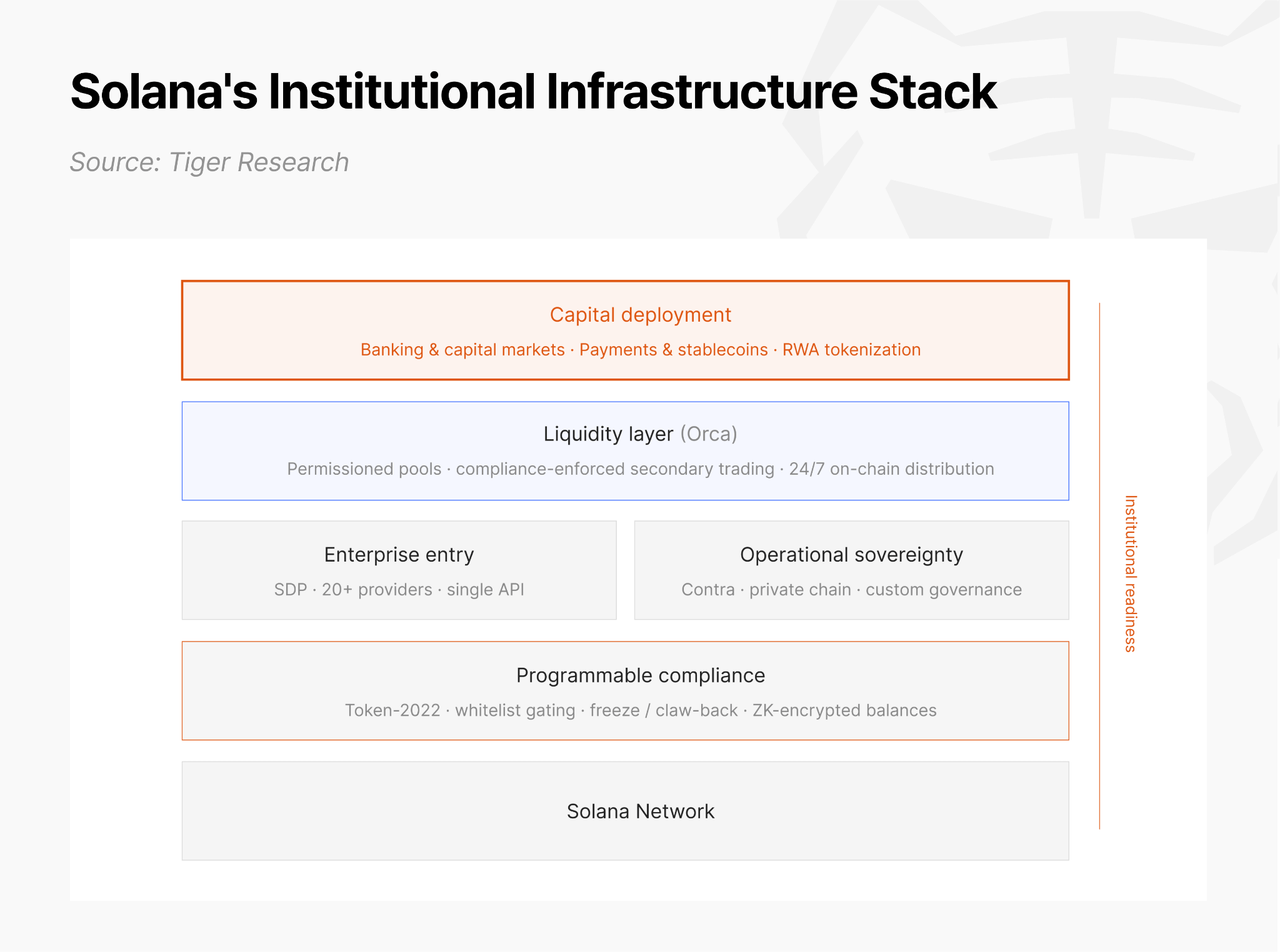

Orca x Streamex: Regulated RWA Distribution (GLDY)

The tokenized listed-stock market has long carried a disconnect between issuance and distribution. Listed-stock-type tokenized assets had secondary-trading paths open through multiple exchanges, as with Kraken’s xStocks, but non-stock tokenized securities such as bonds, commodities, and private loans lacked issuer-controlled, eligibility-gated liquidity infrastructure after issuance. Issuance technology advanced, but distribution infrastructure did not keep up.

In response, in May 2026, the leading Solana on-chain infrastructure provider Orca launched permissionless automated market maker (AMM) infrastructure that permits issuers to create customizable pools based on the requirements of its regulated assets. The Nasdaq-listed company Streamex was the inaugural issuer to utilize this bespoke solution for regulated assets by using it to launch secondary liquidity of its GLDY token, yield-bearing token security linked to physical gold. Only investors who meet Streamex’s eligibility requirements (i.e., accredited investor status) may provide liquidity or trade GLDY.

Streamex: issues the GLDY token, performs KYC and accredited-investor verification, and manages whitelist onboarding. It is a Nasdaq-listed digital-asset infrastructure company specializing in commodity tokenization.

Orca: provides the permissionless automated market maker trading infrastructure on which issuers like Streamex can create ring-fenced permissioned pools for their regulated assets. Operating since February 2021 as Solana’s longest-running DEX, it has processed more than $500 billion in cumulative volume and completed multiple independent security audits.

Monetary Metals: manages the underlying assets, generating returns backed by physical gold for GLDY holders through gold lease contracts.

The core of this business lies not in the type of asset but in how trading is controlled. It is a structure that enforces compliance requirements through code rather than a human review process. The GLDY pool operates in three stages.

Default freeze and KYC verification: every investor wallet starts frozen and unable to trade by default. Only a wallet that passes Streamex’s KYC verification is automatically unfrozen at the on-chain access-control layer.

Access unlock and trading: GLDY trades peer-to-peer in real time within the Orca AMM pool only between verified wallets. No broker or reviewer intervenes.

Around-the-clock distribution and yield payment: unlike conventional gold investment products tied to exchange hours, GLDY trades 24/7/365 on Solana. The returns from Monetary Metals’ gold lease contracts are paid directly to GLDY holders.

The token-level freeze and unfreeze control works the same way regardless of asset type, whether stocks, bonds, or commodities. GLDY demonstrated this structure first for a gold security, but the same approach can apply directly to any regulated asset, including Treasuries, corporate bonds, and private credit. This is why Orca proposed the structure as the trading infrastructure for the Project Open pilot framework, since it can serve as an infrastructure layer combined with regulation. It is an example of what kind of business is demonstrably possible beyond issuance.

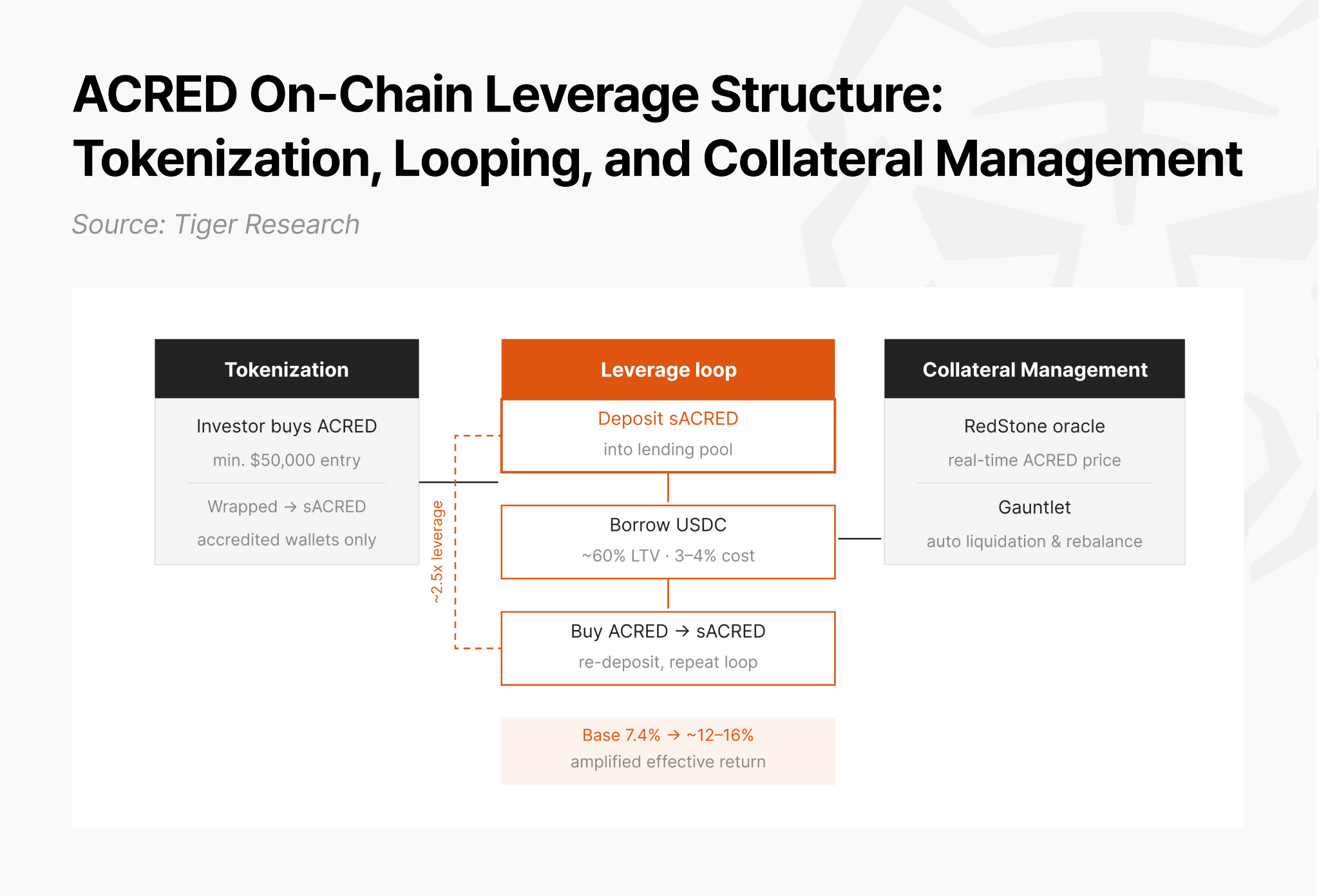

Apollo: Private Credit Tokenization (ACRED)

The conventional private-lending market, despite high returns, has had two structural barriers. High minimum investments left it open only to institutions and ultra-high-net-worth individuals, and once invested, capital was tied to the asset until maturity, an illiquidity problem.

The global private-equity firm Apollo began an effort to resolve these constraints on-chain in January 2025. It issued ACRED, a tokenized feeder fund based on its Apollo Diversified Credit Fund (ADCF), through Securitize. ACRED is a restricted security for accredited investors only, issued on multiple chains including Solana. In the Solana ecosystem, four parties combine to build an institution-only on-chain leverage structure.

Securitize: the issuance platform for ACRED, handling accredited-investor KYC and AML verification and the sACRED wrapping structure. Because ACRED is a conventional fund interest that cannot be used directly in DeFi, a structure was introduced to convert it into a smart-contract-based wrapper token, sACRED. Accredited-investor verification is enforced by smart contract during the conversion as well.

Solana-based on-chain lending protocol: operates an institution-only lending pool that takes sACRED as collateral and provides a stablecoin borrowing facility.

Gauntlet: manages the risk of the leverage strategy with an automated engine, adjusting borrowing size in real time to market rates and risk limits.

RedStone: supplies real-time ACRED price data through an oracle, providing the technical basis for collateral valuation and liquidation decisions.

The working process, with a minimum entry of $50,000, runs as follows.

Tokenization and wrapping: when an accredited investor buys ACRED, they hold a token equivalent to a conventional fund interest. To use it in DeFi, they convert it into sACRED through Securitize’s smart contract. sACRED transfers are allowed only between verified, accredited wallets.

Collateralized borrowing and leverage: an investor deposits sACRED into the institution-only lending pool and borrows stablecoins worth about 60% of the collateral value, at a borrowing cost of roughly 3% to 4%. Using those stablecoins to buy back ACRED, convert it to sACRED again, and re-deposit it, repeating the loop, raises effective leverage to around 2.5x. A base return of about 7.3% to 7.5% (against the official fund return of 7.36%) is amplified to roughly 12% on a conservative view, and up to about 16% on Securitize’s projected looping return.

Real-time collateral management: the RedStone oracle supplies real-time ACRED price data, and Gauntlet uses it to decide liquidation conditions and rebalancing timing automatically. Setting and releasing collateral is processed on Solana within seconds, at a fee of less than $0.001 per transaction.

For this leverage structure to hold, setting and releasing collateral must be repeated quickly and cheaply. On infrastructure where settlement takes days or each turn carries a high fee, the same structure can hardly work. Solana’s throughput meets the conditions that support the economics of this strategy.

This is not a risk-free return, of course. If borrowing rates rise, the margin narrows. The limited liquidity of quarterly-only redemption, ACRED’s market cap of around $100 million (as of early 2026), and the liquidation risk tied to oracle-reflected prices all have to be weighed.

For Asian institutions, this case is about asset access. Asset classes that institutions in the region have traditionally found hard to access, such as private credit, infrastructure funds, and real estate funds, can be opened up structurally through tokenization and on-chain mobilization. What ACRED proved is that a structure for converting private-lending fund interests into on-chain collateral and turning them over in real time actually works.

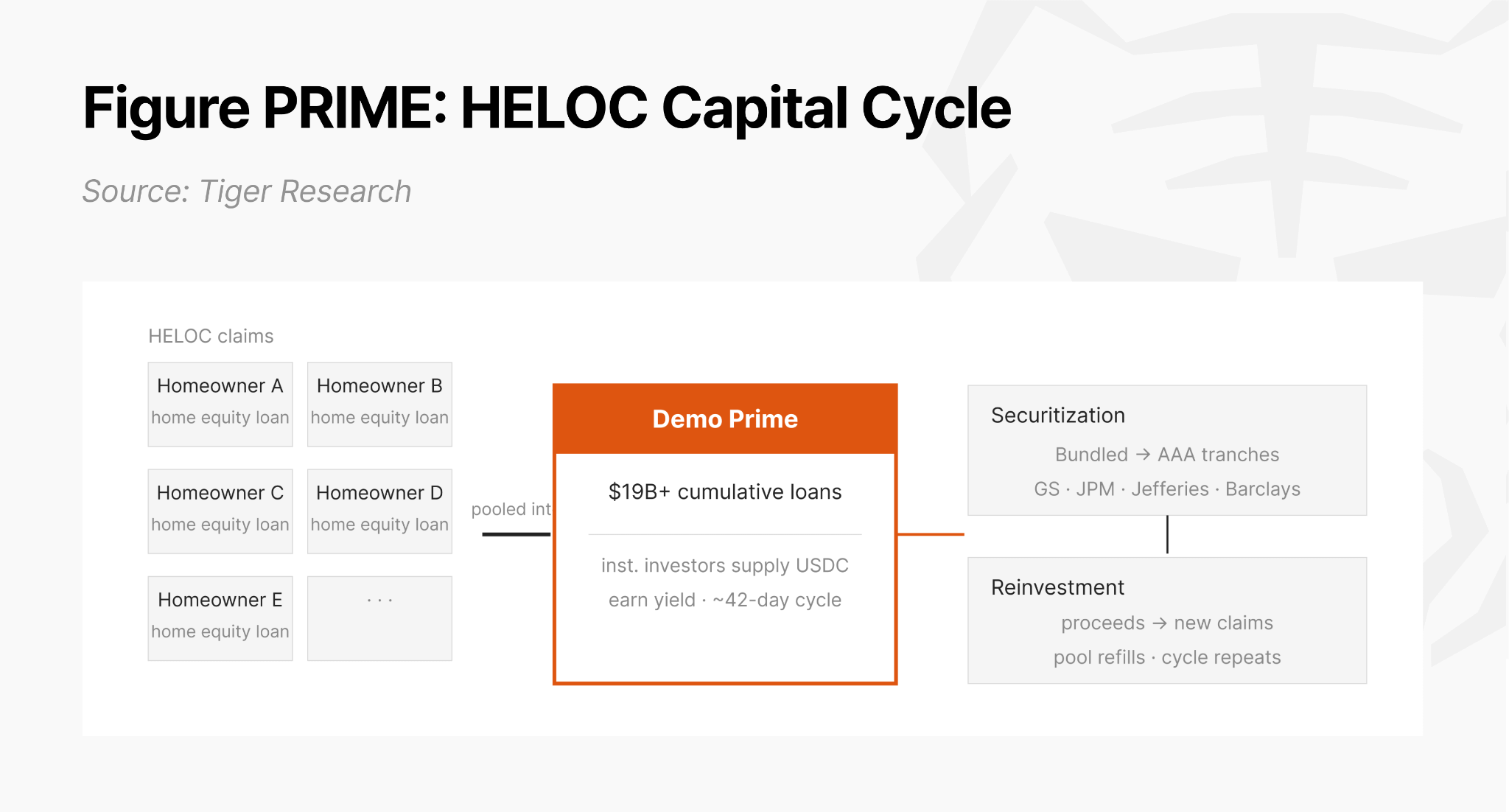

Figure Technology Solutions: Mobilizing Home Equity Lines of Credit (HELOC)

Figure Technology Solutions (Figure) is the largest non-bank issuer of home equity lines of credit (HELOC) in the US. As of December 2025, it holds more than $19 billion in cumulative on-chain loans. It is a mainstream fintech player that has repeatedly issued AAA-rated securitization tranches underwritten by Goldman Sachs, J.P. Morgan, Jefferies, and Barclays.

Figure originally tokenized and mobilized HELOCs on its own appchain, Provenance. A HELOC (home equity line of credit) is a US home-secured credit product that uses home equity as collateral.

Figure’s business works like this. It extends loans secured by homes, records those loan claims on a blockchain, and once enough accumulate, bundles and sells them to institutional investors. Because it sells rather than holds the loans for long, it can re-lend with the proceeds it recovers.

Figure cycles its capital the same way. Newly issued HELOC claims are gathered into an on-chain pool called Demo Prime, where institutional investors supply stablecoins and earn interest. After about 42 days, the claims in the pool are bundled into AAA-rated securitization products and sold to Wall Street asset managers, pension funds, insurers, and banks. When the sale proceeds return to the pool, new claims fill it and the cycle repeats. The faster the turnover, the higher the capital efficiency.

The problem was that this structure was confined within Provenance, a closed chain. Despite being high-credit-quality collateral, it was cut off from the DeFi ecosystem, which limited how far capital turnover could rise. In December 2025, Figure launched the PRIME token to address the capital-turnover problem. The structure connects Provenance’s loan income rights to Solana to absorb the liquidity and leverage infrastructure of the public DeFi ecosystem.

This cross-chain expansion works through a combination of the following infrastructure providers.

Provenance: handles the on-chain tokenization of the underlying HELOCs and the operation of the Demo Prime pool. The full process from loan origination through collateral management to securitization runs on the Provenance chain.

Hastra: a yield-distribution protocol incubated jointly by Figure and the Provenance Foundation. It serves as a liquidity layer that connects the yield generated in Provenance’s Demo Prime to the Solana DeFi ecosystem, with Chainlink CCIP ensuring cross-chain data integrity.

Kamino: the exclusive on-chain lending partner that builds the lending pool and leverage strategy for the PRIME token on Solana. It runs a PRIME/USDC isolated market and supports up to 9x leverage (Multiply).

Orca: the primary spot venue for the PRIME token on Solana, running the PRIME/PYUSD pools where users and institutions provide and access liquidity. While Kamino covers lending and leverage, Orca supplies the AMM depth that makes PRIME tradable and keeps its on-chain price efficient.

The working capital-expansion process is structured as follows.

Tokenization: Figure tokenizes the home-equity loans on the Provenance chain and designs the PRIME token based on the income rights they generate.

Bridging: Chainlink CCIP and the Hastra protocol bridge the value and data of assets locked on Provenance safely to Solana.

Collateralization: the PRIME token, once settled on Solana, is listed on the Kamino lending protocol, where it functions as an active asset that ordinary users and institutions can use as collateral or to supply liquidity.

Figure chose Solana not out of technical preference but for capital efficiency. Provenance is a chain proven in institutional trust, but within its closed ecosystem there was no liquidity infrastructure to build leverage on. The net spread of the 9% Demo Prime yield minus Kamino’s 6% borrowing cost is amplified by the leverage multiple. Unless setting and releasing collateral is processed on Solana within seconds and at less than $0.001 per transaction, the economics of this strategy do not hold.

Even though Figure already had its own chain, it chose Solana to expand liquidity. The lesson is that building your own infrastructure is one option, but connection matters just as much.

4.4 Infrastructure Diffusion

Where the previous three sectors dealt with the transition of individual areas, this sector deals with the point where those transitions converge. Banks issuing bonds on-chain, remittance companies settling in stablecoins, and asset managers tokenizing funds are not proceeding separately but happening at the same time on the same infrastructure.

The diffusion divides into three layers.

Issuance layer: PayPal, Fiserv, Circle, and Tether issue stablecoins or operate issuance infrastructure on Solana. This is not a single company’s experiment but a structure where competing issuers coexist on the same network.

Settlement layer: Visa extended stablecoin settlement for merchant acquirers to Solana, and Worldpay moved merchant transaction settlement onto the Solana network. YouTube adopted Solana-based PYUSD as a means of paying US creators. Companies that own settlement networks are replacing parts of those networks with on-chain rails.

Touchpoint layer: SoFi, a US federally chartered bank, lets its 14.7 million customers buy Solana directly from their bank accounts and has begun operating its bank-issued stablecoin, SoFiUSD, on Solana. The institutional exchange Bullish adopted a Solana-based stablecoin as its main settlement rail across 50 jurisdictions and processed $1.15 billion in IPO proceeds on the Solana network.

When issuance, settlement, and touchpoint operate on the same network, network effects arise. A token issued by a bank is settled by a payment company, and the consumer holds that asset in a bank app, forming a loop. The more participants, the greater the utility for each. The formation of Internet Capital Markets accelerates the moment this loop passes its tipping point.

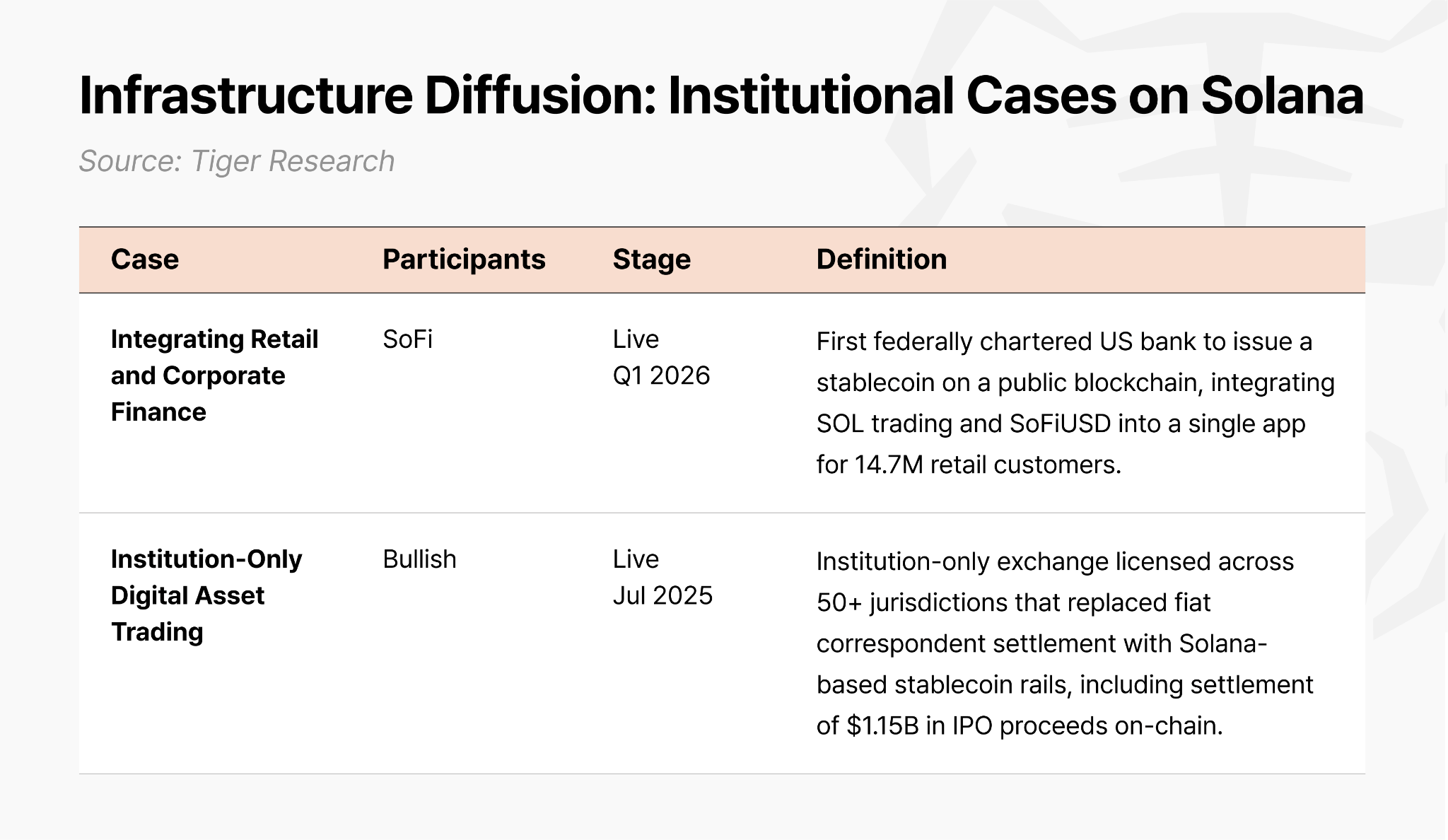

SoFi: Integrating Retail and Corporate Finance

SoFi operates around the listed fintech holding company SoFi Technologies, under which sits SoFi Bank, N.A., a federally chartered bank supervised by the OCC. With 14.7 million members and $53.7 billion in total assets (as of Q1 2026), it started in student-loan refinancing and grew into a full-stack retail finance platform that offers deposits, lending, investing, and insurance in a single app.

In November 2025, SoFi became the first federally chartered bank to launch crypto trading for consumers. It allows customers to buy, sell, and hold 28 digital assets, including BTC, ETH, and SOL, directly from a bank account.

SoFi supports crypto trading directly to prevent the user attrition that comes from poor access. Under existing bank infrastructure, digital assets were accessible only through the separate path of a standalone exchange. To buy SOL, a customer had to leave the SoFi app and sign up for a separate platform such as Coinbase, Kraken, or Robinhood. That was the point where the finance app lost its customer touchpoint to the outside.

SoFi aims to bring that touchpoint back inside the bank app. Supporting crypto trading absorbs digital-asset access into the bank app.

In-app purchase: customers can buy and hold digital assets, including SOL, directly within the SoFi app.

Inbound integration: customers receive a Solana network deposit address and can move assets from external wallets into the SoFi app.

Issuing its own on-chain dollar (SoFiUSD): SoFi builds its own digital-dollar rail through its bank-issued stablecoin, SoFiUSD.

Enterprise expansion: through Big Business Banking, SoFi extends this structure into payment, settlement, and treasury infrastructure for corporate clients.

SoFi began issuing SoFiUSD in Q1 2026 and expanded it into an in-app customer product in May. It is the first case of a federally chartered bank under OCC supervision placing its own liabilities on the Solana public blockchain in the form of a stablecoin. This is not a technology experiment but a structure in actual operation under regulatory approval.

Many Asian internet banks already operate strong mobile-app customer channels, fast-remittance services, and high digital-finance penetration. The constraint on replicating this structure is regulatory rather than technical.

Each country still lacks regulatory standards on whether a bank can issue a stablecoin on a public blockchain and whether interest and depositor protection can apply to tokenized deposits. SoFi was able to do this because the US set the regulation first and provided guidance. Once each country’s financial authorities fix the same baseline, Asian internet banks will be able to apply the same structure.

Bullish: Institution-Only Digital Asset Trading

Bullish is an institution-only digital-asset exchange licensed in more than 50 jurisdictions, including by the Gibraltar Financial Services Commission (GFSC), Germany’s BaFin, the Hong Kong Securities and Futures Commission (SFC), and the New York Department of Financial Services (NYDFS).

In July 2025, Bullish officially declared that it would adopt a Solana-network stablecoin as the main rail for custody, payment, trading, and settlement across its exchange and clearing services. Bullish’s reason for choosing Solana is clear. When an institutional exchange moves funds with counterparties across more than 50 jurisdictions, the conventional settlement structure that routes through each country’s fiat and correspondent banks carries fees of tens of dollars per transaction and processing delays of one to five days.

A stablecoin replaces this multilayered clearing structure with a single rail. For Bullish, this can be seen as expanding the revenue base, not just cutting costs. Beyond trading fees, stablecoin interest income, liquidity-service income, and DeFi protocol income all fall under the service revenue defined in Bullish’s reporting.

Bullish’s settlement structure operates in three stages.

Order matching: when an institutional investor submits a buy or sell order on the Bullish platform, matching occurs in the internal order book. Under a full-reserve structure, client assets are held 1:1 in separated custody, with no maker fees or custody fees. It also applies no collateral haircut up to a notional $1 billion for USD and major stablecoins.

On-chain settlement: a Solana-based stablecoin operates as the main rail across custody, payment, trading, and settlement. Even when counterparties across more than 50 jurisdictions use different fiat systems, the Solana-based stablecoin is designed as a common settlement unit.

Infrastructure deepening: Bullish’s use of Solana extended beyond payment and settlement into security-type assets. In May 2026, it tokenized its own stock, BLSH, on Solana. It runs the structure with SEC-registered transfer agent EQ, allowing only whitelisted addresses, and has not yet opened AMM or DEX trading.

The core of the Bullish case is that a regulated exchange handling billions of dollars in institutional trades placed a Solana-based stablecoin as its core operating rail and actually processed an event carrying legal responsibility, the settlement of IPO proceeds, on Solana. In August 2025, Bullish announced that it received $1.15 billion in IPO proceeds in stablecoins, most of it processed in stablecoins issued on the Solana network. Jefferies coordinated the transaction and Coinbase handled custody. A large capital-market event carrying legal responsibility was processed with a Solana-based stablecoin.

5. Regulatory Change That Embraces the Industry with Solana

Companies build an industry, but regulatory clarity determines how that industry is defined and bounded.

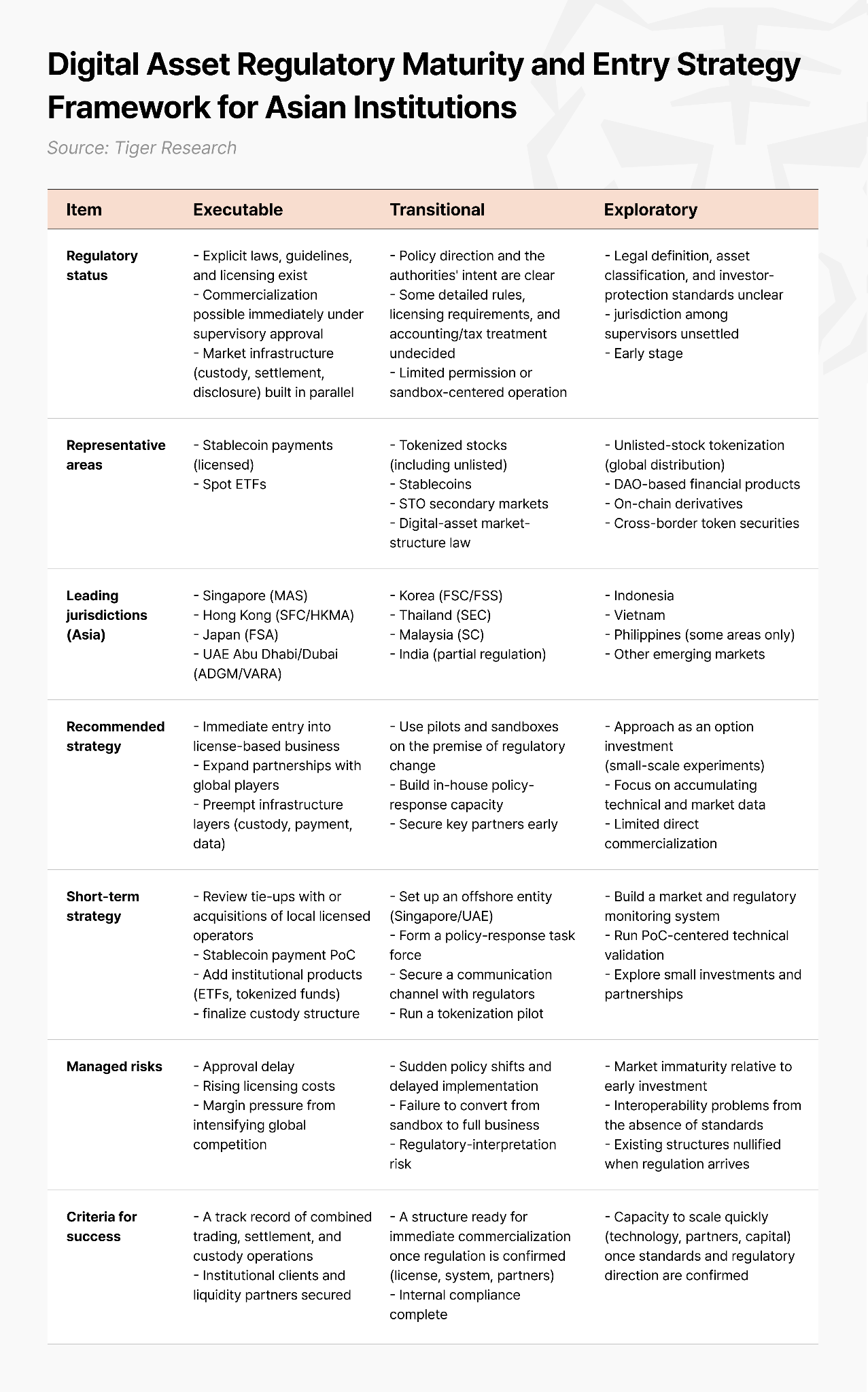

Because Asian financial institutions operate mostly under positive regulation, which restricts entry outside permitted areas in principle, they need to review the global regulatory environment before deploying capital. In major countries such as Korea and Japan, which have followed a government-led growth path, new businesses without a clear legal basis are treated as potential risks or as unlawful.

The West, by contrast, follows the common-law principle of negative regulation, permitting business up front and then drawing boundaries after the fact through reactive policymaking when risks emerge or sufficient scale is reached. Such policymaking can take several forms including legislation, regulation, and enforcement.. This structure became the framework in which diverse innovative services appeared first in the crypto market and were later drawn into the regulated industry.

In the current transitional phase, where institutional inclusion and legal ambiguities coexist, the capacity to anticipate and manage regulatory risk in advance is emerging as a key market requirement.

The Solana Policy Institute (SPI) is deeply involved in this regulatory-design process. A nonprofit policy body founded in Washington, DC, in March 2025, it represents the crypto industry as a whole beyond the Solana ecosystem and has put forward concrete alternatives in legislative and regulatory debate. Its main activities are as follows.

Project Open proposal: submitted jointly with Orca, Superstate, and Phantom (among others) to the SEC crypto task force on April 30, 2025. It is a proposed exemptive relief pilot framework for secondary trading of securities on AMM infrastructure like Orca on a public blockchain like Solana, with a white-listed wallet framework managed by a registered transfer agent. All parties have continued the dialogue with the Commission since, including through written submissions and presentations to SEC leadership and staff. SPI is pursuing a similar pilot program at the Commodity Futures Trading Commission to bring on-chain derivative and futures transactions into the regulatory fold.

Pushing the market-structure legislation (CLARITY Act) and the GENIUS Act: SPI participates as a core driver of the legislative debate and led the inclusion of a clause protecting open-source developers (the Blockchain Regulatory Certainty Act). Last year, SPI assisted Congress in developing the GENIUS Act and is currently participating in the regulatory implementation of that law.

Setting tax standards: it formally asked the Treasury to revise IRS guidance so that staking and mining rewards are taxed at the point of sale rather than at the point of creation. The US Congress is currently considering tax legislation that addresses the taxation of staking rewards, creates a de minimis exemption for digital asset transactions under $10, and more broadly resolves tax questions that have emerged as the industry has developed.

Protecting developers: in response to the Tornado Cash developer case, where writing code itself escalated into criminal liability, it donated $500,000 to a legal-defense fund.

Convening power: in April 2026, it brought federal lawmakers, the SEC, White House officials, and Wall Street institutions together at the Solana Summit NYC, and together with more than 65 crypto organizations submitted a letter of policy priorities to the White House.

These activities show that US regulation is being drawn in real time through interaction between the private sector and the authorities, rather than designed unilaterally by government. The contours of regulation have taken shape as the industry proposes frameworks.

As a result, the current regulatory landscape divides into two areas. Holding, issuing, and settling regulated assets like securities have been brought into a lawful regime, and the SEC appears on the precipice of creating a fully-developed “innovation exemption” for the on-chain trading of such securities via trading protocols on public blockchains. The compliance capacity to anticipate the macro timeline is likely to determine the success or failure of capital deployment.

5.1 What Works Now: Activities Brought into the US Regulatory Fold

The activities brought inside regulation so far have prioritized points of contact with existing regulated markets and assets. Most of the activities are those that conventional finance players already do well. The areas where public blockchains strengths come fully into play remain to be completed.

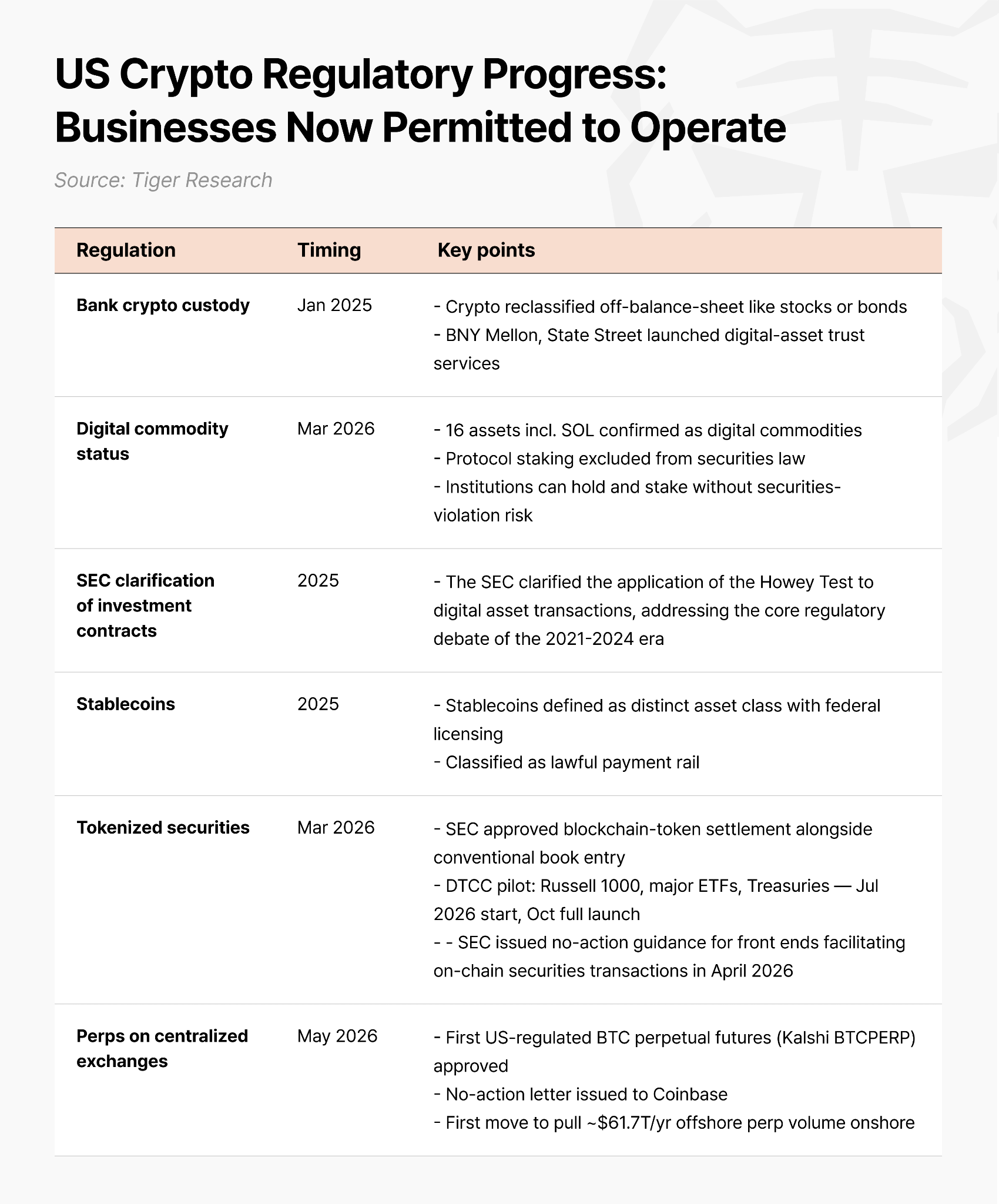

Bank Crypto Custody (Repeal of SAB 121)

In January 2025, the SEC’s Staff Accounting Bulletin No. 121 (SAB 121) was formally repealed, removing the barrier to large banks entering the market. The previous guidance forced banks to record customer crypto held in custody as a liability on the bank’s balance sheet at the same time. As a result, banks had to tie up large amounts of their own capital against custody to meet capital-adequacy (BIS ratio) requirements, which made the custody business unworkable.

After the repeal, crypto is classified off-balance-sheet like ordinary stocks or bonds, establishing a normal business structure of safe custody for a fee. To support this, federal regulators issued joint guidance on risk management, AML, and KYC for digital asset custody (Federal Reserve, as of July 14, 2025), while also confirming a technology-neutral approach that applies identical capital requirements to tokenized securities (Federal Reserve, as of March 5, 2026). Following this clear regulatory framework, large custodian banks such as BNY Mellon and State Street launched digital-asset trust services linking separate wallets with bank accounts.

Digital-Commodity Status and Approval of Protocol Staking

On March 17, 2026, the SEC and the CFTC issued joint interpretive guidance confirming 16 major assets, including Solana (SOL), as digital commodities. The guidance divided assets into five types, discarding the old security/non-security binary, and formally excluded protocol staking from securities-law regulation. This extends the principle the SEC stated in January, that tokenization does not change an asset’s legal classification and that the law applies based on economic substance.

With the legal nature of the assets clarified, institutional investors gained the legal safety to buy, hold, and stake the 16 major assets, including Solana, without securities-law violation risk. Regulatory clearance does not, however, immediately guarantee large inflows. In Q1 2026, US institutions showed a cautious stance, concentrating capital on careful position rebalancing that turns staking-liquidity infrastructure and protocols themselves into assets, rather than increasing exposure to altcoin spot itself.

SEC Clarification of Investment Contracts

In 2025, the SEC clarified the application of the Howey Test to digital asset transactions, addressing the core regulatory debate of the 2021-2024 era. Specifically, the commission established a formal legal distinction between the digital asset itself, recognized as neutral underlying technology, and the investment contract under which it may initially be sold.

By confirming that the secondary market trading of these tokens does not inherently constitute a securities transaction, the SEC effectively removed the persistent legal overhang on major Layer-1 protocols. This critical clarification provided institutions with the regulatory certainty needed to safely hold and trade assets like Solana on regulated platforms without continuous securities-law violation risks (SEC, as of October 2025).

Stablecoins and Treasury Tokenization Under the GENIUS Act

The federal GENIUS Act, passed in 2025, specifies stablecoins as a distinct asset type rather than securities or deposits and imposes federal licensing standards and operating requirements on issuers. With issuers’ legal status established, stablecoins were reclassified within institutional portfolios from a risk asset to a lawful, low-volatility on-chain payment rail. As legal risk lifted, conventional financial firms’ thematic interest in and investment into infrastructure companies such as Circle became visible. The regulatory paradigm will only be complete, however, once it carries through to final passage of the federal market-structure bill (the CLARITY Act), which would close out the entire crypto asset-classification scheme.

Tokenized Securities Led by Legacy Exchanges

On March 18, 2026, the SEC gave final approval for Nasdaq to trade certain securities in tokenized form (approving Rule Change SR-NASDAQ-2025-072). Eligible participants settle with blockchain tokens instead of conventional physical book entry, and tokenized stocks trade in parallel in the same order book as conventional stocks, with the same prices and shareholder rights guaranteed. In step with this, the Depository Trust and Clearing Corporation (DTCC) confirmed a limited pilot starting in July 2026 and a full launch in October, covering Russell 1000 names, major index ETFs, and US Treasuries.

This is an approach that adopts blockchain technology while keeping control of the ledger with existing financial institutions. Because trading itself follows the existing T+1 settlement cycle, the focus is less on technical novelty than on using margin collateral between regulated institutions and improving post-market settlement. It is a closed model not directly connected to the public-chain ecosystem, and attention going forward should turn to expanding free trading.

Perpetual Futures (Perps) on Regulated Exchanges

On May 29, 2026, the CFTC approved Bitcoin perpetual futures trading on a US regulated exchange for the first time. Kalshi obtained approval for its “BTCPERP” contract, and on the same day a no-action letter allowing a perpetual-futures product was sent to Coinbase. This is the first move to pull the large perpetual-futures liquidity that had been concentrated on unregistered offshore exchanges such as Binance and Bybit (about $61.7 trillion a year as of 2025) into the US regulated system. Given the fee rates and leverage terms offered by offshore exchanges, however, a cautious view also holds that, regulation aside, whether trading volume will move meaningfully to the US remains to be seen.

5.2 What Does Not Work Yet: The Frontier Defining Industry Standards

Where the areas above opened first around activities that fit the grammar of conventional finance, the unresolved areas here are attempts to make full use of public blockchain’s own disruptive strengths, decentralization and autonomy.

These areas would all be addressed comprehensively via the CLARITY Act, which would, for example, define the overall market structure for digital assets, create a spot-market regulatory framework for digital commodities, direct the SEC and CFTC to conduct rulemakings to allow for businesses to conduct activities within those regulators’ jurisdictions on public blockchains, and allow US banks to operate on public blockchains. In March 2026 the two agencies classified tokens as digital commodities, digital securities, and stablecoins and divided jurisdiction through joint interpretive guidance, but the SEC defined that guidance as a temporary bridge until Congress legislates a comprehensive framework. CLARITY is the work of Congress hardening into law the boundary the current, and future, executive’s interpretation of how to regulate crypto and public blockchain-based markets.

For institutions to fully remove macro regulatory risk and deploy long-term capital, they need the durability of statute to be confident that regulatory expectations will not shift dramatically with political change.

The bill’s scope is not limited to crypto-native operators. It also covers the standards conventional intermediaries must follow when they bring digital rails into their own products. Existing market rules assume that every trade has an intermediary such as a broker or a custodial exchange, but on a blockchain that assumption does not hold. CLARITY would codify rules premised on a market structure without intermediaries.

The industry, including SPI, is pushing the bill hard at the front of the legislative effort, but the outlook in Washington is far from the optimism on social media. The bill passed the House 294 to 134 in July 2025 and cleared the Senate Banking Committee 15 to 9 on May 14, 2026, but its chance of becoming law this year is about 50% or lower. The two parties are at odds over an ethics clause that would restrict the president and senior officials from profiting from crypto businesses while in office. A May 2026 agreement on stablecoin yield restored some legislative momentum, but the banking sector still strongly opposes core provisions.

The decisive factor is time. The roughly four-week legislative window in the Senate from mid-July to the recess in early August is effectively the deadline for passage this year. Miss that window, and the timeline slips into the 2026 midterm phase, where reaching agreement becomes harder in the pre-election landscape. While macro legislation is delayed, the barriers facing key businesses on the regulatory boundary and the attempts to break through them with technology are as follows.

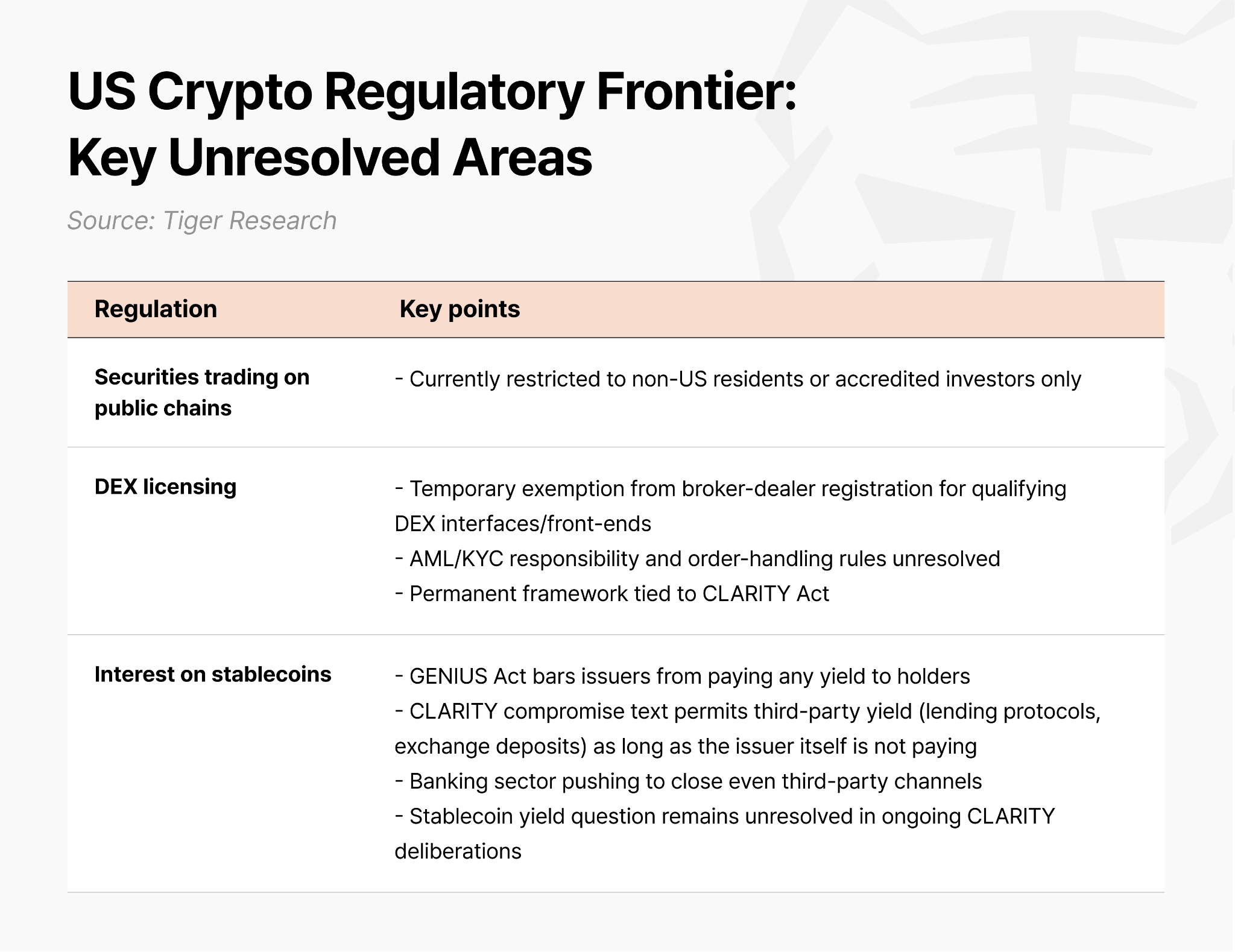

Free Trading of Stocks on Public Chains

The SEC recently raised expectations by discussing approval of “third-party stock tokenization” without the listed company’s consent (an innovation exemption), but two key hurdles remain before actual approval. First, the authorities’ strict standard that excludes mere synthetic stocks and permits only on-chain stocks that fully guarantee actual shareholder rights, voting and dividends. Second, strong resistance from conventional finance (Nasdaq, SIFMA, and others) worried about the liquidity fragmentation that spreading trading across many blockchains would bring. Final approval is therefore on hold amid tense disagreement.

To comply with existing SEC requirements, tokenized-stock services on public chains today remain a half-market, restricted strictly to non-US residents (Reg S) or wealthy accredited investors (Reg D). To break this limit, the Solana Policy Institute (SPI) and others have proposed the Project Open pilot, which performs real-time settlement (T+0) between KYC-completed wallets through a non-custodial AMM (Orca) without a conventional intermediary, in an attempt to enable fully free securities trading on public chains.

Deferred Licensing for Interfaces (Front Ends)

On April 13, 2026, the SEC’s Division of Trading and Markets issued temporary guidance (a staff statement) stating that decentralized interfaces meeting certain conditions may operate without broker-dealer registration. This is a sunset provision expiring in five years, however, and essential regulatory gaps remain, such as who bears the anti-money-laundering (AML/KYC) obligation and who is responsible for order handling, so it carries risk for large institutional capital to flow in immediately.

In this institutional transition, decentralized exchanges are looking for a way through to prepare for the expiry. Orca, for one, is combining institutional compliance tools and real-time on-chain screening into its own front-end and smart-contract layer to advance a transparent order-handling infrastructure. The self-regulatory compliance model they build during the deferral period is likely to be cited as a reference when a permanent legislative framework is set.

Interest Payments on Stablecoins

Despite stablecoins gaining formal regulatory recognition, the GENIUS Act strictly prohibits issuers from paying any form of interest or yield to holders. The concern is that if stablecoins were to offer competitive returns, household funds would flow out of bank deposits and into tokens in significant volume.

Under the CLARITY compromise text that has passed the Senate Banking Committee, yield generated through third-party platforms, such as lending protocols or exchange deposit products, falls outside the scope of the prohibition, as long as the issuer itself is not paying the yield. Banking industry pressure to close even these affiliated and third-party channels is intensifying, however, and attempts to structure yield-bearing stablecoins on public chains remain on the regulatory boundary. The CLARITY Act has not yet been finalized, and the specific question of stablecoin yield payments is among the issues that remain unresolved in further deliberations.

6. Why Institutions Choose Solana: The Technical Reasons

As the earlier cases show, global financial institutions with different aims did not choose Solana out of simple preference. Given that conservative finance puts capital into systems that actually work rather than into theoretical possibilities, it is because Solana met the technical requirements of institutional finance.

The Economics of Settlement: T+0 and Atomicity

The utility of Internet Capital Markets begins with the efficiency of settlement. The existing financial system has a physical time gap between trade execution and fund settlement, and clearinghouses and intermediaries have occupied a place to fill that gap.

On blockchain infrastructure, the asset transfer and the payment execute bundled into a single transaction. If one side’s condition is not met the whole trade is canceled, so counterparty performance risk is removed even without a clearinghouse.

Solana’s distinction lies in the conditions under which this structure works. Finality takes about 0.5 seconds, and the average fee is $0.0013 per transaction. If every cycle of setting and releasing collateral added several dollars in cost or took a day to settle, a leverage strategy would be eaten up by costs before it produced any return. Solana’s speed supports it.

Built-In Compliance: Programmable Compliance

The most sensitive area in institutional finance is compliance. A financial institution must keep strict control over the issuance, holding, and trading of assets. Where compliance in the existing blockchain environment was an after-the-fact measure dependent on external systems, Solana embeds this requirement directly into the token standard (Token-2022) and the protocol layer.